Hershey Has Paid Uninterrupted Dividends Since 1930

Founded in 1894 in Hershey, Pennsylvania, Hershey (HSY) manufactures and sells chocolate and other confectionery products including gum and mints; baking ingredients such as toppings, beverages, and syrups; and snack items, including spreads, meat snacks, bars, mixes, popcorn, protein bars, and cookies.

These products are marketed under over 80 leading brands including Hershey’s, Reese’s, Kisses, Kit Kat, Jolly Rancher, Almond Joy, Brookside, barkTHINS, Cadbury, Payday, Rolo, Twizzlers, York, Ice Breakers, SkinnyPop, Krave, and Bubble Yum.

Internationally (the company sells in over 90 countries), the company's brands include Pelon Pelo Rico, IO-IO, Nutrine, Maha Lacto, Jumpin, Sofit, and Tyrrells.

Source: Hershey

While Hershey sells its products in about 90 countries, over 80% of its revenue and profits are generated in the U.S. and Canada.

Hershey has paid a higher dividend every year since 2009 and has maintained or grown its payout every year since 1930.

Business Analysis

Mature consumer foods companies like Hershey are known for their stability. Their business models usually evolve very slowly, and consumers continue to eat during good times and bad.

Importantly, their brands enjoy prominent shelf space thanks to decades of marketing investments, longstanding relationships with retailers, and well-known tastes that customers have historically been willing to pay a premium for.

However, their future success depends on the ability of their name brands to stay relevant as consumer preferences and shopping habits evolve. Fortunately, few companies have a stronger portfolio of brands than Hershey.

Over the past 125 years, Hershey has built up a strong assortment of popular candies and snack foods. For example, the Hershey bar was first produced in 1900, Kisses were conceived in 1907, Reese's peanut butter cups launched in 1928, and the Kit Kat bar was invented in 1935.

The company supports these product lines and others with substantial advertising spending. Including R&D to support new product launches, the company generally reinvests about 8% of sales (more than $600 million annually) into activities that help secure or grow its market share.

Over the past five years, Hershey has invested about $3 billion into marketing and R&D, a figure few rivals can match. In fact, in order to break into the retail market upstart brands typically have to pay retailers slotting fees that makes competing with industry giants like Hershey even more challenging.

The firm's brand-building efforts and longevity (many decades of spending to promote awareness of its products) have helped Hershey carve out an impressive 30% market share position across all U.S. confectionery sales while maintaining some of the most emotionally loved brands with parents and kids.

Source: Hershey Investor Presentation

Importantly, private label products account for less than 5% of the market. Unlike some other food categories, when consumers want to indulge on a guilty pleasure snack in the confectionery market, they have shown a habit of buying products sold under their favorite brands.

As a result, Hershey has historically raised prices faster than inflation and sports one of the highest gross margins of any consumer packaged good company.

Hershey's dominance is also reflected across its top six brands (Reese's, Hershey's, Kit Kat, Ice Breakers, and Kisses), which on their own generate $5.9 billion in annual revenue (about 75% of company sales).

The popularity of these mega brands gives Hershey a solid position with grocers, convenience stores, and other retailers in terms of securing the best shelf space and holding its prices. These companies want proven products that sell quickly and draw customers to their stores.

Hershey's chocolates and snacks have long demonstrated an ability to help retailers achieve success. Combined with its large advertising spending, Hershey has historically defended its market share well against smaller rivals with less proven brands.

While the slow-changing nature of the packaged food industry helps Hershey defend its market share, demand rises slowly as well, tracking population growth over time.

As a result, like many food companies, Hershey relies on acquisitions to help fuel its growth. In fact, the company and has bought over 50 businesses and brands since 1963. Most recently, Hershey's acquisitions have focused on taking part in the "healthier snack" movement as consumer tastes evolve.

From beef jerky to popcorn and chips, Hershey's long-term growth plan is to expand its portfolio into other faster-growing, high-margin categories while maintaining its dominance in the U.S. confectionery market.

Despite its focus on acquisitions, Hershey has historically maintained modest debt levels. The Hershey Trust controls roughly 80% of the firm's voting rights, instilling a conservative approach that has earned Hershey a strong "A" credit rating from Standard & Poor's. As a result the firm has financial flexibility to continue investing in its brands, acquiring on-trend products, and returning cash to shareholders.

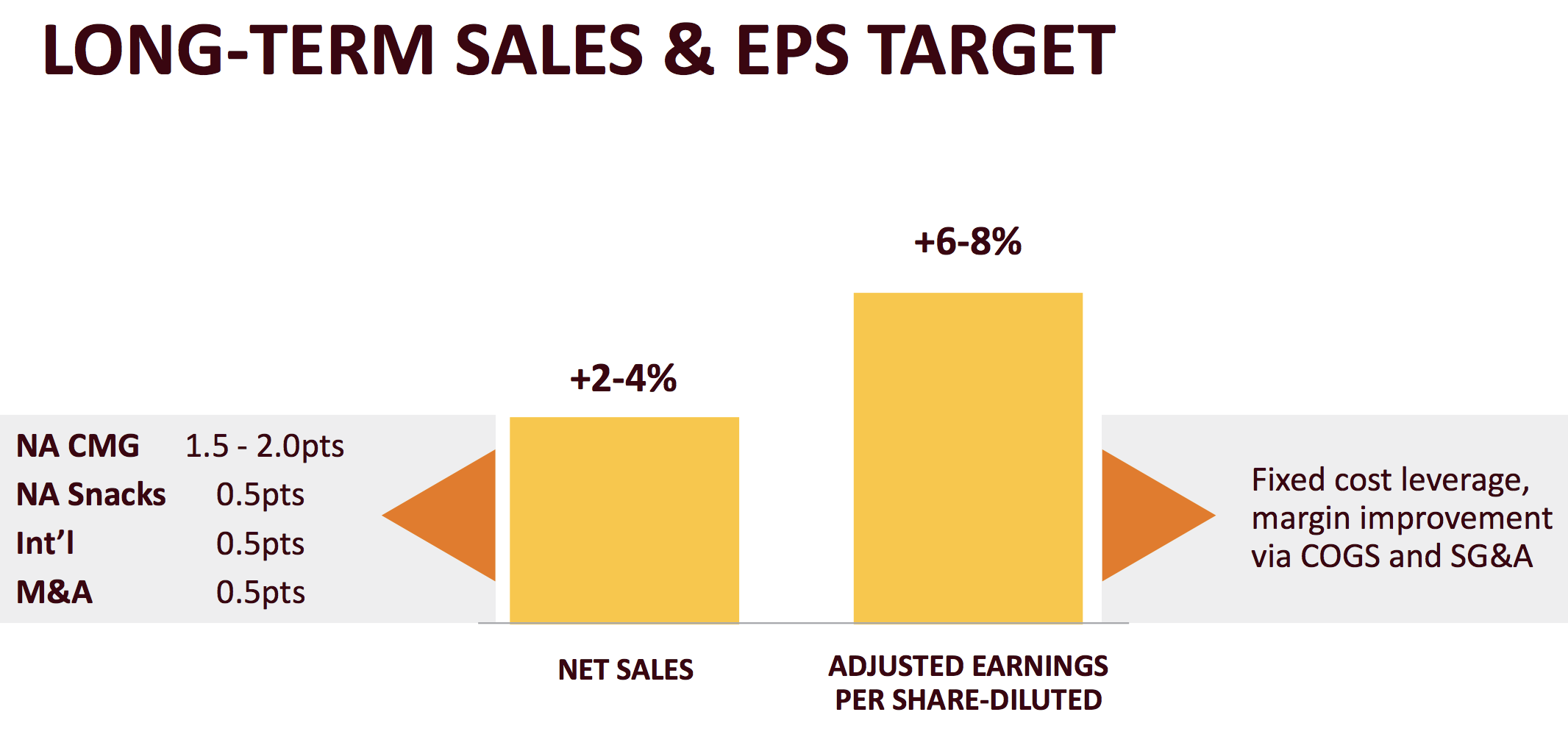

Over the long term, Hershey's sales seem likely to grow at a low single-digit pace. The U.S. food industry is very mature and becoming increasingly competitive due to changes in consumer tastes and shopping habits, which could make organic growth more difficult for Hershey.

However, the firm's brands remain strong in their core categories, and acquisitions will continue supporting top-line growth as well. Combined with some cost cutting, management believes the business can deliver 2% to 4% annual sales growth and 6% to 8% EPS growth over time.

This guidance is essentially in line with the company's historical growth rates and thus seems reasonable.

Source: Hershey Investor Presentation

The company says it remains committed to a dividend payout ratio of at least 50%, which is about where this metric has sat for Hershey for more than a decade. Therefore, Hershey's dividend growth will likely continue tracking its EPS growth, increasing at a mid-single digit pace going forward if all goes well.

However, while Hershey appears to be one of the better consumer foods companies available today, there are still risks that investors need to consider.

Key Risks

Like many large packaged food companies, Hershey has faced some growth challenges from shifting consumer tastes. Specifically, high-calorie candy is out of fashion with some of today's more health-conscious eaters, making volume growth more difficult.

While Hershey's top line is still growing and the firm is moving in the right direction with acquiring and marketing healthier snacks, keep in mind that about 75% of its sales come from its top six mega brands, which do not fit with what might be a permanent secular trend in consumer tastes and shopping habits.

In the past few years, management has said that mass-market advertising for some of its smaller brands has not been having the desired returns on investment. Thus Hershey refocused its market efforts on its core brands, but again those are its dominant candy names which could struggle to generate modest organic growth.

In such a scenario, Hershey could find itself increasingly dependent on making acquisitions to expand and diversify its business, which is a riskier growth strategy. Every M&A deal comes with the risks of overpaying for assets, increasing debt on the balance sheet, and failing to achieve its targeted long-term synergies.

Volatile commodity costs are another risk factor to consider, although they are unlikely to threaten Hershey's long-term earning power. The company's chocolate-focused products require a number of raw ingredients, including cocoa powder.

Prices for these raw materials and others can swing meaningfully from one quarter to the next, potentially crimping Hershey's profitability. To protect its margins the firm has historically been able to raise its selling prices above inflation rates, flexing the strength of its popular candy brands.

However, Hershey's concentration with retailers such as Walmart could reduce its pricing power in the future. Mass retailers have struggled with maintaining their own margins as they move to a more online-focused business model, making them even more reluctant to accept higher prices from name brands.

For now, Hershey appears to be executing better than most of its packaged food peers as the environment evolves. Management is sticking to the company's strengths while maintaining a safe balance sheet as it pursues both organic and acquisitive growth.

Closing Thoughts on Hershey

Hershey is one of America's best food company success stories, having spent over 100 years building up a stable of beloved candy and snack brands. The chocolatier still enjoys a wide moat today, created by industry-leading economies of scale, a large advertising budget, and premium shelf space across its core U.S. market.

Management's long-term plan to increasingly mix in healthier snack brands, while continuing to cut costs and boost margins, should continue delivering safe, growing dividends over time.

That being said, with 75% of sales currently derived from just six candy mega brands, Hershey could struggle with slower sales growth than it has enjoyed in the past. Investors will want to monitor Hershey's top-line growth in the coming years to make sure that management's long-term shift to healthier and more popular food items is actually achieved, without sacrificing margins.

Even if long-term growth is ultimately slower than expected, Hershey should remain a cash cow with an extremely safe dividend thanks to its well-known products, the entrenched nature of guilty pleasure snacks, and management's financial conservatism.