Dividend Stocks vs. Bonds for Retirement Income: Which is Better?

Retirees have traditionally relied on bonds to generate income. Bonds are predictable, easier to plan around, and historically played a key role in reducing portfolio volatility.

But today, many investors wonder if high-quality dividend stocks can do more of the heavy lifting. Companies can raise their dividends over time, while bond payments stay fixed.

So which is better for retirement income: dividend stocks or bonds?

The answer is not one or the other. Each serves a different purpose.

Prefer to watch? Check out our YouTube video showing how dividends and bonds can work together so you never run out of money in retirement.

Why Bonds Have Been a Retirement Staple

Bonds are designed to deliver dependable income.

When you buy a bond, you receive scheduled interest payments and the return of your principal at maturity. That structure makes bonds useful for funding near-term spending because the cash flow is known in advance.

Bonds also tend to be less volatile than stocks, which can help retirees stay invested during market downturns.

The tradeoff is that bond income usually does not grow. Once you lock in a yield, it stays largely fixed.

The Challenge With Relying Only on Bonds

Retirement is not a 5- or 10-year problem. For many investors, it is a 25- to 30-year journey.

During that time, expenses rarely stay flat. Inflation gradually pushes the cost of living higher, while bond income remains unchanged.

That creates a gap between what your portfolio earns and what you need to withdraw.

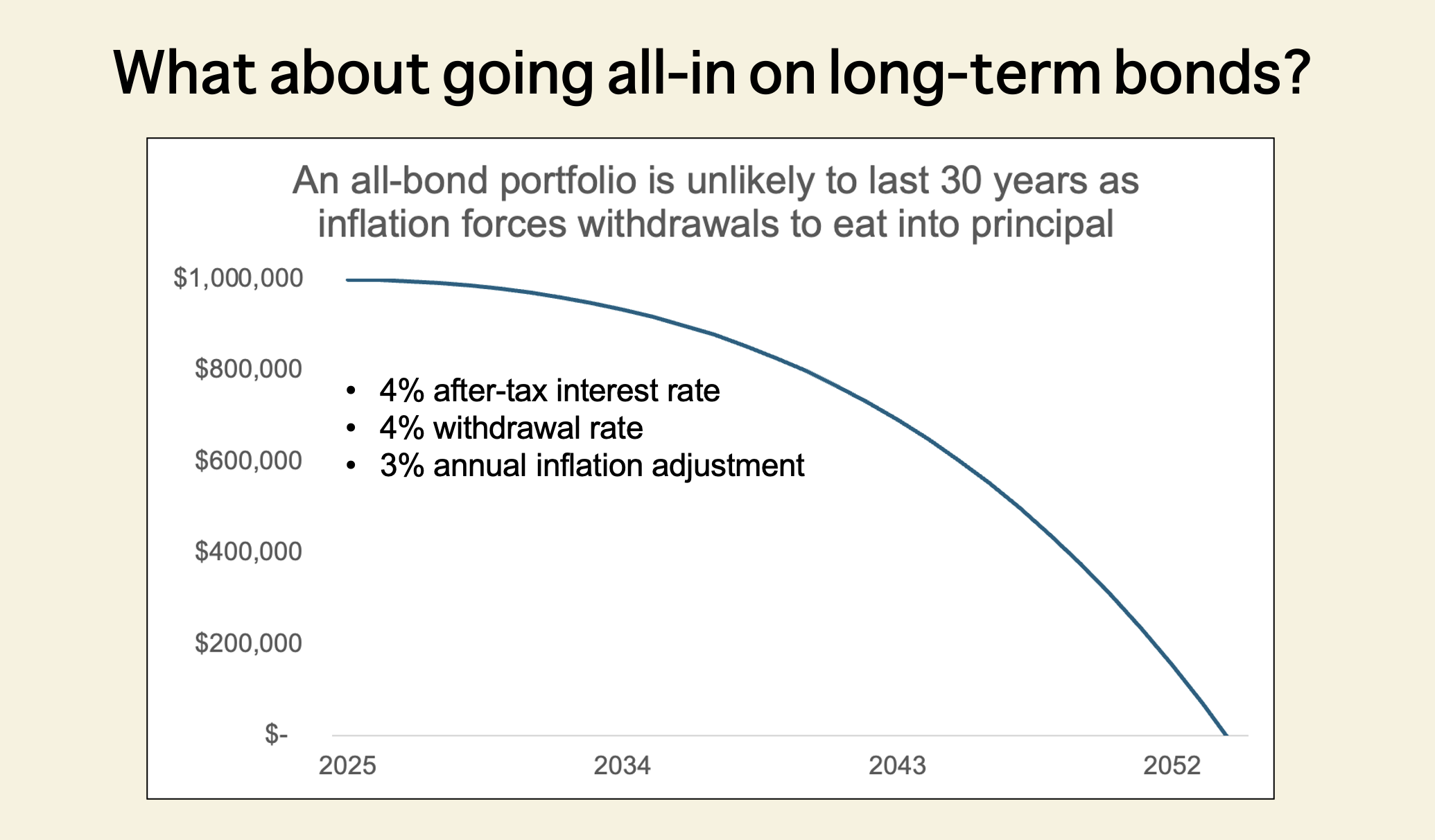

Below is a simple illustration of the challenge. This example assumes a 4% after-tax bond yield and a 4% withdrawal rate adjusted for 3% inflation.

Even though income initially matches withdrawals, inflation forces spending higher while bond income stays flat, eventually requiring investors to draw down principal.

Source: Simply Safe Dividends

Bonds can provide stability, but on their own they may struggle to maintain purchasing power over long retirements.

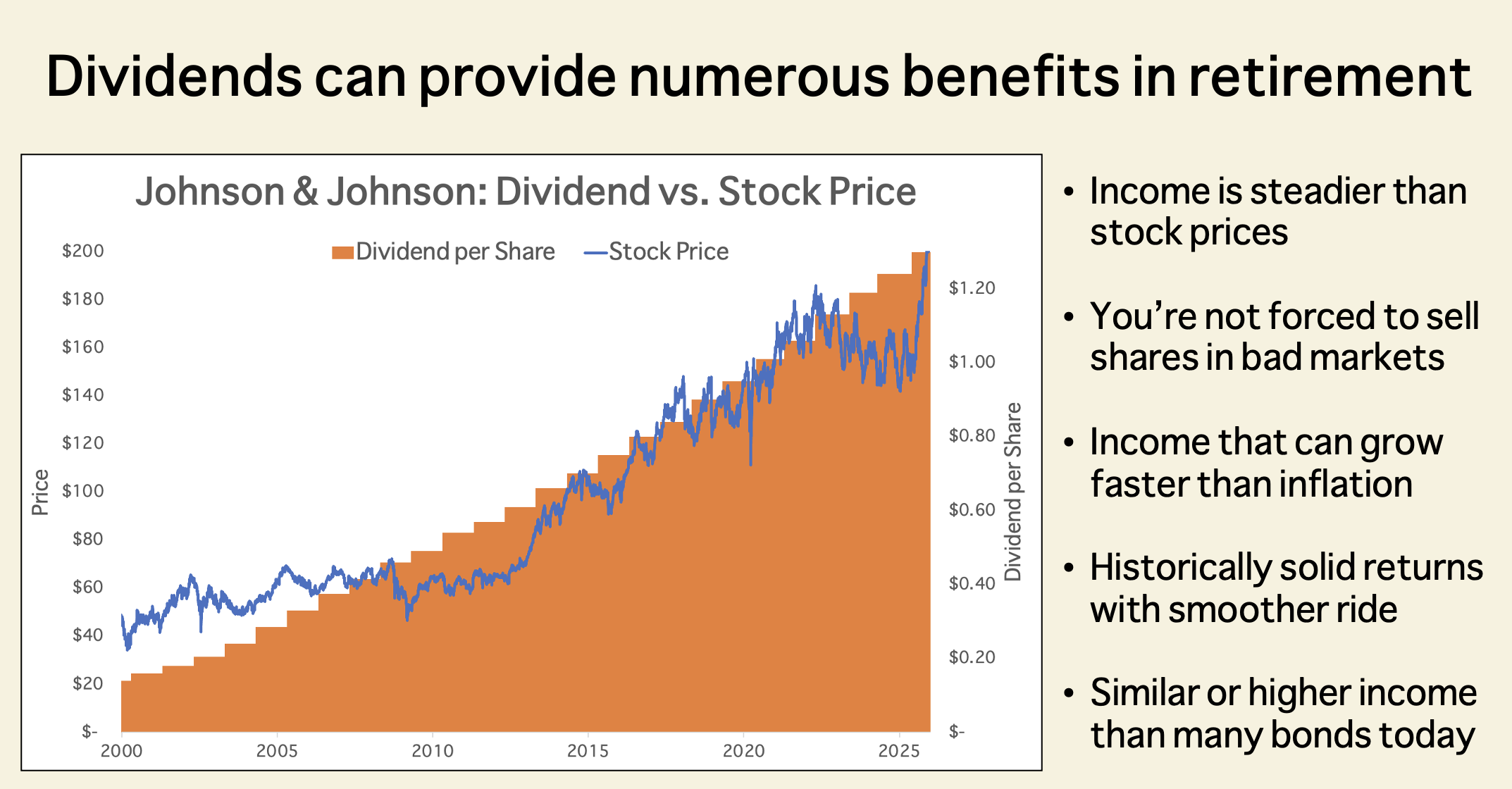

What Dividend Stocks Add

Dividend stocks represent ownership in businesses rather than a lending agreement. That difference matters because businesses can grow.

Companies with durable earnings and strong balance sheets often raise their dividends over time. Those increases can help offset inflation and support a rising income stream.

Dividend-paying stocks also participate in long-term economic growth, offering the potential for capital appreciation alongside income.

Source: Simply Safe Dividends

Of course, this comes with more short-term volatility. Stock prices move, and dividends are not guaranteed. That is why quality and diversification are essential.

The Stability vs. Growth Tradeoff

Many investors compare bonds and dividend stocks by looking at yield alone. But yield misses the bigger picture.

Bonds are designed to provide stability and fund spending in the near term. Dividend stocks are designed to help income grow over time.

Most retirees need both.

Why Many Retirement Portfolios Use a Mix

A portfolio invested only in bonds may have trouble keeping up with inflation. A portfolio invested only in dividend stocks can feel uncomfortable during market declines.

Blending the two allows bonds to act as a buffer while dividend-paying companies provide the long-term growth needed to sustain income.

This balance can help investors avoid selling stocks at the wrong time while still allowing their income stream to expand.

Avoid Reaching for Yield

One of the most common mistakes income investors make is chasing the highest yield available, whether in bonds or stocks.

Higher yields often come with higher risk, including weaker credit quality, greater sensitivity to economic cycles, or unsustainable payouts.

A retirement income strategy should focus first on reliability, not maximizing current income.

The Bottom Line

Dividend stocks and bonds are not competitors. They are complementary tools.

Bonds can provide stability and predictable cash flow, especially for near-term spending needs.

Dividend-paying companies can deliver rising income and help protect purchasing power over decades.

A thoughtful retirement portfolio typically includes both, combining the dependability of bonds with the long-term income growth of high-quality dividend stocks.

The goal is not to chase yield. It is to build an income stream that can endure across many different economic environments.