B&G Foods (BGS) Faces Heightened Risk of Dividend Cut

Rising interest rates, substantial raw material inflation, and tighter consumer spending have increased the odds that B&G Foods will need to cut its dividend to protect its balance sheet.

In recognition of these mounting headwinds, we are downgrading B&G's Dividend Safety Score from Unsafe to Very Unsafe.

B&G has historically generated strong and consistent free cash flow to support its large dividend, which has been paid without interruption since 2004 except for a 20% cut in 2008.

However, the company's profitability has proven less predictable in recent years as B&G's sales mix and raw material dependences have evolved.

B&G in 2020 acquired Crisco, a shortening and vegetable oil maker that accounts for close to 15% of the company's sales, making it B&G's second-largest brand.

Crisco has encountered much higher cost inflation than the rest of B&G's portfolio as soybean oil, the primary input for the business, has doubled in price since the acquisition was announced.

Soybean oil accounts for 40% of B&G's commodity exposure due to Crisco. With the war in Ukraine dragging on, it's hard to say when prices may come down since Russia and Ukraine are among the 10 largest soybean producers and exporters.

Meanwhile, Green Giant, B&G's largest brand accounting for around 25% of sales since being acquired in 2015, brings its own challenges producing frozen and shelf-stable vegetables.

Peas and broccoli are among B&G's top raw material exposures thanks to Green Giant. Disruption caused by the Ukraine-Russia war has led farmers to shift their crop planning in response to record high prices in soybeans and corn.

This has resulted in more expensive vegetable planting contracts for Green Giant's core crops with less supply available.

Along with a jump in freight and delivery costs due to higher oil prices, B&G's overall portfolio is tracking for total inflation near 20% this year. Margins look set to continue their steady decline.

Source: Simply Safe Dividends

B&G hopes to improve its margins with price increases kicking in over the next year.

But this could prove challenging since B&G invests so little behind its brands compared to peers, and more shoppers may trade down to private label alternatives if the economy slows further.

The company's payout ratio sits at a dangerous level barring a swift recovery in earnings, which we view as unlikely in the current environment.

Source: Simply Safe Dividends

Surging interest rates are another challenge to profits since the B- rated company maintains high leverage and around 40% of B&G's debt has floating rates.

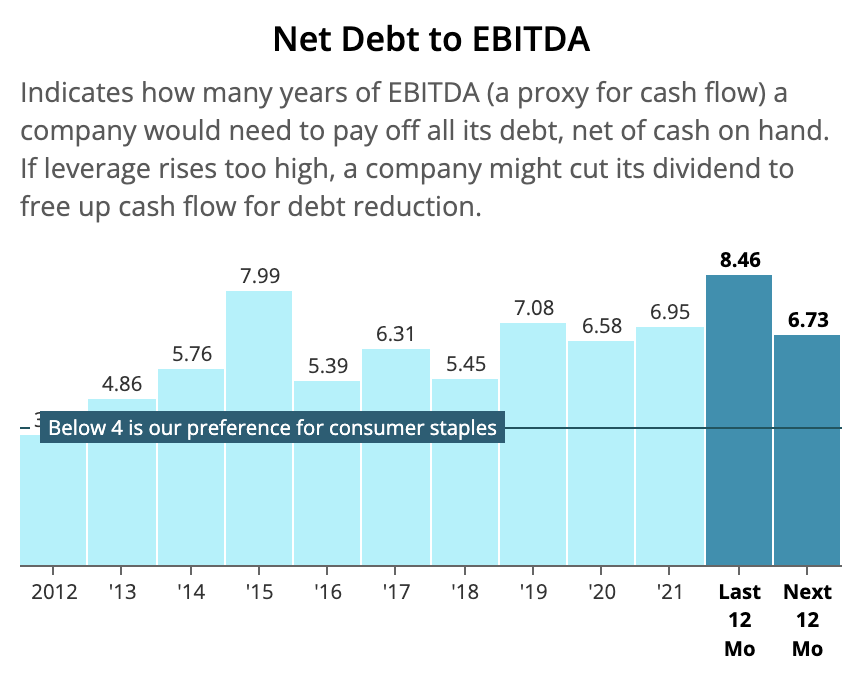

It's also worth noting that B&G's net debt to EBITDA leverage ratio sits above the 5.2x level it recorded before the company's 2008 dividend cut.

Source: Simply Safe Dividends

Management has expressed interest in potentially making "select asset divestitures" to help deleverage the business.

While this would help the balance sheet, losing the cash flow provided by any brands that are sold would further strain B&G's dividend coverage.

Overall, the one-two punch of inflation and rising interest rates has made B&G's dividend more vulnerable.

We believe a 30% to 50% dividend cut would be prudent to protect B&G's balance sheet and better align the payout with the firm's current cash flow generation.

Shares of B&G would still yield at least 6% to 8% following a dividend reduction of that magnitude. However, we believe investors would be better served owning companies with healthier balance sheets.