Investing in real estate investment trusts (REITs) can provide high dividend yields, steadily growing income, and exposure to many types of real estate without the headaches that come from owning rental property directly.

After reading this primer you will have a thorough grasp on REIT investing, including how REITs work, the different types of REITs, the most popular REIT stocks, the sector's historical performance, tax implications, and research tips.

What is a REIT?

REITs own income-producing real estate such as retail stores, apartments, industrial warehouses, office buildings, malls, and hotels.

Tenants sign lease agreements with REITs to use their properties. For example, Walgreens rents around 90% of its U.S. pharmacy stores, and FedEx leases many of its warehouses. Renting ties up less capital for these tenants compared to owning their own properties.

REITs collect rent payments from their tenants over a specified period, ranging from month-to-month contracts for self-storage to 20-plus year lease terms for logistics facilities.

As long as a REIT's properties remain occupied and tenants continue paying their rent, this business model generates the type of predictable, recurring cash flow valued in retirement.

How to Invest in REITs

Publicly traded REITs are listed and traded just like any other stock on exchanges such as the NYSE. Investing in REITs is as simple as punching in a REIT's ticker symbol in your brokerage account and buying the stock.

Non-listed and private REITs exist outside of stock exchanges. Most investors should ignore these REITs because they are hard to value and trade, with limited liquidity, no market price readily available, high fees, and management structures that can create conflicts of interest.

That said, investing in publicly traded REITs still requires an understanding of how they differ from regular corporations.

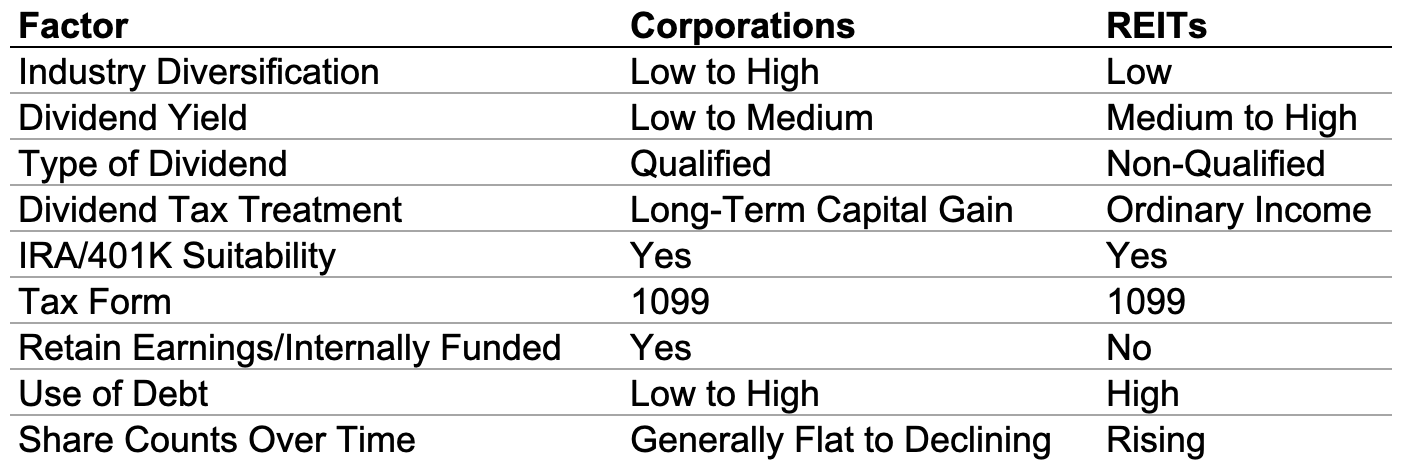

REITs Versus Regular Corporations

The main differences between regular dividend-paying corporations and REITs are summarized in the table below.

Source: Simply Safe Dividends

Like corporations, owning shares in a REIT means owning a stake in a company.

The main difference is that REITs are legally required to annually distribute at least 90% of their taxable income in the form of dividends to shareholders.

This supports larger dividends but also means REITs retain little cash flow.

To fund their capital-intensive growth (i.e. property acquisitions), REITs therefore rely on raising external debt and equity capital from investors.

As a result, most REITs maintain high debt levels and have rising share counts over time. Management must find properties that produce higher cash yields than the REIT's cost of debt and equity capital in order to create value.

The unique structure of REITs carries tax consequences for investors, too.

How are REITs Taxed?

By distributing at least 90% of their taxable income as dividends, REITs pass through their corporate tax burden to shareholders rather than pay federal income taxes themselves.

As a result, REIT investors receive non-qualified dividends taxed as ordinary income rather than the lower long-term capital gains rate that most regular corporate dividends enjoy.

A portion of REIT dividends may be a capital gains distribution taxed at a lower rate or classified as a return of capital, which is not taxed and instead reduces an investor's cost basis.

However, in most cases, non-qualified dividends will account for the majority of a REIT's payout as discussed in our review of REIT taxation.

Investors generally prefer to own REIT shares in a tax-sheltered account (e.g. IRA) to avoid the higher tax rate applied to non-qualified dividends.

Otherwise, at tax time REIT investors will receive a form 1099 (no K-1 is issued).

To maintain their pass-through tax status, REITs must adhere to additional federal tax law requirements regarding the composition of their income and assets, including:

Investing at least 75% of assets in qualifying real estate

Receiving at least 75% of income from rent, interest, and other qualifying sources

Essentially, companies that elect to be taxed as a REIT must be driven by ownership of cash-producing properties.

Businesses rarely change their tax elections, so investors do not need to worry about monitoring these guidelines for REITs they invest in.

Types of REITs

Over 200 publicly traded REITs exist. Some REITs diversify their portfolios across many types of properties, but most concentrate on just one or two industries.

This makes it easy for investors to bet on certain types of real estate they like.

For example, believers in the continued growth of internet traffic could buy shares in a REIT focused on data centers, such as Digital Realty (DLR).

And investors bullish on e-commerce sales rising strongly in the years ahead could target REITs that own warehouses used by retailers to store products before they reach end customers. STAG Industrial (STAG) is one example.

Here is a list of the most common types of REITs:

Offices

Industrial Facilities

Shopping Centers

Malls

Single Family Homes

Apartments

Medical Buildings

Data Centers

Student Housing

Senior Housing

Hotels

Freestanding Retail Stores

Storage

Timber

Infrastructure

Note that there is also a separate class of REITs known as mortgage REITs.

These stocks, known as mREITs, are unsuitable for conservative investors seeking steady incomes because their business models are very sensitive to interest rate fluctuations rather than stable rental income.

mREITs primarily own mortgage-backed securities rather than physical properties. Nearly all mREITs have histories riddled with multiple dividend cuts, reflecting the challenges of running a highly levered business with aggressive payout ratios and volatile net investment income.

Most Popular REIT Stocks

Focusing on traditional property-based REITs, which account for the bulk of the sector, here is a look at 30 of the most popular REIT stocks to invest in.

These are some of the best REITs for beginners because they generally have time-tested operations, a diversified mix of properties and tenants, long track records of paying reliable dividends, and prudent financial policies which earn most of them healthy Dividend Safety Scores™.Many of these REITs are popular with investors because they have historically delivered solid long-term returns along with the broader real estate sector.

Historical Performance of REITs

A law signed in 1960 by President Eisenhower enabled the creation of America's first REITs. But the sector did not really take off until President Reagan signed the Tax Reform Act of 1986, which gave REITs greater flexibility to manage their own operations.

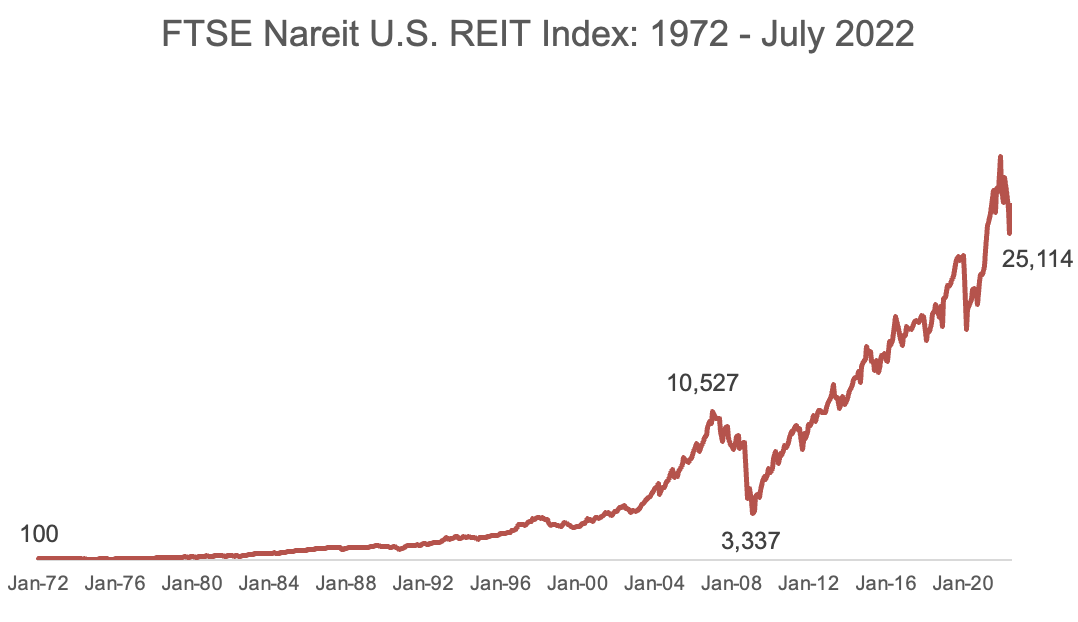

Many of today's largest REITs went public in the 1990s, but REIT performance data is available going back to 1972 thanks to the work of Nareit, the trade association for REITs, and benchmark provider FTSE.

These two organizations created the FTSE Nareit U.S. Real Estate Index Series, which "contains all tax-qualified REITs with more than 50% of total assets in qualifying real estate assets other than mortgages secured by real property that also meet minimum size and liquidity criteria."

The index contains around 150 publicly listed U.S. REITs (mREITs are excluded) spread across 16 property subsectors, none exceeding 20% of the index.

From 1972 through July 2022, the REIT index recorded an annual total return of 11.6%, topping the S&P 500's 10.4% annual return over the same period.

Starting from 1995 instead, when more REITs existed, the index compounded by 10.5% annually, edging out the S&P 500's annualized return near 10%.

Source: Nareit, Simply Safe Dividends

That said, REITs can exhibit higher volatility when the tide goes out due to their high payout ratios and dependence on fickle capital markets for funding.

During the 2007-09 financial crisis, the REIT index plunged by 68%. And from May 2008 through March 2009, approximately 30% of all REITs suspended, cut, or switched to paying part of their dividend in company stock, according to The Wall Street Journal.

Overall, REITs have historically delivered similar long-term total returns to the broader stock market but can experience sharper downturns.

Studying a REIT's business model can help investors focus on owning REITs best positioned to thrive over a full economic cycle.

How to Analyze REITs

Here is a basic investment checklist we follow when evaluating REITs:

Industry exposure: Which industries does the REIT focus on? Do these seem like markets that will experience higher demand over time?

Tenant concentration: How many properties does the REIT own? How big are the largest tenants as a percentage of rental revenue? More diversification is better. Do these seem like profitable, creditworthy tenants capable of meeting their rent obligations during a downturn?

Property quality: Are most of the REIT's properties "Class A" (newer, higher quality, located in good areas)? Has occupancy remained high and stable over time, reflecting solid demand? Higher quality properties are less risky.

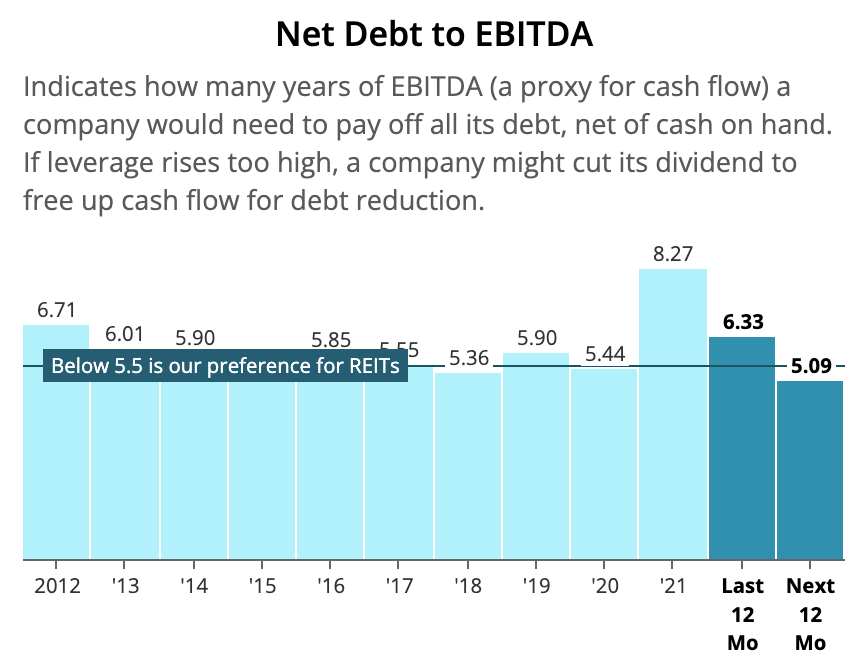

Balance sheet health: REITs generally have high leverage, but some are more aggressive than others. Does the REIT have an investment-grade credit rating? Has leverage increased significantly in recent years? Maintaining reliable access to debt financing is important in this capital-intensive sector.

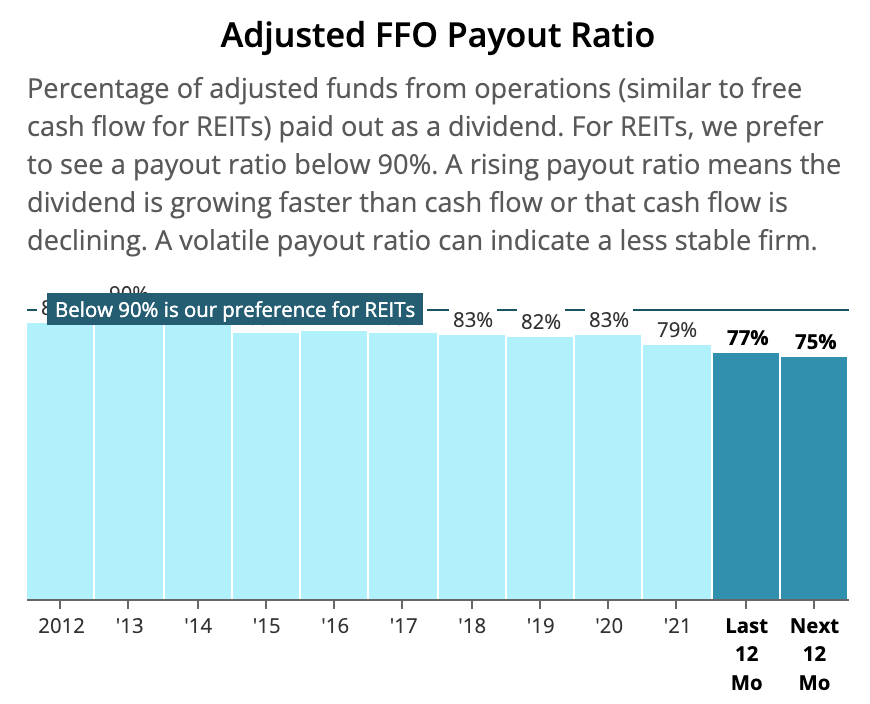

Dividend coverage: Has adjusted funds from operations (AFFO), a metric similar to free cash flow for REITs, consistently covered the dividend? We prefer an AFFO payout ratio below 90% for most REITs. Higher payout ratios leave a smaller margin of safety to protect the dividend in the event of any dips in cash flow (due to lease expirations, tenant defaults, etc).

Dividend growth track record: Has the REIT delivered stable dividends over time? If dividend cuts have occurred, what drove them? How fast has the dividend grown over time? A high-yielding REIT with minimal to no dividend growth may not be an appealing long-term investment.

Using Realty Income (O) as an example, the retail REIT was founded in 1969 and now owns thousands of freestanding, single-tenant properties leased under long-term contracts to hundreds of tenants operating in dozens of industries.

Retail generates most of Realty Income's rental revenue, with industrial warehouses accounting for most of the remainder.

Parts of brick-and-mortar retail face pressure from online shopping. But Realty Income mitigates this risk by focusing on tenants with a service, non-discretionary, or low price point element to their business.

Coupled with premium locations and an extremely diversified portfolio of tenants and industries (none greater than 5% and 11% of rental revenue, respectively), Realty Income's occupancy rate has never fallen below 96%. This seems like a durable business with in-demand properties.

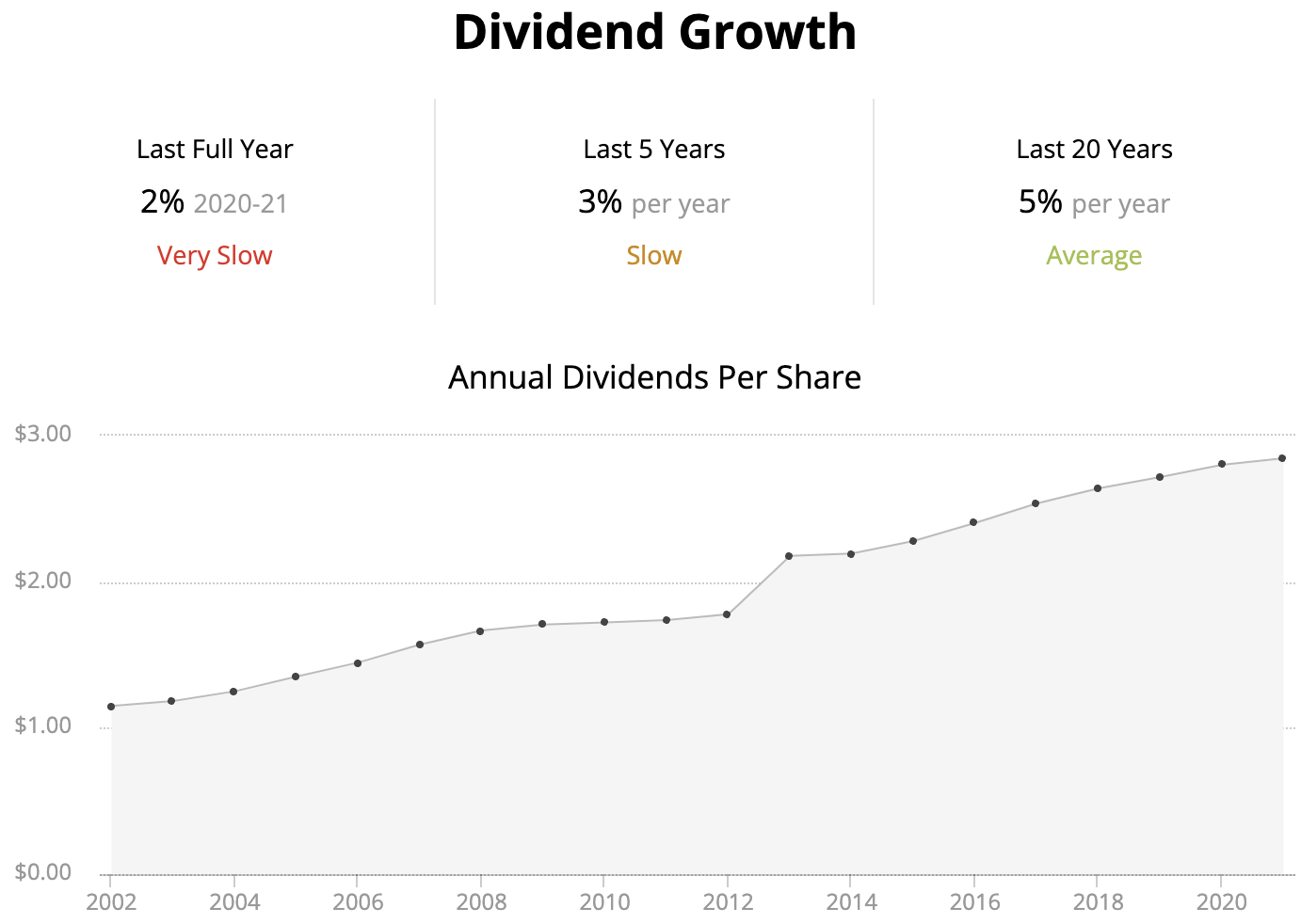

From a financial perspective, our website Simply Safe Dividends makes it easy to evaluate a REIT's dividend coverage by showing a company's key fundamental metrics, including AFFO payout ratios over the past decade.

Realty Income's AFFO payout ratio has remained at a healthy level for many years, indicating a sustainable dividend based on the REIT's ongoing cash flow.

Source: Simply Safe Dividends

The company's balance sheet remains in good shape as well. Realty Income's leverage ratio (net debt to EBITDA) sits about in line with its moderate historical levels, earning the firm an A- credit rating from Standard & Poor's.

Source: Simply Safe Dividends

All of these factors culminate in an outstanding dividend track record. Realty Income has paid uninterrupted dividends since the firm's founding and raised its payout each year since going public in 1994.

While the company's pace of dividend growth has decelerated over the last 20 years, Realty Income seems like a good bet to continue delivering low single-digit dividend increases in good times and bad.

Source: Simply Safe Dividends

Running through an investment checklist like we did with Realty can help investors identify REITs with stronger fundamental outlooks and safer dividends.

However, the real estate sector still possesses a handful of risks investors should be comfortable with.

Key Risks to Investing in REITs

While some REITs are riskier than others, most companies in this sector have at least some sensitivity to the factors below.

Interest rate sensitivity: Rising rates can increase a REIT's cost of capital and reduce its growth potential by pushing up borrowing costs and causing bond-like REIT stocks (e.g. triple net lease REITs) to sell off. However, REITs have been positively and negatively correlated with interest rates over different periods of time. No hard and fast rules exist.

High leverage: Most REITs rely heavily on issuing debt to fund their capital-intensive businesses. Leverage magnifies returns and increases risk, especially during downturns.

Dependence on capital markets: REITs depend on issuing debt and equity to run their businesses and execute their growth plans. If access to capital gets shut off, perhaps due to a deep recession, REITs may be more likely to preserve capital by cutting their dividends.

Concentrated operations: REITs often specialize in one type of property. This lack of diversification can result in greater volatility as an industry's outlook changes, for better or worse.

Investors can mitigate some of these risks by maintaining a well-diversified portfolio that includes many different sectors and types of businesses.

The Pros and Cons of REIT Investing

REITs offer a number of advantages and disadvantages to consider.

Reasons not to invest in REITs include:

Non-qualified dividends taxed as ordinary income

Higher interest rate sensitivity

Generally weaker dividend safety due to high payout ratios and leverage

Greater downside potential during recessions

Diversification (the Real Estate sector accounts for just 3% of the S&P 500)

While some of those factors are valid concerns, investors can mitigate most of these risks by focusing on the fundamentally strongest REITs, owning REITs in tax-advantaged accounts, and maintaining diversified portfolios.

In return, investing in REITs can provide numerous benefits:

High dividend yields backed by recurring rental income

Exposure to real property as an inflation hedge

Competitive long-term annualized returns

Diversification as REITs are only moderately correlated with other sectors

Overall, REITs can make a solid addition for many dividend portfolios. Investors just need to be selective in the types of REITs they own, understand the risks, and remain properly diversified.