My late grandfather entered the world in 1902, one year after the first Nobel Prizes were awarded, and one year prior to the founding of Ford Motor Company.

Born in a rural town in Iowa with a population of less than 100, he started out as a farm laborer with the dream of one day having his own farm.

During this period, America's economy experienced a tremendous amount of change. Electricity replaced steam. Factories got much more efficient with assembly lines. Railroads connected everything. And big, dominant companies started to emerge, including AT&T (1876), Coca-Cola (1886), General Electric (1892), Sears (1893), U.S. Steel (1901), and UPS (1907).

Farming transformed as well. My grandfather began with horses before moving to steam tractors and eventually the Farmall tractor, which made it practical for one farmer to do the work that once required several men and a team of horses. Coupled with the rise of the Ford Model T, it was a tough stretch to be a horse in early 20th century America.

Source: Iowa PBS, Robert Pripps

My grandfather had to grow up fast. He only had an 8th grade education and went to work to help support his parents and 11 siblings. His mother passed away when he was 16. He had to adapt to change all around him.

During his lifetime, he saw many marvels: TV, radio, cars, men on the moon and, sadly, two world wars. Through it all, with hard work and faith, he managed to get his own farm in the 1940s in northwest Minnesota, where my father would later be born and raised.

It's easy to look back on that period now and see a clear arc of progress, but living through it likely felt very different and often uncertain.

In many ways, that's not so different from today. Powerful new technologies like artificial intelligence are reshaping industries, while trade wars, military conflict in the Middle East, and questions about the balance of government power are making even some seasoned investors uneasy.

When several of these forces hit at once, it can feel like the rules are changing. One of our members recently reached out with the following question:

In my lifetime, I've never seen what we're seeing now. Previously, there have been policy disagreements but the system our forefathers put in place always served as the backbone. Now the administration is attempting to change the system itself.

We have data that tells us what happens during wars, pandemics, bank runs, and industrial technological changes. We have no data to analyze what happens when an administration is trying to change both policy and, more importantly, the system.

Based on our current system, I know the answer; keep it going. But based on an administration looking to change the system, I don't know the answer. As I approach retirement, it makes me wonder whether I should stay invested or move more to cash.

It's a fair question, and one I suspect many of you have wrestled with as even a single social media post can now upend longstanding norms across trade policy, foreign alliances, federal agencies, and financial markets.

But I think it helps to step back. My grandfather lived through periods that likely felt far more system-altering than what we see today.

Farm commodity prices collapsed after World War I, wiping out rural banks across the Midwest. The Great Depression devastated farmland in the 1930s. The U.S. abandoned the gold standard. Inflation surged into the double digits in the 1970s. Two world wars reshaped the global order.

Those were not just policy changes. In many cases, they were fundamental shifts in how the system itself operated. And yet, through all of it, the underlying engine of the American economy kept moving forward.

When you own a share of stock, you own a small piece of a real business, including its factories, customer relationships, and ability to generate cash year after year. The bigger question underneath all of today's noise is whether you still believe that great businesses will remain productive, and that your right to participate in their earnings will be protected.

If the answer is no, if you believe the policy environment has become so unpredictable that the system may no longer function in a way that reliably rewards long-term investors, or that your capital may not be treated fairly over time, then moving to cash might feel logical.

But if the answer is yes, even a cautious one, then the investment case has not fundamentally changed.

I think the answer is still yes. History makes that case pretty clearly.

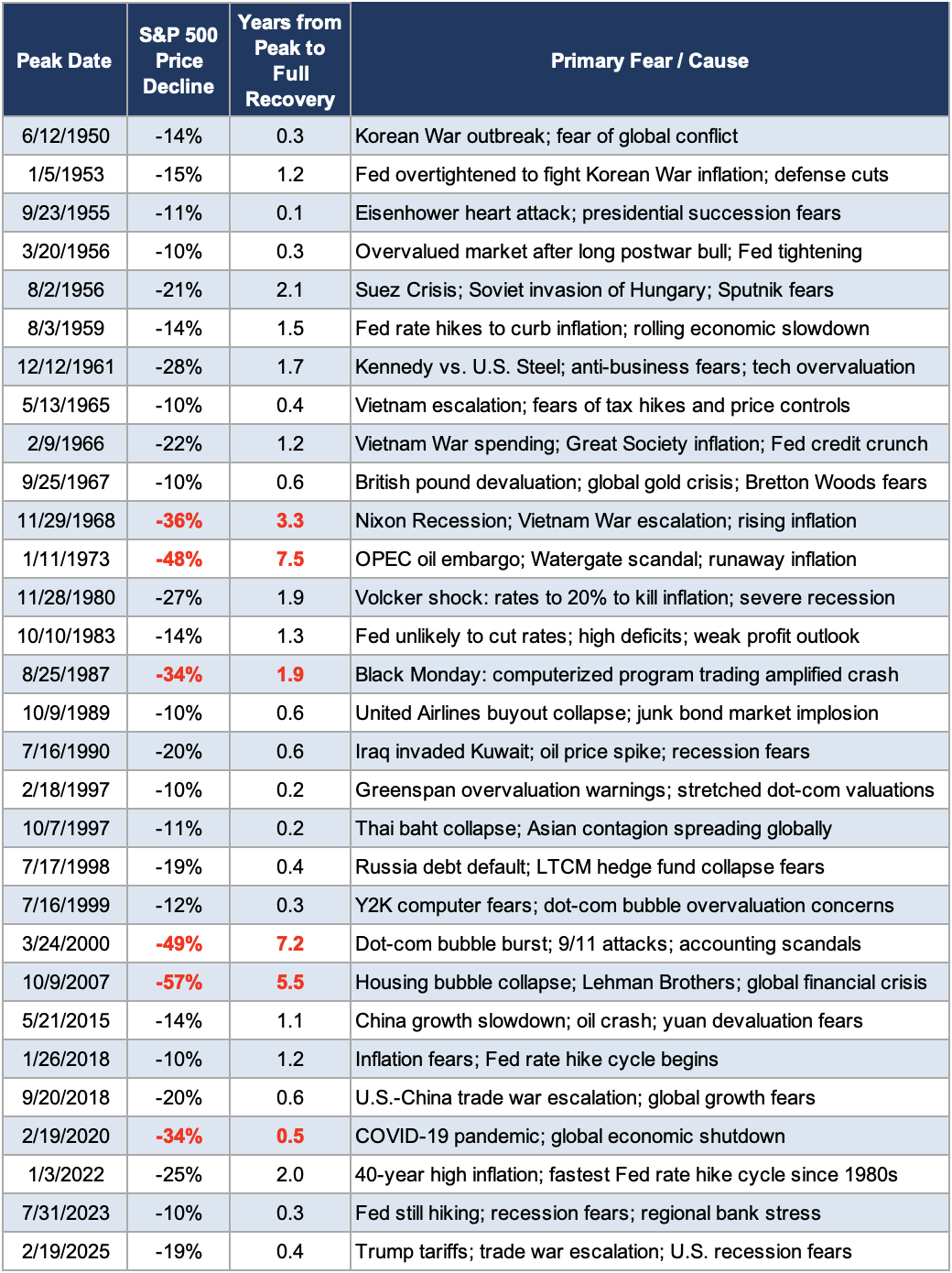

I built the table below using S&P 500 data going back to 1950. It shows every correction of 10% or more from a market peak, what caused each selloff, and how long it took the market to fully recover. The column containing the primary fear driving each decline is especially worth skimming. (You can download the table with additional data included if you'd like.)

You probably noticed that many rows represented a moment when investors could have concluded that this time was genuinely different. A president forced to resign. Runaway inflation. The Fed hiking rates to 20%. A global financial system on the brink of collapse. A pandemic that shut down the world economy in weeks. Wars that changed the structure of the world.

Each one felt, in the moment, like it might be the exception that broke the pattern of prosperity. The numbers tell a different story, though.

Since 1950, there have been 30 corrections of 10% or more from market peaks, or about one every two and a half years. The average decline was 21%, and markets recovered in roughly a year and a half.

Thirteen of those corrections turned into bear markets, with an average drop of 32% and nearly three years to recover. Six turned into something worse, deep bear markets with declines between 30% and 60%. Those were genuinely painful. The crashes of 1973, 2000, and 2008 each cut the market roughly in half. But they each fully recovered, albeit requiring five to eight years of patience.

To bring this to life, imagine an investor with perfectly bad timing, someone who invested $1,000 at each of the 30 market peaks in the table, right before every single correction.

Adjusting each investment for inflation, those 30 purchases represent about $167,000 in today's purchasing power. That portfolio is worth approximately $1.65 million today on price return alone, a roughly 10x return (7-8% annualized). Add dividends reinvested and the number would be substantially higher.

Even the unluckiest single investment in the group, buying at the dot-com peak in March 2000 right before a 49% crash that took around seven years to recover, earned 5.6% annualized over the following 26 years on price alone.

The 1973 entry is also worth reviewing since it probably comes the closest to what our member is describing. That period combined Watergate, which forced a sitting president to resign for the first time in U.S. history, with an Arab oil embargo that sent energy prices soaring, the end of the gold standard, and the worst inflation in a generation.

If any moment in the postwar era qualified as a threat to the system itself, not just to policy within it, that was likely it. The S&P 500 fell 48% and took over seven years to fully recover. And then it went on to produce one of the greatest bull markets in history.

One reason is easy to overlook. You are not invested in static businesses frozen in time. The companies in a well-diversified dividend portfolio are run by some of the most talented and driven people in the world, people who are aware of the shifting landscape and highly incentivized to adapt and protect shareholder value.

Some of my biggest investing mistakes have come from not trusting that process. Exiting Caterpillar in 2016 marks the first entry in my investing hall of shame. At the time, I worried that the heavy equipment maker's end markets were structurally impaired from the slump in commodities and would face years of overhang from cheaper used equipment.

In the moment, I failed to appreciate Caterpillar's entrenched market position, strong balance sheet, and long history of navigating cycles to position the business well for future growth. Caterpillar has returned over 900% since then, more than tripling the S&P 500.

Staying patient with financially sound businesses often proves far more valuable than trying to time the exits. I only average around one to two trades per portfolio each year, and that may be one or two too many.

We all face our Caterpillar moments, points where the near-term evidence seems to justify an exit and the uncertainty feels different from anything before it. Moving everything to a money market fund can feel like the prudent response. But unless you have a portfolio so large that investing for growth is no longer a concern, it requires a lot to go right.

You need to sell at the right time. You need to know when to get back in. You need to outlast inflation over a 20- to 30-year retirement. And you need to give up a growing income stream from companies that have navigated far worse than most events in today's headlines.

Of course, staying invested isn't always easy either. A 50% drawdown in stocks is not a remote theoretical risk. It has happened two times since 2000 alone, and you should be mentally prepared for it to happen again.

What makes that survivable for a dividend investor is that your income does not depend on what the market does on any given day. Dividends keep coming in whether the S&P 500 is up or down. They are an output of company fundamentals, not Mr. Market's latest mood.

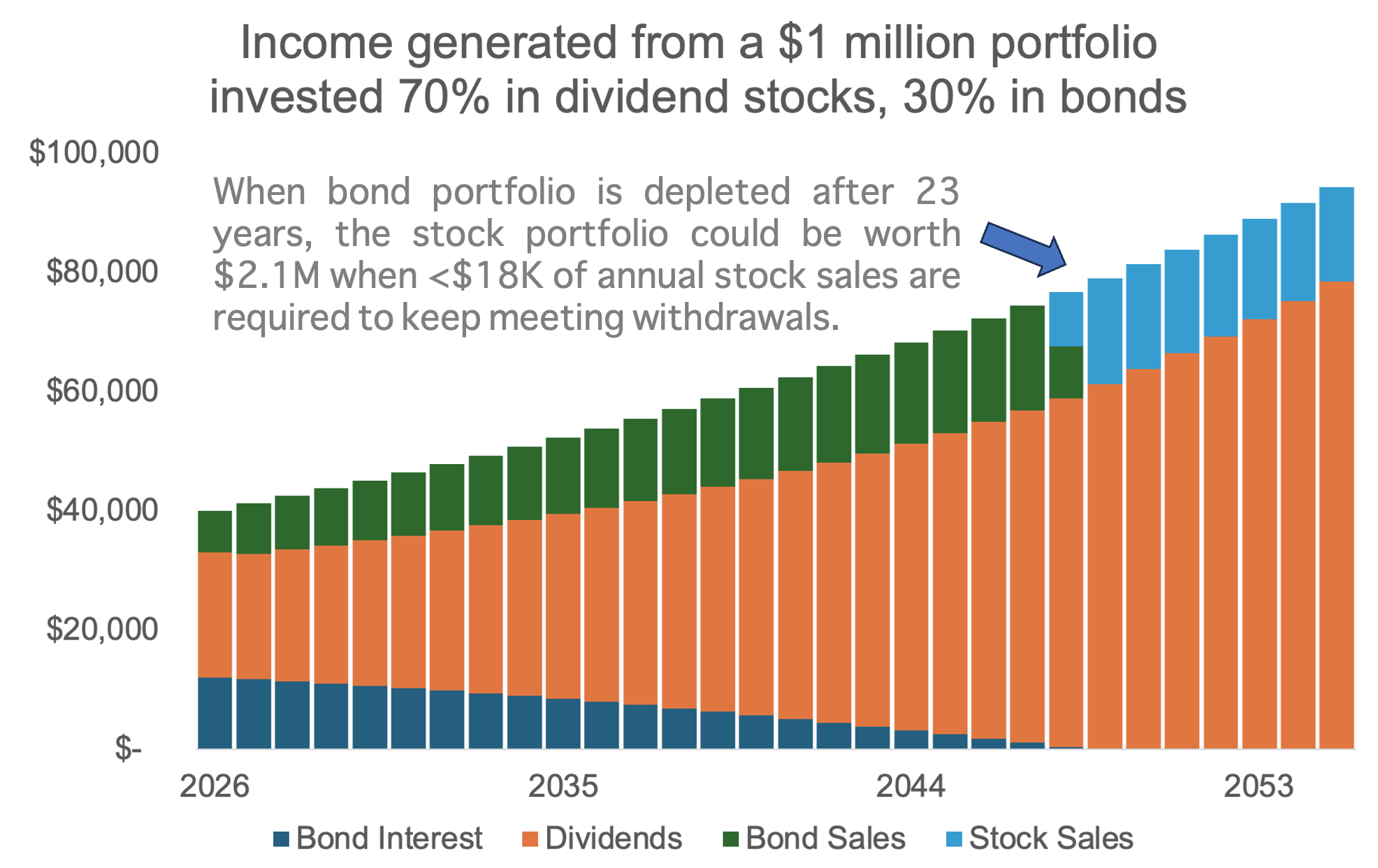

A practical way to think about this is to consider pairing your dividend stocks with a bond allocation that helps fund near-term spending needs while your dividend snowball grows. Take a $1 million portfolio invested 70% in dividend stocks yielding 3% with 5% annual dividend growth, and 30% in bonds yielding 4%.

With a 4% withdrawal rate growing 3% annually to offset inflation, interest income and bond sales cover the gap between your dividend income and spending needs for roughly 23 years before the bond portion is drawn down.

By then, your dividend income has grown substantially on its own because the underlying businesses kept compounding their earnings and raising their payouts, regardless of what the market was doing. You still own all your shares of stock, which at that point would be worth over $2 million if the portfolio continued to yield 3%.

With perhaps only a decade left in your retirement horizon, less than 1% of the portfolio would then need to be sold each year to keep meeting withdrawals as dividends continued to shoulder most of the load. A 50% market decline along the way is still painful on paper. But your dividend checks do not get cut in half when stock prices do. Companies don't reduce dividends because stock prices fall. They cut them as a last resort when their businesses deteriorate.

That is why we focus on higher quality companies with sustainable payout ratios and strong balance sheets rather than reaching for the highest yields available. A portfolio yielding 3% from durable businesses is far more dependable through a downturn than one yielding 6% from companies carrying too much debt or operating in cyclical industries.

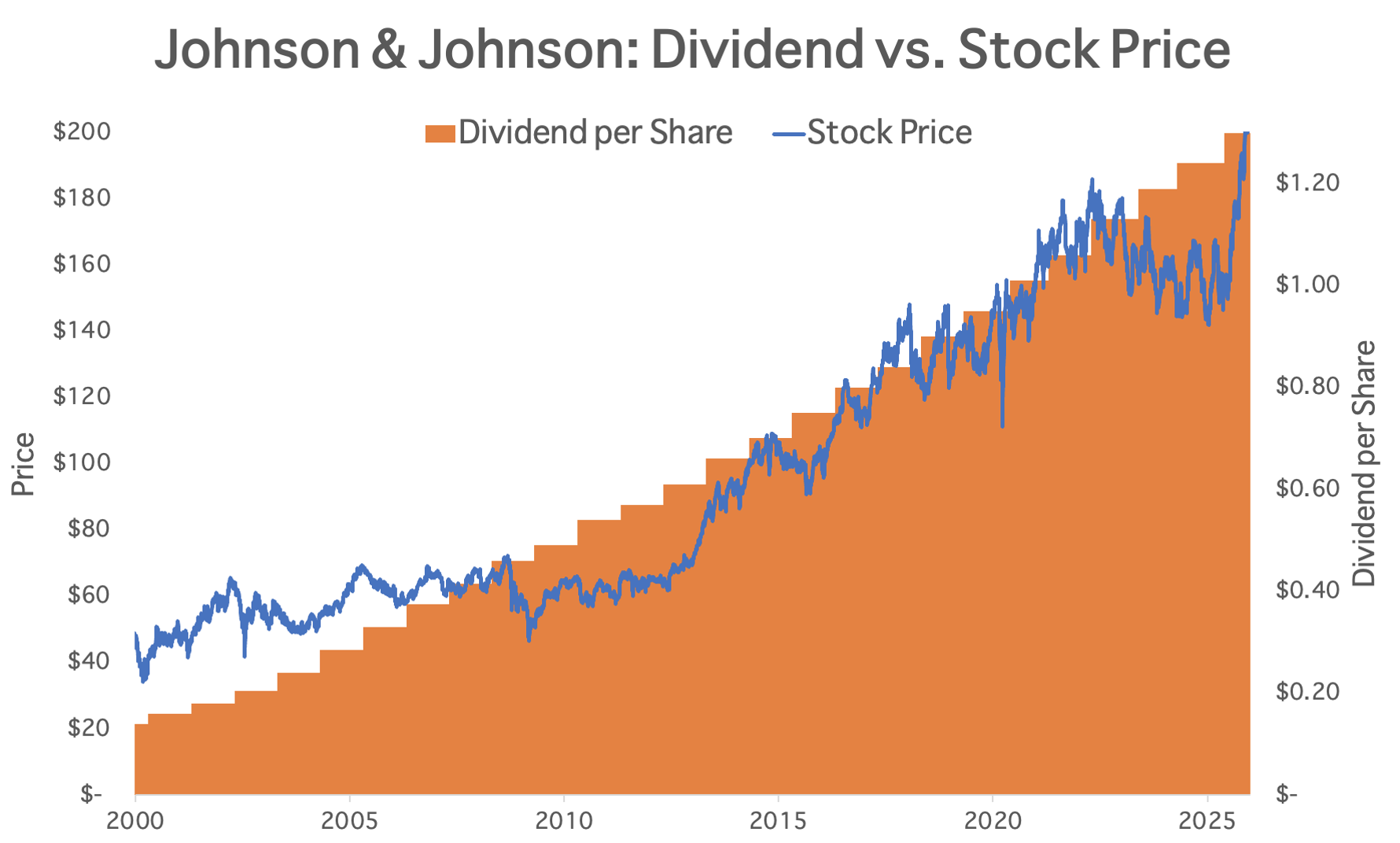

Johnson & Johnson, for example, has raised its dividend annually for over 60 years through recessions, crashes, and every variety of uncertainty. The income kept coming regardless of what the share price was doing. That steadiness is what allows you to look at a 50% market decline on paper and stick with the plan. And while near-term visibility can be clear as mud during downturns, zooming out to see that J&J's stock price has followed its dividend over the long run provides peace of mind that the value of your stake is still intact with each steady payout declared.

We cannot predict how policy will evolve or how markets will react in the short term. But we can build portfolios that are resilient to a wide range of outcomes.

The biggest risk in a moment like this is not the Iran war, AI disruption, or an executive branch that feels unpredictable. The biggest risk is making a permanent portfolio decision based on a temporary feeling.

With that in mind, it's worth briefly looking at what's driving the current anxiety. One of the biggest concerns is the surge in U.S. oil prices from around $65 a barrel to over $110 in a matter of weeks. When more of every paycheck goes toward gas, inflation-weary consumers have less available for discretionary spending.

The longer this drags on, the tougher life will become for businesses that depend on consumers opening their wallets freely, such as restaurants, apparel retailers, and home furnishing stores. The same is true for branded food companies facing higher input costs and more value-seeking customers.

A spike in oil prices also fans inflation at a time when the Fed was already cautious about cutting rates. Markets have shifted from pricing rate cuts this year to questioning if we could even see a hike by the fall. This creates challenges for rate-sensitive areas like housing, raises borrowing costs, and pressures the valuations of bond-like dividend stocks, which tend to sell off when bond yields rise.

While the timing of a resolution to the war is anyone's guess, we aren't in new territory. Oil shocks have rattled markets before, and the companies best positioned to emerge stronger were those with pricing power, essential products, and balance sheets strong enough to wait out the cycle. That describes the core of our portfolios.

AI anxiety has also hit markets as investors question whether the handful of tech giants spending hundreds of billions of dollars on AI infrastructure will generate returns proportionate to the cost. At the same time, fears have grown that AI tools could displace certain software companies and even entire categories of knowledge work, making some businesses less profitable or obsolete.

This is a strange paradox, but it has highlighted the appeal of "hard asset" businesses like many of the dividend growth stocks we own. It's hard to imagine a day where AI is capable of providing waste management services, operating cell towers, generating and delivering electricity, or running global restaurant chains like McDonald's. Those are the cash cows we've long favored.

Of course, a diversified portfolio will always have some laggards. A handful of our holdings have slipped on AI disruption fears, including Accenture, ADP, Paychex, and Broadridge.

I've been humbled enough times not to dismiss a concern this significant. But given these firms' long track records of innovation, strong cash flow generation, conservative balance sheets, and entrenched customer relationships, I'm willing to give them time to adapt, extending the same patience I try to give any high-quality business navigating change.

No one knows exactly how AI will reshape these industries over the next decade. But across a diversified portfolio of exceptional companies with strong financial positions, I expect our winners to more than offset any losers that emerge.

Staying invested through uncertainty, with a portfolio structured to weather it, has carried investors through even more dramatic periods of change than what we face today.

It is the same approach that helped my grandfather navigate a world that was transforming all around him. The tools have changed and the headlines are different, but the underlying challenge, learning to stay steady in uncertain times, remains very much the same.

Go back to the one question. Do you still believe that great businesses will create value over the next 20 to 30 years, and that your claim on that value will be protected?

If so, and I do, the plan does not change.

Thank you for your support of Simply Safe Dividends, and please reach out with any questions or ideas for how we can keep improving the service for you.