Sizing Up Pfizer's Dividend Safety as Patent Losses Loom

Shares of Pfizer have slumped over 30% this year while the broader pharmaceutical industry is about flat. Shares now sport a dividend yield of 5%, representing the stock's highest yield since the depths of the pandemic.

Source: Simply Safe Dividends

Pfizer's slump reflects worries about the firm's falling Covid revenues and ability to sell enough new drugs to offset a looming revenue hole from medicines losing patent protection soon.

Starting on the Covid front, Pfizer's vaccine and treatment generated $57 billion in revenue during 2022 (more than the entire company's pre-Covid sales) but are projected to come crashing down to about $22 billion this year (31% of total sales).

Management is hopeful Covid revenue will return to growth in 2024 based on estimated vaccination rates and the ability to charge more for its vaccines in commercial markets compared to the government contracts that drove this business during the pandemic.

However, as the world continues to move past the pandemic and many of the precautionary practices it temporarily ushered in, Pfizer's forecast could prove optimistic. The more important long-term driver is Pfizer's non-Covid portfolio of medicines.

Several heavy hitters, including blood thinner Eliquis (14% of Q2 sales) and breast cancer treatment Ibrance (10%), lose patent protection over the next five years, opening them to competition from generic drugs and an estimated $17 billion of revenue losses.

Source: Pfizer Investor Presentation

Despite these hits, management expects to keep the overall business growing by adding $20 billion of revenue from commercializing Pfizer's internal pipeline and another $25 billion of sales from acquisitions from 2025 through 2030.

To maximize financial flexibility, Pfizer wisely retained the more than $30 billion of excess free cash flow it generated from Covid products rather than spending the money on buybacks.

This cash pile will help fund deals to replenish Pfizer's pipeline, including its planned $43 billion purchase of cancer drug company Seagen, which is expected to close around the end of the year and bring Pfizer much closer to its target of $25 billion in revenue from acquisitions by 2030.

Analysts aren't as optimistic about Pfizer's ability to grow Seagen and develop its own internal pipeline of medicines, though. The company has long had a reputation for being more of a marketer than a science company like rivals Merck, Eli Lilly, and Johnson & Johnson.

Albert Bourla, who took the reins as CEO in 2019, is working to change that perception. He divested Pfizer's non-science consumer businesses and increased the firm's spending on R&D.

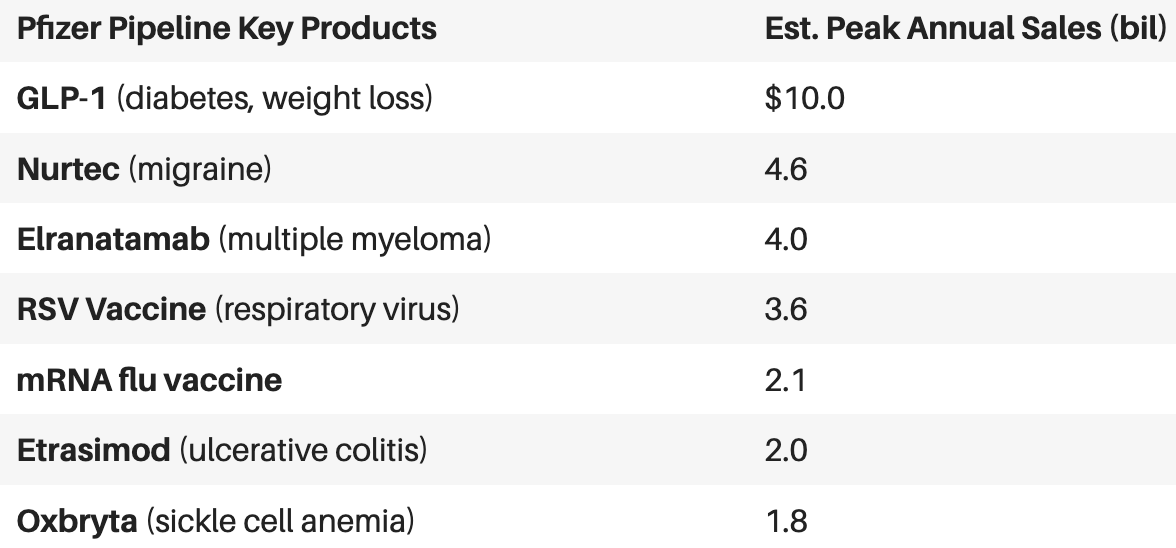

While change is hard at a company this big, these efforts could help Pfizer find success as it marches ahead with its plan to launch 19 new products and indications in an 18-month span, with most of the revenue contributions beginning in the back half of 2023.

Source: Pfizer Investor Presentation

Predicting which drugs will become the next blockbusters is never easy. But investors can take some comfort in knowing that Pfizer has spread its bets across a wide range of products, with only one new treatment expected to top $5 billion of annual sales, according to estimates from Goldman Sachs cited by Barron's.

Source: Barron's, Goldman Sach's data

Pfizer's efforts could also be aided by mRNA technology and advancements in artificial intelligence, which have potential to develop new therapies and get medicines to market faster.

The stock's relatively low expectations provide a margin of safety, too. Shares of Pfizer trade at a forward P/E ratio of 10.9, representing a meaningful discount compared to the valuation multiples enjoyed by Merck (13.6) and AbbVie (14.1).

If management executes and restores confidence in Pfizer's drug development skills and ability to navigate future revenue losses, the stock could re-rate higher.

Until then, income investors can continue banking on the drugmaker's dividend, which we expect will keep growing at a low single-digit pace with potential for faster growth in the back half of the decade.

Supporting that outlook, Pfizer appears set to maintain its A+ credit rating even after the Seagen acquisition, and the firm's payout ratio is projected to hold near 50% over the next few years after earnings finish retreating from their Covid vaccine-induced highs.

Source: Simply Safe Dividends

While Pfizer's performance has been disappointing exiting the pandemic, the company's strong balance sheet, healthy cash flow, recession-resistant products, and diversified portfolio support a stable long-term outlook.

We plan to continue holding shares of Pfizer in our Conservative Retirees portfolio and will keep monitoring the company as it navigates future patent expirations.