2026 Monthly Dividend Stocks List: All 75 Ranked and Analyzed

Monthly dividend stocks can provide predictable income and make budgeting easier because they pay dividends every month of the year.

Most companies distribute dividends quarterly. Today, 75 stocks pay dividends monthly, and many of them offer dividend yields above 7%.

If you want to learn more about how this approach works in practice, check out our video on building a portfolio made up entirely of monthly dividend stocks, including the pros and cons of this strategy.

If a list is more your style, the table below includes every monthly dividend stock with up-to-date dividend yields and Dividend Safety Scores™.

Monthly dividend stocks without Dividend Safety Scores™ are typically micro-caps and or trade over-the-counter, which can make them less appropriate for most investors.

Below the table, you will find our analysis of every company that pays dividends monthly, ranked from our most to least favorite.

2026 Monthly Dividend Stocks List

Ranking the Best Monthly Dividend Stocks

We analyzed all dividend stocks that pay monthly, starting with some of the most popular companies for regular income.

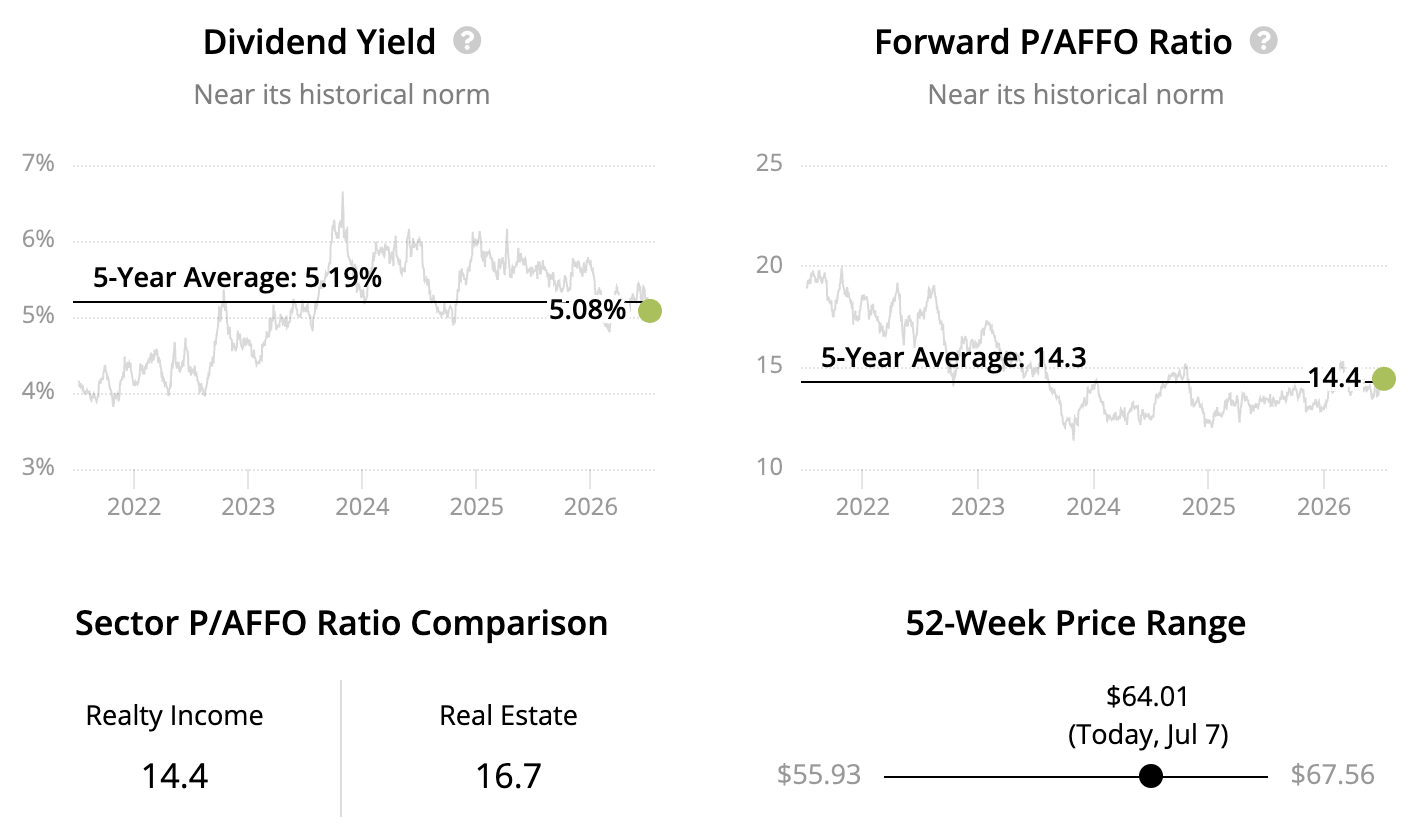

The most popular monthly dividend stock on our list, Realty Income (O) has been paying dividends since 1969 and has built a reputation as one of the more durable income stocks across market cycles.

The large-cap net lease REIT owns a massive portfolio of single-tenant properties diversified across a wide range of tenants and industries.

Realty Income generates most of its rent from tenants that have a service, non-discretionary, or low price point element to their business, providing some insulation from e-commerce. And a meaningful portion of its rent comes from tenants with investment-grade credit ratings.

Source: Realty Income Investor Presentation

Coupled with premium locations and long-term lease agreements, Realty Income has historically maintained very high occupancy, even during major downturns.

With an investment-grade balance sheet, broad access to capital, and a diversified portfolio properties, Realty Income appears positioned to continue its long track record of paying higher monthly dividends every year since 1994.

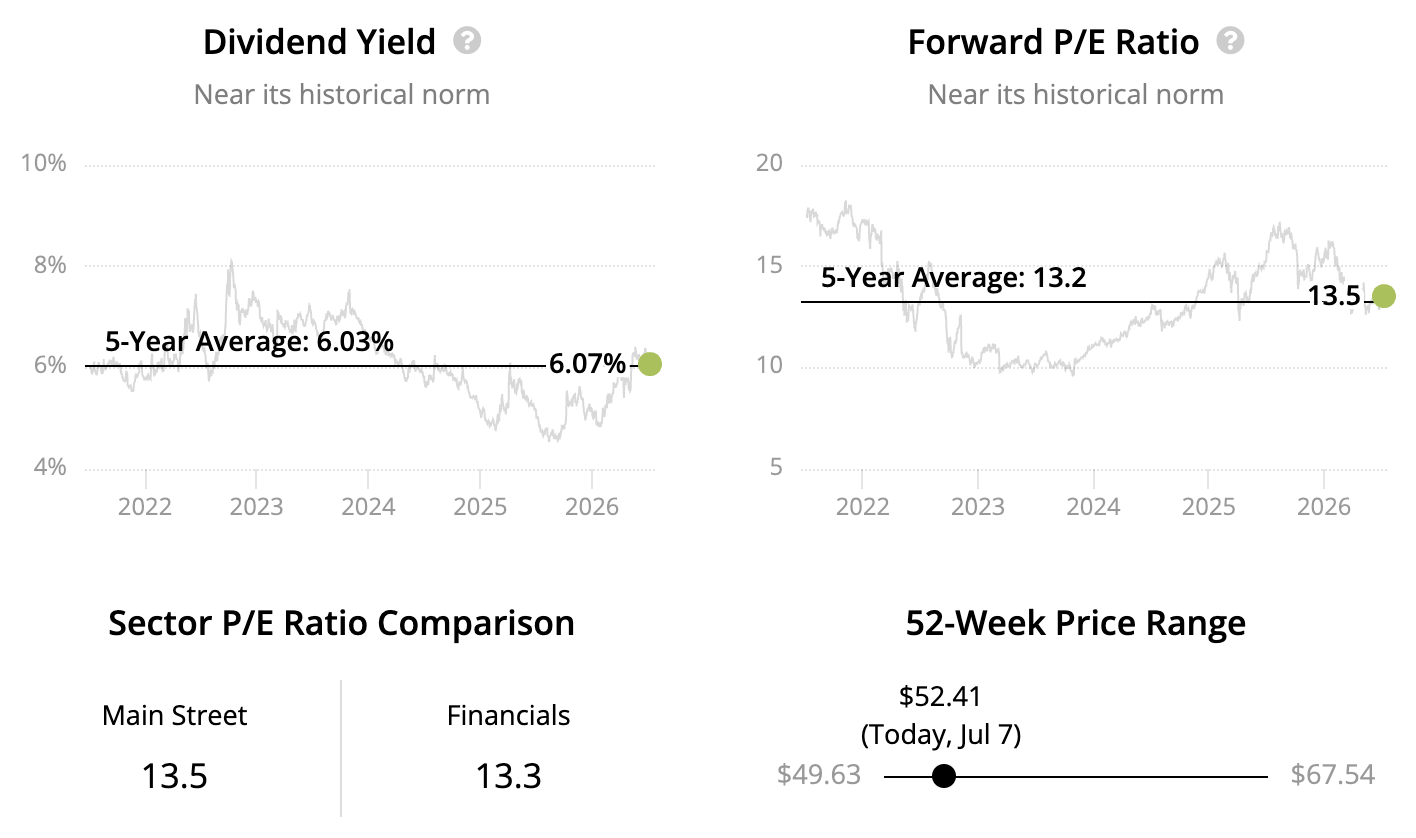

Sector: Financials – Business Development Companies Dividend Yield: 6.1% Dividend Safety Score: Safe Uninterrupted Dividend Streak: 18 years

Main Street Capital's (MAIN) roots trace back to the mid-1990s, making the internally-managed business development company (BDC) one of the oldest and largest in the industry. The firm is also one of the best high dividend stocks.

Unlike most of its peers, Main Street has a strong record of supporting its regular monthly dividend through multiple cycles, including periods when many BDCs were forced to reset payouts.

The firm’s success starts with diversification. Main Street's portfolio includes loans and equity investments across a large number of companies, which helps limit the damage from any single credit problem.

With no single investment dominating income and industry exposure generally kept in check, Main Street reduces the risk that one troubled corner of the economy derails results.

Source: Main Street Investor Presentation

Management also focuses on first-lien secured loans, which get paid first in the event of a default and allow Main Street to seize property if its loans are not repaid. This provides some protection against major loan losses during downturns.

The BDC takes a disciplined approach to leverage as well, holding much less debt than is allowed by regulators. Coupled with a relatively conservative portfolio, Main Street earns a BBB- investment grade credit rating.

The firm's monthly dividend enjoys a final layer of protection from funds Main Street retains after exiting a successful investment.

These funds, known as spillover, provide an offset against the inevitable credit losses that will be experienced when making investments in subprime debt securities.

Overall, Main Street is one of the few monthly dividend stocks to earn a Safe Dividend Safety Score and may be considered by income investors who are comfortable with the BDC industry's cyclicality.

Source: Simply Safe Dividends

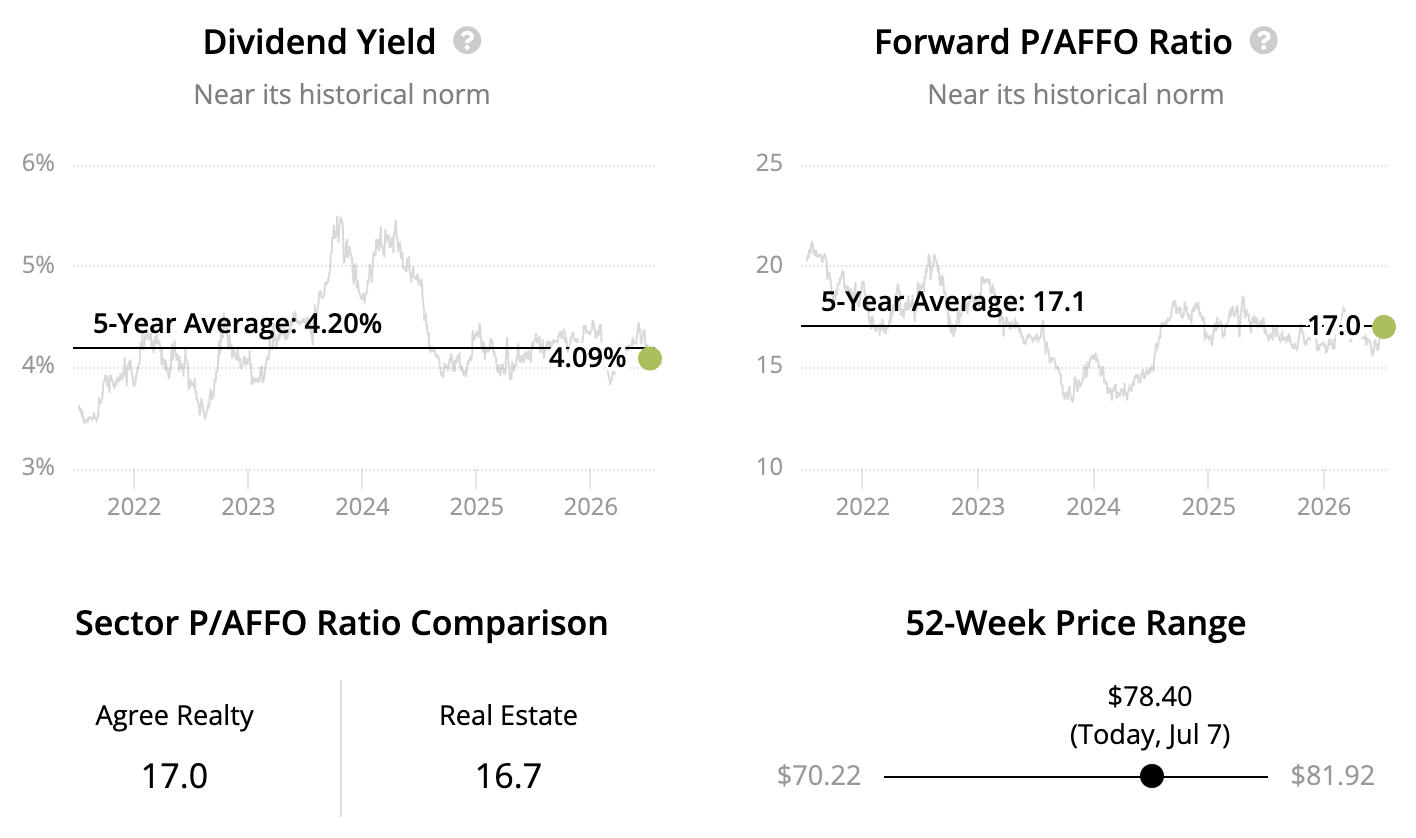

Founded in 1971, Agree Realty (ADC) owns over 2,000 free-standing, single-tenant properties leased primarily to national retailers with investment-grade credit ratings.

Some of the mid-cap REIT's largest tenants include Walmart, Dollar General, Best Buy, TJX, and CVS. No tenant exceeds 6% of rent, with only Walmart topping 5% of ADC's revenue.

Source: ADC Investor Presentation

ADC also diversifies across retail industries, with none accounting for more than 10% of rent. The portfolio focuses on essential businesses more resilient to e-commerce, such as tire and auto service, grocery stores, home improvement, and convenience stores.

Doing business with a diversified set of mostly essential, creditworthy retailers helped ADC collect nearly 90% of rent during the depths of the pandemic, one of the best records of any retail REIT.

Management runs the business with conservative financial practices as well, including moderate leverage and strong dividend coverage. These qualities earn Agree Realty a BBB+ credit rating and should help the monthly dividend stock continue growing its payout in the years ahead.

Source: Simply Safe Dividends

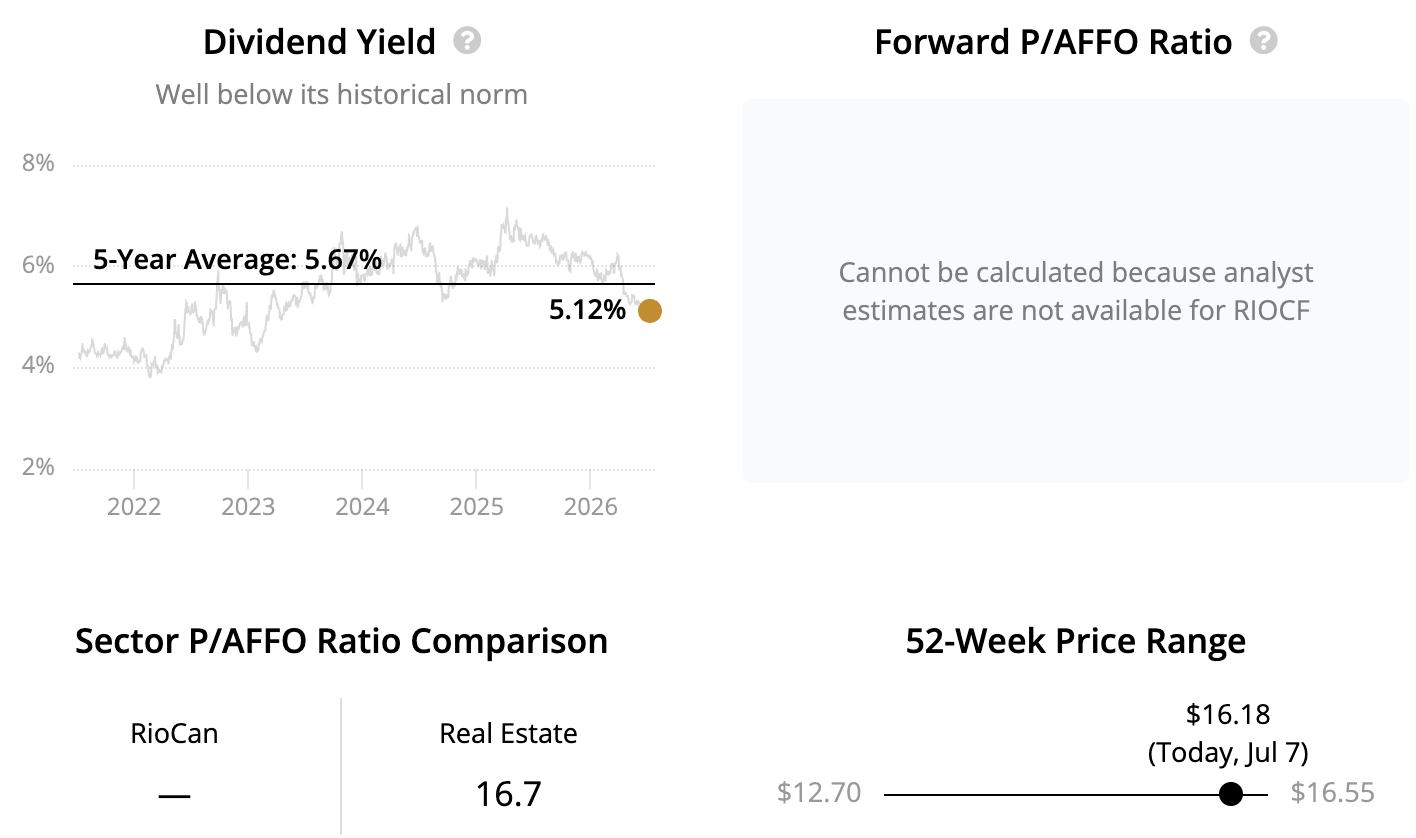

RioCan (RIOCF), one of Canada's largest REITs, owns over 150 shopping centers and mixed-use properties located in large, high-density markets such as Toronto, Ottawa, and Calgary.

Source: RioCan Investor Presentation

Just over half of the company's revenue is derived from grocery-anchored shopping centers, which provide a consistent source of foot traffic for adjacent retail tenants.

In total, management estimates that around 85% of the mid-cap REIT's rent comes from tenants with "stable rent-paying ability, strong covenants, and sustained foot-traffic."

Examples include essential personal services, grocery, pharmacy and liquor stores, and value retailers.

This focus helped the company maintain high occupancy and pay uninterrupted dividends since 1994 until the 2020 pandemic forced a 33% payout cut when many retailers fell on hard times and stopped paying rent.

RioCan's monthly dividend, which is likely to grow at a mid-single-digit rate to keep pace with cash flow growth, should be on more solid ground going forward.

The company's payout ratio sits at its lowest level in at least a decade, supporting its development and acquisition plans.

Overall, RioCan's focus on grocery-anchored shopping centers, mixed-used properties, and Canada's largest markets should insulate the retail REIT from e-commerce pressures and help the firm pay a reliable monthly dividend.

Source: Simply Safe Dividends

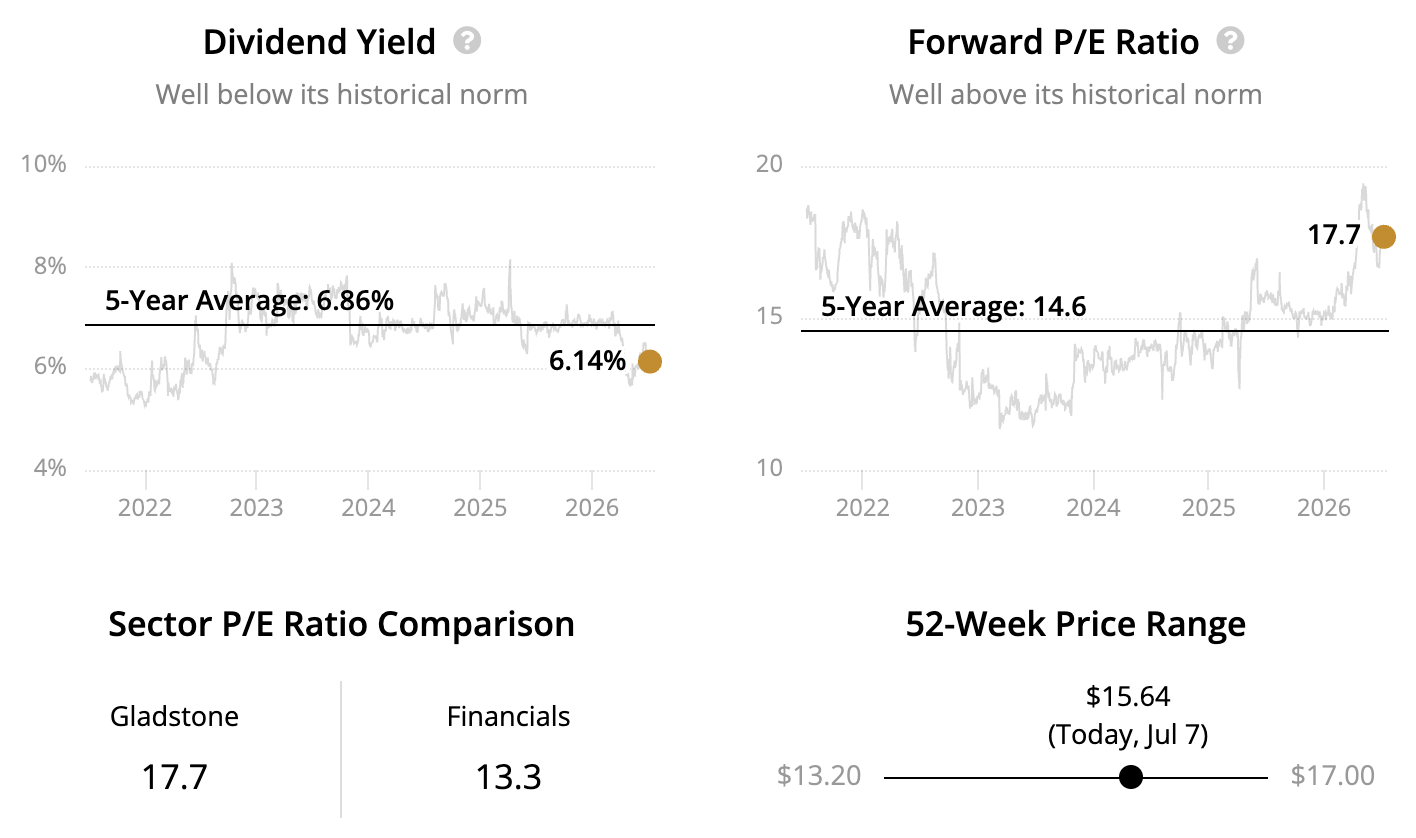

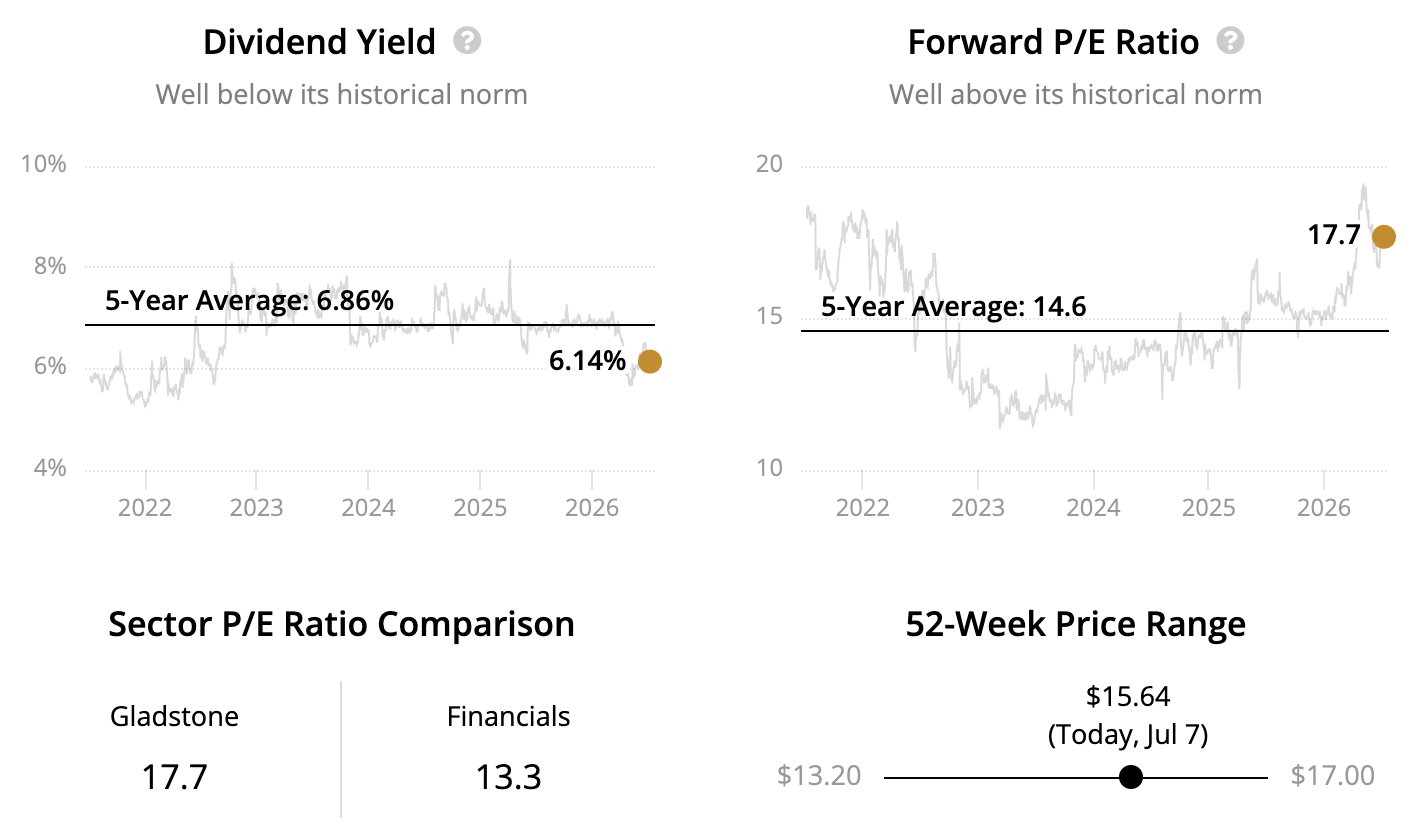

Sector: Financials – Business Development Companies Dividend Yield: 6.1% Dividend Safety Score: Borderline Safe Uninterrupted Dividend Streak: 15 years

Gladstone Investment Corporation (GAIN) formed in 2005 as an externally-managed business development company (BDC) providing equity and secured debt financing to small private businesses.

Unlike most of its peers which prioritize loan investments, equity securities account for over 30% of the small-cap BDC's portfolio. This provides Gladstone Investment with more upside in the management buyout transactions it helps fund.

Equity investments are riskier, but the firm bases its monthly dividend on interest income earned from its loan portfolio, which consists primarily of first-lien secured debt that gets paid back first if a borrower defaults.

This has helped Gladstone Investment pay uninterrupted dividends since 2010 while frequently paying out supplemental dividends tied to capital gains on investment exits.

Investors should note that the BDC's portfolio consists of only around 50 companies spread across just over a dozen industries, providing limited diversification compared to many of its peers.

Source: GAIN Investor Presentation

However, management participates on the boards of its portfolio companies to help drive value creation and takes a long-term approach.

Management also focuses on established, cash-flow positive businesses rather than early-stage companies and runs the BDC with relatively low leverage to reduce risk.

Despite its smaller size and higher mix of equity holdings, Gladstone Investment has proven over time to be one of the better managed BDCs with a solid performance track record.

Source: Simply Safe Dividends

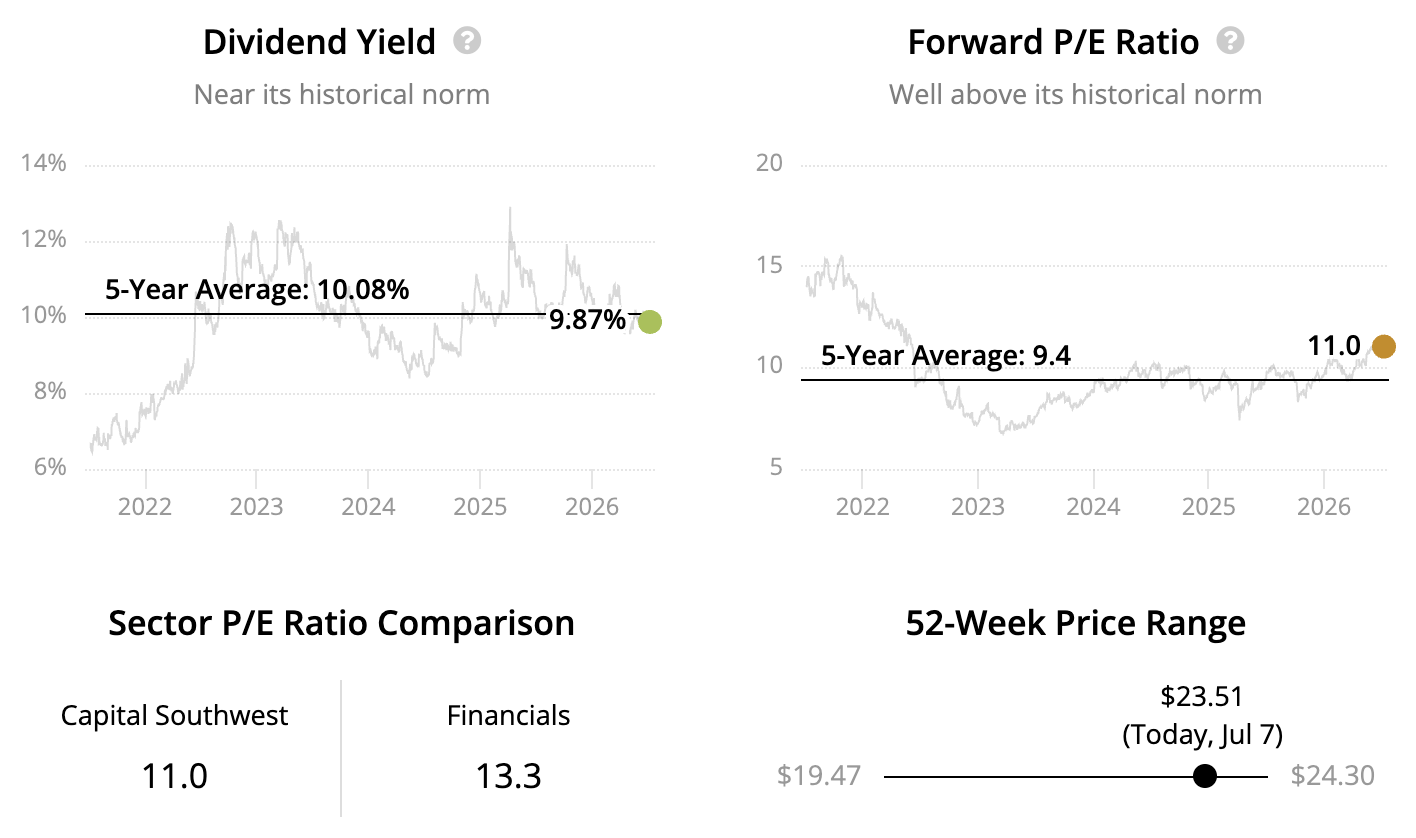

Monthly Dividend Stock #6: Capital Southwest

Sector: Financials – Business Development Companies Dividend Yield: 9.9%

Dividend Safety Score: Borderline Safe Uninterrupted Dividend Streak: 9 years

Founded in 1961, Capital Southwest (CSWC) is an internally-managed BDC that lends primarily to lower middle-market companies. The firm focuses on first-lien loans, meaning it gets paid back first if a borrower runs into trouble, which helps reduce risk compared to lenders that sit further down the capital structure.

The portfolio is spread across more than 100 companies with limited exposure to any single industry, helping avoid heavy reliance on one area of the economy.

Capital Southwest has also built a meaningful reserve of undistributed income from past investment gains. This “"spillover" can be used to help support the regular dividend during tougher periods, giving management added flexibility across economic cycles.

A conservative balance sheet and leverage well below regulatory limits support the firm's investment-grade credit rating from S&P, too.

Combined with its internally-managed structure, which keeps expenses lower and aligns management with shareholders, these qualities make Capital Southwest one of the more disciplined monthly-paying BDCs, though it still carries the normal risks associated with lending to smaller businesses.

Source: Simply Safe Dividends

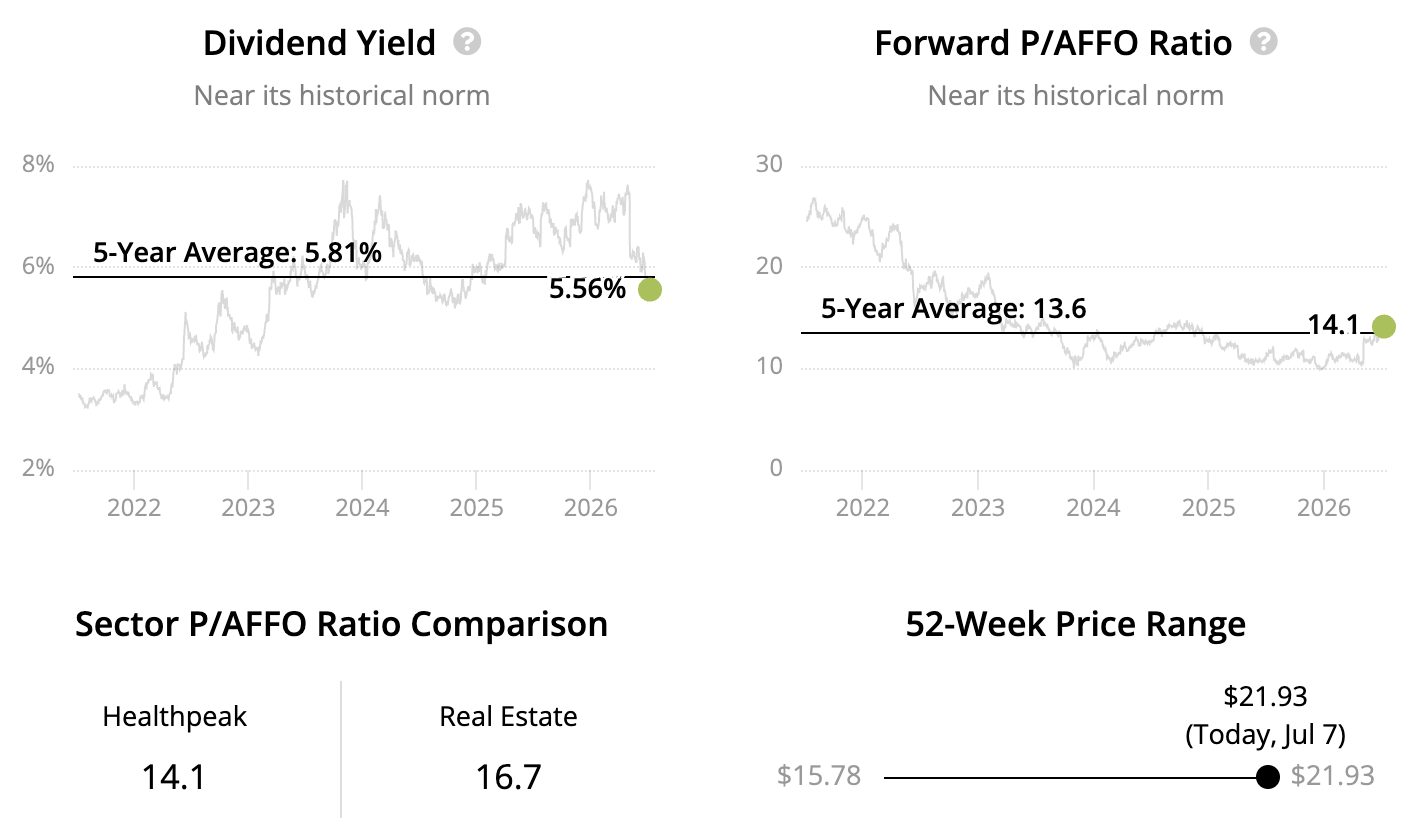

Monthly Dividend Stock #7: Healthpeak Properties

Sector: Real Estate – Health Care REITs Dividend Yield: 5.6%

Dividend Safety Score: Borderline Safe Uninterrupted Dividend Streak: 4 years

Founded in 1985, Healthpeak Properties (DOC) switched from quarterly to monthly dividends in early 2025.

Prior to that, the healthcare REIT underwent a transformative merger with Physicians Realty in 2024 to transition away from senior housing (~10% of rent) toward life science facilities (~50%) and medical office buildings (~40%).

Life science and medical office buildings (MOBs) typically attract higher-credit-quality tenants and have longer lease terms, higher margins, and better growth prospects than senior housing.

Private investors and government funding provide strong financial backing for the biotech and pharmaceutical firms occupying many of Healthpeak's life science facilities, boosting confidence in their ability to meet rental obligations.

Meanwhile, the trend of health systems moving outpatient care outside hospitals is driving demand for medical office buildings, which require modern, conveniently located spaces to meet growing patient needs.

Coupled with the aging population's growing demand for outpatient care and the REIT's strong tenant base and mission-critical properties, Healthpeak looks like one of the more reliable monthly payers.

Source: Simply Safe Dividends

Monthly Dividend Stock #8: Gladstone Land

Sector: Real Estate – Specialized REITs Dividend Yield: 6.1%

Dividend Safety Score: Unsafe Uninterrupted Dividend Streak: 11 years

With roots tracing back to 1997, Gladstone Land (LAND) is an externally-managed agricultural REIT which owns more than 150 farms across over a dozen states.

The company's farms are leased to more than 90 farming tenants who grow about 60 different types of mostly specialty crops (rather than commodities such as corn and soybeans).

Leases run up to 10 years, and the farmers are typically responsible for covering property insurance, maintenance, and taxes. Over 90% of revenue was historically from fixed rent payments, with most of the rest from revenue-sharing agreements tied to a farm's crop sales.

However, that percentage will decline to around 80% this year as more farms transition to participation-based agreements. This shift is happening with farmers struggling to keep up with rent payments amid declining crop prices, drought conditions, rising input costs, and higher interest rates.

Adding to these pressures are growing concerns that government subsidies may shrink and that access to affordable immigrant labor – critical for many farms – could become even more constrained.

To help struggling farmers stay in business, Gladstone Land is adjusting some leases by reducing or eliminating fixed rent payments in favor of a share of future crop revenues.

This has pushed the REIT's payout ratio above 100%, where it will remain until market conditions improve or the dividend is ultimately right-sized. Coupled with Gladstone Land's small size and external management structure, conservative income investors may prefer to look elsewhere for ideas.

Source: Simply Safe Dividends

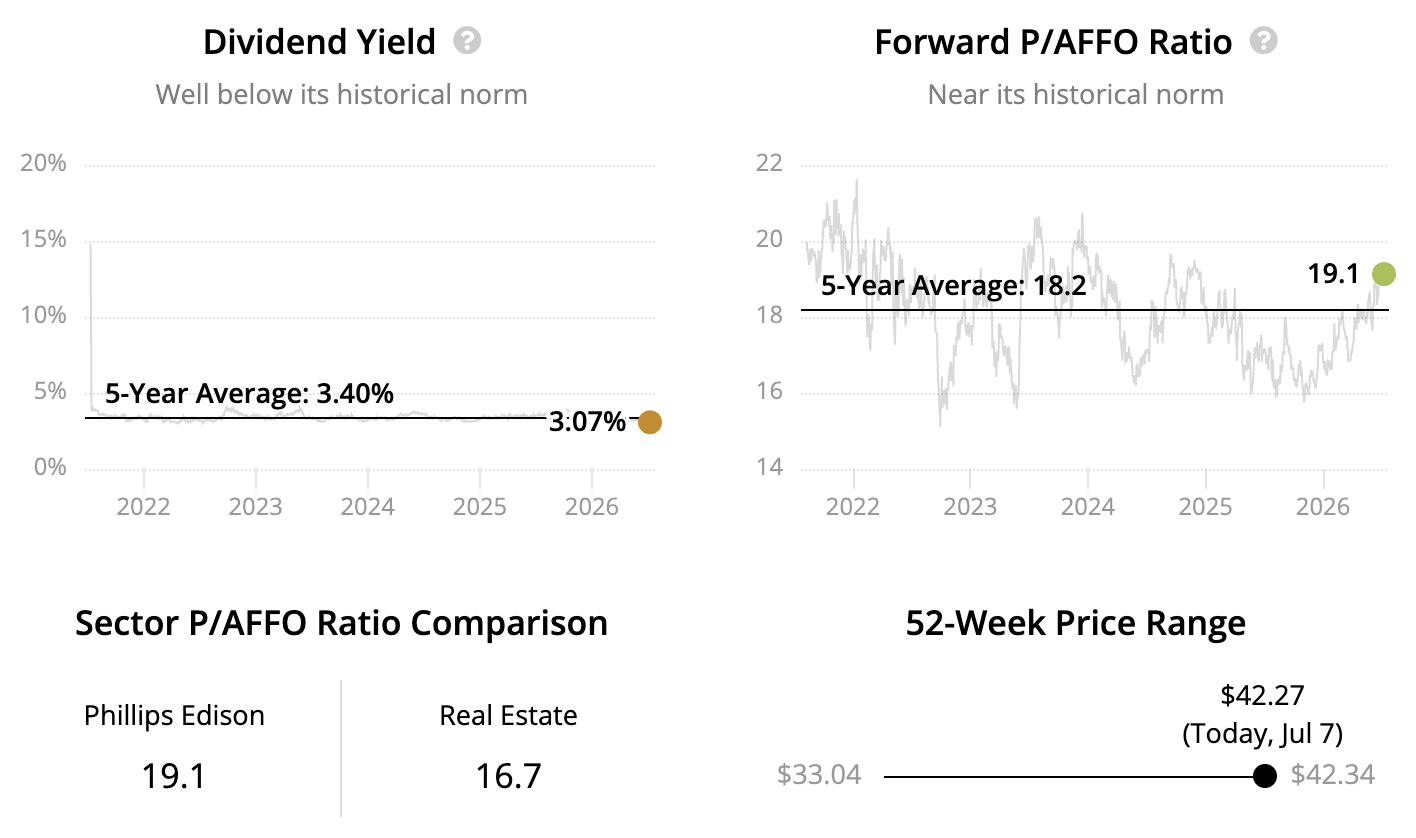

Founded in 1991, Phillips Edison (PECO) owns over 300 grocery-anchored shopping centers located in secondary or suburban markets, with the Sun Belt region driving roughly half of rent.

The midsized retail REIT has a short track record having gone public in 2021, but PECO looks like one of the more reliable stocks that pay monthly dividends.

Grocery chains such as Kroger, Publix, and Albertsons account for around 20% of PECO's rent, providing a stable source of cash flow and reliable foot traffic for surrounding tenants, none of which account for more than 2% of rent.

Source: PECO Investor Presentation

Management also estimates that roughly 70% of PECO's rent comes from tenants providing necessity-based goods and services, providing some insulation from the continued rise of online shopping.

With high occupancy, a conservative payout ratio, dependable rental income (net operating income fell just 4% in 2020 during the pandemic), and a BBB credit rating, PECO looks poised to keep its monthly dividend safe and growing.

Source: Simply Safe Dividends

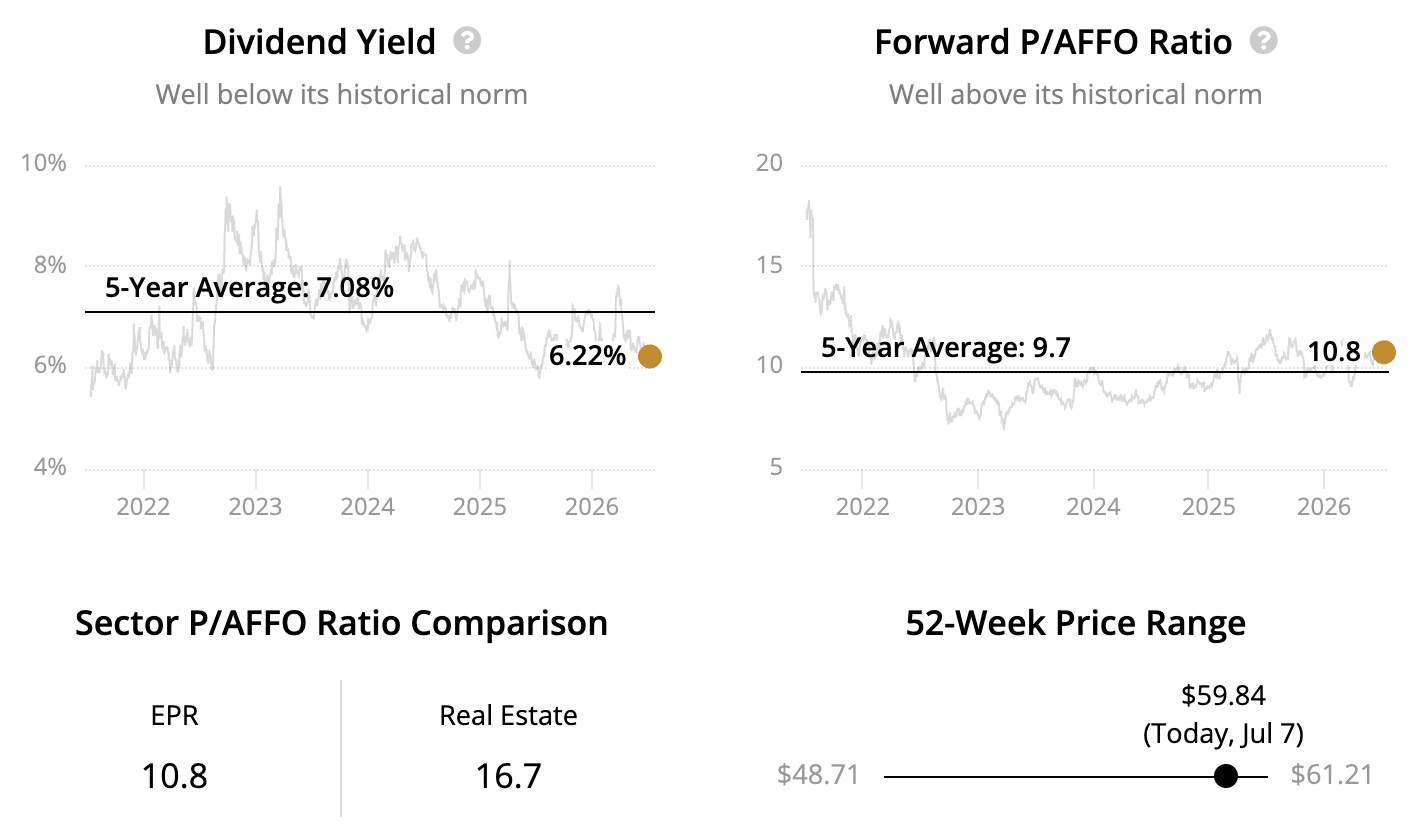

Monthly Dividend Stock #10: EPR Properties

Sector: Real Estate – Experiential REITs Dividend Yield: 6.2% Dividend Safety Score: Borderline Safe Uninterrupted Dividend Streak: 4 years

Formed in 1997, EPR Properties (EPR) owns over 350 experiential properties including movie theaters (around 35% of rent), eat and play concepts such as Top Golf and indoor karting (over 20% of rent), waterpark and amusement parks, skiing, lodging, and casinos.

Source: EPR Website

The 2020 pandemic forced many of these properties to temporarily close. EPR suspended its dividend for almost one year in response, marking the REIT's second dividend cut since it began making payouts in 1998.

The other cut occurred during the 2008-09 financial crisis. During recessions, consumers cut back on discretionary purchases, including many of the experiences offered at EPR's properties.

This can strain the financial health of EPR's tenants, many of which have junk credit ratings such as AMC and Top Golf (each over 10% of EPR's total rent).

EPR must also contend with an uncertain long-term outlook for movie theaters as streaming challenges the traditional box office business model.

The company's theaters enjoy some insulation from this trend as most of them serve food and beverages, have quality locations, and sit in the top half of theaters nationwide for box office revenue generated.

Looking ahead, EPR expects to diversify its tenant and industry concentration through acquisitions, with hopes to materially shrink its exposure to movie theaters.

This would lower the risk of EPR's rental revenue stream, which otherwise enjoys stability thanks to the REIT's long-term triple-net leases.

But given the cyclicality of EPR's tenants and their generally suspect credit profiles, investors considering EPR for its monthly dividend need a strong stomach for risk when the tide goes out.

Source: Simply Safe Dividends

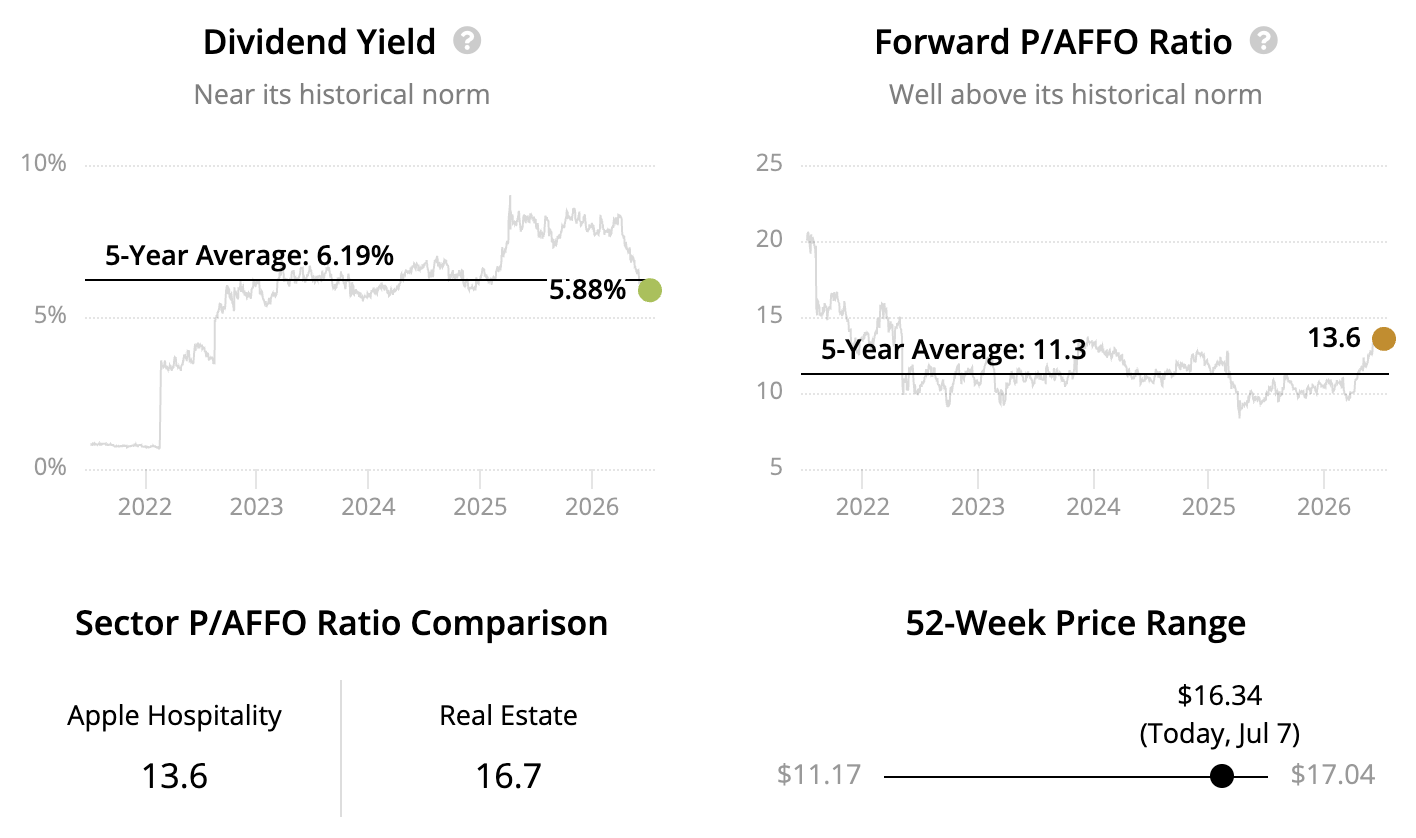

Apple Hospitality (APLE) formed in 2007 and owns over 200 hotels located across more than 30 states.

The mid-cap REIT's hotels contract with third-party hotel management companies, primarily Marriott and Hilton, to operate their locations.

Source: Apple Hospitality Website

Most REITs receive fixed rent payments from their tenants, insulating their cash flow from underlying trends in the industries they serve.

Apple Hospitality and most hotel REITs are different. The company is directly exposed to the operating results of its properties, with revenue driven by hotel occupancy and room rates.

Similarly, Apple Hospitality foots the bill for direct room operating expenses, marketing, utilities, maintenance and renovation costs, and management fees paid to Marriott and Hilton.

Coupled with the cyclical nature of the lodging industry, this high-fixed-cost business results in volatile cash flow over a full economic cycle.

When the pandemic struck, sapping demand for travel and events, Apple Hospital suspended its dividend for nearly two years as revenue plunged more than 50%.

The next downturn is unlikely to be as harsh as the pandemic was for hotel REITs. But income investors still need a strong stomach for volatility to hold these businesses.

For those who are comfortable with the lodging industry's risks, Apple Hospitality is one of the better REITs in the space with relatively newer properties, an association with trusted hotel brands, geographical diversification, and a decent balance sheet.

Source: Simply Safe Dividends

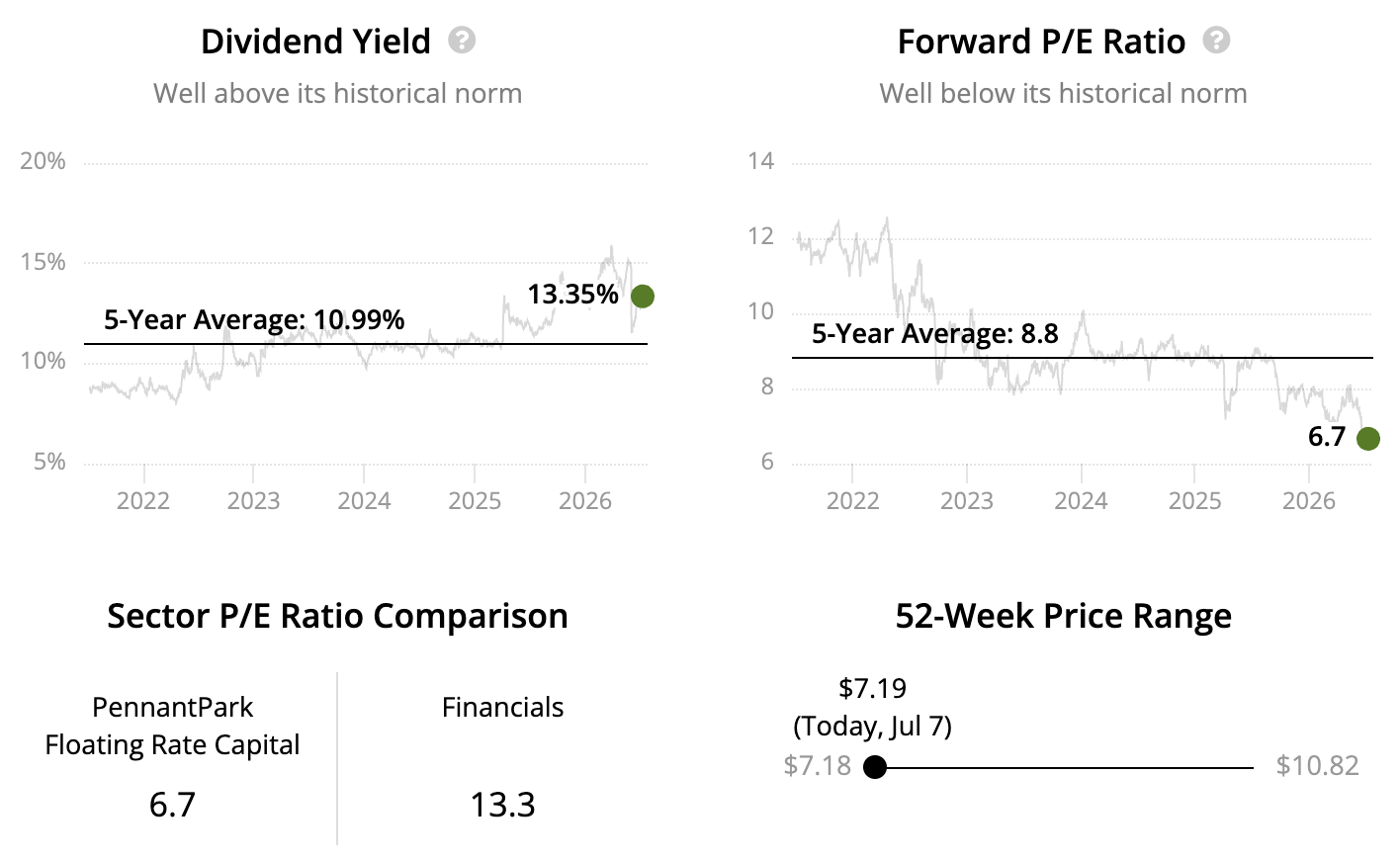

Monthly Dividend Stock #12: PennantPark Floating Rate Capital

Sector: Financials – Business Development Companies Dividend Yield: 13.4% Dividend Safety Score: Unsafe Uninterrupted Dividend Streak: 14 years

PennantPark Floating Rate Capital (PFLT) has paid uninterrupted dividends since going public in 2011, giving the externally-managed business development company (BDC) one of the best dividend track records in its industry.

PennantPark lends to somewhat smaller companies compared to most of its peers. While these businesses can be more likely to default during downturns, management mitigates this risk with the types of investments the firm pursues.

First lien senior secured debt accounts for the vast majority of PennantPark's portfolio. These loans are paid back first when a borrower defaults, and most of PennantPark's loans have covenants which further help protect the firm's capital.

PennantPark's portfolio spans more than 100 companies, with a strong focus on less cyclical industries such as business services, consumer, government services and defense, healthcare, and software and technology.

Management targets high-growth businesses in these areas. In many cases, PennantPark is part of the first institutional capital into a company where a founder is selling their business to a private equity firm, which provides equity support as it seeks to grow the firm.

With the opportunity to make an equity co-investment in many of these deals, PennantPark can participate in the upside of these deals. All of its loans have floating rates as well, lifting the firm's net investment income when interest rates rise.

Overall, PennantPark has a solid operational track record and maintains a diversified portfolio invested in securities with more protection from loan defaults. Income investors considering the stock still have to be comfortable with the BDC industry's cyclicality, though.

Source: Simply Safe Dividends

Monthly Dividend Stock #13: Gladstone Commercial

Sector: Real Estate – Diversified REITs Dividend Yield: 9.6% Dividend Safety Score: Unsafe Uninterrupted Dividend Streak: 2 years

Gladstone Commercial (GOOD) had paid uninterrupted dividends since 2004 until management surprised many investors with a 20% cut in January 2023. Simply Safe Dividends had assigned the firm an UnsafeDividend Safety Score™ leading up to the cut announcement.

The small-cap, externally-managed REIT was formed in 2003 and owns over 130 industrial and office properties leased to more than 100 different tenants in around 20 industries.

Source: Gladstone Commercial Investor Presentation

Despite the firm's relatively small size, Gladstone Commercial's portfolio is reasonably diversified with no tenant exceeding 6% of total rent and no industry exposure greater than 15%.

Management has also done a nice job filling the REIT's properties with creditworthy tenants. Since 2003, occupancy has not dipped below 95%, and only six tenants have defaulted across the 100-plus properties Gladstone Commercial has invested in.

That said, Gladstone Commercial has run its business with aggressive financial policies. Prior to the January 2023 payout reduction, the REIT's dividend regularly exceeds the firm's adjusted funds from operations (AFFO), a metric that is similar to free cash flow for REITs. And leverage has held at a high level.

These qualities reduce Gladstone Commercial's margin of safety to maintain its payout in the event of any unexpected weakness, making the stock less appropriate for conservative income investors.

Source: Simply Safe Dividends

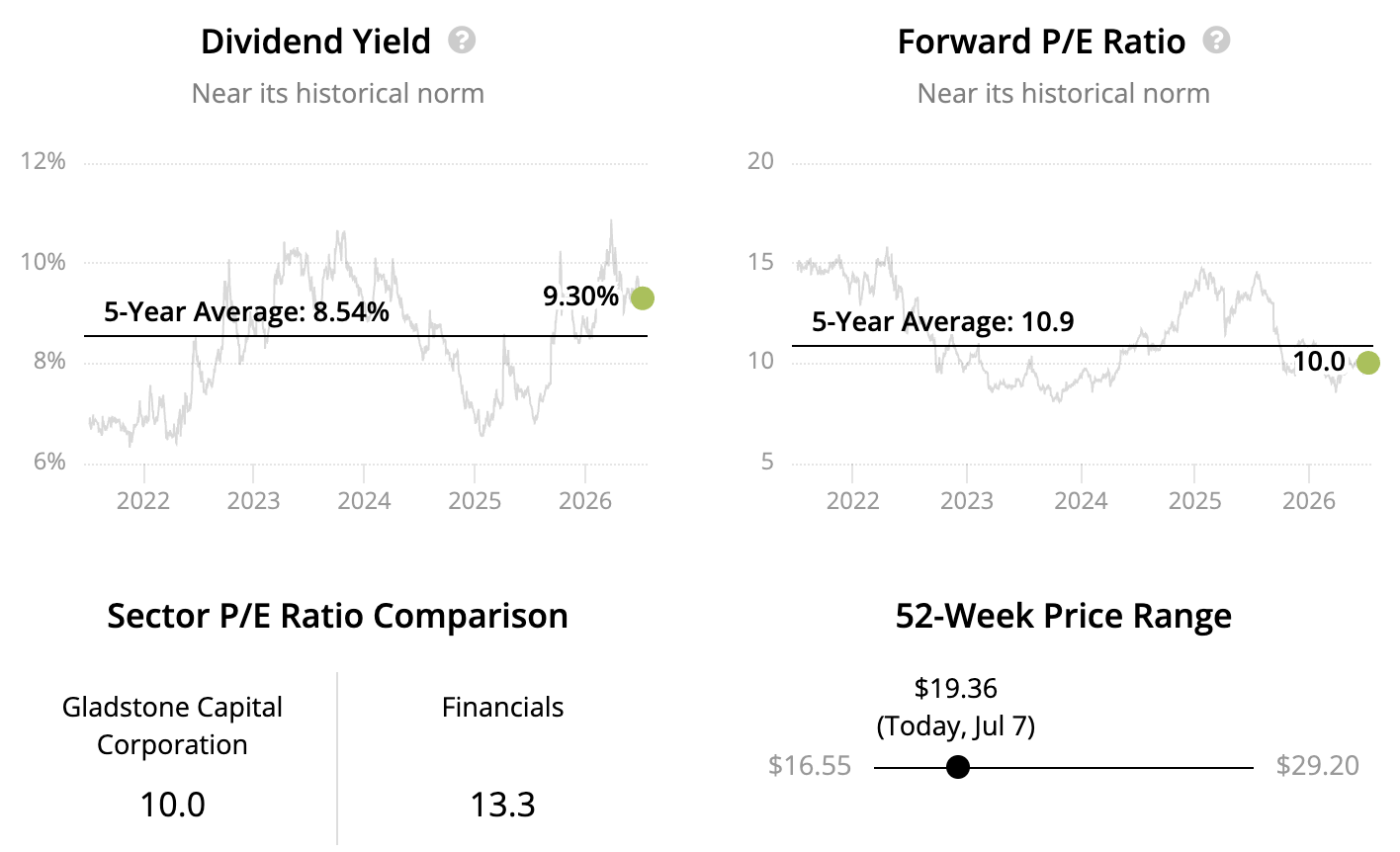

Monthly Dividend Stock #14: Gladstone Capital Corporation

Sector: Financials – Business Development Companies Dividend Yield: 9.3% Dividend Safety Score: Unsafe Uninterrupted Dividend Streak: 3 years

Founded in 2001, Gladstone Capital Corporation (GLAD) was one of the first business development companies (BDCs) focused on making loans to relatively small, private U.S. businesses.

Compared to most of its peers, Gladstone Capital lends to smaller businesses which can be riskier given their fewer financial resources. However, most of these companies are backed by private equity, giving them additional managerial oversight and sources of capital.

Gladstone Capital is also one of the smaller BDCs in the market and has a somewhat less diversified portfolio as a result. The firm holds only around 50 portfolio companies spread across roughly a dozen different industries.

To mitigate its somewhat more concentrated portfolio, Gladstone Capital avoids financial services, high-tech companies, and commodity or cyclical businesses. These firms can have greater downside risk when the tide goes out.

Gladstone Capital has also prioritized first-lien debt, which gets paid back first when a borrower defaults and now accounts for over 70% of the portfolio compared to around 50% in past years.

Overall, Gladstone Capital's strategy has managed to deliver mostly reliable dividends since the externally-managed BDC made its first payout in 2002, recording just two cuts – a 50% reduction in 2009 and a 7% cut during the 2020 pandemic.

With most of its loans carrying variable interest rates, Gladstone Capital's net investment income falls when rates decline. This tends to happen during recessions when the Fed steps in to ease financial conditions.

Coupled with Gladstone Capital's high payout ratio and modest leverage, this can cause the dividend to track net investment income lower.

Income investors considering Gladstone Capital should be comfortable with this ever-present possibility, as well as the firm's smaller portfolio, higher mix of second-lien debt, and focus on smaller businesses with subprime credit profiles.

Source: Simply Safe Dividends

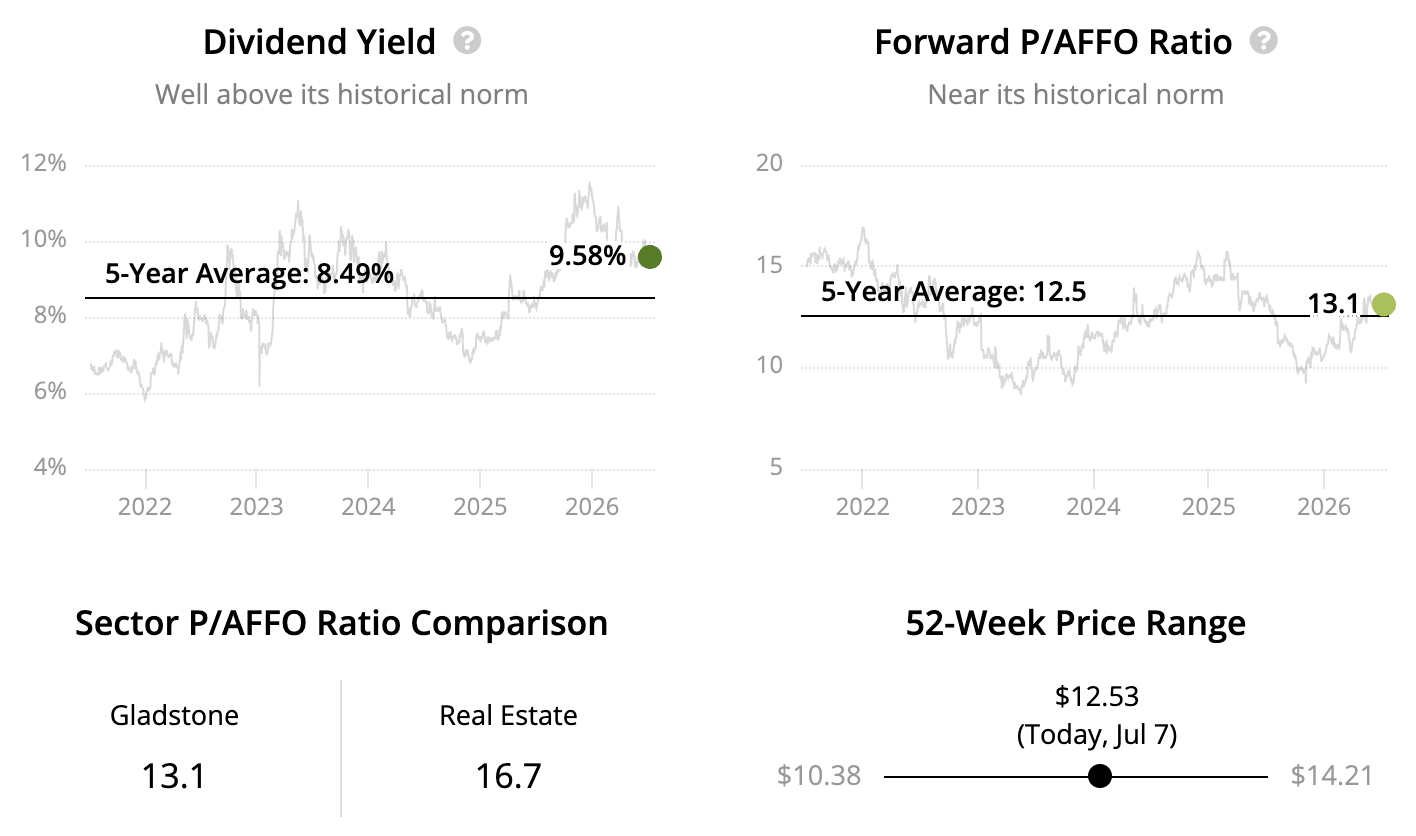

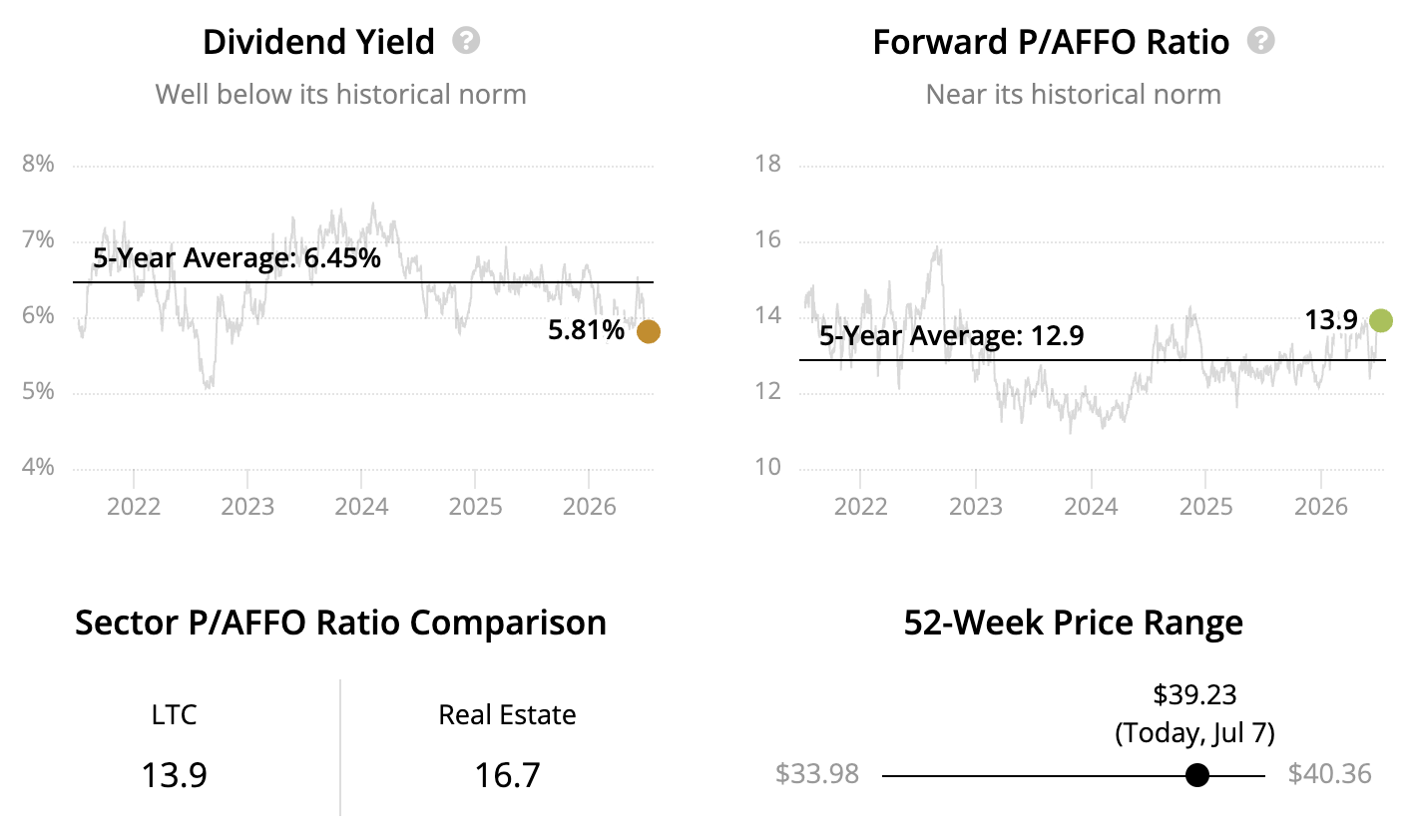

LTC Properties (LTC) began in 1992 providing mortgages to skilled nursing facilities (SNFs). While financing activities still account for around one-fourth of revenue, LTC now primarily acts as a landlord to over 30 SNF and senior housing operators who lease the small-cap REIT's roughly 200 properties.

LTC's tenants provide essential services for seniors and should enjoy higher patient volumes over time due to America's aging population. These factors have helped the company pay uninterrupted dividends since 2003.

However, most of LTC's tenants operate on razor-thin margins due to past changes to government health policy and the pandemic's adverse impact on industry occupancy rates and operating costs.

With many tenants' rent coverage stretched, especially if government aid from stimulus passed in 2020 is excluded, LTC may be forced to restructure more of its leases if the industry's occupancy does not recover fast enough to restore operators' profits.

LTC's five largest tenants account for nearly half of the REIT's revenue, making for an even murkier outlook as management navigates these challenges while trying to keep the firm's monthly dividend covered.

Overall, LTC is a well-managed firm operating in a difficult industry that faces numerous risks outside of management's control. While the REIT has been resilient in maintaining the dividend, conservative income investors may want to look at other stocks given LTC's wider range of outcomes.

Source: Simply Safe Dividends

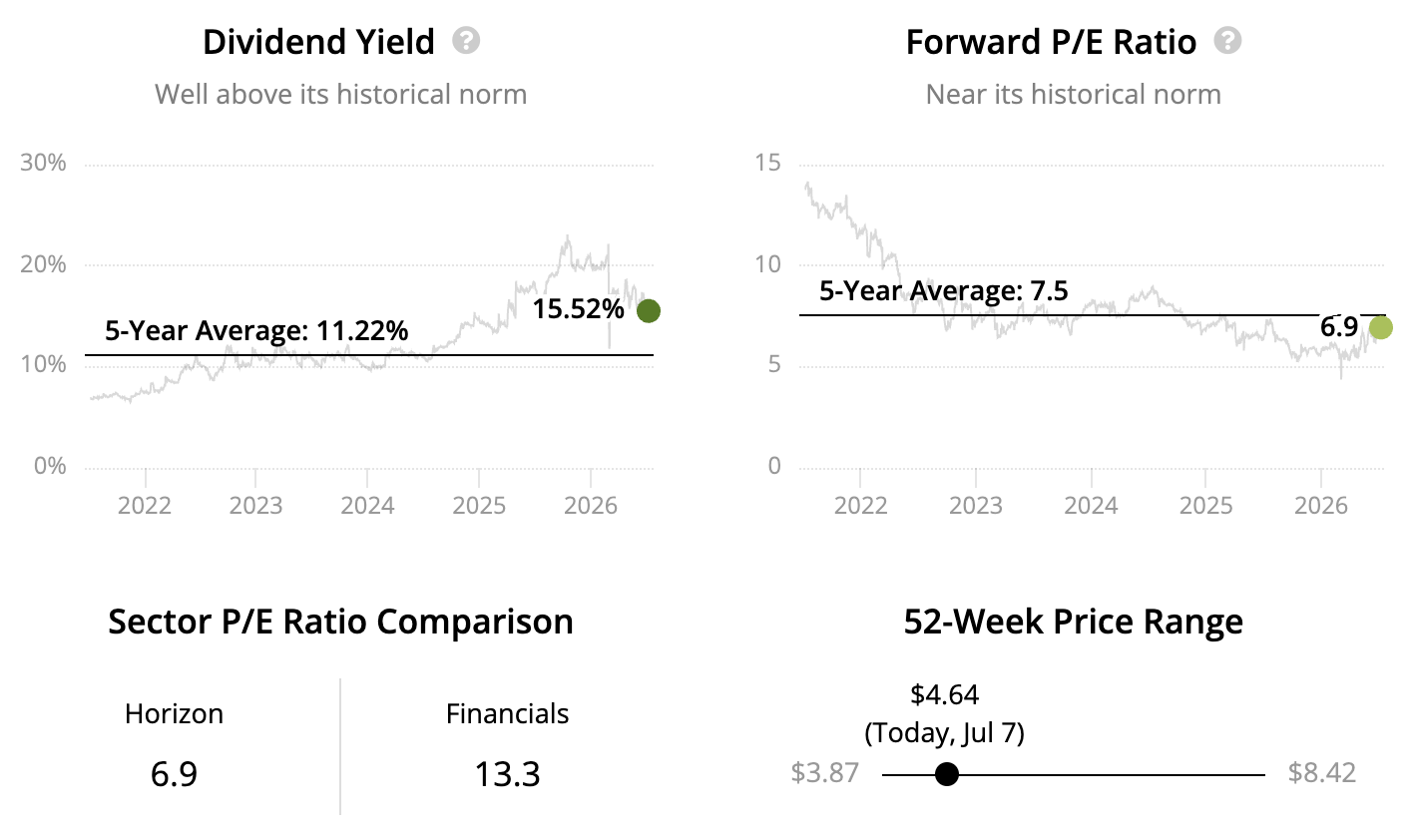

Monthly Dividend Stock #16: Horizon Technology

Sector: Financials – Business Development Companies Dividend Yield: 15.5% Dividend Safety Score: Unsafe Uninterrupted Dividend Streak: 0 years

Horizon Technology Finance Corporation (HRZN) commenced operations in 2008 and lends primarily to development-stage companies in the technology, life science, healthcare technology, and sustainability industries.

Source: Horizon Technology Investor Presentation

The externally-managed business development company (BDC) provides a way for income investors to gain exposure to venture capital-backed growth stage companies via Horizon's secured loans and warrants to purchase stock, which provide capital appreciation potential.

However, from biotechs to medical device makers and software providers, many of these disruptive portfolio companies face uncertain futures. Most of Horizon's loan investments sport yields well above 10% to reflect this risk.

While management spreads Horizon's bets across around 50 debt investments and has only reduced the dividend twice since 2010, conservative investors may prefer to stick with larger BDCs that have more diversified portfolios.

Source: Simply Safe Dividends

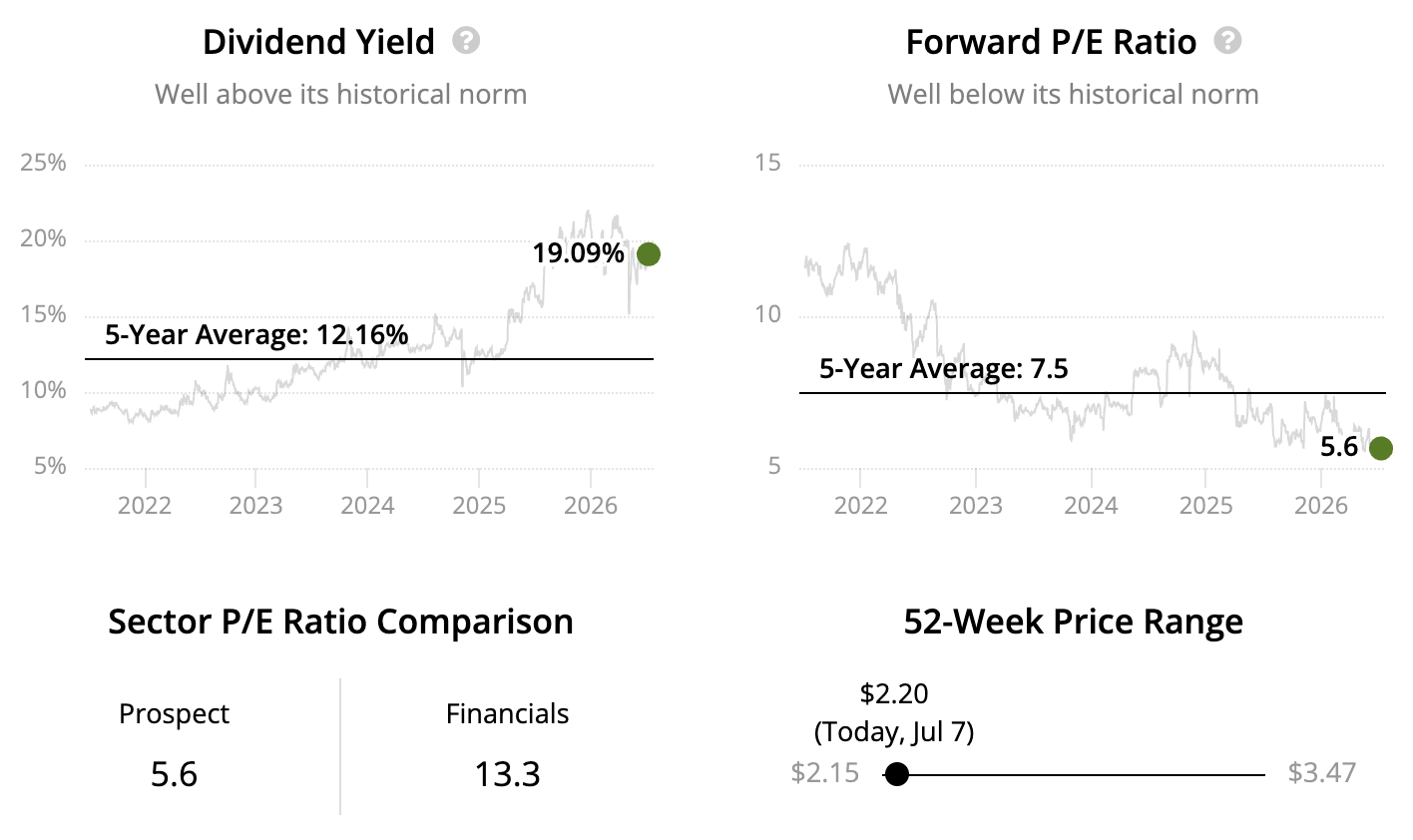

Monthly Dividend Stock #17: Prospect Capital

Sector: Financials – Business Development Companies Dividend Yield: 19.1% Dividend Safety Score: Unsafe Uninterrupted Dividend Streak: 0 years

One of the largest and oldest business development companies (BDCs), Prospect Capital (PSEC) was founded in 2004 and has several attractive qualities at first glance.

PSEC's scale enables it to target larger, more credit-worthy companies with one-stop financing options. And PSEC's portfolio is spread across over 100 investments and dozens of industries.

Source: PSEC Investor Presentation

However, PSEC has historically struggled to create shareholder value and maintain its dividend, which has undergone two large cuts over the past decade. The BDC's external management structure and riskier investment portfolio are the main culprits.

Despite its large size for a BDC, PSEC has an external management team in which it pays an outside investment advisor various fees to run its business.

Part of this arrangement includes a base management fee calculated an annual rate of 2% on PSEC's total assets, incentivizing the advisor to grow the business at any cost.

Debt and cash that is not yet invested are included in PSEC's asset calculations, too. Management can sell new shares and take on more debt to grow its fees, even if the resulting shareholder dilution destroys value over time.

PSEC has done this for years, with the resulting dilution and management fees causing the firm's net asset value (NAV) to steadily decline. NAV takes a company's total assets and subtracts out its liabilities, effectively representing the net worth a business.

Further complicating PSEC's outlook is its investment portfolio, which has less exposure to first-lien secured loans compared to most of its peers. This creates greater potential for credit losses during downturns when defaults rise.

PSEC also has higher exposure to riskier areas such as class B and C real estate and residual interests in collateralized loan obligations (CLO).

The bottom line is that PSEC's strengths are offset by its weaknesses, which make an investment in this monthly dividend payer a riskier bet over a full economic cycle.

Source: Simply Safe Dividends

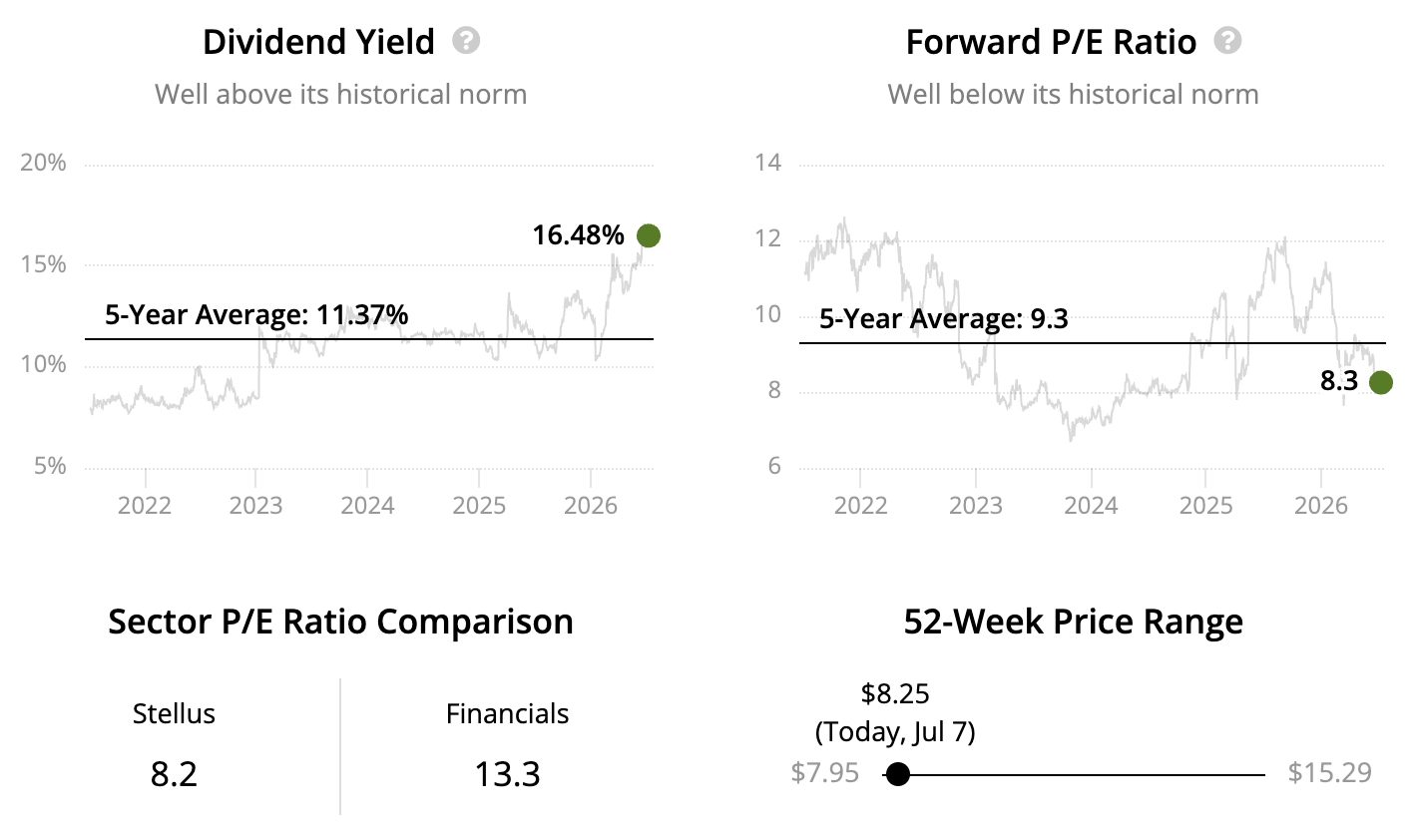

Monthly Dividend Stock #18: Stellus Capital

Sector: Financials – Business Development Companies Dividend Yield: 16.5% Dividend Safety Score: Very Unsafe Uninterrupted Dividend Streak: 0 years

Stellus Capital (SCM), an externally-managed business development company (BDC), went public in 2012 and switched to paying dividends monthly in 2014.

The firm has only cut its dividend once, a 26% reduction during the 2020 pandemic when management temporarily switched to a quarterly payout cadence as falling interest rates pressured Stellus's investment income.

As a BDC, Stellus provides debt capital to relatively small, private businesses with subprime credit profiles. Most of the companies Stellus finances are backed by private equity sponsors.

Management likes lending to so-called sponsored companies because their private equity backers provide an additional layer of governance and can put in new funding to help the company achieve its goals or address problems.

Stellus originates almost all of the loan investments it makes, giving management the opportunity to negotiate covenants, financial reporting disclosures, prepayment penalties, and other clauses that reduce the firm's risk.

Stellus also invests over 80% of its portfolio in first-lien secured loans, which are paid off first when a borrower defaults. Coupled with a focus on businesses with low capital intensity and minimal commodity exposure, this reduces risk of major loan losses during recessions.

Management emphasizes diversification across the BDC's portfolio as well. Stellus seeks to limit positions to 2.5% of the portfolio's value to avoid being overly exposed to any company that underperforms.

Source: Stellus Investor Presentation

Despite its defensive qualities, Stellus may not appeal to conservative investors due to its small size. This makes it harder to raise capital and can result in a more volatile stock price during downturns. With around 100 investments, the BDC's portfolio is less diversified than many others, too.

Stellus's payout ratio has also historically averaged a touch over 100%, providing no margin of safety to absorb credit losses or unfavorable interest rate fluctuations on its mostly floating rate loans.

As a result, Stellus's monthly dividend may face higher risk of being cut whenever the next recession hits.

Source: Simply Safe Dividends

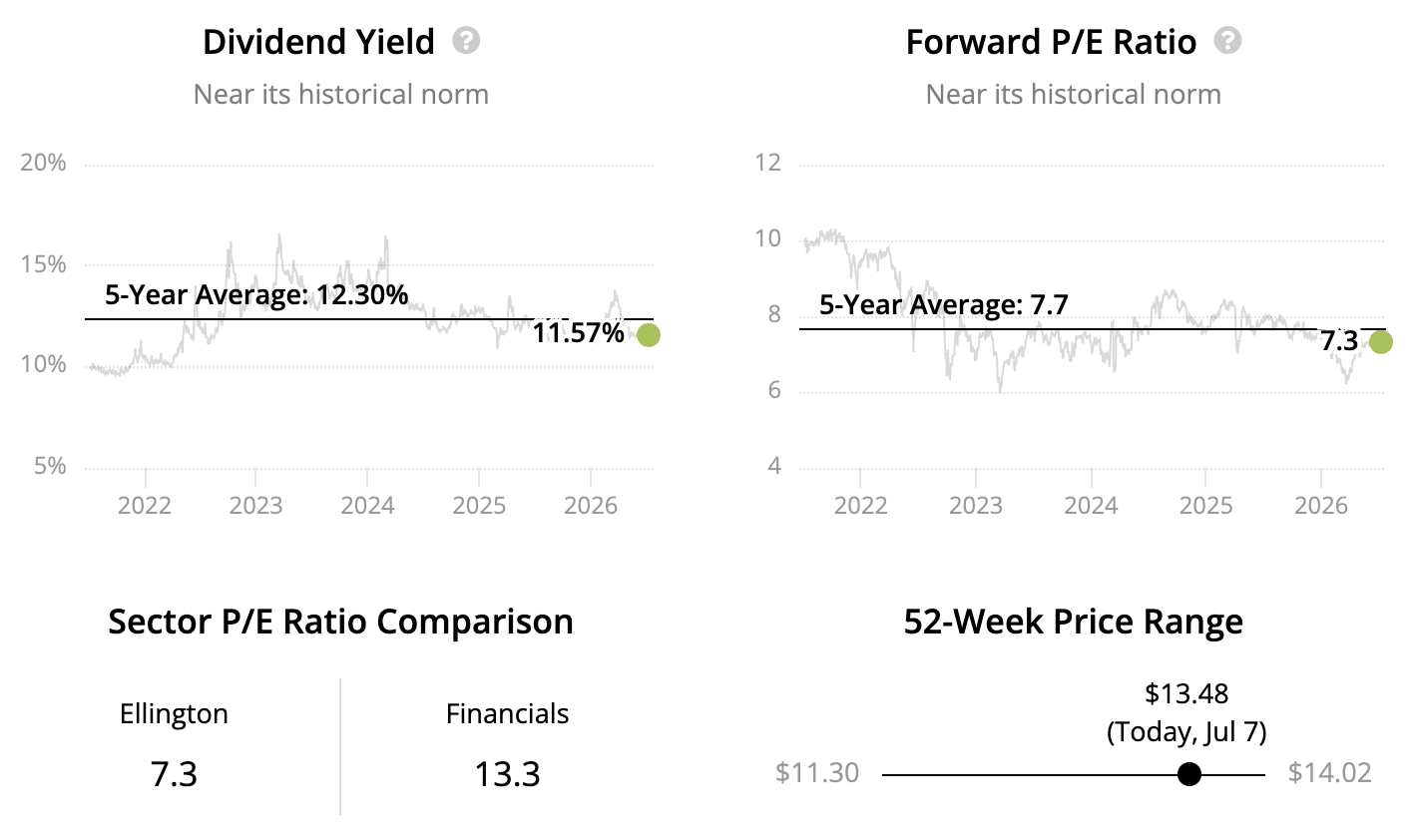

Founded in 2007, Ellington Financial (EFC) is an externally-managed mortgage REIT with an investment portfolio spanning residential and commercial mortgages, consumer loans, and corporate loan sectors.

Unlike many mortgage REITs which concentrate on a single type of investment such as agency mortgage-backed securities (MBS), Ellington's diversified portfolio gives management more flexibility to allocate capital opportunistically over various interest rate and economic cycles.

Agency MBS account for around one-third of Ellington's assets. These securities generate cash flows from pools of residential mortgage loans backed by Fannie Mae and other government-sponsored entities.

While credit risk is very low in this business, interest rate sensitivity is high.

MBS have longer durations with mostly fixed rates, while Ellington borrows primarily using short-term financing with variable interest rates. Shifts in the yield curve can reduce the margin Ellington earns, even despite management's best attempts at hedging.

Ellington's credit portfolio, which drives the remainder of the business, helps reduce the volatility of the firm's investment returns.

This division invests in everything from non-qualifying (i.e. higher risk) residential mortgages, non-agency MBS, and reverse mortgages to bridge loans, commercial MBS, and non-performing loans.

With shorter durations and lower leverage, Ellington's credit investments have much less sensitivity to interest rate fluctuations than the agency business.

Risk of loan losses is much higher in this space, but the firm's credit segment provides diversification to protect Ellington from being overly exposed to an area that falls on hard times.

That said, the mortgage REIT and its monthly dividend are not immune to the industry's challenges caused by high leverage, high payout ratios, and elevated interest rate sensitivity.

Ellington's annualized dividend per share has wavered between $1.50 and $3.00 over most of the firm's corporate life as it has ridden numerous economic cycles.

During the last downturn in 2020, when asset values plunged and some of Ellington's lenders became more anxious about the value of their collateral, Ellington slashed its dividend by nearly 50% to preserve liquidity.

The dividend returned to its pre-Covid levels around one year later, but investors considering this hybrid mortgage REIT need to be comfortable with this type of volatility.

Ellington's diversification makes it a somewhat more attractive pick in its industry, but most mortgage REITs aren't designed to deliver safe monthly dividends.

Source: Simply Safe Dividends

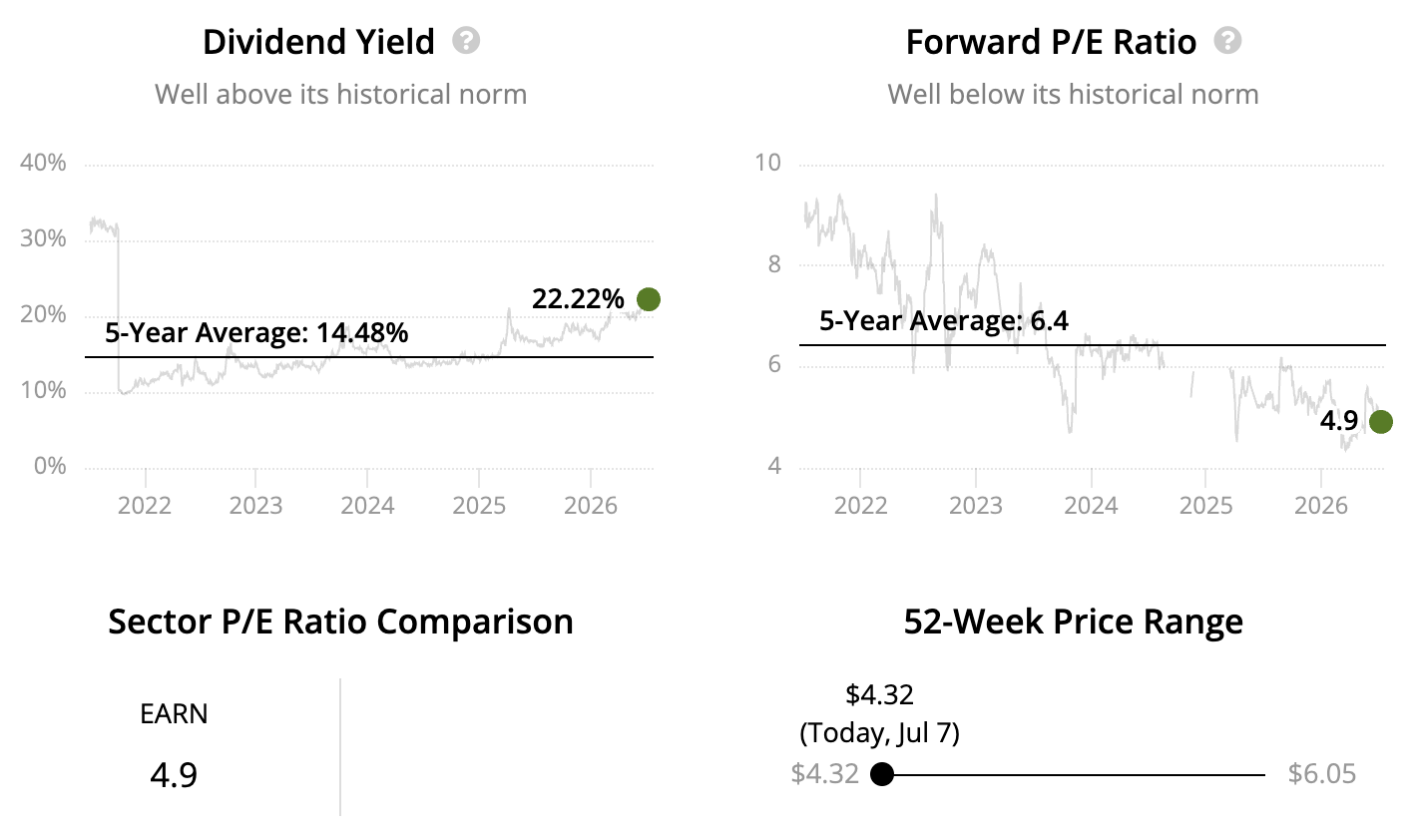

Monthly Dividend Stock #20: Ellington Residential

Sector: Financials – Residential Mortgage REITs Dividend Yield: 22.2% Dividend Safety Score: Very Unsafe Uninterrupted Dividend Streak: 1 year

Formed in 2012, Ellington Residential (EARN) is an externally-managed mortgage REIT focused on owning a portfolio of agency mortgage-backed securities (MBS), which represent claims to cash flows from pools of residential mortgage loans.

Since the principal and interest payments backing these securities are guaranteed by government entities, agency MBS have minimal credit risk and relatively low yields.

To generate more income to support its large monthly dividend, Ellington Residential uses substantial leverage to boost the size of its portfolio.

Repurchase agreements, or repos, account for the vast majority of Ellington Residential's debt and require the firm to pledge its investment securities in exchange for funding from lenders.

Repos typically mature every few months and carry floating interest rates. This is in contrast to the agency MBS the mortgage REIT invests in, which generally pay fixed interest rates and have effective durations spanning at least several years.

The spread between Ellington Residential's variable borrowing costs and MBS investment yields expands and contracts throughout a market cycle.

A sharp uptick in short-term rates result in the firm's borrowing costs moving higher quickly, reducing profits. If longer-term rates have also jumped, Ellington Residential can gradually rotate its portfolio into higher-yielding MBS to improve profits over time.

Managing large swings in interest rates and mortgage spreads has proven difficult for most mortgage REITs despite numerous attempts to hedge rates, mortgage prepayments, and credit risks.

Coupled with the firm's high payout ratio, a standard in this industry, Ellington Residential has a long history of dividend cuts, including a 20% payout reduction in May 2022 when rising interest rates pressured the firm's net interest margin.

As conservative income investors, our preference would be to invest in monthly dividend stocks outside the residential mortgage REIT space.

Source: Simply Safe Dividends

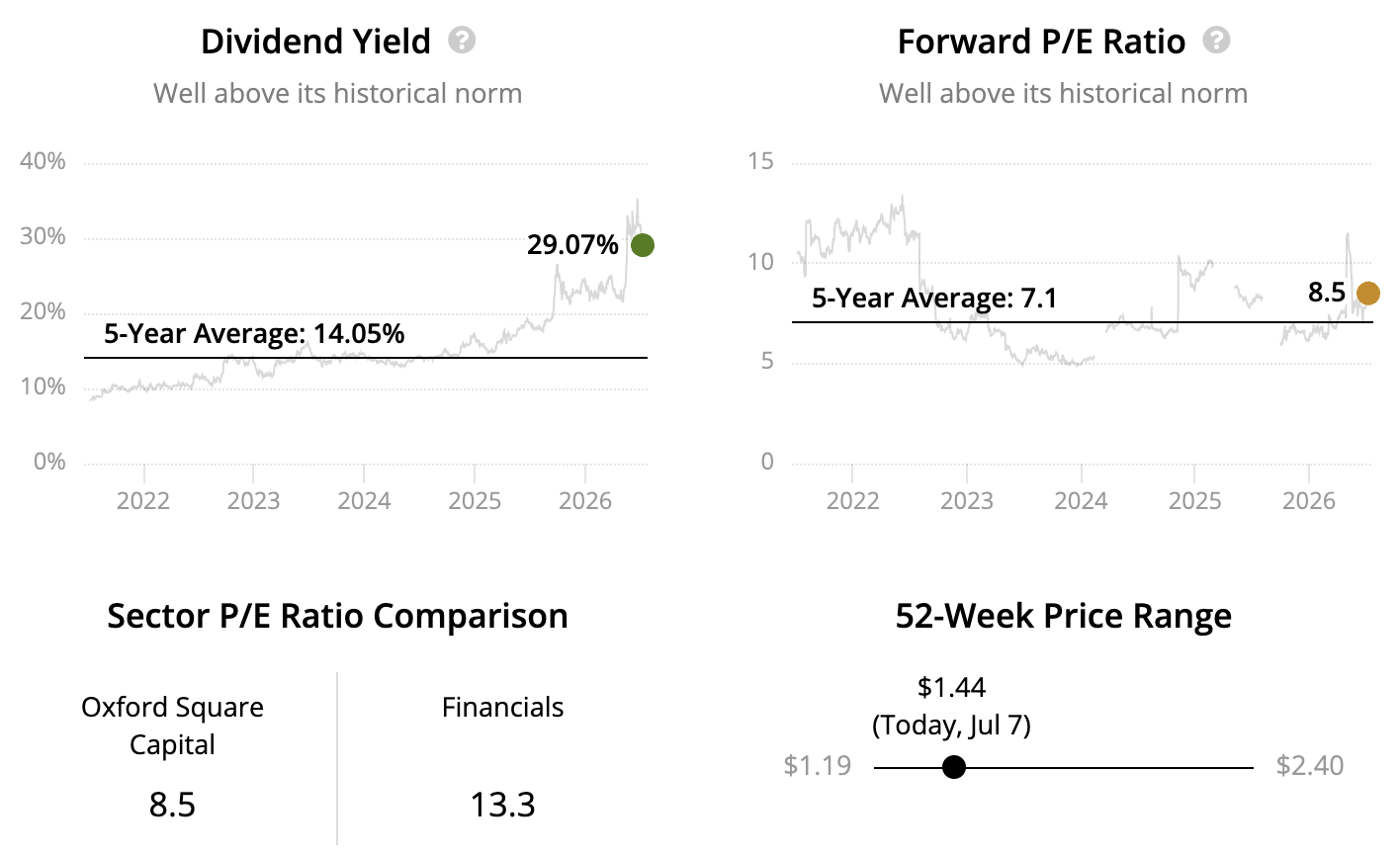

Monthly Dividend Stock #21: Oxford Square Capital

Sector: Financials – Business Development Companies Dividend Yield: 29.1% Dividend Safety Score: Very Unsafe Uninterrupted Dividend Streak: 3 years

Oxford Square Capital (OXSQ), an externally-managed business development company (BDC) formed in 2003, invests in corporate loans and collateralized loan obligations (CLO) that provide capital to relatively small, private businesses that can't access traditional financing from banks.

These borrowers tend to be highly levered companies that are considered below investment grade. Many of Oxford's loans carry double-digit yields reflecting their elevated credit risk.

Compared to some of its peers, Oxford invests more aggressively. The firm's portfolio contains mostly second-lien secured debt and CLO equity, with first-lien debt making up the remainder.

In the event of a borrower's insolvency, second-lien debt is second in line to be repaid after first-lien debt is paid off. And CLO equity is even riskier as it absorbs the CLO's losses before any of the CLO's other tranches while also having the lowest level of payment priority.

These securities generally have floating interest rates that can increase Oxford's income during a period of rising rates and help keep the value of its portfolio steady. But junk loans and CLO equity exposure can cause trouble during recessions when loan defaults spike and Oxford's leverage magnifies losses.

Despite investing most of its portfolio in more stable industries such as business services, software, and healthcare, Oxford slashed its dividend by 48% during the 2020 pandemic. And during the 2007-09 financial crisis, the company's payout declined by 58%.

Other BDCs such as Main Street Capital (MAIN) also pay monthly dividends but invest more conservatively and have greater diversification compared to Oxford, which invests in less than 75 portfolio companies. Dividend investors valuing stability over a full cycle should look elsewhere.

Source: Simply Safe Dividends

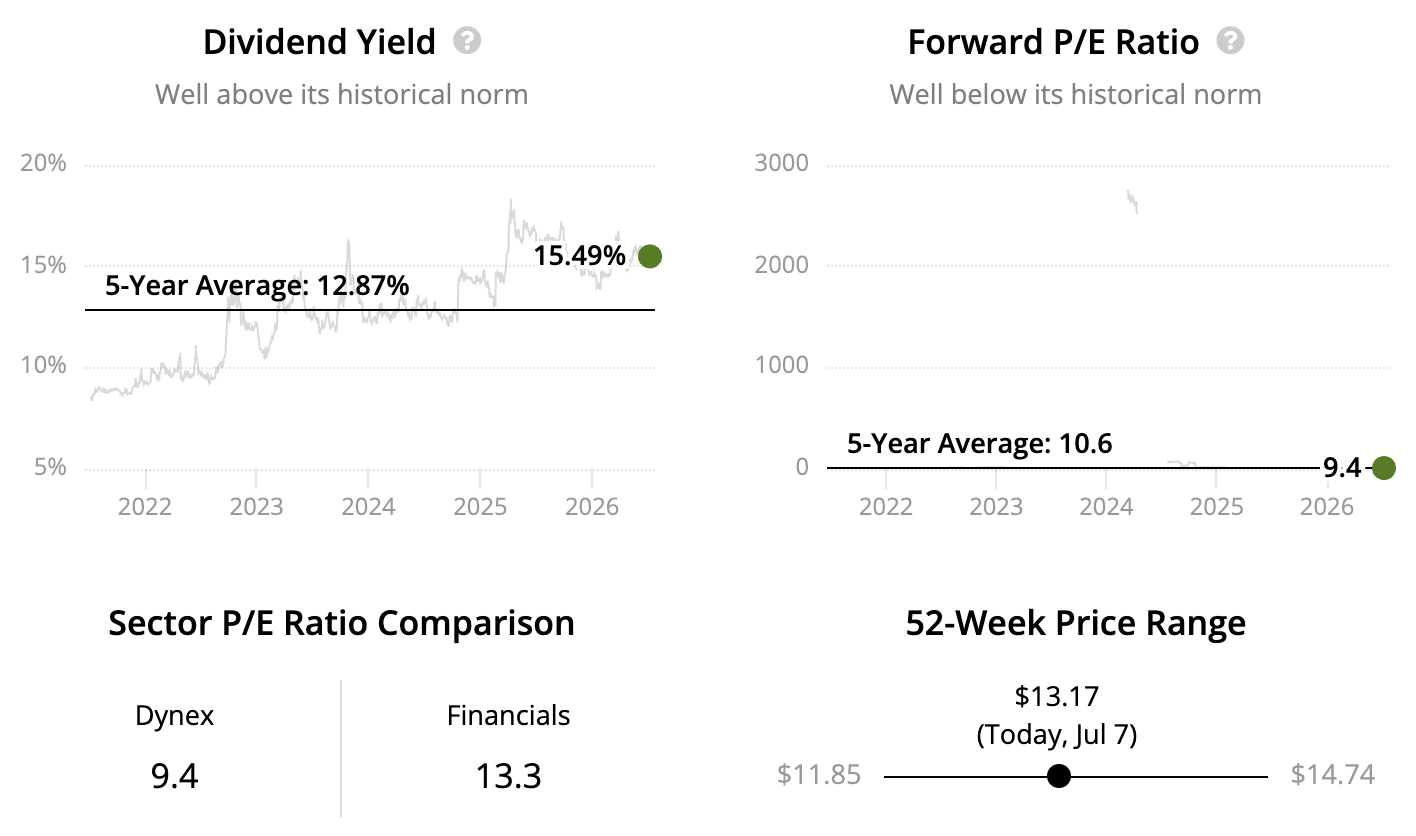

Dynex Capital (DX), an internally-managed residential mortgage REIT founded in 1988, has cut its dividend seven times since the beginning of 2013, with its most recent cut occurring in June 2020 when the firm reduced its payout by 13%.

Investing over 90% of its portfolio in agency mortgage-backed securities (MBS), Dynex's interest-rate sensitive business model makes it hard for the company to pay reliable dividends over a full economic cycle.

The payment of principal and interest on these residential mortgage loans are guaranteed by government-sponsored organizations, so most of the firm's investments are AAA rated and offer low yields around 2% to 5%.

That's not enough to support a large monthly dividend, so Dynex uses repurchase agreements, or repos, to boost its earnings and dividend power. With repos, the company pledges its investment securities (i.e. agency MBS) in exchange for short-term funding from lenders.

Dynex's repos have floating interest rates and typically mature within a couple of months. But most of its agency MBS have fixed interest rates and long-term maturities. This mismatch in duration and rate variability creates several challenges.

Periods of rising interest rates or a relatively flat or inverted yield curve decrease the spread between the interest payments Dynex earns on its long-term investments and the interest payments it makes on its short-term borrowings.

This inevitable profit squeeze over a full economic cycle can quickly stress dividend coverage since mortgage REITs are required to pay out the vast majority of their profits.

Dynex's reliance on repo funding creates additional risks during downturns, when the value of assets posted as collateral declines or lenders require a larger margin of safety. This can force firms like Dynex to provide additional securities or cash at an inopportune time.

Overall, an investment in Dynex is not for the faint of heart. Interest rate spreads, hedging gains and losses, repo market funding, mortgage prepayments, use of leverage, and the industry's aggressive payout policy all create risks for the dividend over time.

Source: Simply Safe Dividends

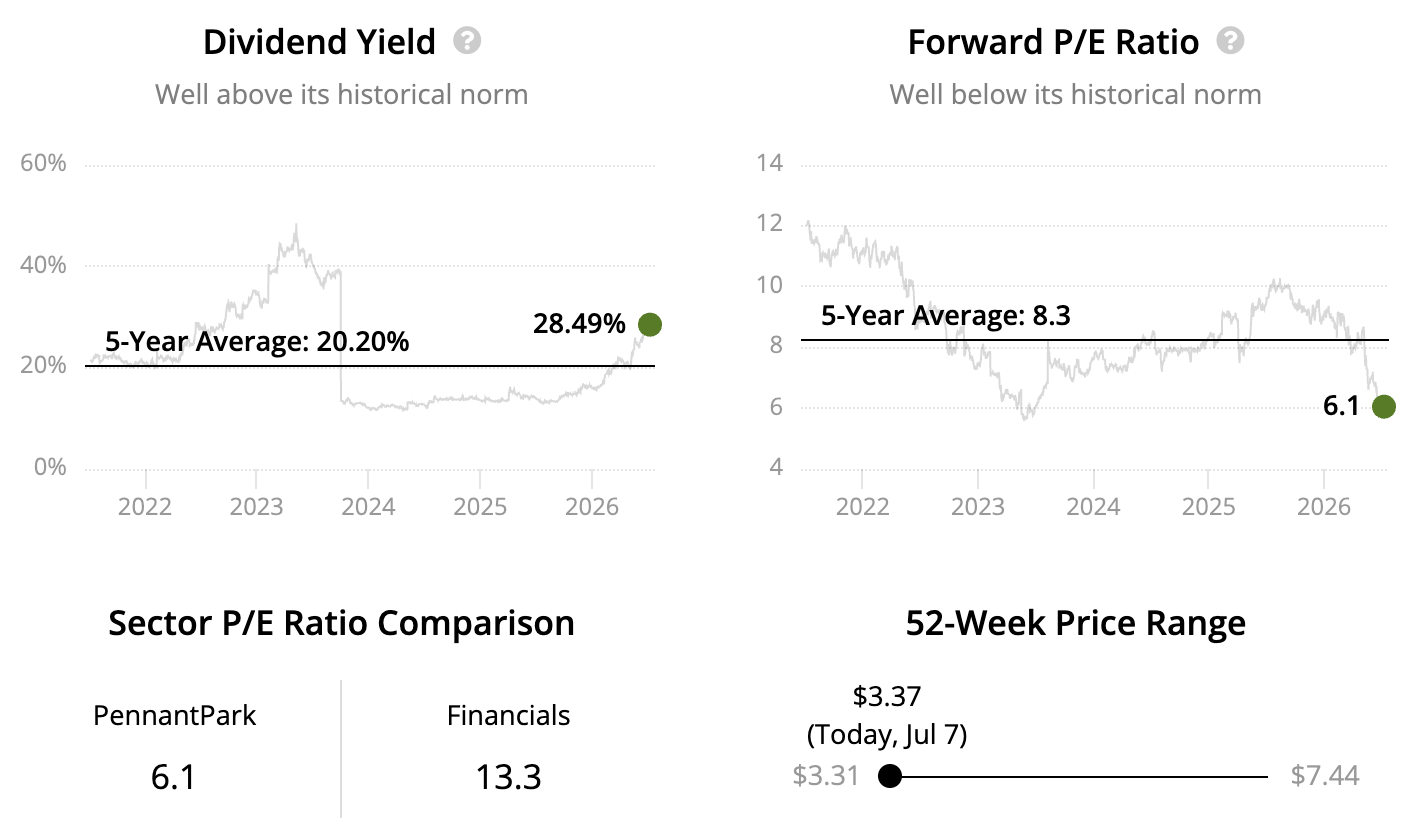

Monthly Dividend Stock #23: PennantPark

Sector: Financials – Asset Management and Custody Banks Dividend Yield: 28.5% Dividend Safety Score: Very Unsafe Uninterrupted Dividend Streak: 4 years

PennantPark (PNNT), founded in 2007, is an externally-managed business development company (BDC) that provides debt and equity financing to middle-market businesses in the United States.

The firm’s primary focus is on first-lien senior secured loans, which are the highest-priority debt in the event of a borrower default, and second-lien loans, which carry higher risk but offer greater yields. Equity investments make up a smaller portion of the portfolio and provide potential for capital appreciation.

PennantPark’s portfolio spans a range of industries, including healthcare, business services, and technology, helping to diversify risk. However, the portfolio is relatively concentrated, with fewer than 100 investments.

To offset these risks, PennantPark targets companies with stable cash flows and strong backing, often from private equity sponsors, which provide additional capital and governance support.

Management primarily invests in floating-rate loans, which generate higher income as interest rates rise. However, this approach increases vulnerability when interest rates fall or during economic slowdowns when defaults may climb.

PennantPark reduced its dividend by 33% in 2020 and by 67% in 2023, reflecting the cyclical risks inherent in its portfolio. Given the firm's forward-looking payout ratio exceeds 100%, the firm looks poised for another cut if conditions don't improve.

Conservative investors should weigh these risks carefully before considering the stock.

Source: Simply Safe Dividends

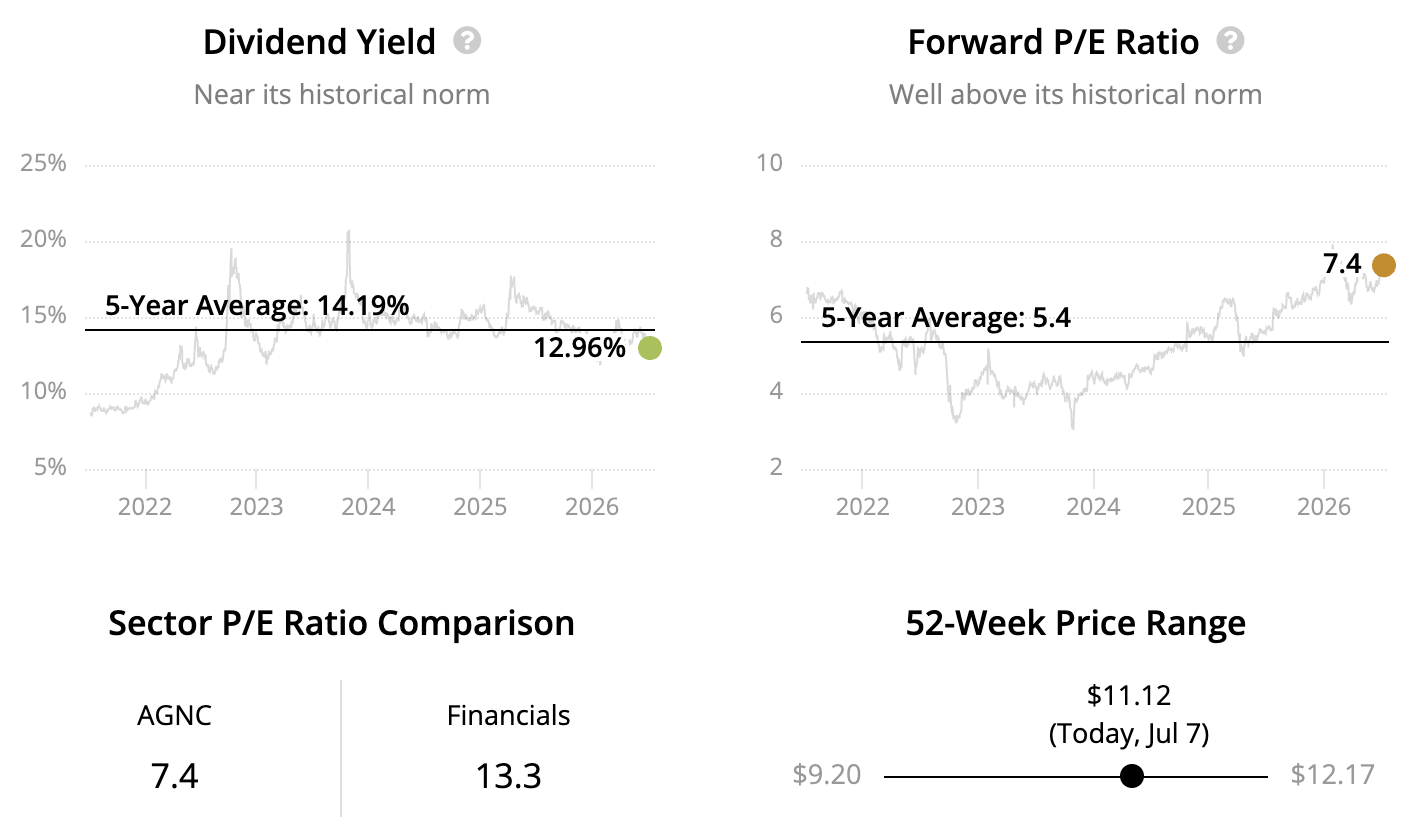

AGNC (AGNC) commenced operations in 2008 and invests predominantly in agency mortgage-backed securities (MBS).

Agency MBS represent interests in pools of mortgage loans secured by residential real property. The principal and interest payments tied to agency MBS are backed by government-sponsored agencies such as Fannie Mae.

Given the minimal credit risk of these securities and their correspondingly low yields, the internally-managed mortgage REIT employs high leverage to boost the size of its portfolio and the income it generates.

Similar to other residential mortgage REITs, AGNC's debt consists primarily of repurchase agreements, or repos, in which the company pledges its MBS in exchange for funding.

Repos typically have variable interest rates and mature within a few months, but most of AGNC's investments have fixed interest payments and long-term maturities.

As a result, the spread AGNC earns between its MBS and borrowing costs can get squeezed when short-term interest rates rise and the yield curve flattens or inverts. Efforts to hedge interest rate fluctuations are only so effective given the number of variables in play.

Coupled with the firm's significant leverage, which can cause problems during downturns when lenders become more anxious, AGNC has not been a reliably monthly dividend payer over a full economic cycle.

In fact, the mortgage REIT's dividend has declined around 10% annually over the past decade, including a 25% cut during the 2020 pandemic when MBS values plunged and repo funding markets locked up.

AGNC has maintained a more modest payout ratio following the pandemic, and its larger size and internal management team give it one of the lowest cost structure in the industry.

While these factors may make AGNC more dependable than most of its smaller, externally-managed peers with more aggressive financial practices, conservative income investors prioritizing safe dividends should look elsewhere for monthly dividend stocks.

Source: Simply Safe Dividends

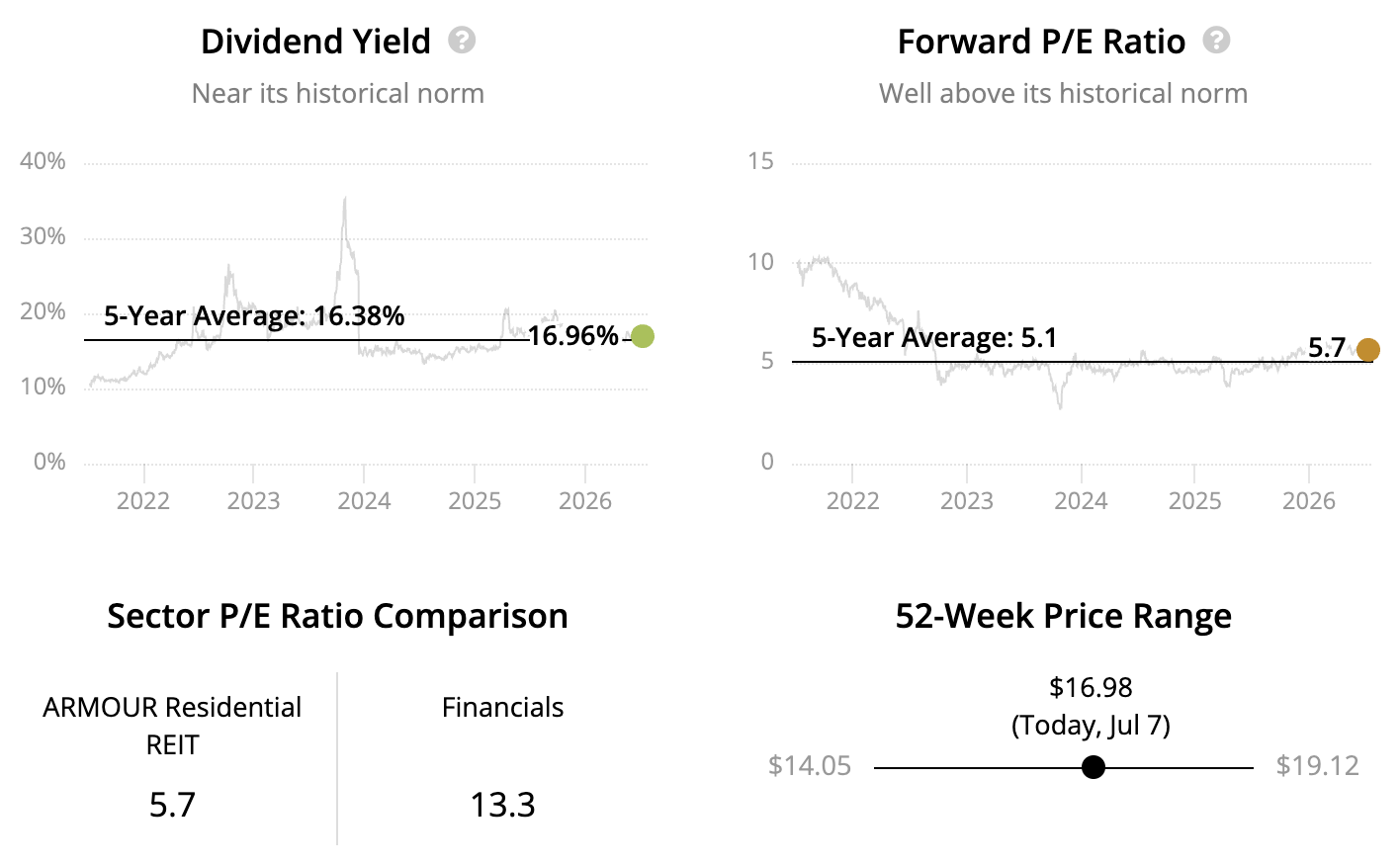

Founded in 2008, Armour Residential REIT (ARR) is an externally-managed mortgage REIT focused on owning agency mortgage-backed securities (MBS).

Agency MBS represent claims to cash flows from pools of mortgage loans, usually on single-family homes, with their payment guaranteed by government-sponsored organizations such as Fannie Mae.

These largely AAA-rated securities offer low yields, reflecting their minimal credit risk. To boost its income and support an attractive monthly dividend, ARR uses substantial leverage to increase the size of its portfolio.

ARR's debt consists mostly of repurchase agreements, or repos, in which the firm pledges its investment securities in exchange for funding from lenders.

Repos generally have floating interest rates and mature within a few months. But most of ARR's agency MBS pay fixed interest rates and have long-term maturities.

This mismatch in interest rate variability and duration can pressure earnings when short-term interest rates rise and the yield curve flattens or inverts, decreasing the spread between the interest payments on ARR's MBS and the firm's borrowing costs.

Coupled with ARR's high leverage and the less reliable nature of repo funding during market downturns, the mortgage REIT has struggled to pay steady monthly dividends over time.

In fact, ARR's dividend has declined by 20% annually over the last decade. While ARR has held its dividend flat since mid-2020, conservative investors seeking stocks that can pay reliable dividends each month over a full economic cycle should look elsewhere.

Source: Simply Safe Dividends

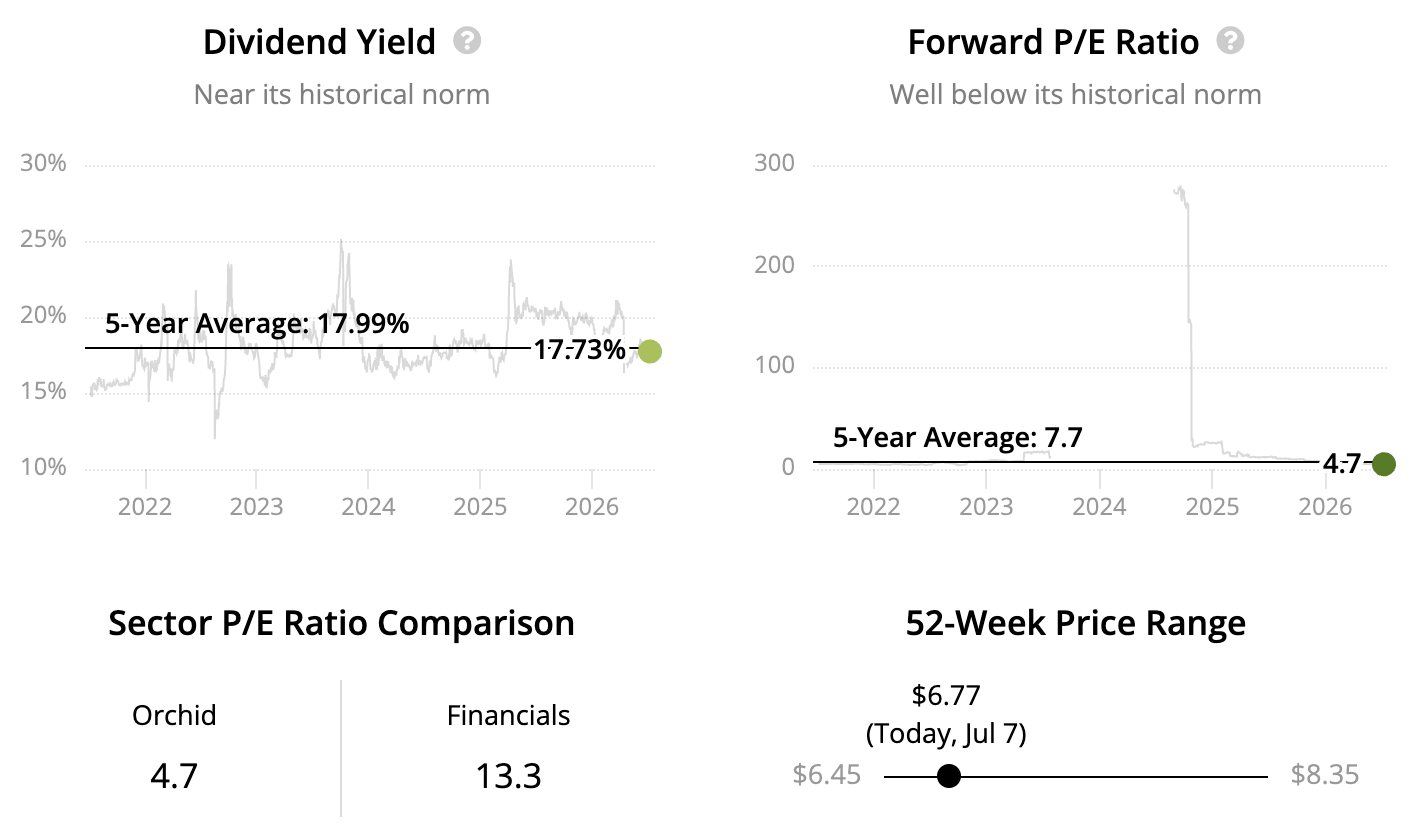

Monthly Dividend Stock #26: Orchid Island Capital

Sector: Financials – Residential Mortgage REITs Dividend Yield: 17.7% Dividend Safety Score: Very Unsafe Uninterrupted Dividend Streak: 0 years

Orchid Island Capital (ORC) has a long history of double-digit dividend cuts since the externally-managed mortgage REIT went public in 2013, including a 25% reduction announced in October 2023.

Taking on significant leverage to invest in residential mortgage-backed securities (MBS), Orchid's profits are driven by the difference between the yield on its long-duration, fixed-rate MBS and the cost of its short-term borrowings, which generally have floating interest rates.

Rising borrowing costs and a flattening yield curve shrink Orchid's profits, stressing the mortgage REIT's high payout ratio and leading to dividend cuts over a full cycle.

Orchid also maintains aggressive leverage, relying on repurchase agreements to fund its investments. This form of short-term financing can be less dependable during downturns when anxious lenders demand more collateral, potentially forcing poorly timed asset sales to meet margin calls.

Although agency MBS have extremely low credit risk because their payments are backed by federal agencies such as Fannie Mae, the mortgage REIT business model of high leverage, high payout ratios, and high interest rate sensitivity makes this a challenging place for reliable monthly dividends.

Investors comfortable with these risks may want to look for mortgage REITs with lower-cost internally-managed structures, more moderate leverage, and less dependence on repurchase agreements. Annaly Capital Management (NLY) is one example, though it pays dividends quarterly rather than monthly.

Source: Simply Safe Dividends

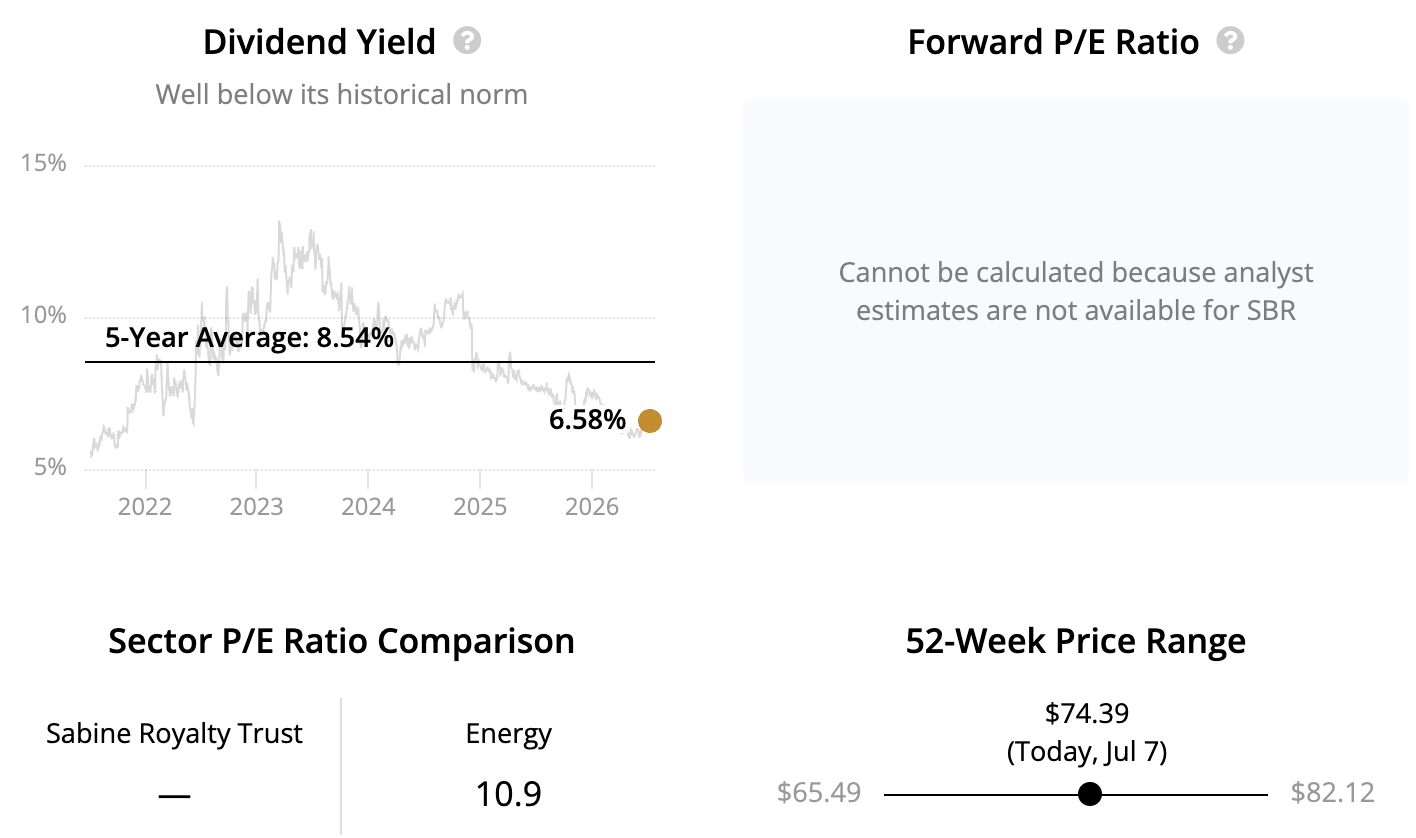

Monthly Dividend Stock #27: Sabine Royalty Trust

Sector: Energy – Oil and Gas Royalties Dividend Yield: 6.6% Dividend Safety Score: Very Unsafe Uninterrupted Dividend Streak: 0 years

Sabine Royalty Trust (SBR) is not a reliable stock for steady monthly dividends. The trust was formed in 1982 and owns royalty interests in producing and undeveloped oil and gas properties.

Sabine owns over 2 million acres in some of the most prominent producing basins, including the Permian (40% of total acres), Gulf Coast (17%), and Anadarko (13%).

Oil and gas exploration and production companies pay Sabine a cut of their proceeds when they extract and sell energy commodities from properties the trust has a royalty interest in. The trust has no other assets and does not engage in production activities itself.

The trust's monthly distributions hinge on the prices realized from the sale of crude oil and natural gas. These commodities frequently experience large and sudden swings in price, which have caused Sabine's variable payouts to fall as much as 50% in a year.

A sustained drop in energy prices can further hurt Sabine's revenue if drillers reduce their production volumes to conserve capital.

Estimating future production and drilling activity depends on fuzzy oil and gas price forecasts. But the trust's reserves, or the amount of oil and gas estimated to be recoverable, have an estimated life span of 8 to 10 years.

If realized, this means Sabine's properties would run out of production in about a decade, and the trust would wind down. (The trust otherwise does not have a specific end date.)

However, Sabine's reserves have had a similar estimated life span for decades. Oil and gas companies have had success developing more properties to replace the trust's depleting reserves, but it is admittedly challenging to assess whether that will continue.

Income investors considering Sabine should be comfortable with the potential for the trust to wind down in a decade, at which point its large monthly distribution will also come to an end.

Source: Simply Safe Dividends

Micro-Cap and OTC Monthly Dividend Stocks

Unlike the 27 monthly dividend stocks analyzed above, the companies below trade over-the-counter (OTC) and/or are micro-cap stocks.

These stocks tend to be highly illiquid, have more concentrated operations, and may not have to meet any minimum financial standards unlike stocks traded on major exchanges.

Conservative income investors should avoid these securities. That said, we ranked the list of micro-cap and OTC monthly dividend stocks below in order from least to most risky.

Global Water Resources (GWRS) formed in 2003 and has paid monthly dividends without interruption since going public in 2016. The firm owns and operates around 20 water and wastewater utilities in communities around Phoenix, Arizona. With new connections in existing service areas, acquisitions, and utility rate increases, Global Water has an attractive growth profile to support a rising monthly dividend despite its concentrated footprint.

Slate Grocery REIT (SRRTF) is based in Canada but owns over 100 U.S. grocery-anchored shopping centers spanning more than 20 states. The small-cap retail REIT earns the majority of its rent from grocery stores and other essential tenants, resulting in a stable cash flow stream that has supported growing monthly dividends since the first payout was made in 2015.

BSR REIT (BSRTF), an internally-managed REIT based in Canada, owns around 30 apartments located primarily in suburban Texas. The predictable cash flow generated by this business has enabled BSR to pay uninterrupted monthly dividends since it began making payouts in 2018. The REIT has attractive growth qualities given Texas's faster rate of population growth, but its small size comes with risks.

CT REIT (CTRRF) owns over 370 mostly single-tenant retail properties across Canada. The REIT enjoys very high occupancy and generates nearly all rent from investment-grade tenants. However, this is driven by the fact that BBB rated Canadian Tire Corporation accounts for the majority of rent. While creating concentration risk, this stable exposure has also enable CT REIT to pay uninterrupted monthly dividends since 2014.

Firm Capital Property Trust (FRMUF), a Canadian REIT formed in 1988, owns over 60 commercial properties spanning retail, industrial, apartments, and manufactured housing. The micro-cap company's properties are spread across Canada, and only one tenant exceeds 6% of rent. Firm Capital has raised its monthly dividend every year since 2012 but maintains an aggressive payout ratio. Overall, the firm has created solid value for investors over time.

Savaria (SISXF) was founded in 1978 and is headquartered in Canada. The small-cap firm provides accessibility solutions such as stairlifts, home elevators, medical beds, and wheelchair lifts for the elderly and physically challenged people. The world's aging population should provide a tailwind for Savaria, which generates consistent cash flow and has paid mostly rising monthly dividends over the years.

Diversified Royalty (BEVFF) is headquartered in Canada and owns a small portfolio of trademarks such as Mr. Lube oil change services, Air Miles rewards program, Sutton real estate services, and Nurse Next Door home care services. The capital-light business generates high margins from the royalties it receives and has paid uninterrupted monthly dividends since 2014 outside of a 13% cut during the 2020 pandemic.

U.S. Global Investors (GROW) is a boutique investment management firm specializing in actively managed equity and bond strategies with eight mutual funds and two ETFs. The fund's strategies focus on niches such as gold and precious metals, natural resources, emerging markets, and luxury goods. The micro-cap manager's eclectic set of strategies have failed to deliver much shareholder value over the decades, and the dividend has experienced two major cuts since 2007.

Modiv (MDV) owns over 40 commercial properties spanning the industrial, office, and retail sectors. The micro-cap REIT's revenue stream has good visibility thanks to long-term leases, but it is dependent on a handful of tenants which each represent around 5% to 10% of annual rent. This concentration, coupled with a high payout ratio and the challenges of raising growth capital on attractive terms at Modiv's size, reduce the stock's appeal.

Flagship Communities REIT (MHCUF) owns over 75 manufactured housing communities in Midwest U.S. markets. The Canadian-based REIT benefits from operating in a recession-resistant, highly-fragmented industry with opportunities for continued acquisitive growth. But its small size and high leverage create challenges.

Primaris REIT (PMREF) is based in Canada and owns over a dozen enclosed malls. While the REIT boasts a moderate payout ratio target, this business serves less creditworthy tenants such as apparel retailers and must contend with a fuzzy long-term outlook due to the continued rise of online shopping.

Timbercreek Financial (TBCRF) was founded in 2016 and is based in Canada. The small-cap stock provides short-duration structured loans to real estate investors secured by commercial real estate, such as multi-residential, office and retail buildings. This business generates steady cash flow when times are good but can rack up credit losses during downturns. Coupled with Timbercreek's small size, the firm's generally stable monthly dividend track record may not be enough to appeal to most investors.

Fortitude Gold (FTCO) incorporated in 2020 and generates virtually all of its revenue from a single property mining gold in Nevada. The debt-free business generates good margins from its surprisingly low-cost operation. But there is a lot of operational and financial risk depending on one property and one commodity to drive the business.

Pine Cliff Energy (PIFYF) paid its first monthly dividend in June 2022. Based in Canada, the company primarily explores for and produces natural gas. Profits are tied closely to movements in the price of gas, so it remains to be seen if Pine Cliff can sustain its monthly dividend over a full cycle. Management owns over 10% of the stock and runs the business with no debt, providing some downside protection.

Paramount Resources (PRMRF) was founded in 1976 and is based in Canada. The oil and gas exploration and production company is a highly volatile business with profits tied to prevailing energy prices. Coupled with sizable undeveloped reserves that will required substantial capital to develop, the small-cap, BB- rated stock looks unappealing for investors seeking stability.

Tamarack Valley Energy (TNEYF) was incorporated in 2002 and is based in Canada. The B rated firm explores and produces oil, gas, and natural gas liquids in the Western Canadian sedimentary basin. The business has followed an acquisitive growth strategy and maintains low debt levels, but its profits are very sensitive to energy prices. And the stock's performance over the last two decades leaves a lot to be desired.

Closing Thoughts on Monthly Dividend Stocks

Dividend stocks that pay every month appeal to investors desiring a simple retirement income strategy, especially given the high yields offered by most of these securities.

However, while over 70 monthly dividend stocks exist, most of them fall into just a handful of industries, possess meaningful risk factors, or are too small for conservative investors to consider.

Stocks should always be purchased based on their business quality and valuation, not their dividend payout schedule.

It's important to remember that most income investors will still create their own monthly dividend portfolios by owning a diversified group of dividend-paying stocks, even if only a few of them pay dividends monthly.

For investors desiring to own stocks with monthly dividends, please remain aware of your risk tolerance and size your positions appropriately.