Dividend Reinvestment Plans (DRIPs) are an appealing way to put your financial future on auto-pilot.

Anything you can do to take emotions out of financial decisions is often a very good thing, and DRIPs can certainly help.

However, as with most things in the world of finance, the devil is in the details.

Let’s look at six specific tips that DRIP investors need to keep in mind to best maximize the chances of meeting their long-term financial goals.

Tip 1: Selecting the Right Kind of Stock to DRIP

The best thing about DRIP investing is that it’s a powerful tool that helps you to automate investing. Since the wealth and income compounding power of the stock market requires time and patience, DRIP investing can be thought of as the lazy (but smart) person’s road to riches.

DRIP investing is very much a hands-off approach, so it is best used for stocks that are of such high quality and low risk that you don’t need to pay all that much attention to them.

In other words, DRIP investing is best done with blue chip dividend stocks, those companies with predictable businesses and durable competitive advantages that have proven themselves to be excellent wealth compounders over time.

Popular places to start one’s search for these types of DRIP-friendly companies are the lists of dividend achievers (10+ consecutive years of dividend increases) dividend aristocrats (S&P 500 companies with 25+ consecutive years of rising dividends), and dividend kings (50+ consecutive years of dividend increases).

The key to these DRIP candidates is that most of these businesses have proven themselves over decades. Each has steady cash flows to support growing dividends and a shareholder-friendly corporate culture that is dedicated to rewarding investors for their patience over time – no matter what the economy or stock market is doing in the short-term.

With a diversified portfolio in place, you can feel comfortable reinvesting dividends back into these high quality businesses.

Tip 2: Maximizing the Tax Efficiency of DRIP Investing

DRIP investing won’t work if you don’t give your investments the time needed for the compounding power of rising dividend streams to work. That means you should only ever DRIP on shares owned in a long-term portfolio.

And keep in mind that you will have to pay taxes on DRIPed dividends. For most stocks (basic corporations) that means qualified dividends, which are taxed at the capital gains rate (0%, 15%, or 20%).

Owning these stocks in a tax-deferred account, such as an IRA or 401(k), can be an ideal solution to avoid these taxes until you start withdrawing required minimum distributions at the age of 70.5.

Also keep in mind that owning dividend stocks on a DRIP plan can be a great way to match up your time horizons. After all, any money saved in an IRA or 401(k) can’t be removed without paying hefty fines until the age of 59.5. This can help you keep your eye on the prize and maintain your long-term discipline.

However, when it comes to pass-through stocks such as REITs and MLPs, things can get a bit more complicated.

Tip 3: Making the Most of DRIPs

There are two major benefits that DRIP investing can give you and that investors need to make the most of.

First is the power of exponentially growing dividends to help you achieve strong long-term returns. For example, let’s consider Realty Income (O), which is one of the best high yield monthly dividend stocks.

Since its IPO, Realty Income has been growing its dividend by 4.7% per year, a rate which the company’s long growth runway should allow it to continue for the foreseeable future.

However, while the stock's relatively high yield near 5% is what initially attracts income investors to the stock, the true power of this dividend growth legend comes to those that hold for the long-term.

In fact, if you had bought Realty Income at the IPO, and never sold it, then your yield on cost (current dividend/cost basis) would exceed 30%.

Meanwhile, if you had set up a DRIP to accumulate additional shares over time, then the dividend stream you would now enjoy would be enough to cover your initial investment more than fivefold, every single year.

DRIP investing, with its emphasis on the long term, is a reasonable way to keep your focus on the horizon and avoid the temptation to time the market or let short-term volatility scare you out of an excellent investment.

The second big benefit to DRIP investing is that some stocks will actually allow you to buy discounted shares.

For example, Enterprise Products Partners (EPD), one of the best midstream pipeline MLPs, offers up to a 5% discount on its units for DRIP participants.

That is the equivalent of 5% free money, in the form of a growing number of units, each which has a growing income stream that can enhance your total returns over time.

Tip 4: Setting Up the Most Cost Effective Drips

There are two main ways to set up a DRIP, through your broker or individually by company through a transfer agent such as Computershare, which many businesses use for DRIP programs.

However, the downside to such an approach is that you can get hit by fees, both onetime and ongoing.

For example, as you can see below, using Computershare to set up a DRIP with Johnson & Johnson (J&J) involves numerous fees, including a very steep commission to sell your shares, $25 plus 12 cents per share.

Source: Computershare.com

Instead, one of the best ways to DRIP is to do it through a DRIP-friendly discount broker such as TradeKing, Scottrade, TD-Ameritrade, or Vanguard.

These brokers, in addition to fee-free DRIP programs, offer other cost saving (and performance boosting) features. For example:

TradeKing: $4.95 commissions, and you can set up your entire portfolio to be DRIPed (instead of each company individually)

TD-Ameritrade: $6.95 commissions and every form of stock, ETF, and mutual fund is eligible for a fee-free DRIP

Vanguard: $7 commission, except for Vanguard ETFs and mutual funds, which are commission free, no fee DRIP

Scottrade: $6.95 commissions, Flexible, fee-free DRIP that collects dividends in a pool and then reinvests them commission-free into any stocks you select (allows you to target the most undervalued companies)

Tip 5: DRIPing is Great, but There are Downsides

DRIP plans are essentially a way to automatically dollar cost average, meaning to invest a particular sum into a stock on a set schedule regardless of price.

While DRIPs are a great choice for most investors, if for no other reason than it continuously puts your capital to work in the market, that doesn’t mean they are necessarily an optimal means of investing.

That’s because valuation matters, and even high-quality blue chip dividend growth stocks can run up and become overheated. Blindly DRIPing every stock virtually guarantees you will be purchasing some shares of overvalued companies, which increases risk of underperformance.

Identifying fairly priced or even undervalued holdings to reinvest the dividends into instead would improve your portfolio’s long-term returns.

Of course, most people don’t have a portfolio so large that any individual holding, especially one with a relatively low yield, would generate enough dividends each quarter to make such a targeted approach practical.

Instead, you would need to pool your dividends for a time (say a month or a quarter) and then redeploy that cash into whatever appears to be the most undervalued at the time.

Investors pursuing such a strategy need to keep commission fees in mind, which is why such an approach will only work with a very low cost discount broker such as Robinhood (which offers unlimited commission free trades).

In addition, this optimal value dividend growth approach also requires investors to put in the time and energy to track individual companies and select which are the most undervalued, something most people are simply too busy to do.

Despite the allure of manually redirecting capital to the highest potential opportunities within my portfolio, my personal preference is to automatically reinvest dividends. It speeds up compounding, helps resist the temptation to time the market, and keeps a portfolio reasonably diversified over time.

It is also surprisingly hard to know which of your holdings will go on to be the best long-term performers, further raising the challenge of deciding where to actively reinvest dividends. I prefer to maintain an equally-weighted portfolio for that reason as well – if nothing else, it protects me from myself!

Tip 6: Remember the Most Important Rule of DRIP Investing

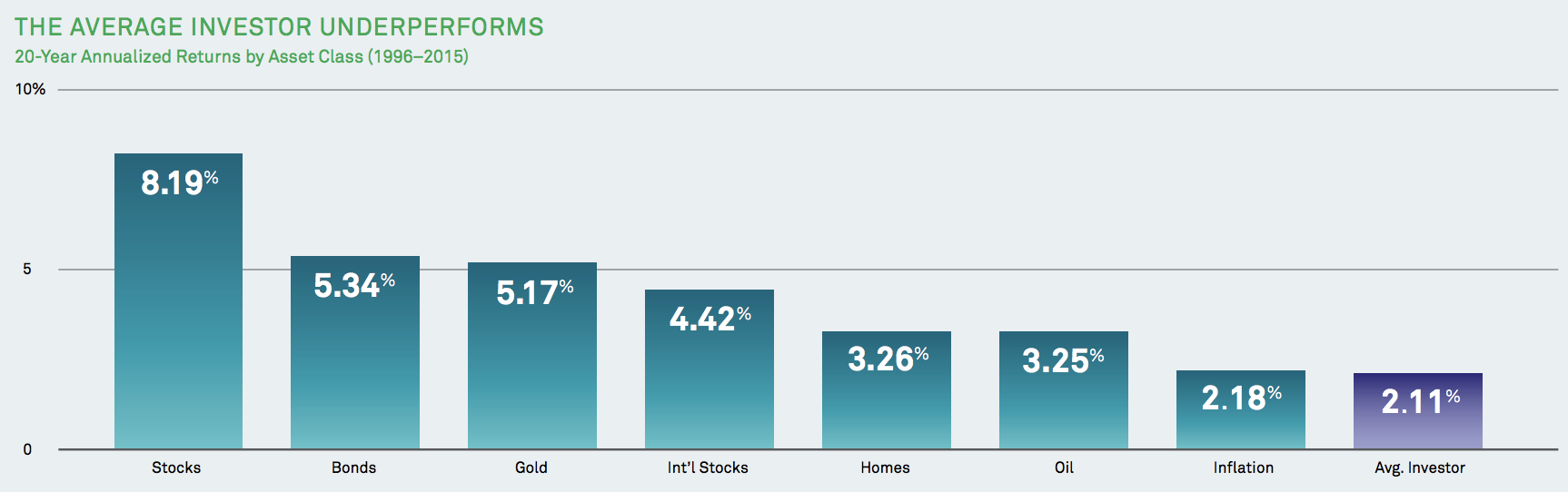

As you can see below, from 1996 through 2015 stocks returned 8.19% per year, yet the average investor woefully underperformed with an annual return of just 2.11%.

In today’s age of ever more popular and low-cost exchange traded funds (ETFs), what explains the fact that most people’s portfolios haven’t even kept up with inflation?

Source: Blackrock

The answer is that, even in today’s golden age of high-quality market data, human nature is still getting the better of us. Emotions are causing most people to overtrade, including with low-cost ETFs that track the broader market.

This is understandable because over the last few decades psychologists have found that humans brains are naturally hardwired to feel the pain of losing $1 twice as much as the pleasure of gaining a $1 (an evolutionary benefit that is now working against us in investing).

As a result, people naturally attempt to minimize losses and essentially attempt to time the market. However, market timing is the best way to ensure you waste the market’s compounding power.

Since DRIP investing is merely an automation tool that you generally set up through your broker, it can’t save you from yourself if you intentionally sabotage your results through market timing and overtrading.

In other words, DRIP investing only works over the long term, which is why, as with dividend growth investing in general, what matters isn’t market timing but time in the market.

DRIPs Can Be a Dividend Investor’s Best Friend…If Done Right

Today is a true golden age for retail investors because there has never been an easier or more cost effective way for people to save and grow their wealth and income over time.

That’s due to the plethora of quality research tools, low-cost brokers, and ways of automating one’s long-term investment strategy. However, at the end of the day DRIP investing is just a tool and not a guaranteed way to riches or success.

Like with all tools, what matters most is the person wielding it, which means learning to become disciplined and patient enough to allow the compounding power of the market to work for you.

That being said, if you can create a long-term investing plan that suits your needs, risk profile, and time horizon, and most importantly, stick to it in good times and bad, then DRIP investing can be one of the best ways to reach your financial goals.