Natural Gas Price Slump Creates Uncertainty for Antero Midstream

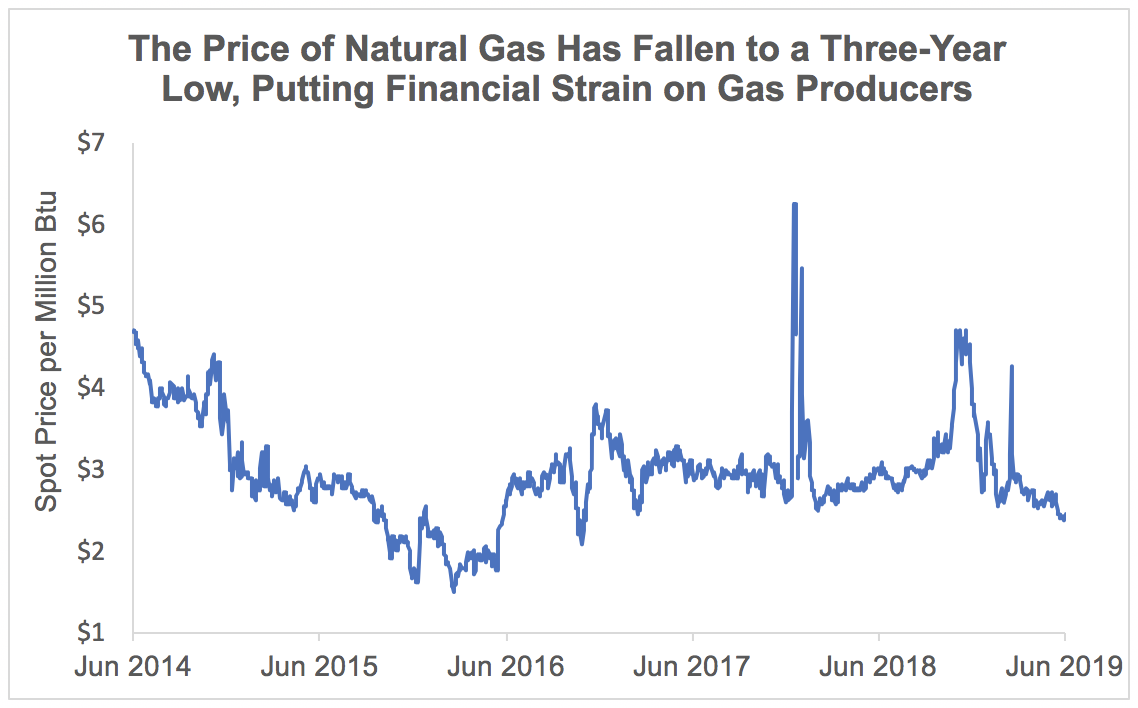

The price of natural gas has fallen about 20% over the last year to reach its lowest level since the summer of 2016. Mild summer temperatures, which reduce demand for gas used to power air conditioners, have contributed to the weakness. Meanwhile, U.S. gas production continues to rise, hitting a record earlier this year.

Source: U.S. Energy Information Administration, Simply Safe Dividends

Thanks to their use of long-term, fixed-fee, and take-or-pay customer contracts, midstream businesses such as Antero Midstream Corporation (AM) have long touted their ability to generate steady cash flow that is insensitive to the volatile prices of oil and gas.

While that has generally proven true, the recent slump in natural gas prices has pulled down AM's stock price and resulted in its shares sporting a dividend yield above 10%. Such a high yield can indicate something is wrong with a business, and the payout could be at risk of being cut.

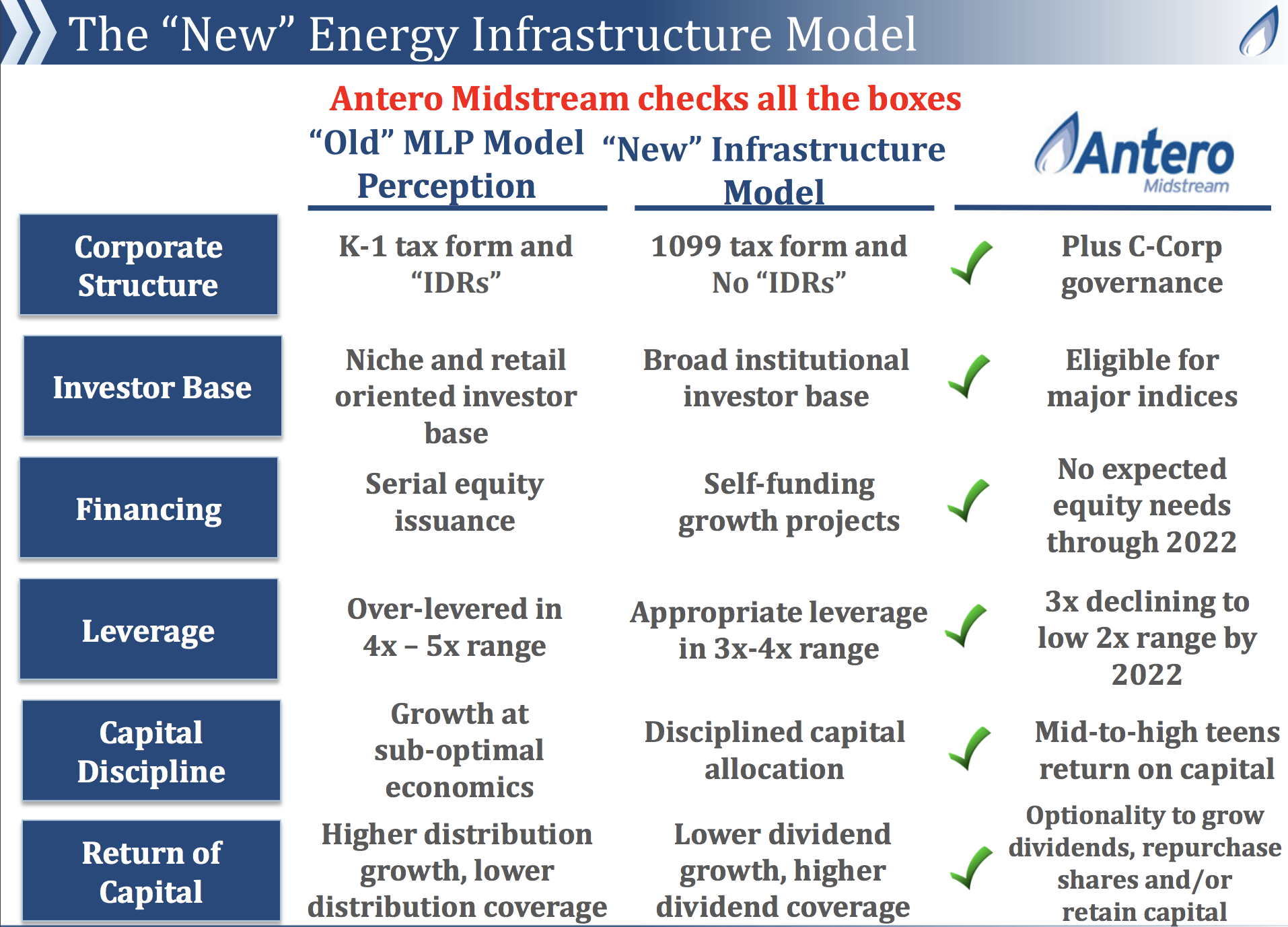

Antero Midstream's case is particularly interesting since just three months ago it completed steps to reduce its risk profile. Specifically, the firm used to be an MLP but merged with its general partner, eliminated its incentive distribution rights, and converted to a corporation.

Many MLPs have completed their own simplifications in recent years with hopes of expanding their investor base, reducing their long-term tax burden, de-risking their growth financing, enhancing governance and shareholder rights compared to the MLP structure, and allowing them to run a more conservative business in general.

Source: Antero Midstream Investor Presentation

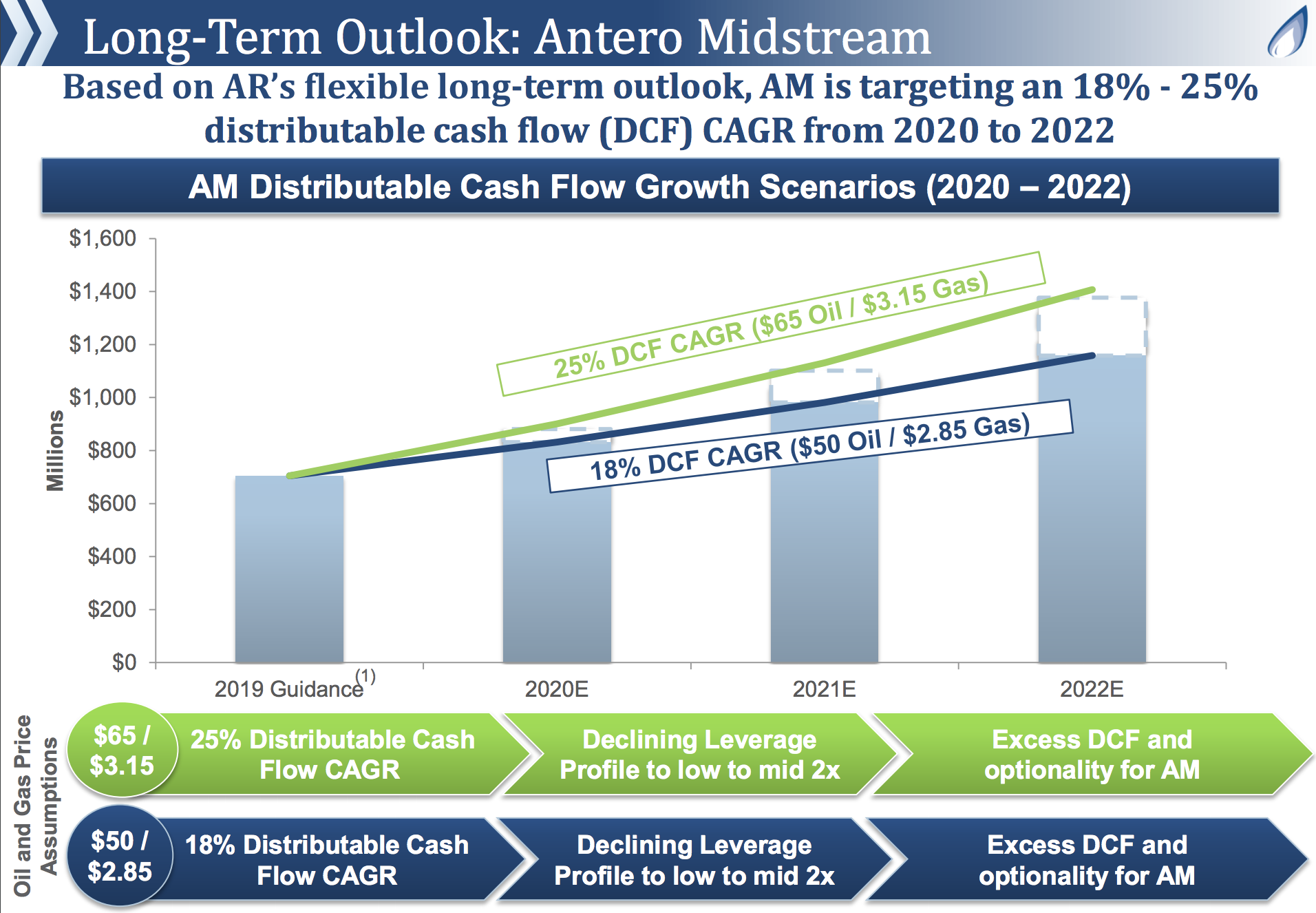

As we discussed in our March note, Antero Midstream's simplification resulted in higher leverage and lower coverage of its distribution (1.1 to 1.2 times coverage expected in 2019), though both of those important dividend safety areas are expected to improve in the future if cash flow growth goes according to management's plan.

Source: Antero Midstream Investor Presentation

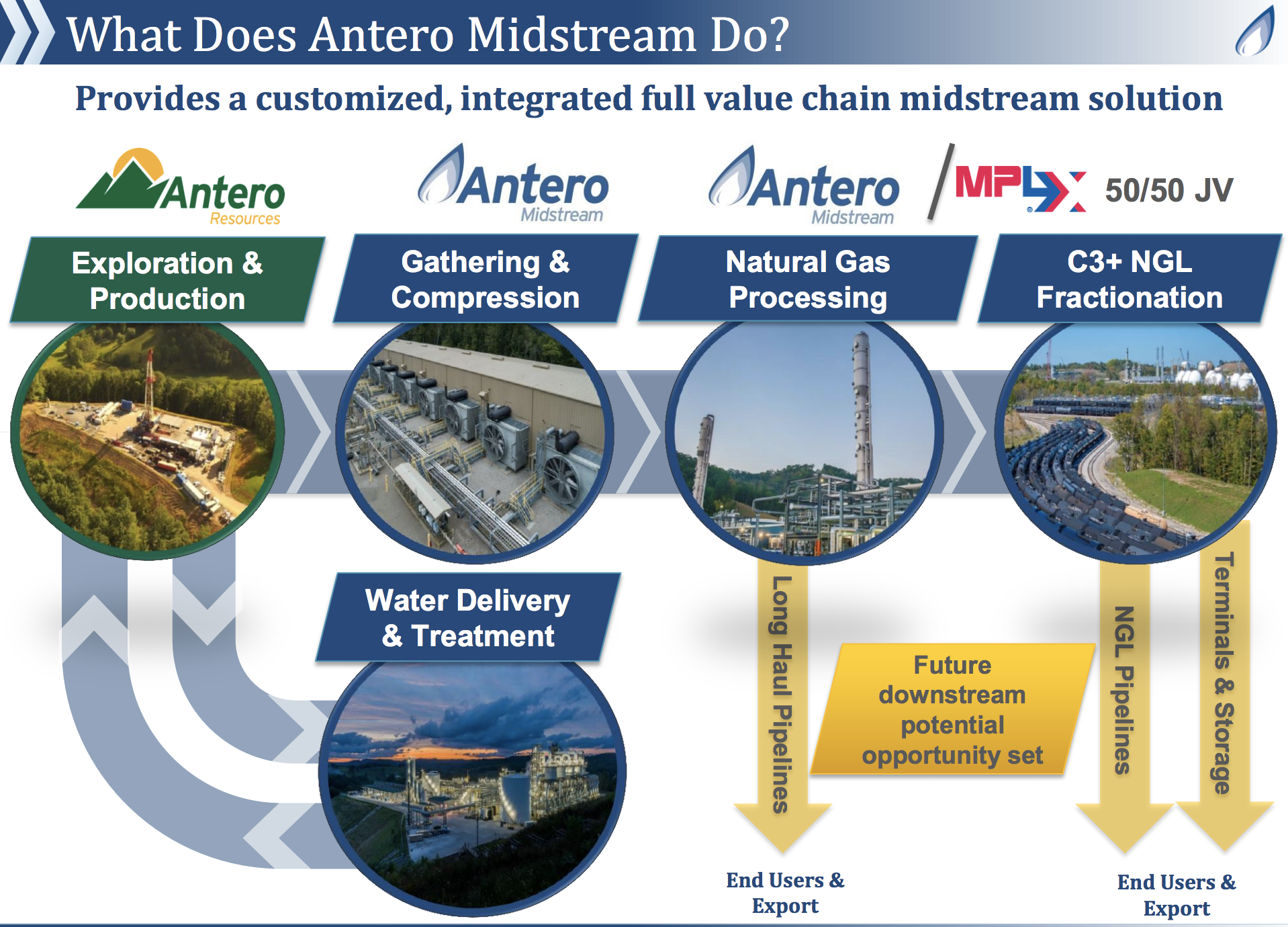

However, the weak price of natural gas has potential to disrupt the company's plans for the future. Recall that virtually all of Antero Midtream's revenue is generated from one customer, Antero Resources (AR).

Antero Resources is the largest natural gas liquids producer in the U.S. and the fourth largest natural gas producer in the country with approximately 3,000 core drilling locations. Antero Midstream's integrated midstream assets support Antero Resources' exploration and production activities.

Source: Antero Midstream Investor Presentation

All of Antero Midtream's revenue is generated from fee-based contracts tied to the volumes of natural gas that the firm gathers and compresses and water that it handles and treats for Antero Resources.

Unfortunately, not all of Antero Midstream's contracts have minimum volume commitments. The company does not specify what percentage of its cash flow is supported by take-or-pay contracts, but in its 10-K filing it notes that the pipelines and compressor stations it had in place prior to its late 2014 IPO do not have minimum volume commitments:

"The gathering and compression agreement includes minimum volume commitments only on new high pressure pipelines and compressor stations that we construct subsequent to our initial public offering in November 2014 at Antero Resources’ request.

The high pressure pipelines and compressor stations that existed prior to our initial public offering are not supported by minimum volume commitments from Antero Resources. Any decrease in the current levels of throughput on our gathering and compression systems could reduce our revenue and cash flows and adversely affect our ability to make cash distributions to our unitholders."

The good news is pipelines and compressor stations built after 2014 appear to account for the majority of Antero Midstream's asset base today. Management also notes that their contracts call for Antero Resources to utilize or pay for 70% to 75% of their capacity for the first 10 years following their completion, supporting the stability of Antero Midstream's cash flow.

But in light of depressed natural gas prices, what if Antero Resources sees its production decline or can't honor the terms of its contracts with Antero Midstream?

Shares of Antero Resources have lost more than 70% over the past year as investors worried about the firm's financial health and long-term growth potential. Antero Resources previously indicated it could achieve free cash flow neutrality at $50 per barrel oil and $2.85 gas, but gas prices sit near $2.40 today.

Source: Antero Resources Investor Presentation

The company's gas volumes are 100% hedged for 2019 at $3.00 and 90% protected in 2020 at $2.87, providing some short-term relief. However, if the price of gas remains weak, Antero Resources will struggle to generate free cash flow and deleverage its balance sheet like it had previously hoped.

Earlier this year Antero Resources reaffirmed its long-term outlook of 10% to 15% annual production growth. However, lower commodity prices could reduce the amount of natural gas the company can produce economically.

Furthermore, in its 10-K, Antero Midstream notes that "natural gas volumes from completed wells will naturally decline and our cash flows associated with these wells will also decline over time. In order to maintain or increase throughput levels on our gathering systems, we must obtain new sources of natural gas from Antero Resources or third parties."

In other words, a sustained reduction in development or production activity would likely result in reduced utilization of Antero Midstream's assets and spell bad news for the firm's distributable cash flow. The firm's balance sheet and payout ratio are already higher than management desires following the recent simplification transaction, so this is a rather delicate situation.

Until Antero Resources finds itself on more stable ground, demonstrating it can and will continue honoring its contracts and growing its gas production, Antero Midstream's stock will likely remain beaten down.

These situations are difficult to evaluate. Even Antero Midstream says it "cannot predict the extent to which Antero Resources’ business would be impacted if conditions in the energy industry deteriorate, nor can we estimate the impact such conditions would have on Antero Resources’ ability to execute its drilling and development program or perform under our gathering and compression and water handling and treatment services agreements."

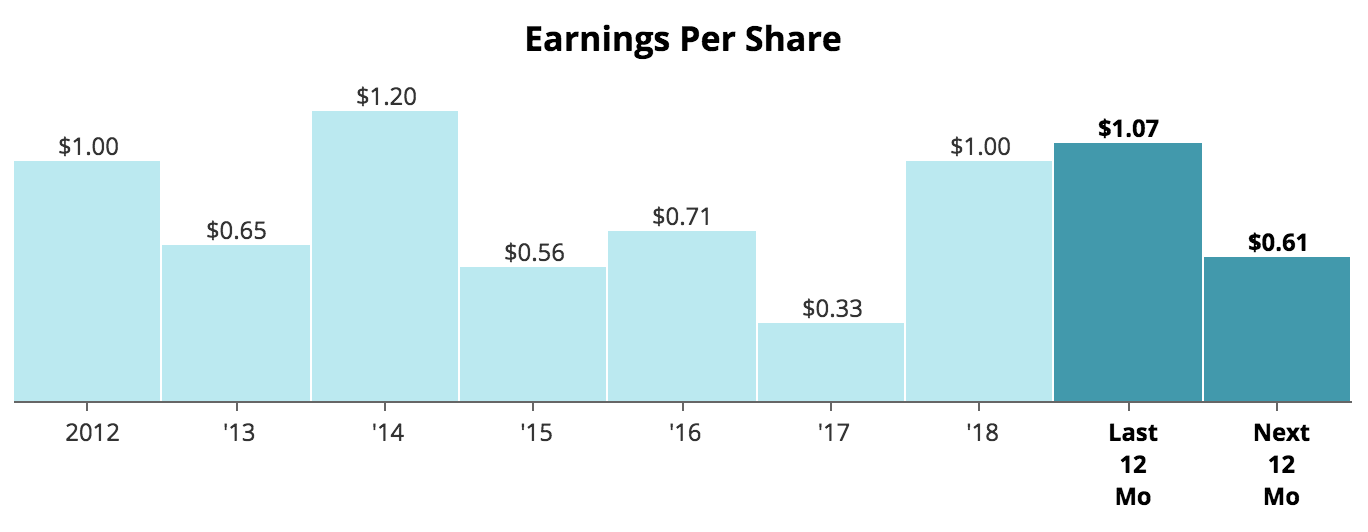

Investors should monitor Antero Resources' financial health and any updates it provides to its production guidance going forward. The company's earnings are very volatile (see below), just like the price of natural gas, so it's hard to say if the latest slump in energy prices will cause management to revise its production growth targets. For now, Antero Midstream will retain is low Borderline Safe Dividend Safety score.

Antero Resouces – Source: Simply Safe Dividends

Investing in smaller companies usually means accepting more risk in the form of less diversified cash flow streams. Antero Midstream is no exception, with primarily one customer accounting for all of its business, plus all of its assets operating in one region and focused primarily on natural gas production.

The company's recent simplification has improved its long-term risk profile, including a move to a self-funding business model. However, conservative income investors are likely better off sticking with larger, more diversified midstream businesses that are less sensitive to commodity prices and the performance of any single customer.