Shift in Client Funds from Cash to Accounts with More Yield Raises Anxiety About Schwab's Unrealized Losses

Schwab was excluded from our bank analysis shared Wednesday because traditional bank loans account for less than 10% of the firm's assets.

However, the provider of full-service investment platforms for retail investors and advisors has exposure to some of the same issues weighing on bank stocks.

Schwab launched in 1975 as one of the first discount brokers and has consistently grown its assets by taking share from wirehouse firms, banks, and other channels that have higher commissions.

Today, Schwab generates around 40% of revenue from asset management fees and trading revenue. But just over 50% of sales (up from 20% in the early 2000s) are from net interest revenue earned by investing clients' cash in safe, longer-term securities like U.S. Treasurys and agency mortgage-backed securities.

Earning much of its income by investing clients' cash (rather than charging them more fees) helps Schwab offer its customers a great platform at a low cost, attracting more assets from higher-cost channels and creating a flywheel effect.

The concern is that Schwab over the past decade has reached too far for yield by buying longer-dated securities, while its primary funding source, clients' uninvested cash, can be moved at any time.

With interest rates jumping over the past year and pounding the value of longer-term bonds, Schwab's investment securities saw their gross unrealized loss balloon from $4.9 billion in 2021 to $27.9 billion at the end of 2022.

For context, Schwab's common equity tier 1 (CET1) capital stood at $30.6 billion. CET1 capital is the most loss-absorbing form of capital since it primarily consists of a firm's common stock and retained earnings.

Unrealized investment losses are not counted against Schwab's CET1 capital because they would not be realized if the firm holds its debt investments through maturity, when safe bonds get paid back in full.

But if enough customers move their cash at the same time, Schwab could face a liquidity crunch that forces the firm to tap expensive funding sources or sell some of its securities at a loss, reducing profitability and wiping out a chunk of the company's equity.

How likely is a bank run on Schwab? Not very. Around 80% of the firm's total bank deposits fall within the FDIC insurance limits, giving Schwab one of the five highest ratios of the top 100 U.S. banks.

However, deposit outflows could still accelerate as more clients reduce their cash balances in favor of higher-yielding accounts, such as CDs and money market funds, that now yield 3% to 5%.

During the last tightening cycle from 2004 to 2007, clients' cash balances fell from 3.6% of assets to 2.2%. The decade of rock-bottom interest rates that followed caused uninvested cash balances to swell to around 6% to 7% of client assets.

Source: Simply Safe Dividends, Schwab Filings, Federal Reserve Data

With the Fed hiking rates to a similar level over an even shorter time period, the big question is where (and how quickly) uninvested cash balances will settle as more clients react to the availability of higher yielding cash alternatives.

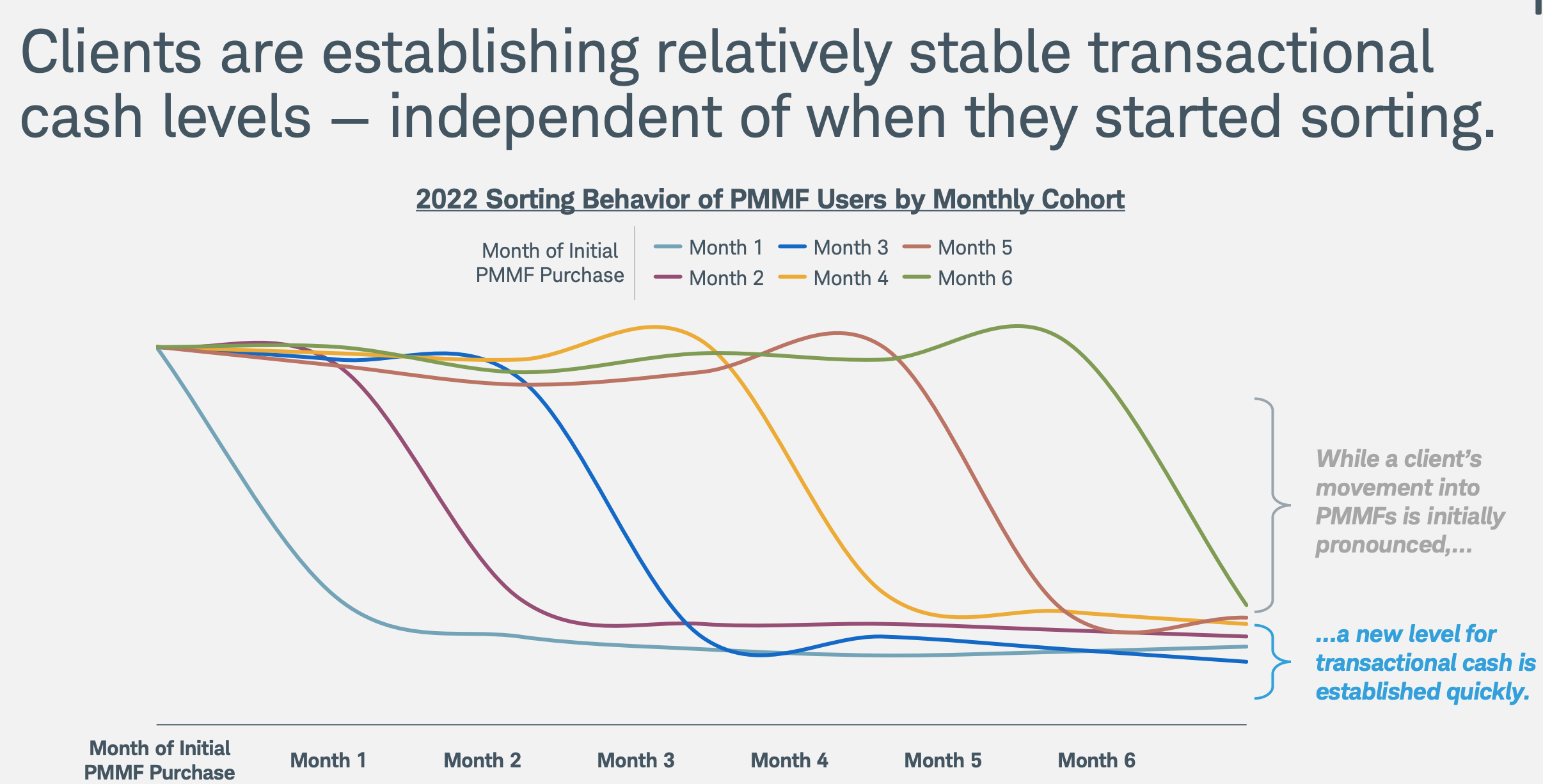

Management expects these shifts in cash, known as sorting, to abate in 2023, noting that client behavior has thus far tracked with past cycles where an initial move into money market funds takes place quickly before stabilizing.

Source: Schwab Investor Presentation

That said, if uninvested cash balances moved closer to 3.5% of client assets versus current levels near 6%, Schwab could lose $200 billion of cheap deposits – that's equivalent to nearly 40% of the firm's total assets.

There's no indication that this is happening, though. Earlier this week Schwab noted that uninvested cash outflows in March were tracking consistent with February levels, which were $5 billion lower than January.

Should the pace unexpectedly pick up, Schwab's liquidity to meet outflows includes around $25 billion of investments set to mature this year and $40 billion of cash on hand. We also estimate the company will see uninvested cash inflows of around $15 billion as new assets are gathered.

In fact, Schwab on Friday disclosed that over the past five trading days clients have brought in $16.5 billion of net new assets despite the market's turbulence (perhaps 5% to 7% of this money sits in uninvested cash).

Beyond those sources, management also believes Schwab could issue up to $8 billion in retail CDs per month and has over $300 billion of incremental capacity with the Federal Home Loan Bank and other short-term credit facilities.

That said, investors may remain anxious about Schwab's positioning until we have more clarity that uninvested cash balances, which are already down 22% since the first quarter of 2022, will not plunge further from here.

Either way, Schwab's funding costs will almost certainly increase to retain clients. During the 2004 to 2007 tightening cycle, Schwab's average funding costs rose from 0.5% to over 2% over the course of a few years.

Schwab's average yield on its assets grew at a faster pace, expanding net interest margins. But back then, duration risk wasn't an issue since available for sale investment securities with longer maturities represented 9% of total assets.

Today, Schwab's investment securities account for nearly 60% of assets. Only 25% of these securities mature within the next five years, and 55% do not mature for at least 10 years. The investment portfolio will take longer to reinvest at higher rates.

Source: Simply Safe Dividends, Schwab Filings

Depending on how fast funding costs jump, and the use of any higher-cost financing sources to meet potentially elevated cash outflows, Schwab's net interest margin could get squeezed.

Since this part of the business accounts for around half of revenues, Schwab's earnings could take a big hit if this plays out. The company's 25% payout ratio provides some margin of safety for the dividend, though. And Schwab has kept its A credit rating thus far despite the banking industry's turbulence.

Overall, we believe it is prudent to downgrade Schwab's Dividend Safety Score from Very Safe to Safe. This recognizes Schwab's large unrealized losses relative to its equity capital, plus the possibility of an earnings squeeze if uninvested cash balances contract and funding costs rise much faster than management expects.

If cash deposits showed signs of shrinking at a less manageable pace or regulators decided to force firms like Schwab to begin counting unrealized losses against their capital, we would consider another downgrade.

Otherwise, Schwab feels less scary to us than the higher-risk regional banks we highlighted earlier this week.

We will keep an eye on Schwab's performance and provide updates as needed.