T. Rowe Price: A Quality Dividend Aristocrat Facing Growth Uncertainties

Founded in 1937, T. Rowe Price (TROW) is one of the world’s largest investment managers. The company uses fundamental and quantitative analysis to create and manage a wide variety of equity and bond funds, which have historically beaten their indexes and thus attracted consistent inflows of investor capital.

The company makes most of its money through investment advisory fees (90% of net revenue) charged for managing clients' portfolios. Fees are generally assessed as a percentage of assets under management, so they are driven by the total value and mix of the funds T. Rowe Price manages for investors.

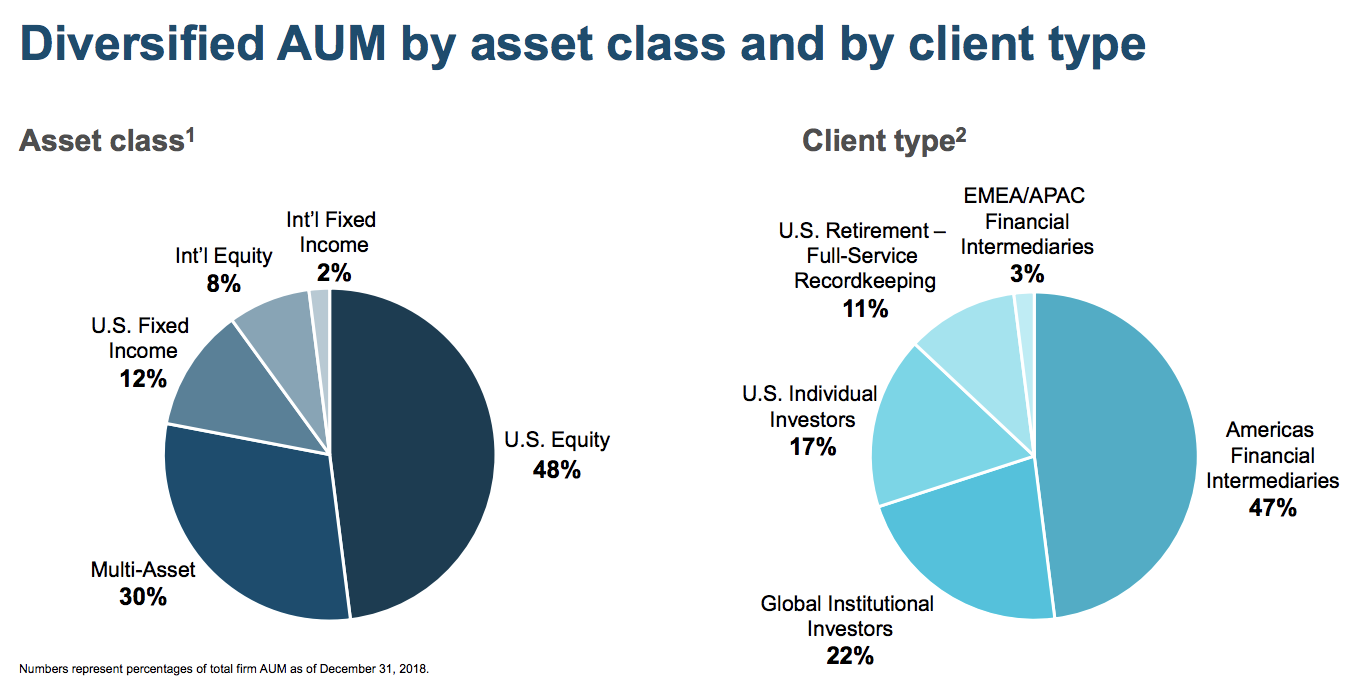

T. Rowe Price had $962 billion in assets under management at the end of 2018, with roughly two-thirds of its assets in retirement accounts. Stock and blended asset portfolios account for 86% of T. Rowe Price’s total asset mix. In total, the company offers over 500 investing products, such as mutual funds, separate accounts, and trusts.

Source: T. Rowe Price Investor Presentation

The business is very focused on the U.S. with international investors only representing about 6% of T. Rowe Price's assets. However, T. Rowe is working on growing its business via expanded fund offerings in Europe, Japan, and Australia.

With 32 consecutive years of dividend growth, T.Rowe Price is a dividend aristocrat. Impressively, over the last 20 years the firm's annual dividend growth rate has averaged 15% or about double the rate of the S&P 500's dividend growth.

Business Analysis

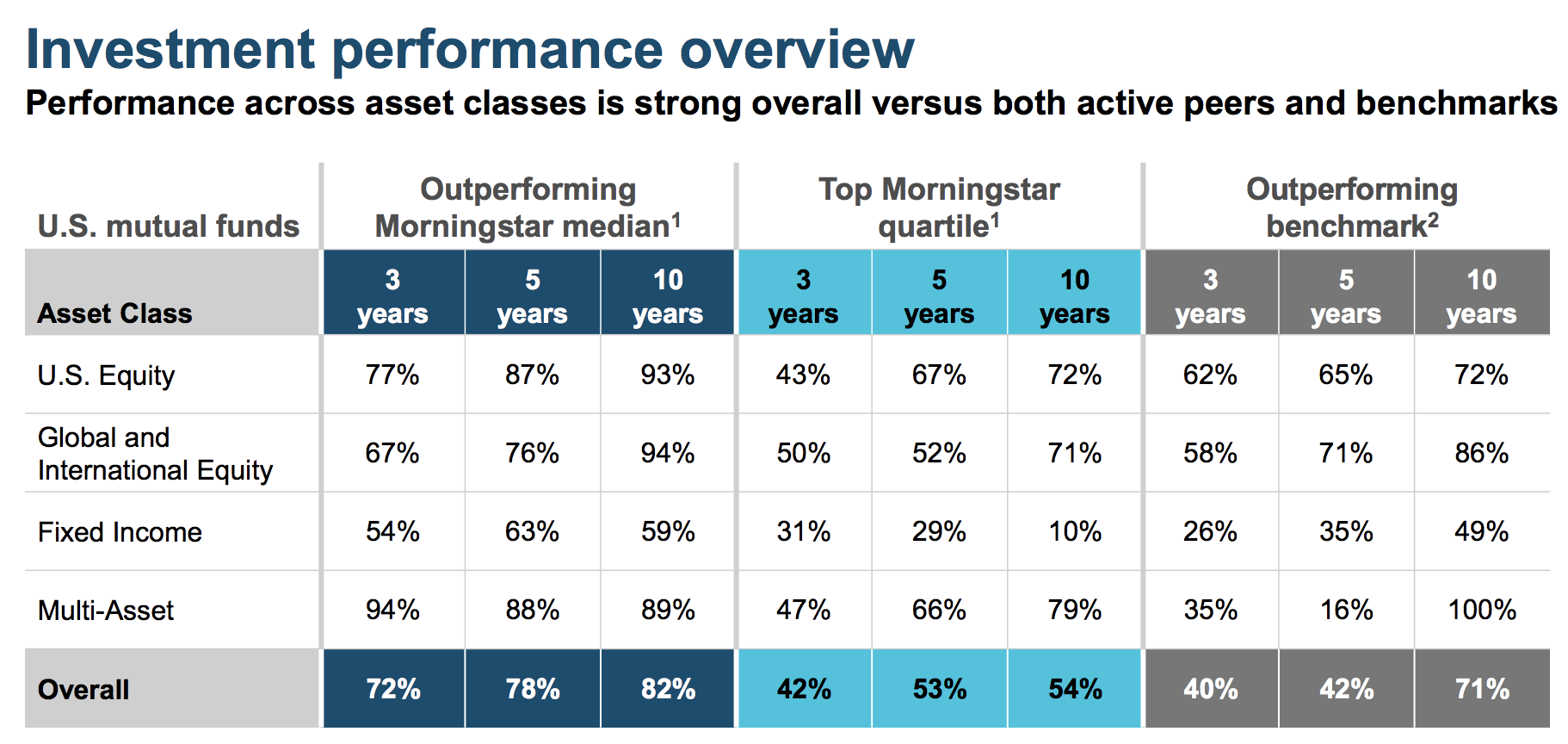

Performance and trust drive the asset management business, and T. Rowe has both. The firm has been in business for more than 75 years, demonstrating impressive investment performance over most time periods.

The performance data below shows the percentage of T. Rowe Price U.S. mutual funds that outperformed their median peer and benchmark, as well as the proportion of its funds with performance ranked in the top quartile of their peer groups.

You can see that the firm's equity strategies have delivered very competitive performance over longer time periods. In fact, 93% of T. Rowe's U.S. equity mutual funds have outperformed their median peer over the last decade, and 71% of its overall U.S. mutual funds have outperformed their benchmarks over the same period.

Simply put, T. Rowe's performance track record is among the best of any active fund manager.

Source: T. Rowe Price Investor Presentation

As a result, while many active managers have experienced net outflows due to performance struggles and the rise of passive products, over the last five years T. Rowe's organic assets under management (AUM) have grown 0.7% per year. Management targets 1% to 3% organic AUM growth over time.

To meet its goal and maintain its status as the dominant name in active asset management, T. Rowe will increasingly focus on international markets which have faster growth rates. In 2018 the firm's organic asset growth in overseas markets was 10.5%, showing that its foreign growth strategy is working so far and helping the company report overall organic asset growth of 1.3%.

Besides performance, part of T. Rowe's success is attributable to its scale. Large, risk-averse institutional investors such as endowments and pension funds drive the majority of industry revenue, so investment funds need to have appropriate scale, secure back-end processes, and a long track record of performance success to gain their business.

Before making an investment decision, institutional investors undertake an in-depth review of funds, analyzing historical performance, tenure length and quality level of fund managers, the efficiency of back office functions, fund expenses, and the breadth of products offered. Not surprisingly, bigger funds are able to put on a better show and engender more trust throughout the review process.

As one of the largest asset managers in the world, T. Rowe Price is able to check all of these boxes. Given its brand strength, stable operations, and performance track record, it would likely take a long stretch of underperformance or extreme staff turnover before its largest investors decided to take their money elsewhere.

While the industry is pretty fragmented, there aren’t that many mega-sized asset managers to meet the needs of the largest institutional investors – less than 3% of firms have more than 100 employees, making the biggest firms’ relationships with big institutions even stronger (fewer alternative firms to manage their money). T. Rowe's business is especially sticky because of its fee structure, asset mix, and product breadth.

Fees contribute significantly to a fund’s overall performance. T. Rowe Price has been a low-cost leader when it comes to fees for its actively managed funds, helping its overall performance and keeping it further out of the crosshairs of lower-cost passive management.

In fact, 88% of T. Rowe's primary U.S. mutual fund share classes have total expense ratios classified as average or below peers, according to data from Morningstar cited by the company. The company’s scale and operational synergies allow it to offer its clients lower costs without hurting its overall profit margin.

While lower fees certainly help performance and client retention (less incentive to switch asset managers as long as performance is “good enough”). T. Rowe’s business also benefits from its heavy mix of retirement-related assets.

Roughly 66% of the company's AUM (including 24% in target date retirement funds) are owned in retirement accounts such as 401(k)s and IRAs, which historically see lower turnover because workers seldom make changes to them unless they are invested in funds that are badly underperforming.

Better yet, many retirement accounts are typically funded every two or four weeks via direct deposit, as enrolled workers make automatic investments over time out of their paychecks. This stable asset base, which automatically rises over time, serves as a natural long-term growth driver for T. Rowe's business.

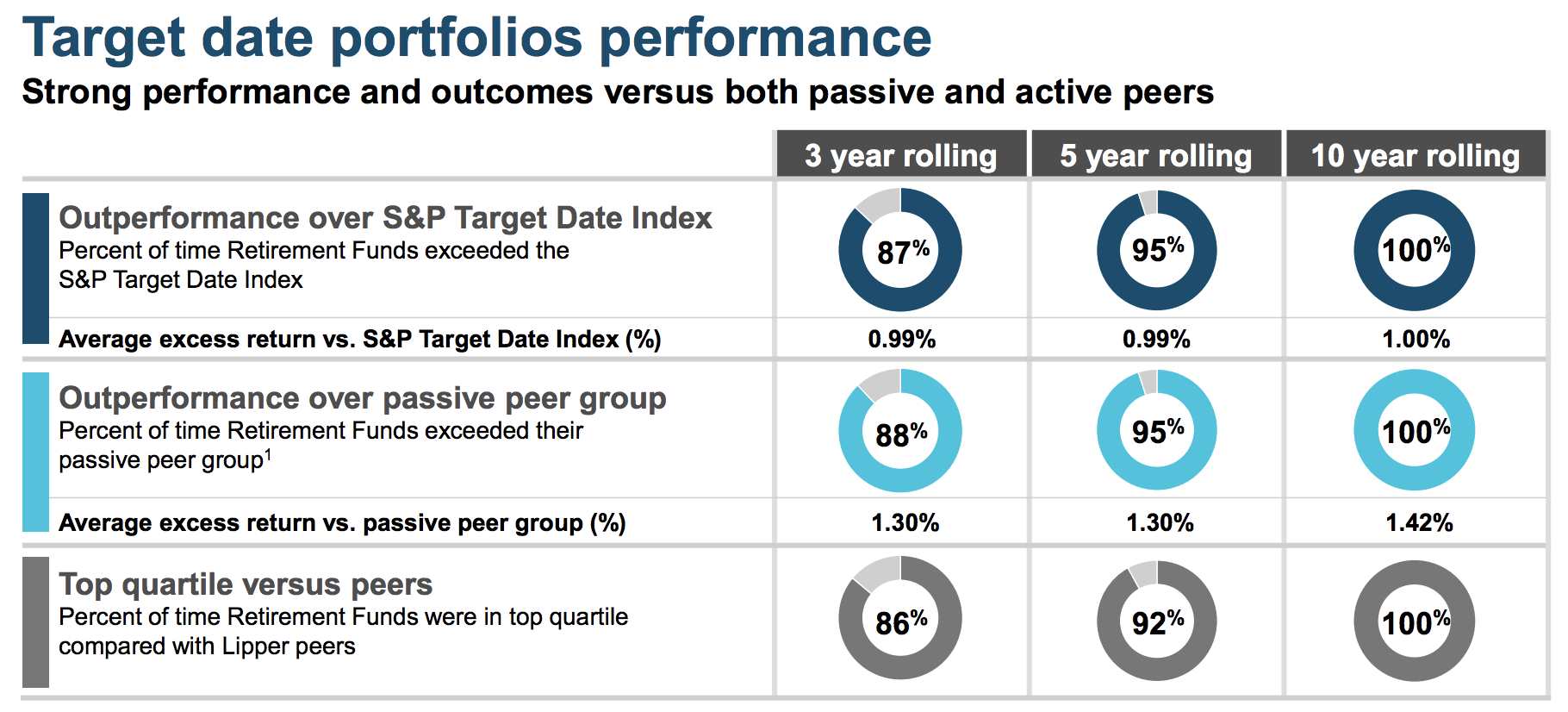

T. Rowe's target date retirement funds have delivered impressive results that help keep clients around, too. These funds are the ultimate "hands off" approach to asset allocation and have consistently beaten their benchmarks over time while delivering an average excess return of 1% compared to the S&P Target Date Index.

While 1% outperformance doesn't sound like much, on a $100,000 investment over 30 years, it amounts to nearly $60,000 in additional money in your retirement account.

Source: T. Rowe Price Investor Presentation

Retirement-related assets are generally stickier than other types of accounts because these clients are especially looking for a manager offering stability, safety, and trust to ensure their goals are met.

In other words, retirement-focused investors are less likely to chase performance as wealth preservation is of utmost importance. With more baby boomers retiring each day, T. Rowe Price seems well-positioned for continued growth in this key part of its business.

Finally, T. Rowe has a wide breadth of equity and fixed income mutual fund products and numerous distribution channels. Given the company’s high-quality reputation and performance figures, it is able to meet most investors’ needs if they want to reallocate assets among different funds. Smaller funds do not possess this optionality since their fund options are much more limited.

This also helps T. Rowe introduce new products faster to meet different investment trends, such as increasing demand for emerging market funds. The company’s reputation and distribution reach allow it to market and scale new products quickly, ensuring the firm stays relevant and maintains solid client retention as trends change.

A final appealing aspect of this business is that revenues rise with the market over time since recurring investment advisory fees are driven largely by assets under management. As long as fund performance remains strong enough to continue retaining clients and fighting off fee pressure, the market's long-term appreciation is a boon for fund managers.

In other words, T. Rowe enjoys a highly scalable business model due to the market's natural inclination to rise over time and the fixed nature of many of the company's costs. T. Rowe has leveraged its growing economies of scale to consistently generate operating margins in excess of 40% and excellent free cash flow, all while maintaining a debt-free balance sheet to continue supporting the safety and growth of its dividend.

However, while T.Rowe is unquestionably one of the most trusted companies in its industry, the business faces several notable growth challenges.

Key Risks

Over the short term, perhaps the biggest risk to consider is an eventual bear market. Equities and bonds have recorded excellent performance following the financial crisis, helping T. Rowe's fee revenue compound at a double-digit pace as assets under management soared.

However, when markets fall, assets under management shrink and many investors fearfully withdraw some of their funds. Lower assets mean less fee revenue, so T. Rowe is very sensitive to the market’s direction, especially given that over 80% of its capital is invested in more volatile stock and blended asset classes.

To highlight this point, consider the stock’s performance during the financial crisis. The S&P 500's peak-to-trough loss from 2007 through 2009 was 55%, but T. Rowe dropped 63% during this period.

The market’s level should rise over longer periods of time (as it always has), but it’s important to be aware of the potential for near-term volatility impacting business results (including assets under management and perhaps fund performance). Fortunately, T. Rowe's dividend seems likely to remain safe and moderately growing during inevitable industry downturns, just like it has for over three decades.

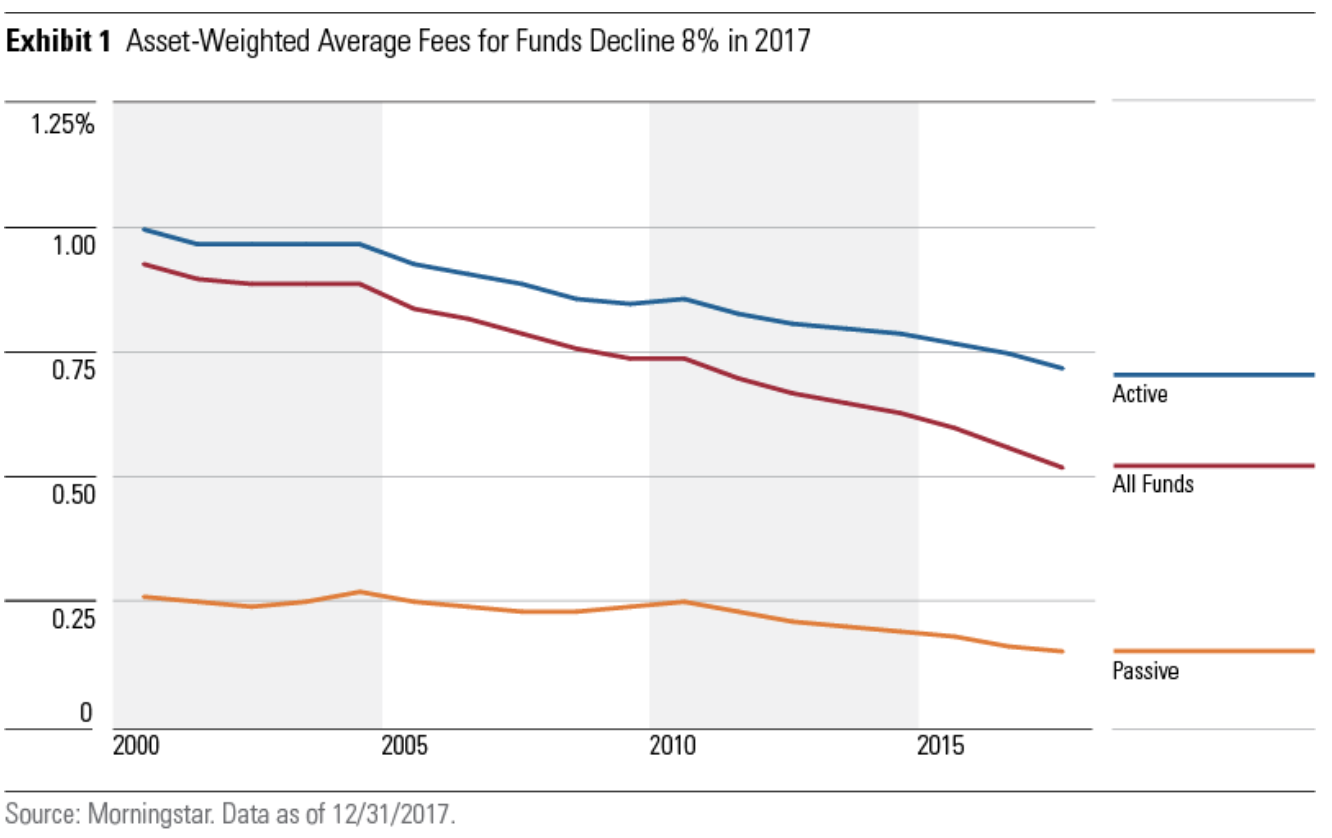

Pressure on fee revenue is a much bigger long-term concern. Passively managed mutual funds still cost just a fraction of their actively managed counterparts. While average active management fees have declined more than 25% since 2000, passive funds remain much cheaper.

In 2017, the latest data available from Morningstar's annual fund fee study, the average asset-weighted fee for active U.S. equity funds was 0.73% compared to just 0.11% for their passive counterparts.

Source: Morningstar

Thanks to their lower costs and the generally disappointing performance of many active managers, passive index funds have seen their market share double from 13.6% in 2008 to 26.6% in 2017, according to the Investment Company Institute.

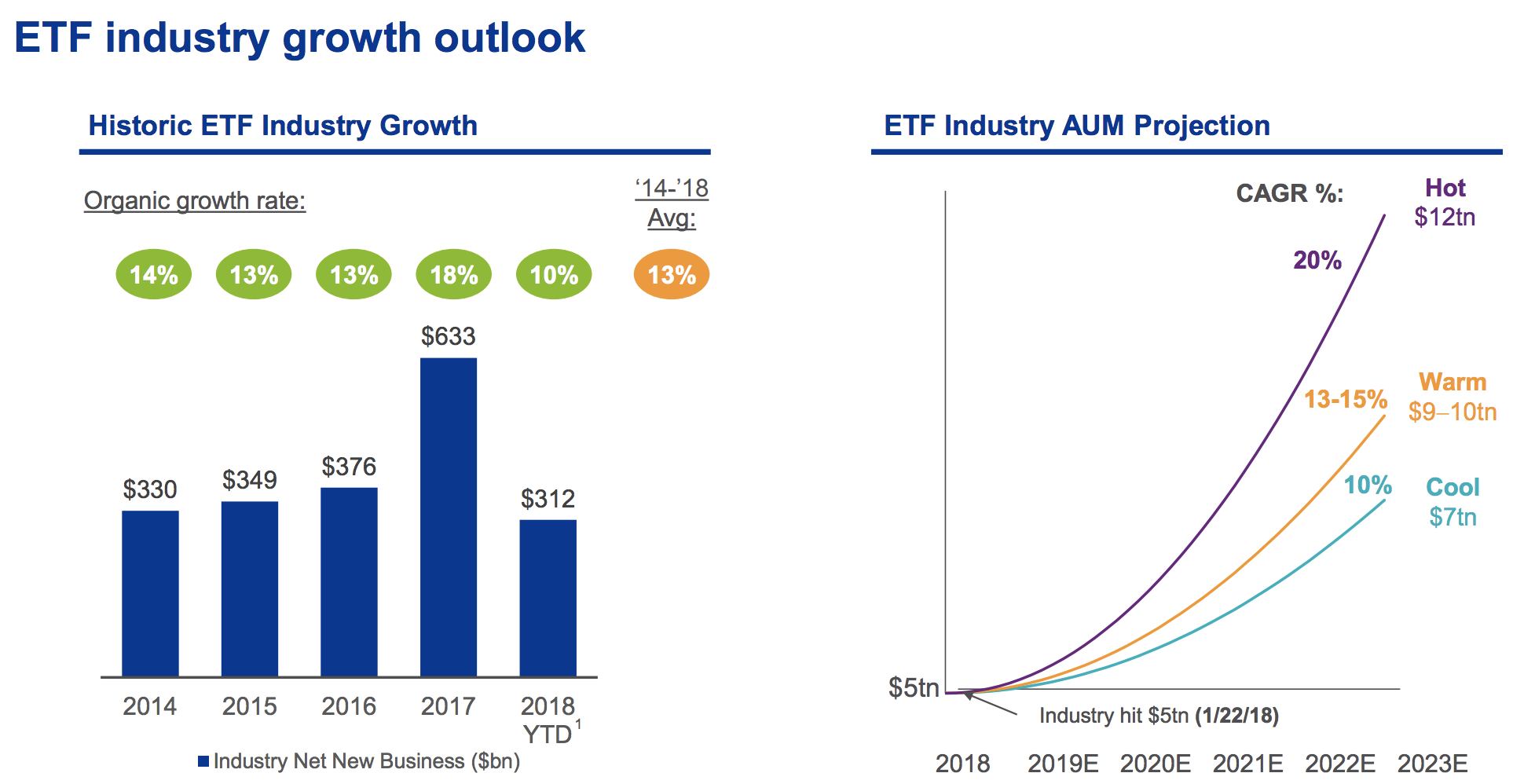

That trend is expected to continue for the foreseeable future, with asset manager BlackRock (BLK) project the ETF industry growing from $5 trillion in early 2018 to as large as $12 trillion by 2023. T. Rowe will likely face added pressure to keep its higher cost funds competitive in an environment where active mutual funds are likely to keep losing market share to passive investment vehicles.

Source: BlackRock Investor Presentation

While T.Rowe has done a relatively good job in swimming against this secular industry trend over the last few years, that's been due to the superior performance of most of its funds. As long as T.Rowe can maintain its status as an elite active manager clients are more likely to stick with it despite paying higher management fees.

However, it's very difficult for mutual fund managers to consistently outperform their peers and deliver excess returns over their passive index benchmarks. In fact, over the 15-year period ending on June 30, 2018, 92.4% or large-cap managers, 95.1% of mid-cap managers, and 97.7% of small-cap managers failed to outperform on a relative basis, according to S&P Dow Jones Indices.

If T. Rowe runs into a stretch of poor performance, then its assets under management could start declining as it loses market share to rivals and passive products, forcing it to reduce its fees in an effort to retain business.

The company's long-term track record of delivering superior returns means this risk isn't necessarily very large, but investors should still keep it in mind. At the very least, T. Rowe's performance and fees seem likely to be increasingly scrutinized by clients.

Rather than attempting to evolve its business, T.Rowe is working hard to avoid introducing hot products like smart-beta funds, robo-advisors, and other passive vehicles, because it wants to keep its focus on higher fee active funds.

In other words, T. Rowe does not have a meaningful presence in passive products to hedge its bet (only around 5% of its assets use passive index strategies, according to Forbes).

Source: Forbes

The company's focus on only its top products also creates concentration risk. For example, its top 10 mutual funds represented 29% of AUM at the end of 2018. This means that T. Rowe's continued success rests heavily on being able to avoid missteps with those particular funds, most of which rank in the top 30% of their peer groups.

Source: T. Rowe Price Investor Presentation

Even if T. Rowe Price is able to hold onto its assets better than peers, clients seem likely to continue applying downward pressure on fees over time. As this plays out, T. Rowe's high operating margin will likely face some pressure, reducing its long-term earnings and dividend growth rates compared to their historical double-digit norm.

Management changes could also impact the company's fund performance and culture, which is very important for investment firms. Brian Rogers, T. Rowe Price’s former chairman and chief investment officer, retired at the end of March 2017 after working for the company for 35 years.

T. Rowe’s CFO retired in 2017 as well, and the company’s current CEO took over only at the end of 2015. The number of key personnel changes risks shaking up the company’s culture during a fragile time for the active fund industry.

The company’s investment team has more than doubled in size since 2005 as well. Such growth comes with cultural changes that could help or hurt the company over time. For now, the company deserves the benefit of the doubt given its successful investing culture which has prevailed for nearly a century.

Closing Thoughts on T. Rowe Price

Despite some of the real pressures facing active investment managers, T. Rowe Price is likely a business that is here to stay for many years to come. However, long-term growth could be challenged by the continued migration from active to passive products, pressure on fees, cultural changes within the firm, and less robust returns from equities given today's high valuations.

The company should be able to continue paying safe and growing dividends, which is something it has done every year since its IPO in 1986. But investors considering the stock need to be comfortable with T. Rowe's sensitivity to financial markets, as well as the possibility that future growth rates will be weaker than they have been in the past.

For now, T. Rowe's solid performance relative to peers, large scale, strong reputation, and high mix of stickier retirement-focused assets are helping the company insulate itself from the worst of the passive investing movement. But like with all investments, past performance cannot guarantee future results.