An exchange traded fund, or ETF, is a publicly-traded fund that tracks an index such as the S&P 500. There are thousands of ETFs in the U.S., but only a few hundred funds are specifically classified as dividend ETFs.

Dividend ETFs can provide a number of benefits for investors seeking safe retirement income or long-term growth. In fact, many investors own a combination of dividend ETFs and individual stocks in their portfolios.

However, there is a never-ending debate over the merits of actively picking stocks versus allocating a portfolio completely into low-cost, passively-managed ETFs.

The reality is that an investor’s mix of dividend ETFs and individual stocks almost completely depends on the investor’s personal preferences. There are numerous pros and cons to each approach, and unfortunately there is no one-size-fits-all solution.

In this article, I will evaluate some of the most common questions facing investors who are considering dividend ETFs:

What are the pros and cons of owning dividend ETFs?

How can I tell which ETFs are “good” ones?

Who should buy dividend ETFs?

By the end of the article, you will know the key advantages and disadvantages of investing in dividend ETFs and have an understanding of whether or not dividend ETFs are for you.

The Benefits of Dividend ETFs

Dividend ETFs offer a number of attractive characteristics. Most notably, in my view, dividend ETFs can save investors a lot of time and potential headaches compared to owning individual stocks.

The majority of dividend ETFs hold between 50 and several hundred companies and are well-diversified across a number of industries.

Purchasing shares of most dividend ETFs provides instant diversification to a portfolio, providing an investor with some protection against being overly exposed to a sector that falls out of favor.

Perhaps more importantly, dividend ETF investors do not need to worry much about monitoring their holdings because many ETFs are diversified across hundreds of companies.

In other words, no single company is likely going to make or break the performance of an ETF, so there is practically no need to stay up to date on news about individual businesses owned in the fund.

Once an investor has found a diversified dividend ETF that comes close to matching his or her objectives, the investor can simply focus on accumulating as many shares as possible and letting the investment ride for the long term.

While ETFs will rise and fall with the underlying indexes that they follow (there is always market risk), it should be easier, in theory, for investors to ride out price volatility in diversified ETFs compared to individual stocks.

For example, suppose you owned a portfolio of 20 individual dividend stocks, and Cisco was your biggest position at 7% of your portfolio’s total value.

If Cisco were to fall by 30% this year on company-specific news, you would be faced with some very difficult, stress-inducing questions:

Cisco has been a dog. Should I sell now?

Or is Cisco bottoming out and potentially a bargain? Maybe I should buy?

Is the company’s dividend at risk? Why is the stock so weak?

Owning individual stocks requires more time commitment to stay on top of new developments and can sometimes encourage excessive trading activity, which is often the enemy of investment returns.

An investor in dividend ETFs can usually sleep better at night than an investor running a portfolio of individual stocks. For every Cisco owned in a diversified ETF, there is likely to be an equal number of winners to balance things out.

While ETFs will match any steep declines in price of their underlying indexes, prudent investors should know that the collective long-term value of a fund’s diversified holdings has not been impaired – the stock market is simply volatile and unpredictably rises and declines.

Unlike Cisco, where something could be structurally wrong with the company to make its stock a poor long-term investment, it would take some sort of apocalyptic event to impair the long-term value of all of a diversified ETF’s holdings.

Put another way, dividend ETF investors can feel more comfortable buying additional shares on a dip instead of worrying about whether or not the long-term earnings power of their individual stock has been impaired.

Investing in dividend ETFs is also just an easy strategy to follow. Investors who own a portfolio of individual stocks typically have at least several dozen holdings to pick between when they have new money to invest.

Trying to decide which individual stock(s) to buy more of often feels complicated, but an ETF investor can simply allocate across several funds to remain diversified and continue following the underlying index.

Simply put, an ETF strategy is much easier to consistently execute and can help an investor maintain more time in the market to enjoy the benefits of compounding.

Investing in dividend ETFs can be particularly appealing for small investors. Generally speaking, most of the benefits of diversification kick in once a portfolio has accumulated as few as 15 to 20 total holdings spread across different sectors.

While trading commissions are generally quite low today, building a portfolio of 20 stocks can still eat into an investor’s returns if their portfolio value is low.

For example, an investor with $10,000 to invest equally across 20 stocks would target an initial value of $500 per holding. A $10 trading commission equates to a steep 2% fee ($10 / $500), which is incurred again every time the investor buys more shares.

It would probably make more sense for the small investor to achieve appropriate diversification and lower fees by accumulating shares of an ETF until his or her account was more sizeable.

Finally, it’s worth pointing out that even Warren Buffett advocated for passive index funds in his 2013 shareholder letter.

After he passes away and his shares of Berkshire are distributed to charity, Buffett’s trustee has very clear instructions to follow:

"My advice to the trustee couldn’t be more simple: Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard’s.) I believe the trust’s long-term results from this policy will be superior to those attained by most investors – whether pension funds, institutions or individuals – who employ high-fee managers."

Warren Buffett owns several dozen dividend-paying stocks in his portfolio, but it’s clear he sees the benefit of cheap, passive indexing – most active investors simply fail to generate performance that justifies their higher fees.

However, there are a number of disadvantages to owning dividend ETFs over individual dividend stocks – especially for conservative retirees primarily focused on capital preservation and safe income generation.

The Downsides of Dividend ETFs

Some dividend ETFs now offer rock-bottom fees as low as 0.05% per year, but ETF investors have no ability to fine-tune a fund for their unique investment objectives and risk tolerance.

For example, suppose a retired investor has $1 million of cash to invest and wants to generate safe income from dividend-paying stocks while preserving capital.

Vanguard is a well-known and trusted brand, and the investor happens to come across the Vanguard High Dividend Yield ETF (VYM).

The fund certainly sounds appropriate for his needs and charges an extremely reasonable fee of 0.08% per year. The fee amounts to less than $1,000 per year for his account and is well worth it for the time savings alone – he can now take a “hands off” approach to generating income by investing in a well-diversified fund.

However, there are a few issues to consider here. First, the fund’s dividend yield is nothing to get overly excited about for current income. It has a dividend yield near 3%, which is too low for many retirees’ income needs.

Second of all, how safe is that income? The Vanguard High Dividend Yield ETF is invested in more than 400 companies – certainly not all of their dividend payments will be safe throughout a full economic cycle.

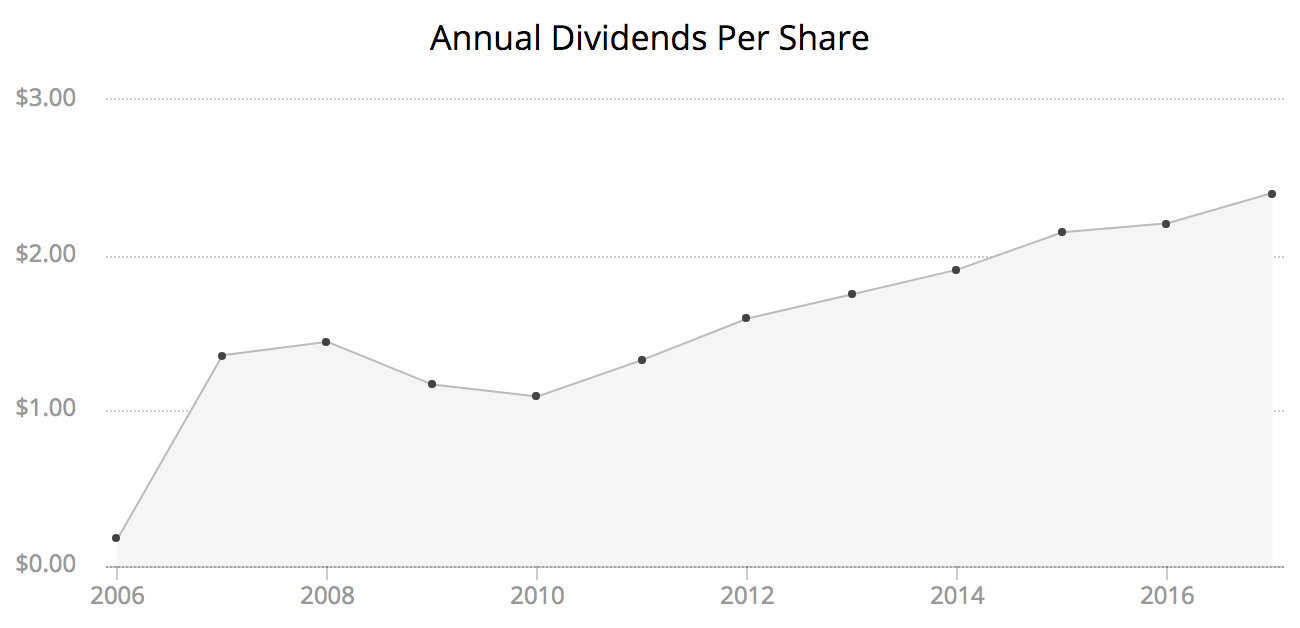

Unfortunately, we can see that the fund’s dividend payments were hit hard during the last recession. Total dividend payments reached $1.44 per share in 2008 before falling to $1.17 in 2009 and $1.09 in 2010, representing a peak-to-trough decline of about 25%. Annual dividend payments didn’t recover back to their 2008 peak until 2012.

Put another way, if the retired investor above owned 25,000 shares of VYM, he would have received $36,000 of dividend income in 2008.

By 2010, his annual dividend income had fallen to about $27,000 – a drop of more than $725 per month. Depending on his budgeting and margin of safety, life could suddenly have become much more stressful.

VYM's price also fell by more than 32% in 2008, likely invoking plenty of fear as the value of his nest egg fell from $1,000,000 to less than $700,000.

Vanguard High Dividend Yield ETF (VYM)

Most of the big dividend ETFs available today were launched sometime over the last five years – after the financial crisis. Unfortunately, that severely limits investors’ ability to understand the real risk of dividend cuts that is embedded in most passively-managed dividend ETFs.

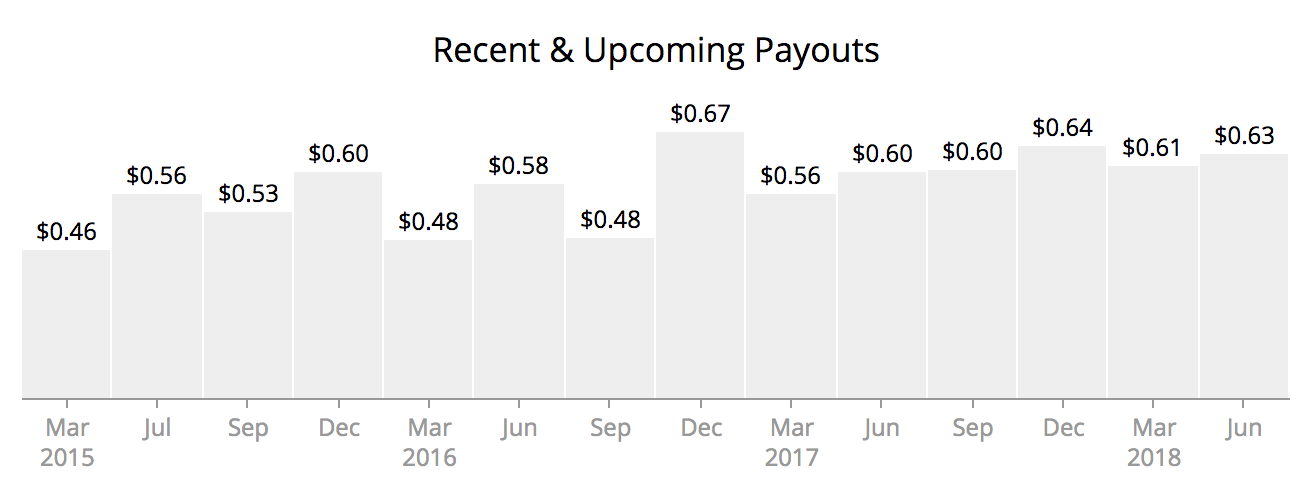

Even when times are good, a dividend ETF's income is highly unpredictable, making monthly budgeting in retirement more challenging. ETFs are constantly rebalancing, and the many companies they own are adjusting their dividends up and down throughout the year. Here is a look at VYM's volatile quarterly payouts over the course of several years.

Building a portfolio of several dozen blue chip dividend stocks requires some time, but it also allows investors to customize the dividend yield, diversification, and dividend safety of a portfolio to their unique needs.

You will also know exactly how much you are getting paid each month of the year since each company has a set dividend payment schedule.

Source: Simply Safe Dividends

While numerous “safe” dividend stocks such as General Electric and Bank of America surprised investors during the financial crisis and slashed their dividends, I believe it is possible to construct a portfolio with a higher yield and more resilient income stream than what is attainable from dividend ETFs today.

Besides greater customization, accumulating a portfolio of individual dividend stocks lets investors keep more of their dividend income.

Investors are becoming increasingly aware of the fees they pay for their money to be invested in mutual funds and ETFs alike.

Passive ETFs have rapidly grown in popularity because they are, on average, substantially cheaper than their actively managed counterparts.

One of the main reasons why ETFs are cheaper is because they do not need to employ a high-paid research team in an effort to beat a benchmark – they are simply trying to match a benchmark’s performance at the lowest cost possible.

I am not going to beat a dead horse and discuss the merits of investing in low-cost ETFs versus active money managers. In the far majority of cases, I would advocate for the ETF due to the fee savings and generally more dependable performance.

Instead, the focus of this article is on investing in dividend ETFs compared to individual stocks.

The beauty of owning individual stocks is that there are no ongoing fees – you only incur costs when you buy or sell a stock, and trading commissions are generally quite low today (typically $5 to $10 per trade at most discount brokers).

While dividend ETFs trade just like stocks, every ETF charges a recurring fee based on the value of your portfolio.

Many fees charged by ETFs appear rather harmless. Fees generally range from less than 0.1% to 0.5% per year for some of the largest and most popular dividend ETFs.

For small investors, these fees are almost a no-brainer to achieve proper diversification and gain time in the market – a $10,000 account might pay as little as $10 per year.

Investors who don’t want to deal with the hassle of owning individual stocks are also happy to pay the fee and sleep well at night.

However, fee dollars can really begin to add up for larger account sizes over the course of many years.

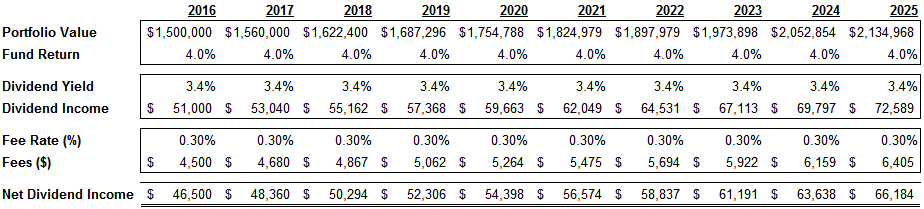

Suppose an investor had $1.5 million he wanted to invest in dividend stocks to achieve a yield of at least 3.5% with low volatility.

The PowerShares S&P 500 High Dividend Low Volatility ETF (SPHD) seemed to meet his objectives. The ETF has an annual expense rate of 0.3% and offers a dividend yield around 3.5%.

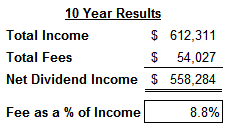

The table below projects his portfolio over 10 years, assuming an annual 4% return from the fund, no reinvestment of dividends (he lives off the income), and a constant 3.4% dividend yield.

In the first year alone, the investor would have seen $4,500 leave his portfolio to pay ETF fees, which amount to about $375 per month.

We can see that over the next decade, his portfolio generated $612,311 of dividend income, but fees ate over $54,000 of that amount.

Put another way, ETF fees consumed close to 9% of his total dividend income over the period – even despite the “low cost” nature of the fund.

Beyond fees, dividend ETFs with high portfolio turnover can also experience lower returns than their benchmarks because of their higher taxes and transaction costs. Owners of individual stocks can avoid these “hidden” costs and potentially generate slightly higher returns by maintaining a buy-and-hold strategy.

Some retirees are fortunate to have portfolios that are significantly larger than the $1.5 million account I used in the example above. As the size of a portfolio grows, fees also rise – a $3 million portfolio would pay over $700 per month in fees during the first year it was invested in the PowerShares S&P 500 High Dividend Low Volatility ETF.

However, some investors with large accounts are happy to pay ETF fees – if they already have enough passive income and aren’t interested in spending any time analyzing stocks, ETF fees are a small price to pay for the time and convenience they provide.

For investors interested in owning funds, let’s take a look at how to identify the best dividend ETFs.

How to Pick Quality Dividend ETFs

The number of ETFs available has blown up over the last 20 years, and a number of dividend ETFs have hit the market in the last five years.

Despite there being more than 100 dividend-focused ETFs in the market, the biggest challenge picking an ETF is finding one that is mostly aligned with your investment objectives (e.g. dividend yield, diversification, volatility).

As I previously discussed as one of the downsides of owning dividend ETFs, it can be difficult to find a low-cost product that meets your current income needs with a high dividend yield while also providing reasonable dividend safety and diversification.

ETF Database provides an ETF screener that contains a number of helpful metrics to help you find a potentially appropriate list of dividend ETFs. Morningstar also offers an ETF screener, but I am not aware of any others.

Once you have identified a handful of relevant ETFs, what should you look for? Aside from your personal preferences (e.g. dividend yield), it’s important to be aware of an ETF’s expense ratio, objective, diversification, turnover, and size.

As I demonstrated above, even a low expense ratio of 0.3% can really eat into a portfolio’s dividend income stream. My personal preference is to stick with funds with expense ratios no greater than 0.3%.

Many of Vanguard’s products charge fees below 0.1%, which is hard to pass up. The easiest way to maximize your dividend income and performance is to find the lowest cost, best diversified product.

Besides expenses, it is important to review a dividend ETF’s objective. You should be aware of the index an ETF is designed to track and feel comfortable with its selection approach – some ETFs will blindly pick the highest-yielding stocks in a particular group, while others will add in some sort of “quality” filter.

While these factors might not seem important during a bull market, they can make a world of difference during a recession – lower quality ETFs and indexes hold companies that are much more likely to cut their dividends and underperform the market. Unfortunately, there is no easy way to view the most important financial ratios for dividend ETFs since they consist of so many individual dividend-paying stocks.

However, for funds with a long enough history, investors can view their historical dividends paid by calendar year using our website to see how much they cut their dividends during the last recession.

The diversification of an ETF is another factor to consider. Some funds are constructed to be significantly over- or under-weight a sector. For example, the PowerShares S&P 500 High Dividend Low Volatility ETF (SPHD) derives around 20% of its exposure from utility stocks, but less than 1% of the Schwab U.S. Dividend Equity ETF’s (SCHD) holdings are utilities.

Each fund has guidelines to follow as it relates to its maximum exposure to any single sector or stock, and my general preference is for no sector to exceed 25% of the portfolio and no stock to account for more than a 5% weight.

If I am going to invest passively in ETFs, I don’t want to lose sleep over any “active” bets the fund might be taking by not being well-diversified – all it takes is a few large holdings to drag down the entire performance of a fund.

A fund’s turnover is important as well. ETFs with lower portfolio turnover pay less in capital gains taxes and transaction costs, which helps the performance of the fund (and the value of your portfolio) better track its index – especially in taxable accounts. I like to look for ETFs with turnover rates no greater than about 25%.

Finally, the size of an ETF also impacts its risk profile. Of the approximately 1,900 ETFs in the U.S., roughly 400 of them have average trading volume of less than 1,000 shares.

The top 150 ETFs also account for over 90% of overall ETF trading volume. In other words, there are a lot of ETFs that are dangerously small and may not be able to stay in business.

ETFs with very low trading volume are also susceptible to higher volatility and bigger trading gaps when you try to enter or exit a position. As a conservative investor, I avoid ETFs with total assets less than $500 million and prefer funds that have a track record going back at least three years.

To summarize, here are the ETF characteristics I prefer to see:

Fund objective is simple and tracks an understandable index

Diversified by sector (no more than 25%) and stocks (no more than 5%)

Expense ratio less than 0.3%

Portfolio turnover less than 25%

Total assets greater than $500 million

Fund inception at least three years ago

Investors can research most of this information quickly by simply “Googling” the name of the fund and viewing information directly on its website.

An ETF fund’s website and prospectus will tell you everything you need to know about its expense ratio, total assets under management, portfolio turnover, inception date, objective, and diversification. It usually takes just a few minutes to review this information to see if it meets your criteria.

Similar information on ETFs can also be retrieved from Morningstar, and a fund’s annual dividend history and growth can be retrieved using our website.

Closing Thoughts on Dividend ETFs

Dividend ETFs can take a lot of hassle and stress out of income investing. For investors who don’t mind the fees and have little interest in analyzing individual stocks, dividend ETFs are an attractive option to consider for the peace of mind and time savings alone.

For the rest of us, especially those with larger portfolios living off dividends in retirement, building a high quality portfolio of 20 to 30 individual dividend stocks can save hundreds or even thousands of dollars each month.

More importantly, building a dividend portfolio of stocks allows an investor to completely customize the dividend yield, dividend safety, and diversification of a portfolio to match his or her unique objectives. Managing a portfolio of individual dividend-paying stocks can certainly be a worthwhile endeavor.