International Paper Plans to Reduce Dividend by 15-20% Following Spin-off of Printing Papers in Q3

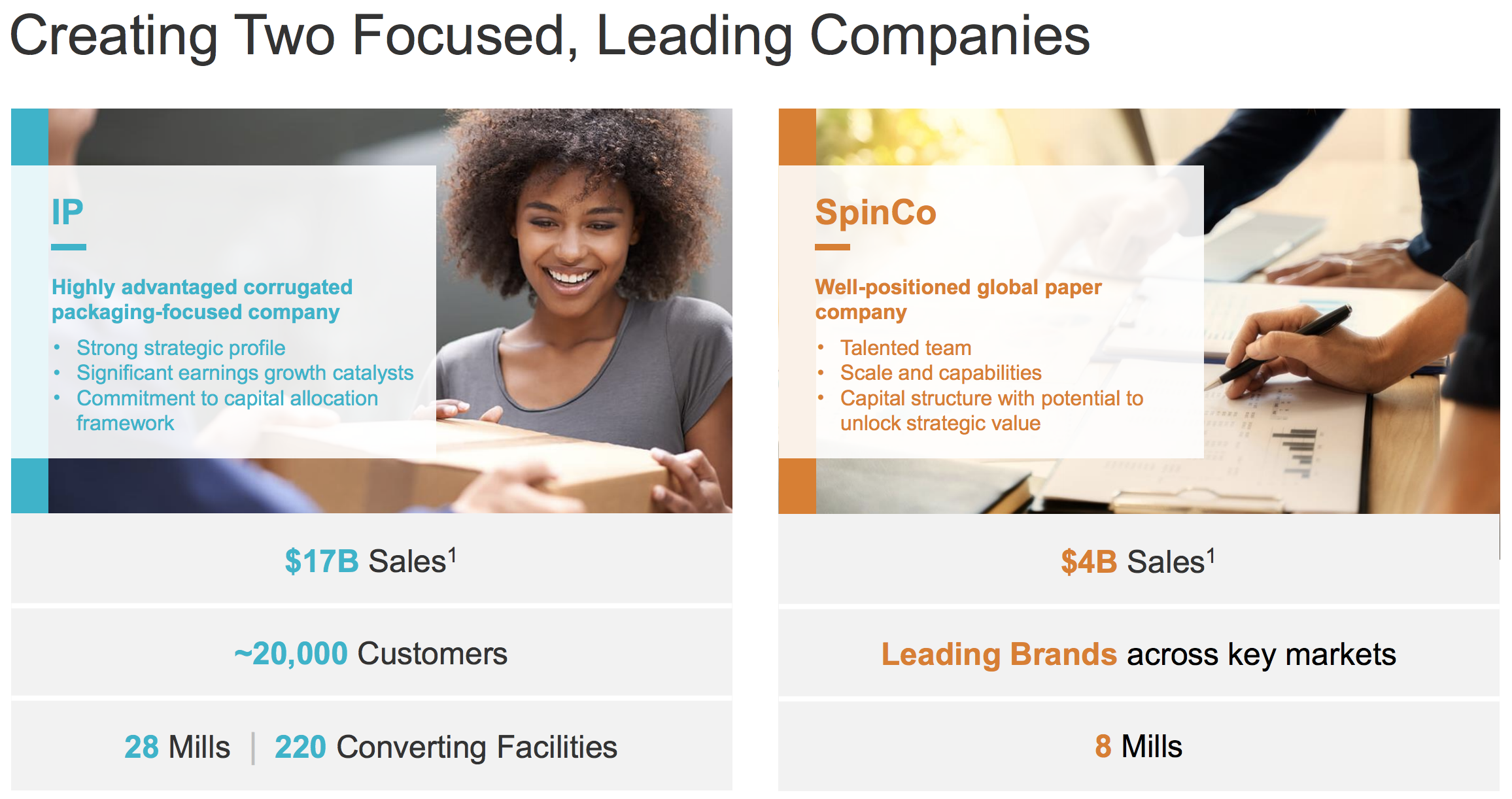

In December, International Paper announced plans to spin off the firm's printing papers business into a standalone, publicly traded company.

Source: International Paper Investor Presentation

The spin-off is expected to be completed late in the third quarter of 2021, at which time shares in the spin-off will be distributed to International Paper investors. The transaction is expected to be tax-free for U.S. federal tax purposes.

Printing papers account for close to 20% of International Paper's cash flow. As a result, International Paper expects to reduce its current dividend by 15% to 20% in proportion to the cash generated by the spin-off once the transaction closes.

This will keep International Paper's payout ratio aligned with management's target of 40% to 50% of free cash flow.

International Paper has already declared its dividend for the first quarter of 2021, keeping its payout flat at 51 cents per share.

We expect this dividend level to be maintained for the second and third quarters before being reduced to around 42 cents per share beginning in the fourth quarter. At today's share price, that works out to a dividend yield around 3.3%.

The spin-off company is not expected to pay a dividend at the outset, but management will evaluate their distribution plans after the spin. As a mature business with limited investment opportunities, we would expect this company to begin paying a meaningful dividend soon after its separation.

That said, we are downgrading International Paper's Dividend Safety Score from Borderline Safe to Unsafe to reflect the upcoming spin-off transaction.

Investors should be aware that the current dividend will be lowered in the fourth quarter of this year. However, that's not necessarily a reason to sell the stock.

Once the transaction is completed and the new, lower dividend is in place, we expect to upgrade International Paper's Dividend Safety Score to at least a Borderline Safe rating.

Not only will the company's dividend coverage remain solid, but the firm expects the transaction to reduce its leverage. The spin-off company will raise debt to pay International Paper a dividend, which will be used to strengthen the balance sheet and further reinforce the company's BBB investment-grade credit rating.

We expect cash flow to remain strong, too. About 85% of International Paper's business will come from its industrial packaging business, which sells linerboards used primarily in packaging products such as cardboard boxes.

This market has consolidated over time to be dominated by just a handful of companies, and International Paper is the largest player.

As a result, the company's production capacity is positioned in the first quartile on the global cost curve, and the shrinking number of competitors has helped the industry's operating rates and pricing discipline.

While boxes are a commodity product, demand is slowly but steadily growing thanks to stable shipment trends in core markets such as food manufacturing, as well as strong increases in online sales of goods that now need to be shipped.

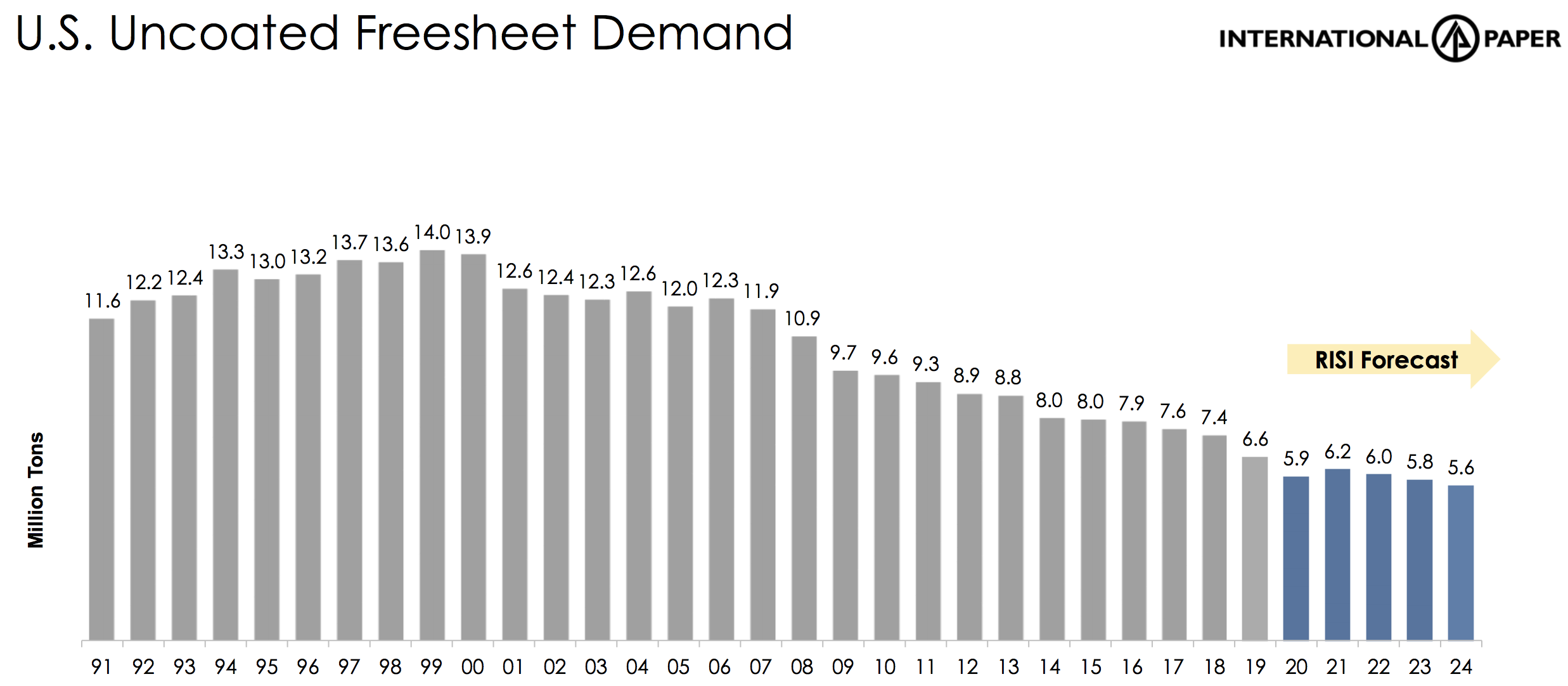

The printing paper business faces more dire prospects. This segment has seen its profits contract over the years as an increasingly digital world has reduced demand for paper.

Source: International Paper Investor Presentation

The spin-off company will need to continue fighting this structural headwind but is also expected to have a junk credit rating after taking on debt as part of the transaction, reducing some of its financial flexibility.

Although shares of the spin-off could trade at a cheap valuation to reflect these concerns, conservative investors may want to look elsewhere for safe income and healthy long-term growth prospects.

Overall, management hopes that separating this business from International Paper's core industrial packaging operations will allow both divisions to be managed more effectively. Losing a shrinking, lower-margin business could help International Paper achieve a higher valuation multiple, too.

We will continue monitoring the spin-off transaction's progress and provide updates as needed.