Over the past decade, as interest rates have essentially been pegged near zero, income-hungry investors have been attracted to higher-yielding equity classes such as: Master Limited Partnerships, Business Development Companies, and Real Estate Investment Trusts.

One class of REITs in particular, mortgage REITs, has been especially popular thanks to its sky-high dividends, which often yield as much as 10% to 15%.

However, of all the various high-yield, pass-through equity classes, in which the company doesn’t pay taxes as long as it distributes almost all taxable net income to investors, mortgage REITs are by far the hardest to invest in successfully.

Let’s take a look at why this equity class, while potentially alluring for some high-risk, hands-on investors, is also the riskiest way to reach for ultra-high-yields in this time of historically low interest rates.

What are Mortgage REITs?

Both equity REITs, or eREITs (which own properties and generate cash flow from rent), and mortgage REITs, or mREITs, were created in 1960 by Congress. The goal was to create: “greater diversification of investment,” “expert investment counsel,” and the means of “collectively financing projects which the investors could not undertake singly.”

In other words, to create a class of equities that could easily raise money from investors to help finance real estate investment, both residential and commercial. And like eREITs, which is what most dividend investors are familiar with, mortgage REITs also are legally required to pay out a minimum of 90% of profits as non-qualified dividends, in order to avoid paying taxes at a company level.

However, the difference between the two types of REITs is in their business models, which are as different as night and day. eREITs function as aggregators of properties, and mostly generate cash flow through collecting rent. mREITs on the other hand, usually own no actual properties but merely function as a type of closed-end, private equity fund (investors can only sell shares, not take money out of the fund).

Specifically, mREITs raise both debt (lower rate, short-term loans) and equity (via new share issuances) capital to buy longer-term and higher interest rate real estate debt and related securities. The difference, or spread, between the cost of borrowing and lending is how they earn their profits, and what ultimately supports the dividend.

In other words, mortgage REITs function as a less regulated, riskier kind of bank, aggregating cheap capital and then indirectly lending it out at higher interest rates by purchasing mortgage backed securities.

Different Kinds of mREITs

Like eREITs, there are several kinds of mREITs that one can invest in. The two biggest distinctions are: residential vs. commercial focus, and internal vs. external management.

Internal management simply means that the managers of the REIT’s assets work for the company itself. Thus their compensation is more transparent and theoretically able to be altered by shareholders via the board of director’s compensation committee.

External management means that the management comes from a third party, usually a large asset manager, who doesn’t have to disclose how much management is paid. Externally managed mREITs pay a base management fee, which is usually a percentage of assets, as well as performance fees based on the growth of book value.

Or to put it another way, externally managed mREITs are essentially private equity funds specializing in real estate based financial instruments.

The other major distinction between mortgage REITs is whether they focus on residential or commercial real estate.

Residential mREITs, such as Annaly Capital Management (NLY) and American Capital Agency (AGNC), make almost all their money by buying low credit risk (i.e. “agency backed”) home mortgage backed securities, or MBS, that are insured against default by Fannie Mae (FNMA), Freddie Mac (FMCC), or Ginnie Mae.

Since these are essentially government backed securities, with virtually no default risk, the yield on these MBS are low, requiring higher leverage by the mREIT, typically around 6-8:1 (i.e. borrow $6 to $8 for every $1 of equity invested).

Commercial mortgage REITs such as Starwood Property Trust (STWD), on the other hand, operate by investing or originating commercial mortgages, which have no government backing and are therefore higher risk. However, because of this, they are higher-yielding loans, which means that commercial mREITs usually operate with far lower leverage levels.

Also, commercial real estate is usually more stable than residential real estate, meaning that, assuming strong underwriting or due diligence (i.e. research into the mortgages backing the security), the default risk can be lower than that of residential mortgages.

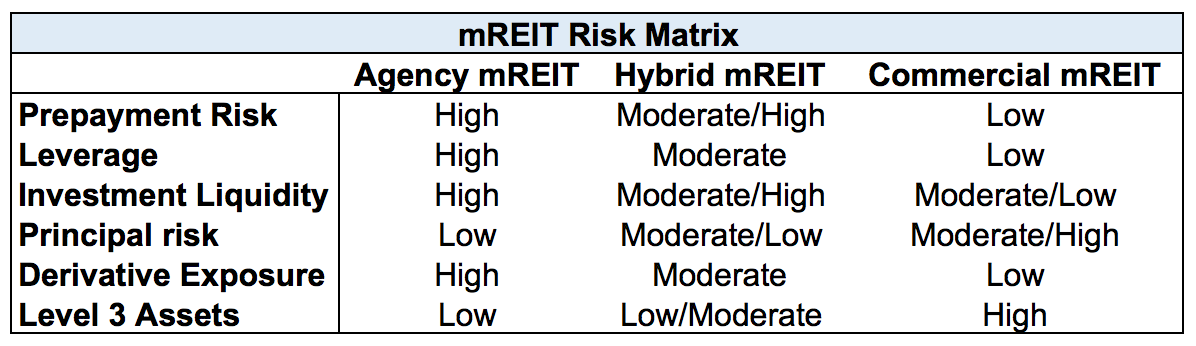

Of course, the differences between residential and commercial mREITs also apply to the risks faced by both, which is the most important thing for potential or current investors to understand.

Key Risks to Owning mREITs

Because mREITs are highly specialized financial companies, understanding both their business models and risks is vital to long-term investing success.

Source: Brad Thomas

For example, residential mREITs, because most of their business is agency-backed MBS, have little principal (i.e. default) risk since they are backed by the government. However, as explained earlier, the lower yield on these types of securities means that residential mREITs need to take on higher leverage and hedge against changes in interest rates via derivatives such as interest rate swaps and swaptions.

In addition, because home mortgage rates have been falling over time there is a higher risk of prepayment. This is when the homeowner refinances and pays off the original mortgage in exchange for a new mortgage with a lower interest rate, and thus a lower monthly cost.

The reason this is bad for residential mortgage REITs is because they usually buy these MBS on the open market at around 4% to 6% above par value (i.e. the value of the underlying principle mortgage loan).

This means they rely on the mortgage holder paying off the loan over the full 15 to 30 year duration of the mortgage, so that interest payments can allow them to amortize the premium they paid for the security. If a loan is refinanced and paid off early, this can mean a loss for the mREIT, which hurts both book value (the intrinsic value of the company) and EPS that funds the dividend.

Commercial MBS, on the other hand, usually have lower prepayment risk but higher credit risk, and thus come with higher-yields that allow the mREIT to utilize lower leverage and less interest rate hedging.

In addition, commercial mortgages are usually floating rate loans, meaning tied to the LIBOR, or London Interbank Offered Rate. In other words, while most residential MBS are fixed-rate, the interest rate on commercial MBS rises with interest rates, allowing commercial mortgage REITs to potentially profit from a rising interest rate environment.

This distinction is important because residential mortgages, usually being fixed, fall in value with rising interest rates, which negatively affects the value of a residential mREITs loan book (i.e. book value, or net asset value per share). And since the share price generally follows the trend in book value, residential mREITs generally thrive in a falling interest rate environment, but suffer if rates rise.

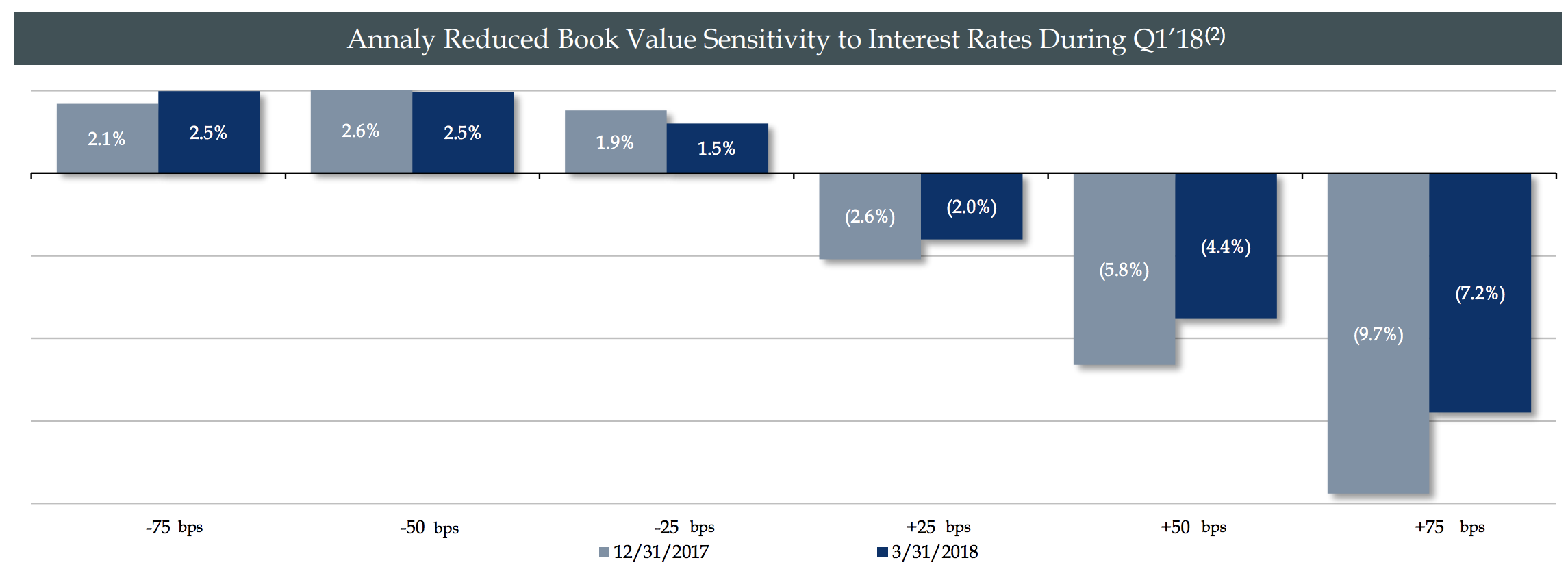

Annaly Capital is the largest residential mREIT in America, and here is a look at the firm’s sensitivity to interest rates. Note that a 0.75% increase in interest rates is expected to reduce the company’s net asset value by 7.2%.

Source: Annaly Capital Management

While it may sound like commercial mREITs are thus safer than residential mREITs (which is generally true if interest rates rise), keep in mind that this is a highly complex industry and there are always tradeoffs.

For example, agency-backed MBS is a highly liquid, high-quality (tier 1 capital) market, meaning that mREITs can usually enter or exit trades very easily. In addition, determining the true value of a loan is also simple because it’s just the last quoted price.

In other words, commercial mREITs usually operate in class, or tier 3, illiquid loans, which are harder to value. This means that commercial mREITs face the risk of having to write down the value of their assets more abruptly, which can hurt book value and can send the share price falling.

Or to put it another way, residential mREITs are more interest rate sensitive, while commercial mREITs have potentially more volatile book value and share prices over time; especially if a recession hits and default rates rise on their underlying loans.

In addition to all this complexity associated with the underlying business model, investors need to consider the track records of individual mREITs. Specifically, because this is still a pretty young industry, there aren’t a lot of long-term track records or battle-tested management teams currently helming these equities.

Furthermore, keep in mind that the general direction of interest rates since 1982 has been downward, meaning that it’s possible that the success of mREITs that have been around longer, such as Annaly Capital (NLY), may be due to a massive, generation-long interest rate megatrend that is now at an end (since rates likely have nowhere to go but up over time).

And even if mREIT management teams are capable of navigating a potentially more challenging rate environment, keep in mind that all mREITs are variable pay dividend securities.

Unlike popular dividend stocks such as Coca-Cola (KO), Johnson & Johnson (JNJ), Procter & Gamble (PG), which raise their payouts every year over decades, mREITs often have to raise and lower their payouts as earnings permit.

This means much higher share price volatility. Now over the long term, as long as you reinvest the dividends (and/or buy on dips), you could still do well if you are highly selective and stick with the best managed mREITs.

However, if you have a low to medium risk tolerance, desire very consistent income, and might need to sell shares to support your lifestyle (such as in retirement), then mREITs are almost definitely not for you.

One final risk factor to discuss is something I touched on earlier, internal versus external management.

Unlike eREITs, which are increasingly going to an internally managed business model, most mREITs continue to be externally managed. The good news is that external management can cost less for the company because the asset manager assumes the back office cost of running a staff, including underwriters, researchers, and risk managers.

In addition, an mREIT sponsored by a giant asset manager can have far more connections to potential clients and be able to put together more lucrative and larger deals than smaller, internally managed mREITs.

But external management comes with two big potential downsides: less ability to achieve economies of scale, and potential conflicts of interest with shareholders.

For example, an internally managed mREIT with, say, $1 billion in assets will spend a lot of money, relative to revenue, on paying its management team and maintaining back office operations (think accounting and legal divisions).

But if the mREIT is successful over time and grows its assets to $10 billion or even $100 billion, then the cost of maintaining its staff and operations will grow less quickly than revenue. Under this scenario, its profitability and ability to sustain and even grow its dividend over time will also increase.

Now compare that to an externally managed mREIT, which may have very low overhead because the external manager is fronting all the back office costs, but must pay say 2% of assets as a base management fee, no matter if the mREIT loses or makes money in a given year. And if the mREIT grows its assets 10x or even 100x in size? Well, that management fee continues to grow just as fast as assets, meaning it can’t achieve economies of scale.

This brings up the final risk with externally managed mREITs, the potential for conflicts of interest with shareholders. Specifically, because management doesn’t work for shareholders and is paid based on the size of assets (i.e. the size of the loan book), external managers can assure higher pay over time by acting in ways that can be detrimental to long-term shareholder value.

For example, an mREIT may be trading at below book value, meaning that raising equity growth capital is guaranteed to destroy shareholder value and likely lead to falling dividends over time. However, by selling more shares and investing the money in more loans, the asset size grows, along with management fees.

In this way, some poorly run externally managed mortgage REITs operate as private equity funds with management working for its own benefits, with little or no care for how long-term shareholders make out.

With so much complexity built into these things, and the risks to both share price and dividend so high, is it possible to successfully invest in this industry at all?

The answer is yes; however it requires a lot of risk tolerance (acceptance of share price, and dividend volatility), a hands-on approach (keeping careful watch on key metrics), and very careful selection of which mortgage REITs you invest in.

How to Successfully Invest in Mortgage REITs

Assuming that you A) don’t mind the high-risk, high dividend/share price volatility that comes with this industry, and B) are willing to put in the time to carefully research mREITs before and after investing in them, here is how you can invest for the long term in this highly speculative, ultra-high-yield industry.

As with investing in any company, the ultimate deciding factor is due diligence, with special focus on the quality and trustworthiness of management. Specifically, that means keeping careful monitoring of several key factors change over time including: book value per share, the dividend payout ratio, asset mix/quality, and net interest margin spread.

Book value per share is one of the most important things to track over time because as with most financial companies, the book value represents the objective value of the company’s assets.

And because mREITs, like their eREIT cousins, are legally required to payout almost all profits as dividends, growth must come from either debt or equity capital markets. In other words, mREITs always have fresh capital flowing into them to grow their assets over time (even internally managed ones).

Thus the trend in book value per share over time will tell you how well management is able to allocate this new shareholder capital. Can they invest in profitable enough loans and/or strategies to ensure accretion to EPS and book value (meaning these metrics rise faster than share count), or are they growing just for the sake of growth (and their higher fees)?

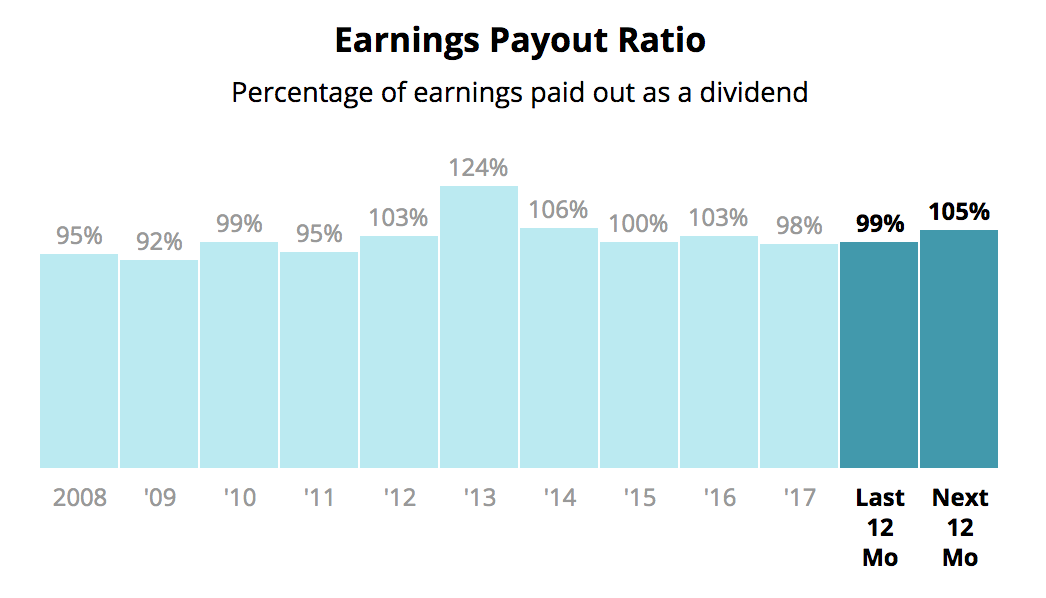

The answer to this question is tied into the second key metric to watch, the EPS payout ratio (sometimes called core EPS payout ratio depending on the mREIT). This tells you how safe a dividend is and in the ultra-high-yield world of mortgage REITs, the safety (rather than growth) of the dividend is paramount, since the sky-high payout is really the only reason to own these things.

Here’s Annaly Capital’s core EPS payout ratio over the last decade. As you can see, the company fallen short of covering its payout some years, which has resulted in numerous dividend cuts over this period.

Source: Simply Safe Dividends

An mREIT's asset mix is another important factor to watch. In recent years many financial companies have been under stress from low net interest spreads, meaning the difference between borrowing costs and how much they can lend at.

Various mREIT management teams responded to this by adapting their companies’ business models. For example, Annaly Capital is trying to evolve beyond its residential mREIT roots to become a major player in commercial real estate, as well as middle market lending. Attempts to diversify and reduce interest rate sensitivity are far from guaranteed to succeed for any mREIT.

Finally, like with banks, investors need to pay attention to a mortgage REIT’s net interest margin spread over time. A falling spread is a warning sign that, despite rising assets (much of which is paid for by diluting existing shareholders), the dividend profile may not be benefiting from the growth in an mREIT.

Conclusion

To be clear, mREITs are by far the most risky ultra-high-yield class of equities you can own, and most dividend investors would be better off ignoring the sector entirely (that’s our preference).

That’s because this is an industry that has come to prominence during a time of historically falling interest rates, which may have created a decades-long tailwind for the business model that may not be repeated as rates gradually climb in the coming years.

In addition, the business model is very challenging to stay on top of, especially as management teams throughout the industry attempt to pivot into new strategies to grow their EPS and book value per share in a time of extreme market difficulties, characterized by severely compressing net interest margin spreads.

That being said, for very risk tolerant and hands-on investors, who don’t mind digging into the weeds of quarterly earnings, conference calls, and investor presentations, there could be a few candidates out there to consider.

But of course, any investments in the mREIT space need to be kept small, and only as part of a very well-diversified dividend portfolio. Mortgage REITs fall in the "too hard" bucket of investment opportunities for us due to their heightened sensitivity to interest rates, dependence on capital markets, and high downside risk in the event of an economic downturn.