Master limited partnerships risks are increasingly in focus by dividend investors following the oil price cash and concerns over rising interest rates.

The sector has attracted income investors thanks to its relatively high dividend yields, historically stable cash flows, and perceived protection from swings in commodity prices.

However, with many energy master limited partnerships having announced distribution cuts, it’s time for investors to revisit the topic of master limited partnerships risks.

We identified a handful of the biggest risks facing master limited partnerships (MLPs) below.

Master Limited Partnerships Risks

1. MLPs have underperformed significantly in the past and risk oversupply resulting from “free” money.

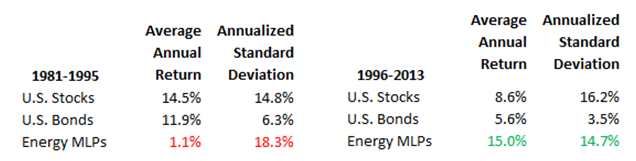

As seen below, energy MLPs turned in terrible performance from 1981 through 1995, trailing the market by over 13% per year while recording much higher volatility. Many of the original energy and real estate MLPs left the market due to challenging economic conditions.

The tax advantages and higher yields of MLPs do not guarantee their future total return performance, and MLPs are coming off of an extremely strong performance run from 1996-2013 in which they nearly doubled the market’s annualized return. It’s easy for investors to forget about master limited partnerships risks during bull markets.

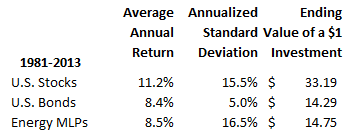

This table shows the performance of energy MLPs relative to U.S. stocks and bonds from 1981 through 2013. MLPs underperformed U.S. stocks by nearly 3% per year with higher price volatility.

Source: Fidelity

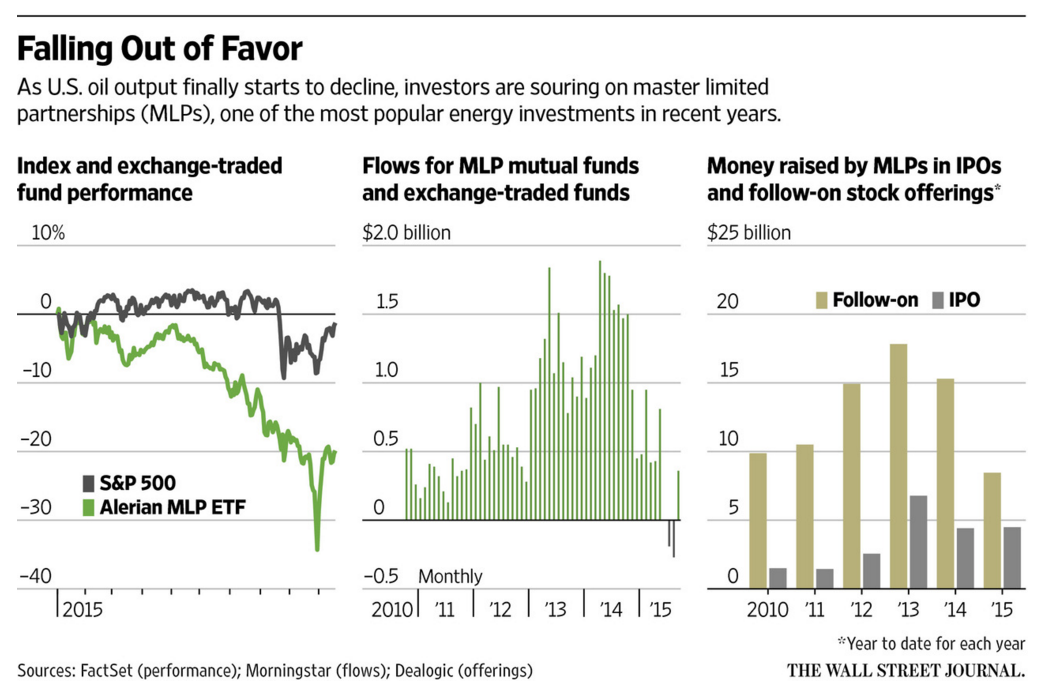

Energy infrastructure has been a booming business. As seen below, courtesy of the Wall Street Journal, MLPs raised substantial capital in IPOs and follow-on stock offerings from 2010 through 2015, and MLP mutual funds and ETFs enjoyed massive inflows:

Source: Wall Street Journal

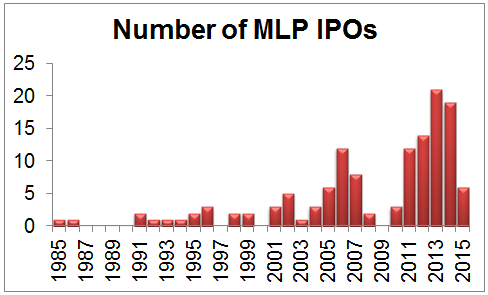

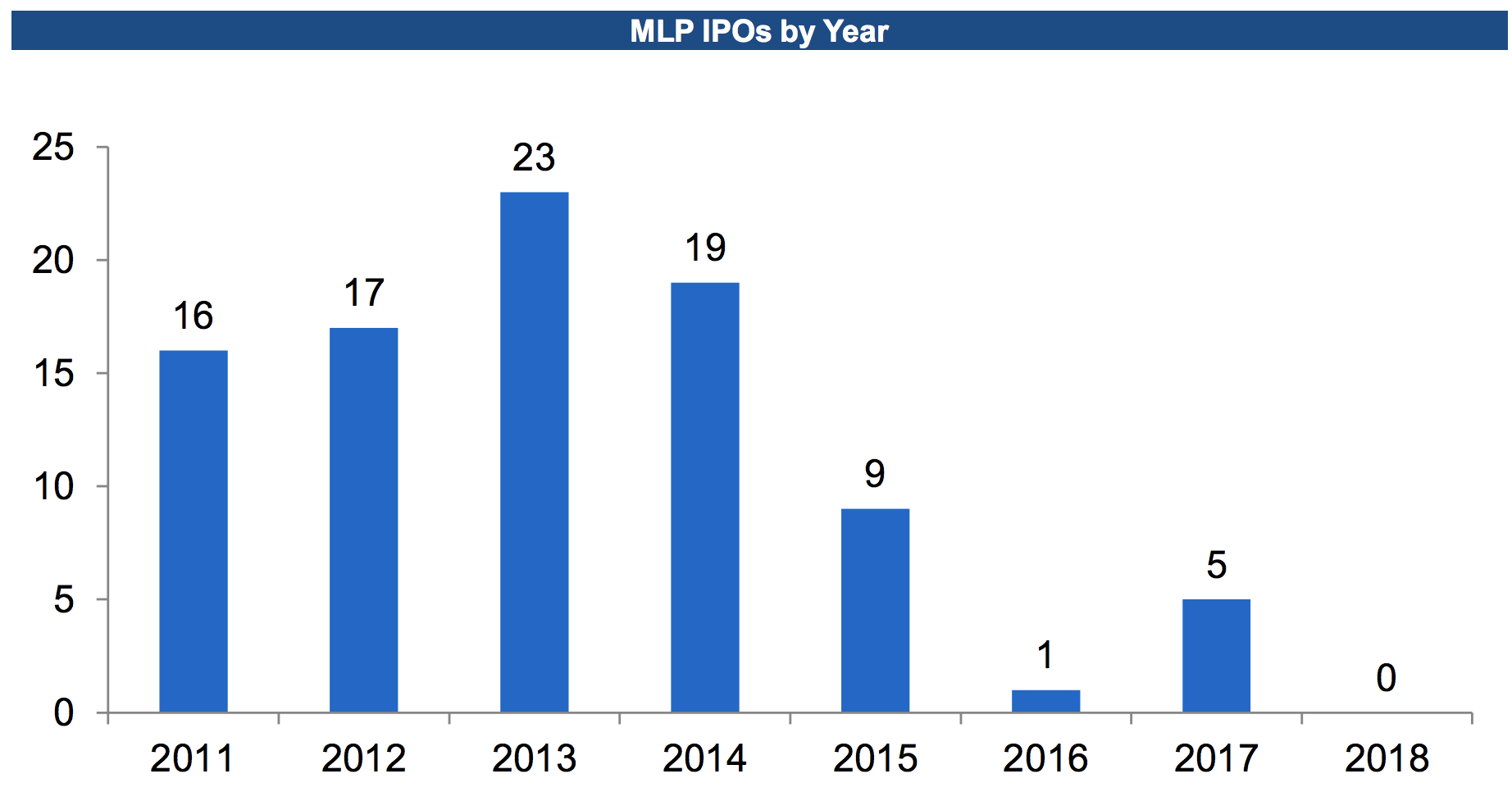

Looking even further back highlights how extreme the past decade has been for MLPs. With low interest rates, yield-starved investors, rising oil & gas production, and new shale plays emerging by the day to drive infrastructure needs, it’s no surprise that there was a record number of MLP IPOs over the last five years:

Source: Latham & Watkins LLP

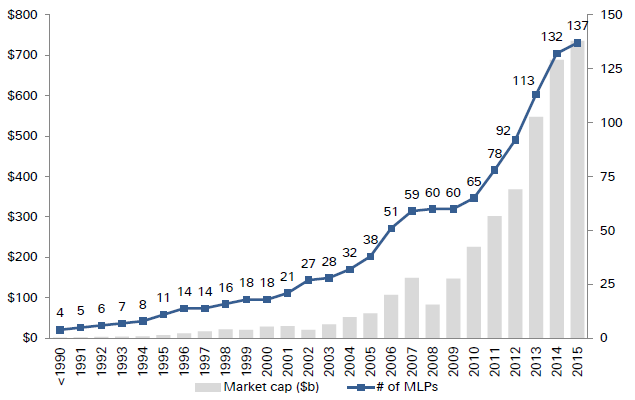

The following chart from Deutsche Bank further highlights the major jump in MLPs over the last decade, with the number of MLPs nearly tripling from 2005 through 2015:

Source: Bloomberg, Deutsche Bank

Investing is part art, part science. The “art” investors would look at this data and suggest that the decade-long run MLPs have enjoyed is a sign they are possibly overvalued and ready for a pullback.

These investors express concern that the amount of “free money” (i.e. infrastructure investments were easily financed by investors hungry for yield) thrown at the energy industry for this long has created a distortion that is still in the early days of correcting.

Perhaps many of the wells drilled by exploration and production companies over the last five years will prove to be uneconomic, reducing the need for pipeline infrastructure that was put in place in those regions.

In other words, there could be too much pipeline capacity chasing falling production in many shale basins that were once booming. Distressed exploration and production companies are announcing more cost cuts and layoffs by the day. Renegotiating their existing contracts with MLPs at lower rates could be a logical action to help them survive.

As sentiment has soured on the MLP model for a number of reasons (oil price crash, distribution cuts, tax code changes, unsustainable distribution growth targets), the number of IPO listings has tumbled.

Source: MLP and Energy Infrastructure Conference

Despite the near-term gloom, MLP bulls believe that new low-cost extraction technologies such as fracking will result in rising energy production and demand for more energy infrastructure in North America over the long term, providing a long runway for MLPs to remain quality income investments. Only time will tell.

2. Dependence on capital markets for cash distribution growth.

While MLPs are not required to distribute most of their cash flow by law, almost all of their partnership agreements call for all “available cash on hand” to be distributed to unitholders. With no income tax at the partnership level and almost all cash being paid out, it’s no wonder why MLPs offer such high dividend yields.

However, these benefits come at a cost. Unlike C-corps, which increase their dividends primarily as a result of earnings growth and retain internally-generated cash flow for growth investments, most MLPs need to borrow money or issue new units to continue growing their distributable cash flows.

When times were good, MLPs enjoyed easy access to capital because they almost looked like bonds with their stable cash flows and clear returns. Their high yields were also an easy sell to yield-starved investors.

Sentiment has clearly changed with the plunge in oil prices. Paying out almost all of your cash flow as a distribution and straining your balance sheet in this environment could prove to be dangerous.

To further complicate things, calculating a payout ratio is a bit of an art with MLPs. Companies list their coverage ratio, which measures how much distributable cash flow the business generates compared to what it pays out.

Distributable cash flow is defined as net earnings plus depreciation, minus maintenance capital expenditures. A coverage ratio of 1.1x indicates that the company paid out distributions of $1.00 per share for every $1.10 in distributable cash flow it earned. Higher ratios are better.

The complicating factor is that the company makes critical assumptions about its “maintenance capital expenditures” to calculate distributable cash flow. There is no standard definition of maintenance capex between firms, and with long-lived assets such as pipelines, maintenance capex is even harder to define. In other words, distributable cash flow calculations have some wiggle room and the potential to be misleading.

The return MLPs will achieve on their growth capex is less certain in today’s volatile oil & gas price environment. If MLPs cut back on growth spending, cash distributions could take a hit and possibly cause investors to re-rate the space even lower.

There are many moving parts here, so it’s hard to say what could realistically happen. However, negative free cash flow, heavy dependence on capital markets, energy production volumes that could be peaking (at least in the near term), and distributabions that could be frozen or reduced are reasons to do all of your homework before investing in MLPs.

3. High debt loads increase financing risk and make the asset class more sensitive to rising rates.

Most MLPs maintain substantial debt loads and, should interest rates start to rise, could see their cost of capital increase. If capital markets were to freeze up again like in 2008, MLPs would likely display significant volatility, just as they did during the financial crisis.

This would be less of a concern if the energy market backdrop was more favorable, but many exploration and production companies (MLPs’ customers) and banks (MLPs’ financiers) are cutting back activity and lending.

4. Take-or-pay or other contracts don’t guarantee safety during a commodity price slump.

Many income investors like MLPs because of the perceived safety provided by take-or-pay contracts (e.g. customers pay for renting space in a pipeline regardless of whether they use it or not) and fee-based cash flow (based on volume, not price).

However, when oil & gas prices plunge and remain low like they have in recent years, there is only so much weaker producers can do to honor their contracts with energy MLPs. Some are unable to meet the agreements, have to renegotiate, or go bankrupt.

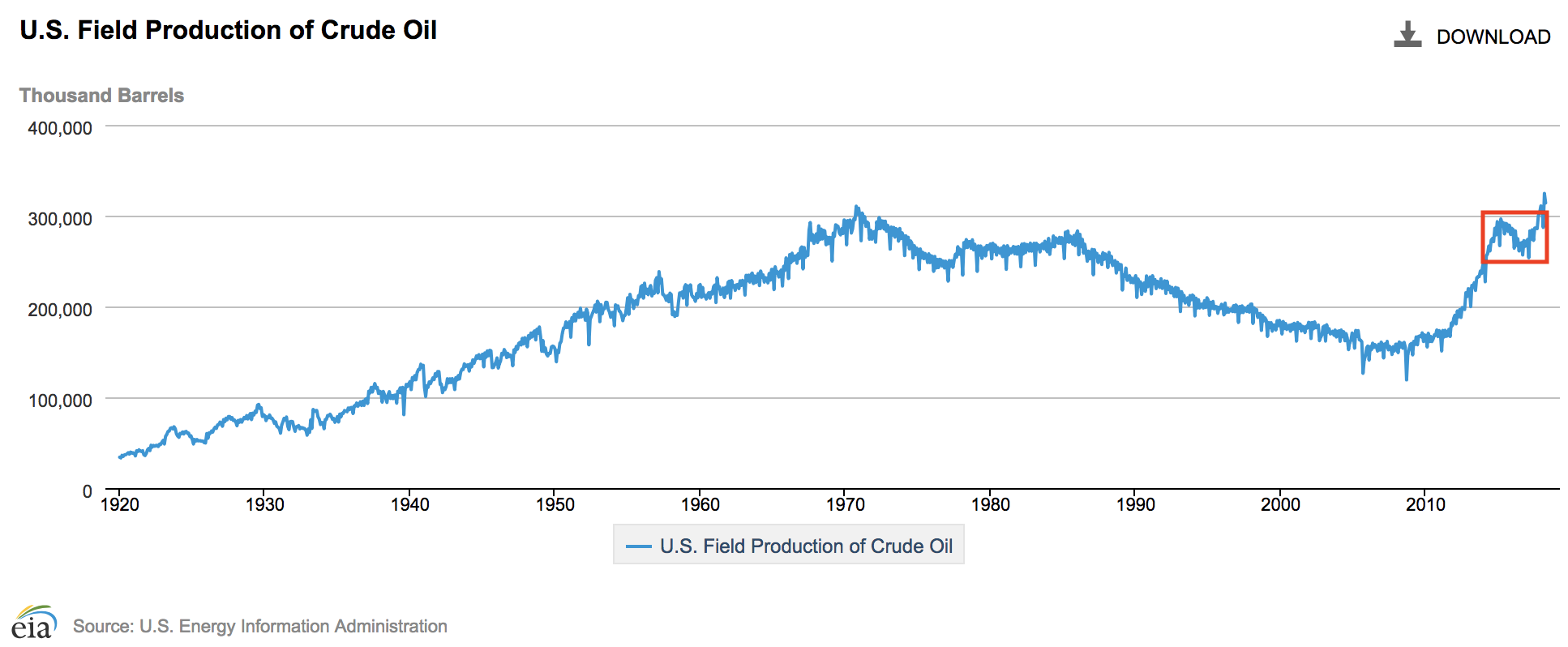

In 2015 as U.S. oil production started to decline in response to lower oil prices, more investors began questioning the ability of MLPs to keep up their steady growth of cash distribution payouts, which has been a key input in valuing MLPs. The following chart shows U.S. oil production dating back to 1920. You can see the production dip in 2010 (outlined in red), but fortunately conditions have since improved.

5. Distribution growth is dependent upon favorable regulation.

MLPs are highly regulated businesses. For example, many pipelines are regulated by the Federal Energy Regulatory Commission (FERC), which has the ability to set rates. Any change in regulations by the FERC could significantly impact cash flows and the rate of an MLP’s distribution growth.

The FERC’s job is to ensure that companies charge “just and reasonable” fees and that exploration and production companies have fair access to transport products. Rates are usually set on a cost-of-service basis, factoring in capital and maintenance costs to keep the infrastructure running.

While regulations have generally been a good thing for MLPs by providing clear returns on their infrastructure investments, they are a major uncontrollable factor the businesses depend on.

For example, in March 2018, FERC revised a 2005 tax policy to no longer allow interstate pipelines owned by MLPs to recover an income tax allowance in the cost of service customers previously had to pay for.

As pass-through entities, MLPs do not pay any federal taxes. In other words, they were essentially getting a double benefit on taxes, which is now being taken away.

The policy revision only affects interstate oil and gas pipelines and will not go into effect for oil pipelines until 2020 since they are regulated differently.

Many MLPs saw their unit prices fall as much as 10% on the announcement. The degree of impact from this regulatory change really depends on the pipeline being evaluated – Is it an interstate pipeline? Are its rates regulated or negotiated with customers?

Either way, this news will likely result in less revenue and cash flow for most MLPs with regulated interstate pipelines. This could cause some of their share prices and credit ratings to come under some pressure, raising their cost of capital and adding more uncertainty to their long-term growth profiles.

A higher cost of capital can also impact the profitability of projects and, if extreme enough in some cases, cause the distribution to come under pressure if management needs to retain more internally generated cash flow to fund investments and protect the company’s credit rating.

6. Organizational and financial complexity requires an extra level of research and understanding.

An academic study of 119 MLP contractual agreements found that partnerships with agreements unfavorable to investors tend to have higher proportions of insider equity ownership compared to those with agreements more protective of investors.

It’s very important to understand the agreements in place for the MLPs you are considering investing in because you most likely will not have voting rights.

Investors need to thoroughly understand an MLP’s “incentive distribution rights,” which provide the general partner running the MLP with a disproportionate share of the cash flow as cash distributions increase. When times are good and production volumes are growing, investors don’t mind these clauses.

However, when growth slows, investors are less willing to provide an MLP with shares upon realizing its high cost of capital because of the incentive distribution rights.

An MLP’s organizational and legal structure should also be thoroughly reviewed before investing. Many of these investments are “too hard” for us to get comfortable with.

7. Investing primarily in MLPs can decrease the benefits of portfolio diversification.

This risk should come as no surprise. The majority of MLPs are exposed to the energy sector, so a portfolio that is overweight MLPs will be overweight energy.

As we have seen in recent years, some MLPs have embedded commodity price risk and remain sensitive to the financial health of major players in the sector (their share prices move with energy prices, even if their underlying businesses are not tied to oil & gas prices).

8. Change in the tax code could hurt the performance of all MLPs.

Dividend investors should also be aware of potential legislative risk against the industry. Tax reform and deficit reduction are always hot topics, and in the future politicians could attempt to alter income tax rates, capital gains, dividend rates, and the treatment of pass-through entities.

MLPs operating outside of real estate and natural resources industries have the greatest amount of regulatory risk. For example, AllianceBernstein (AB) and Blackstone Group (BX) operate in the financial sector and use the MLP structure solely as a tax shield. The government seems more likely to scrutinize these companies and consider disallowing their favorable tax treatment.

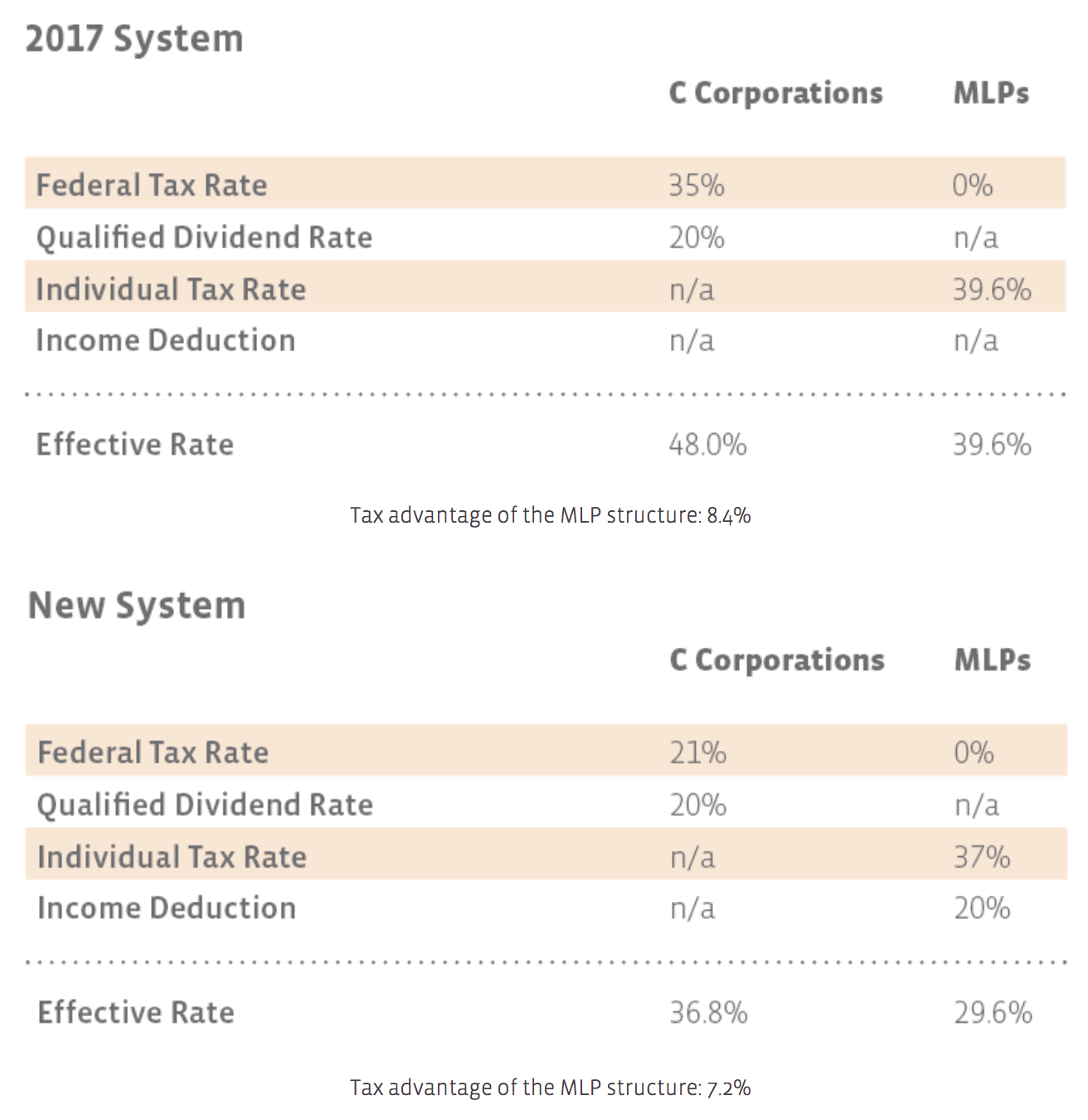

Most recently, the 2017 tax reform act lowered the the federal tax rate on corporations from 35% to 21%. While MLPs also benefited from a new 20% pass-through deduction, the new law reduced their relative tax advantage compared to corporations.

Source: Alerian

Furthermore, due to a bear market in MLPs since the oil crash began in mid-2014 and the FERC tax policy revision in March 2018, many MLPs have now adapted their business models.

Specifically, they are simplifying their structure to either eliminate incentive distribution rights (thus lowering their cost of capital and making future growth more profitable), acquire their GPs, or have the GP buy out the MLP.

If the GP is a C-corp, then this MLP buyout is a taxable event. Changes in regulations and market conditions can clearly have significant implications for MLP investors.

Conclusion

Booms and busts can take place over very long periods of time. Energy MLPs have performed extremely well for nearly 20 years and benefited from easy financing and investors’ appetite for yield following the financial crisis.

The fallout in energy prices woke up income investors to the embedded commodity price risk in many of these stocks that were otherwise generating stable cash flows and promising fast distribution growth.

However, if sustained low oil prices were to erode demand for infrastructure and regulatory changes reduce the appeal of the MLP model, the long-term outlook for MLPs could significantly darken.

There could be a time, perhaps not too far off, when the MLP industry offers an extremely attractive risk/reward ratio. However, we could see many distribution cuts and even greater investor pessimism first due to the duration and magnitude of the boom leading up to the oil price crash.

We do not own any MLPs in the dividend portfolios in our newsletter given our concerns over distribution cuts and the energy shakeout, but we will continue to watch the space closely.