American Tower: An Attractive and Fast-Growing REIT

American Tower (AMT) was founded in 1995 and converted to a REIT business structure in late 2011, minimizing its taxes on its real estate assets and kicking off its dividend program.

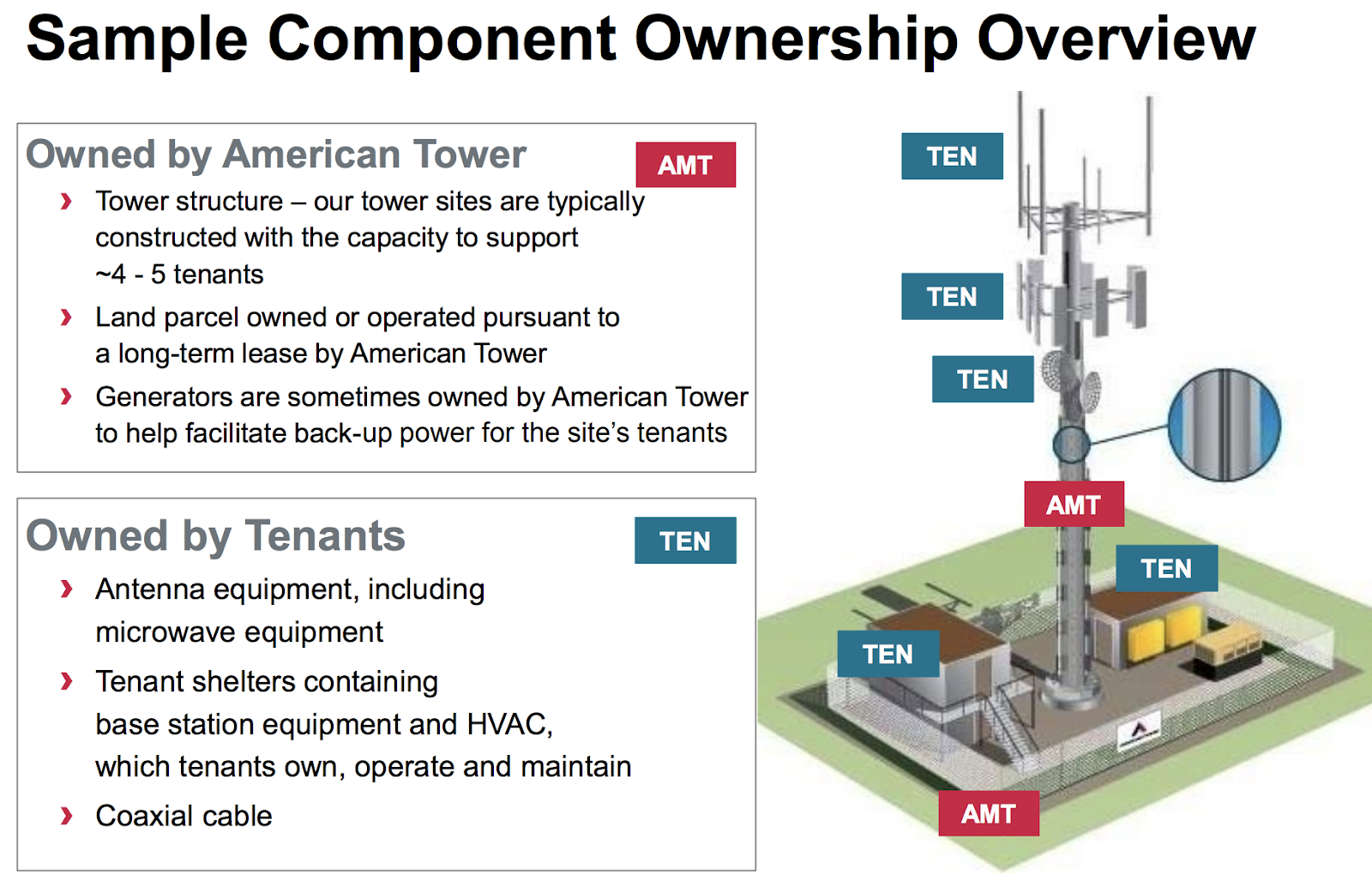

The company owns a portfolio of approximately 171,000 towers that are located mostly in suburban and rural areas and leased out to wireless carriers under long-term contracts. American Tower’s infrastructure is used by carriers to provide wireless service to consumers and businesses, transmitting signals between towers and mobile devices. Most towers have the capacity for 4 to 5 tenants.

American Tower operates similarly to a triple-net lease REIT in that its tenants pay for almost everything needed to transmit signals (communications equipment, cables, antennae, etc.) except the tower and land that American Tower maintains. As a result, the company's maintenance costs are extremely low and its adjusted EBITDA margin in 2018 exceeded 60%.

Source: American Tower Investor Presentation

Unlike Crown Castle International (CCI), the other telecom tower REIT which is purely focused on the U.S. despite its name, American Tower's assets are located across four continents. At the end of 2018 about 76% of the company’s communications sites were located internationally, where prices and capacity utilization are lower than the mature U.S. market.

As a result, while only 46% of American Tower’s property revenue is derived in America, over 60% of its total operating profit is generated in the U.S. with the rest from international markets (Latin America 16% of profit, Asia 15%, EMEA 6%).

Source: American Tower Investor Presentation

American Tower’s large international reach helps the business achieve reasonable tenant diversification. The company’s largest customers are AT&T (16% of revenue), Verizon (15%), Sprint (9%), and T-Mobile (9%).

Globally, where the company is especially focused on India (17% of revenue) and Brazil (8% of revenue), its largest tenants are Vodafone (7% of rent), Airtel (6%) and Telefonica (4%).

American Tower has raised its dividend for six straight years (usually every quarter), ever since it became a REIT. Management says it plans to grow the dividend at least 20% in 2019, which will be the 7th consecutive year of at least 20% payout growth.

Business Analysis

American Tower has arguably one of the most predictable and lucrative business models of any dividend stock in the market.

First, the company enjoys very high visibility into future earnings thanks to its long-term leases with wireless service providers. Almost all of American Tower’s leases are non-cancellable and usually include an initial term of at least 5-10 years with multiple 5-year renewal periods.

Price escalators are embedded into American Tower’s leases as well, with the U.S. averaging 3% annual price increases and international markets’ escalators typically based on local inflation indices.

These predictable pricing gains provide a dependable base for organic growth, which has averaged about 7% to 8% in recent years (mid-single-digits in the U.S. and double-digits overseas). This has allowed the REIT to enjoy double-digit annual growth in operating profits, adjusted EBITDA, and AFFO per share for more than a decade.

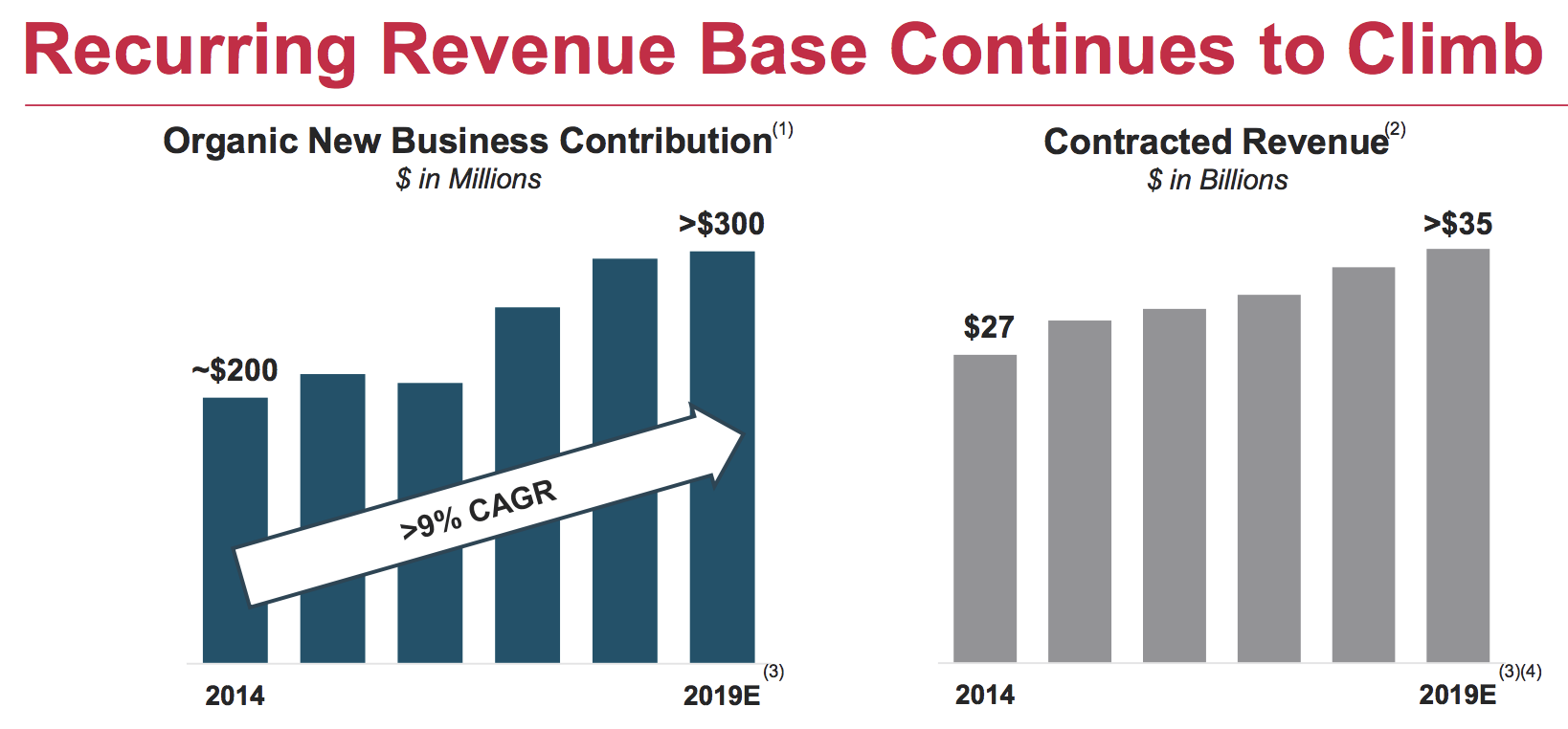

The future remains bright, too. American Tower ended 2018 with $35 billion in non-cancellable tenant lease revenue, which provides great visibility because that amount is worth about five times the company’s annual property revenue and has steadily grown over the years.

Source: American Tower Investor Presentation

When leases have come up for renewal, the company has historically enjoyed 98-99% annual renewal rates based on property revenue, reflecting the limited alternative sites that tenants have to choose from (regulation and zoning requirements help limit supply).

Another reason why American Tower enjoys such strong renewal rates is that it’s historically been cheaper for wireless carriers to outsource their communications site infrastructure needs rather than build and operate their own tower sites.

By spinning off their towers to companies such as American Tower, wireless service providers free up capital that can be used to pay down debt and reinvest in their networks’ quality, which is core to their businesses. Management estimates that over 20 years leasing one of its towers will save a telecom carrier $201,000 compared to building and owning it outright.

What's more, according to industry peer Crown Castle International, it costs about $40,000 to remove a telecom carrier's equipment from a tower and move it to a rival's. With rental leases running about $20,000 to $30,000 per year, this makes it uneconomical to move locations, helping explain why tower REITs enjoy retention rates of nearly 100%.

Not surprisingly, American Tower has historically benefited from wireless carriers exiting the operations of their tower sites.

For example, the company acquired exclusive rights to lease and operate more than 11,000 wireless communications towers from Verizon in 2015 for approximately $5 billion. These towers had existing average tenancy of 1.4 tenants per tower, well under their available capacity.

Other notable deals include American Tower’s purchase of a controlling stake in Viom Networks, an Indian cell tower company, for $1.2 billion in 2015. The company also entered into Nigeria, Africa’s most populous country, in a $1 billion deal in 2014.

In November 2017 American Tower announced it was buying 20,000 telecom towers in India from Vodafone (VOD) and Indian telecom Idea Cellular for $1.2 billion. Those towers came with non-cancellable 5-year contracts and the deal was immediately accretive to AFFO per share.

Most of these acquired towers, plus American Tower's business in general, are highly scalable, with virtually no cost to add additional tenants over time. And since retention rates are so high, it's easier for the REIT to eventually raise the number of tenants per tower.

Source: American Tower Investor Presentation

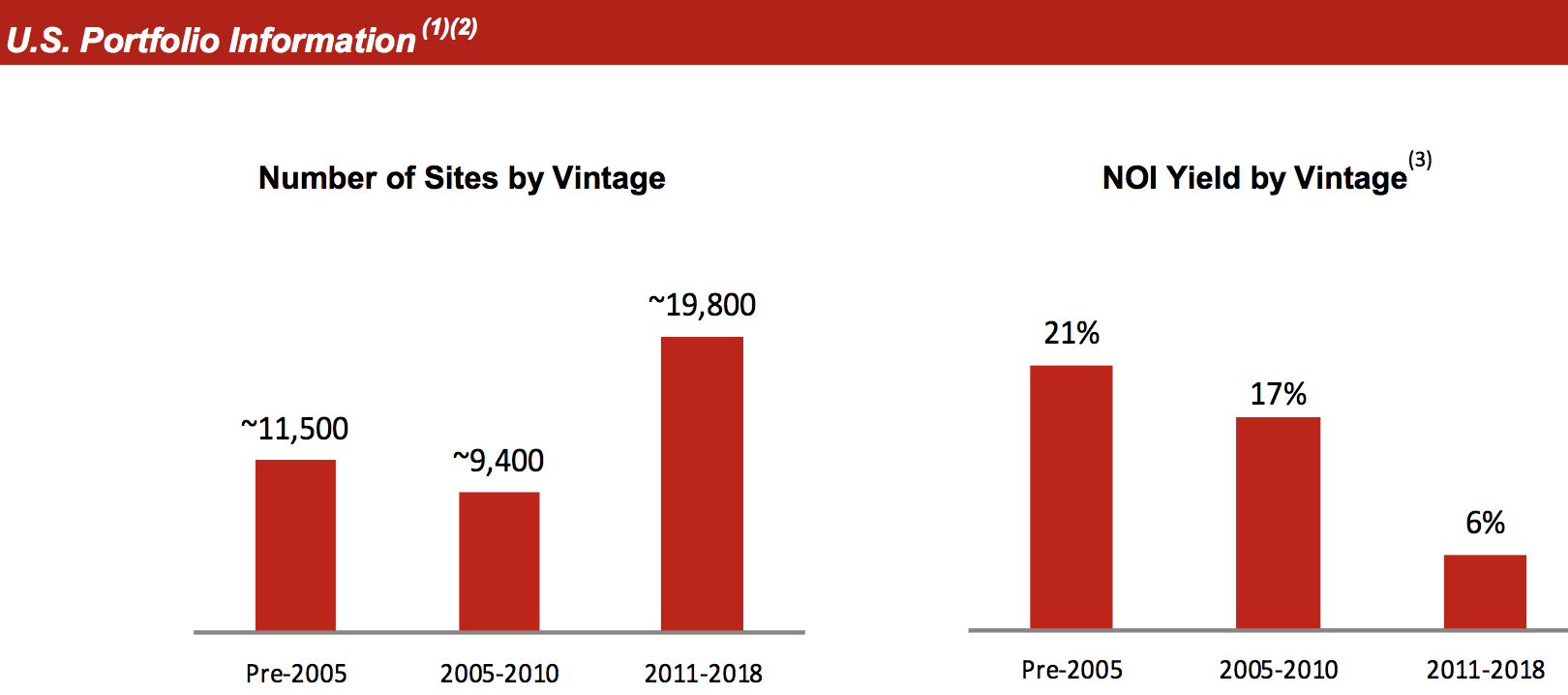

According to rival Crown Castle International, on average one new tenant gets added every 10 years, across its entire tower portfolio. This means the older a tower is (they last for decades) the more profitable it becomes, as seen by high net operating income (NOI) yields American Tower earns on its oldest vintage towers.

Source: American Tower Earnings Supplement

American Tower can capture incremental leasing activity on these underutilized assets and spread its fixed costs over a greater number of towers, driving its returns on invested capital higher over time.

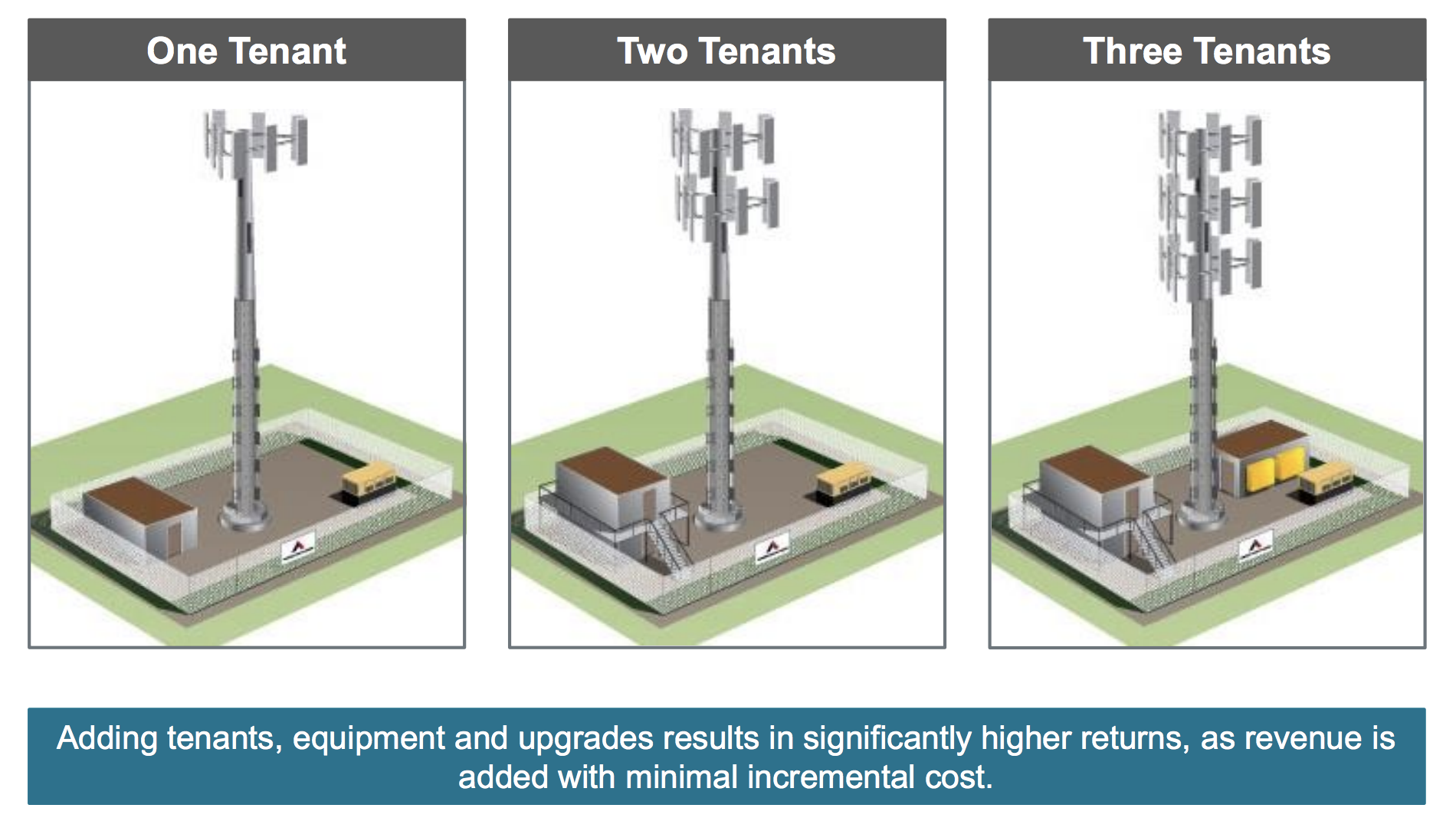

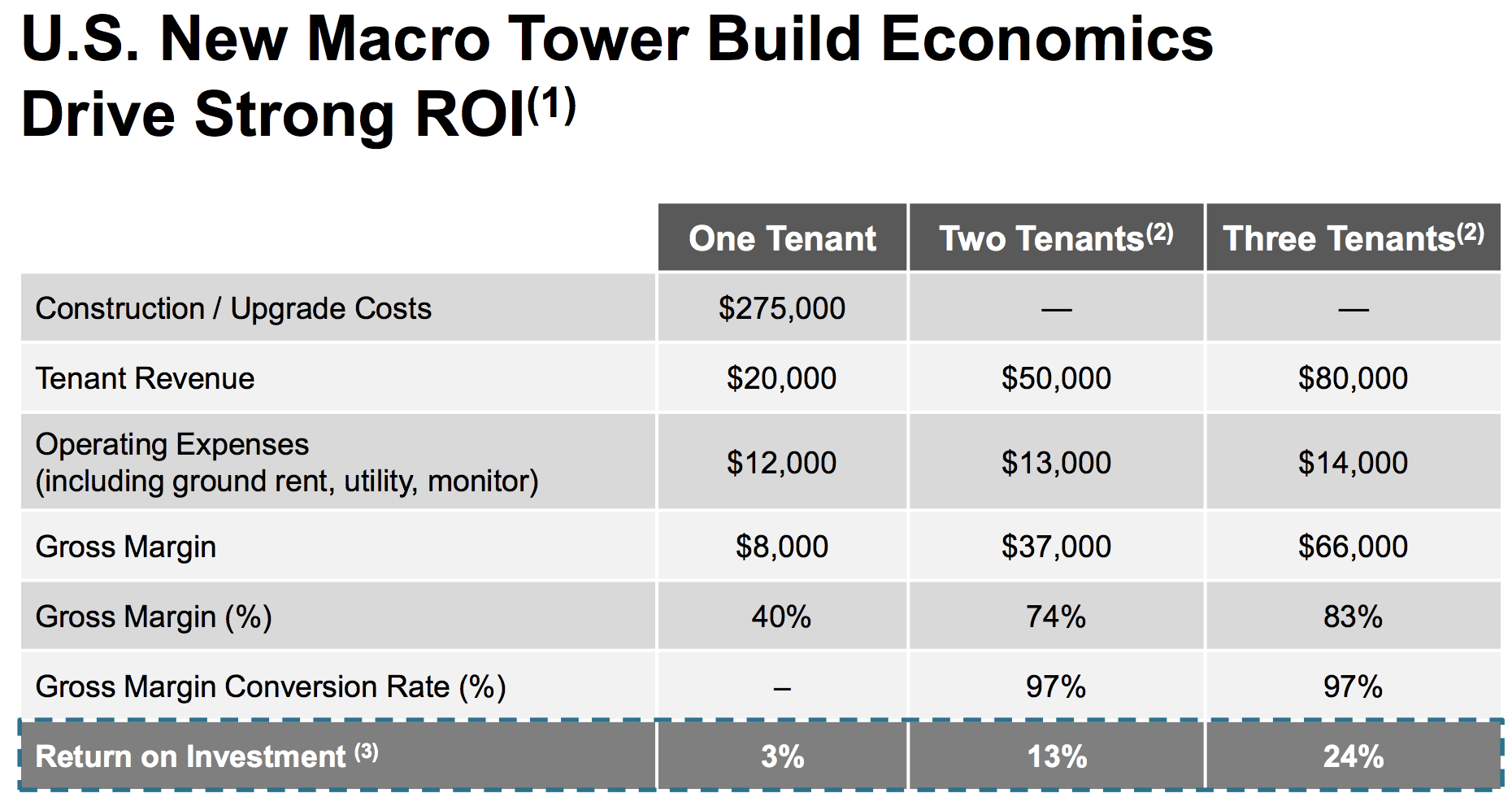

Simply put, adding additional tenants and equipment to existing towers is extremely profitable, with incremental gross margins of 97%. In fact, the company’s return on investment for each tower increases from 3% with one tenant to 13% and 24% with two and three tenants, respectively.

Source: American Tower Investor Presentation

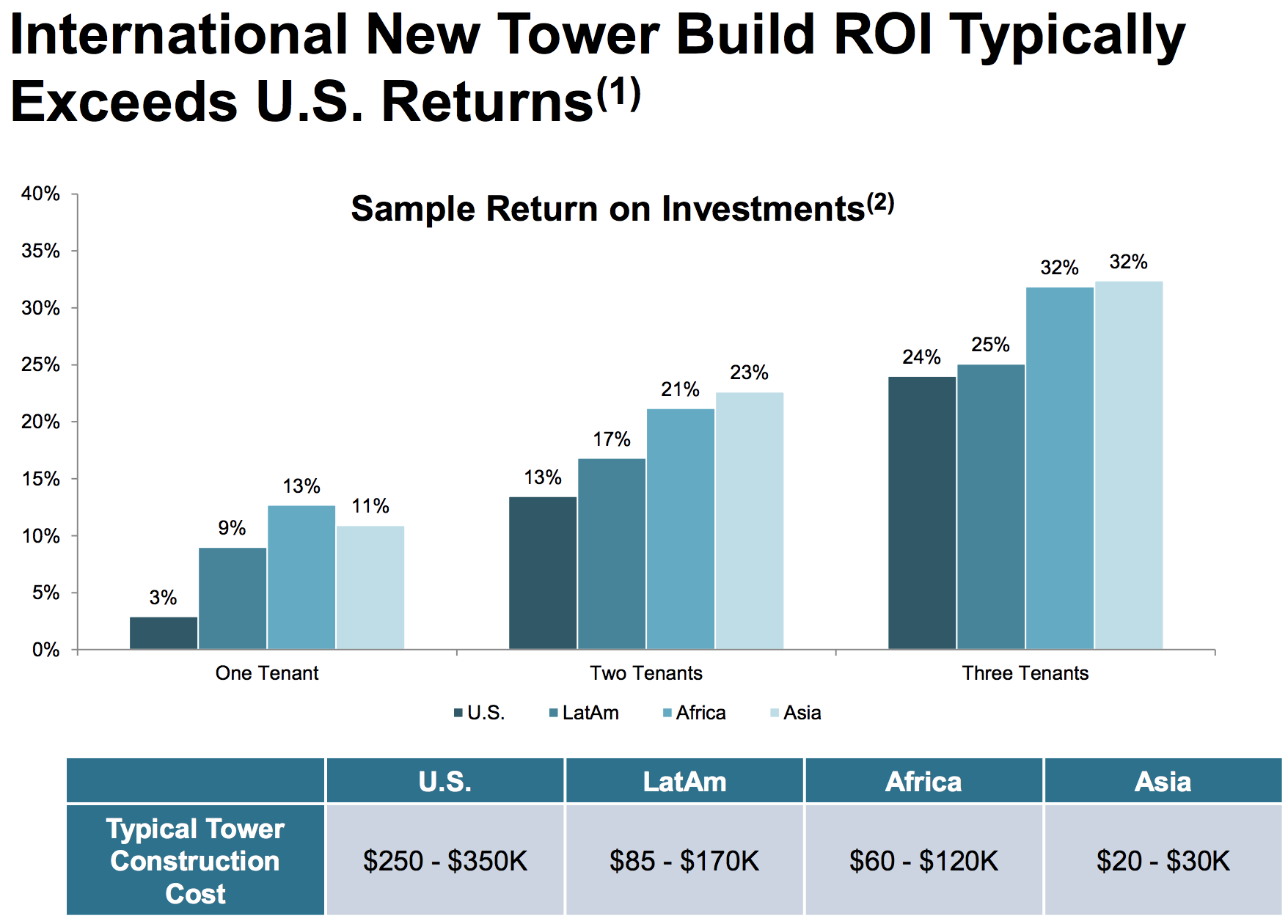

And internationally, thanks to much lower tower construction costs, the returns on investment are even better, up to 32% in Asia and Latin America once a tower is leased to three tenants.

Source: American Tower Investor Presentation

American Tower's ability to expand its high-return business through constructing new towers and making acquisitions is helped by its strong financial profile. The REIT's relatively low leverage and large scale help earn it a stable BBB- credit rating from Standard & Poor's. As a result, American Tower enjoys relatively low cost borrowing rates, which combined with the high profitability on its towers, results in excellent cash flow and dividend growth.

The firm's business model is also appealing because, unlike some REITs, American Tower’s maintenance capital expenditure needs are very low. Maintenance spending has historically averaged less than 3% of American Tower’s revenue. As a result, the company has been a free cash flow machine over the years.

With a global average of 1.9 tenants per tower (less than half of the available capacity), the company has substantial room available to add future tenants. As American Tower gradually fills out its towers around the world, its assets will likely earn significantly higher returns on capital because the incremental cost of adding a new tenant or additional equipment to an existing tower is very low.

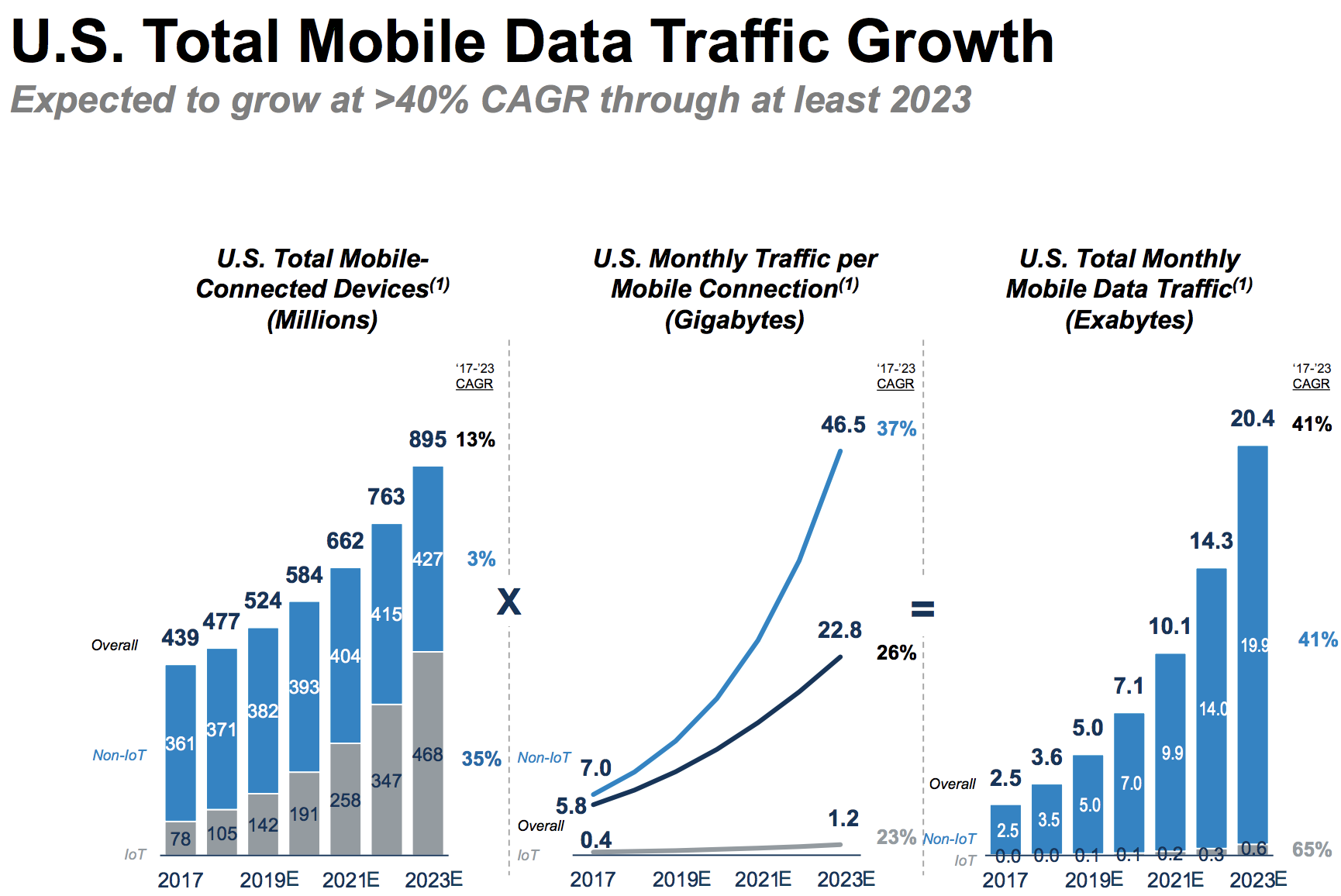

That tenant scale up seems likely to occur over time, driven by growth in mobile data. In the U.S. mobile data growth is expected to run about 40% annually through at least 2023, and the increased adoption of smartphones around the world is fueling the need for wireless carriers to continue investing in their networks’ density to meet demand.

Source: American Tower Investor Presentation

This is particularly true in markets outside of the U.S., where smartphone penetration in many regions is less than 50% today. The technologies deployed in most emerging markets are oftentimes 2G and 3G (i.e. much less advanced than those in the U.S. market), and American Tower’s occupancy rates are low by design, about 1.5 tenants per tower.

Wireless service providers in these markets will need to invest more in their networks to expand and improve their coverage, and increased adoption of wireless data applications (email, internet, video, etc.) and lower cost smartphones will put further upward pressure on network spending.

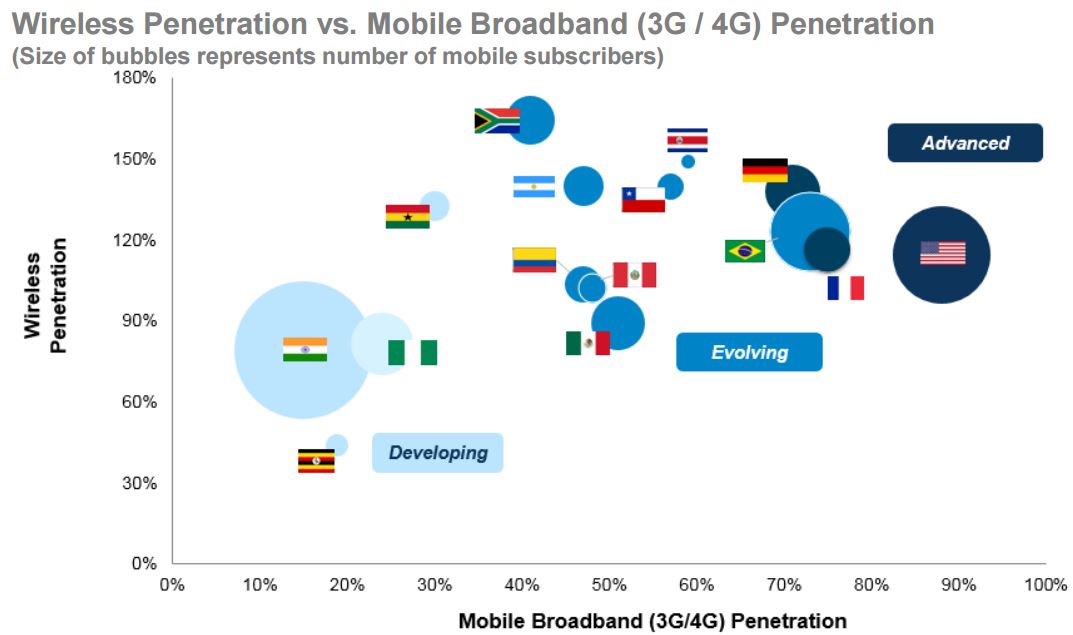

As you can see below, most developing and evolving markets significantly trail the U.S. in both wireless penetration rates and mobile broadband (3G/4G) penetration.

Source: American Tower Investor Presentation

Closing this gap will take many years, if not decades, but American Tower’s strategically-located infrastructure is positioned nicely for the increasing proliferation of wireless devices and the increasing usage of high bandwidth applications on those devices.

The company’s presence in many different markets that are in different stages of wireless development provides healthy diversification as well. With over 75% of its communications sites located internationally, American Tower should benefit from higher network spending over the coming years and decades.

Riding this secular trend should hopefully enable American Tower to continue delivering strong AFFO per share growth, just like it has done over the last decade. For 2019 management is guiding for 9% normalized AFFO per share growth, and according to FactSet Research, most analysts expect the REIT to grow cash flow per share at a double-digit pace over the next five years.

While there are numerous strengths to American Tower’s business, several notable challenges could arise in the future.

Key Risks

While fluctuating foreign currency exchange rates and volatile network infrastructure spending by wireless service providers can impact American Tower over the short term, these issues are unlikely to impair the company’s long-term earning power.

The primary risks that could structurally disrupt American Tower’s future are technological changes, customer consolidation, and the success of management’s capital allocation strategy.

Starting with technology, American Tower is obviously dependent on wireless service providers continuing to need its towers to transmit communication signals.

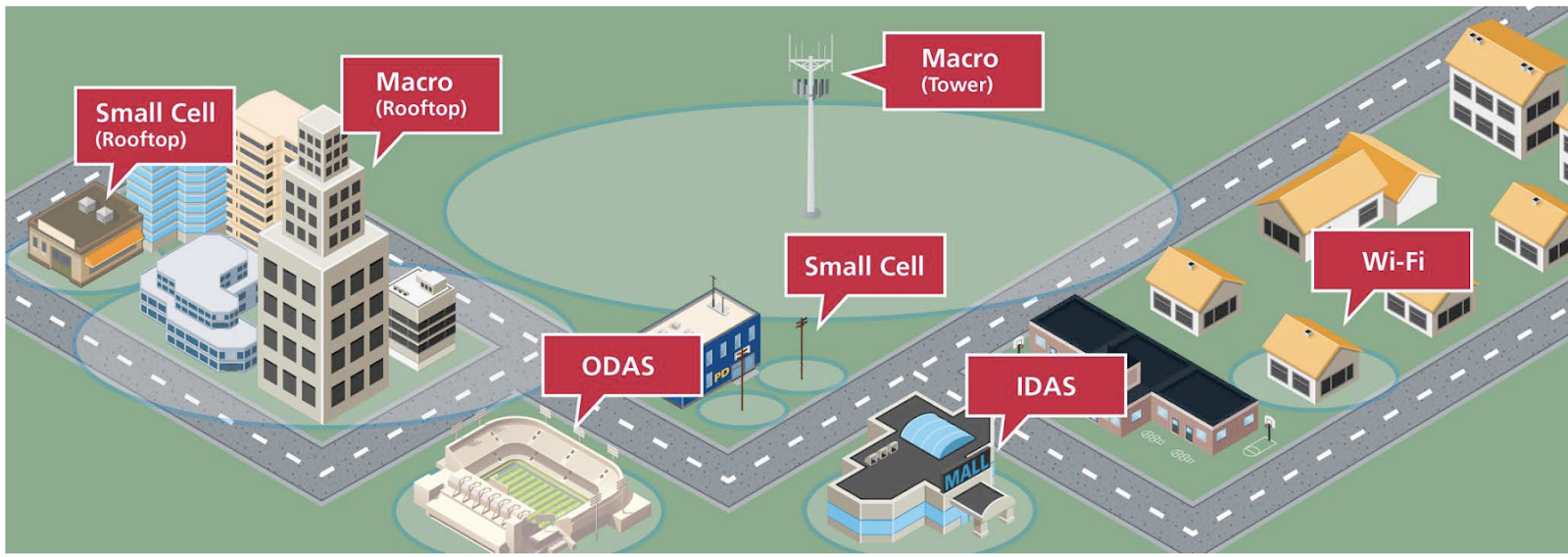

Network deployments today generally consist of multiple layers – traditional macro cell towers (like the ones American Tower leases out) provide a blanket of coverage, while a combination of other technologies (i.e. small cell) are also used to increase network capacity, especially in dense urban areas.

Source: American Tower Investor Presentation

The smartphone boom and widespread move to 4G wireless technology by U.S. carriers drove substantial demand for more macro sites (i.e. towers) over the last decade. In fact, the number of installed macro sites in the U.S. rose from 196,000 in 2006 to 315,000 in 2016, according to data from American Tower.

With many carriers now looking to 5G wireless technology, there is some uncertainty about what the final architecture and standards will look like – and how important tower sites will be.

5G standards have not been fully defined, much less deployed on a wide scale basis, but there is speculation that some infrastructure investment could shift to fiber and small cells to meet the density requirements of 5G.

This would potentially reduce the role of traditional towers in certain areas and threaten the favorable economics they enjoy today.

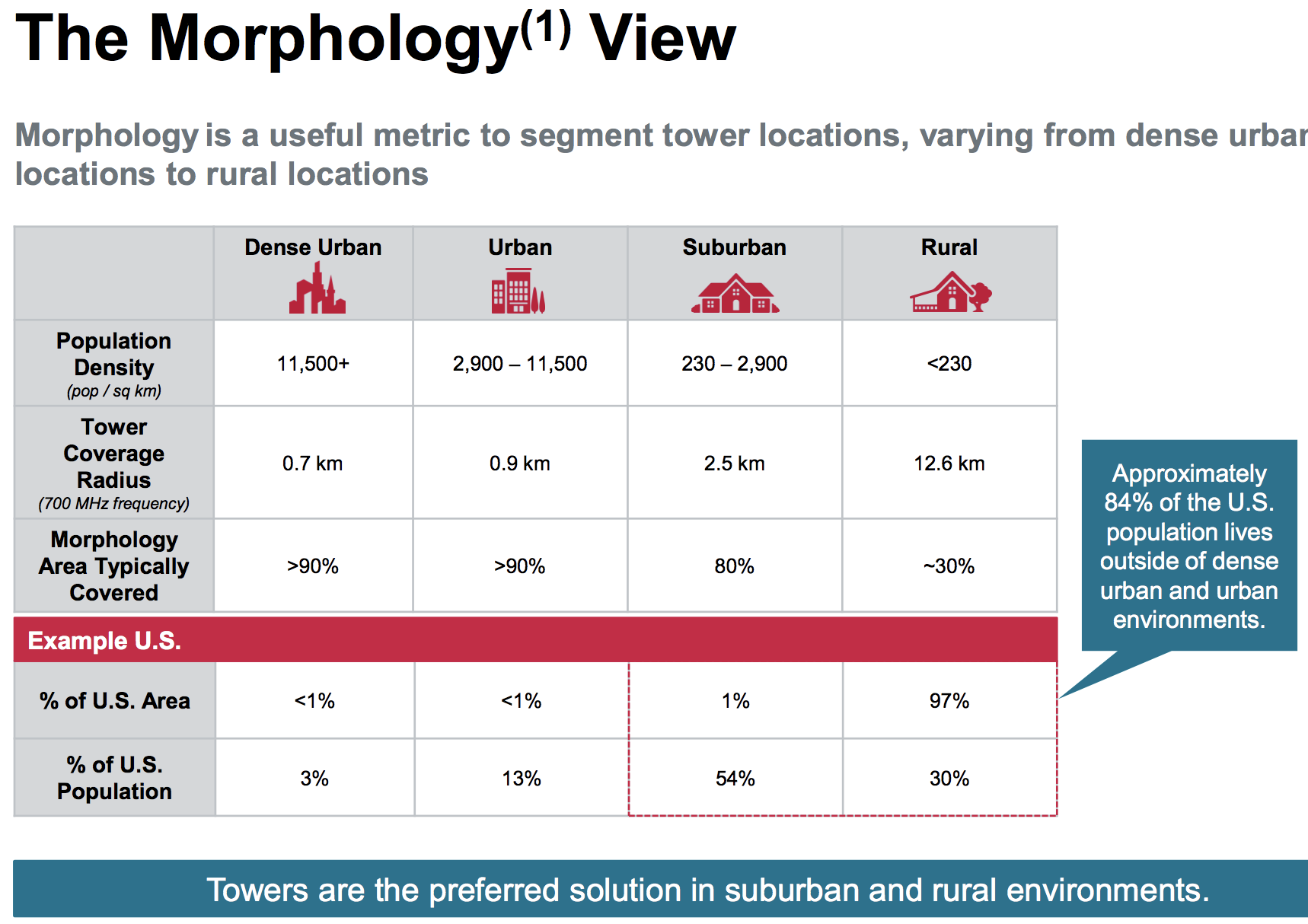

Fortunately for American Tower, in the U.S. just 16% of the population lives in areas ideally suited to small cells that might become the cornerstone of 5G.

Source: American Tower Investor Presentation

You can read more about how the tower companies are responding to this potential threat here. Not surprisingly, American Tower does not believe these new technologies are a viable alternative to towers but can complement them in certain cases, such as in densely populated areas.

Rural and suburban areas seem like less of a fit for small cell deployments, and continued growth in international wireless markets over the coming years can help American Tower continue diversifying away some of the 5G technology risk in the U.S.

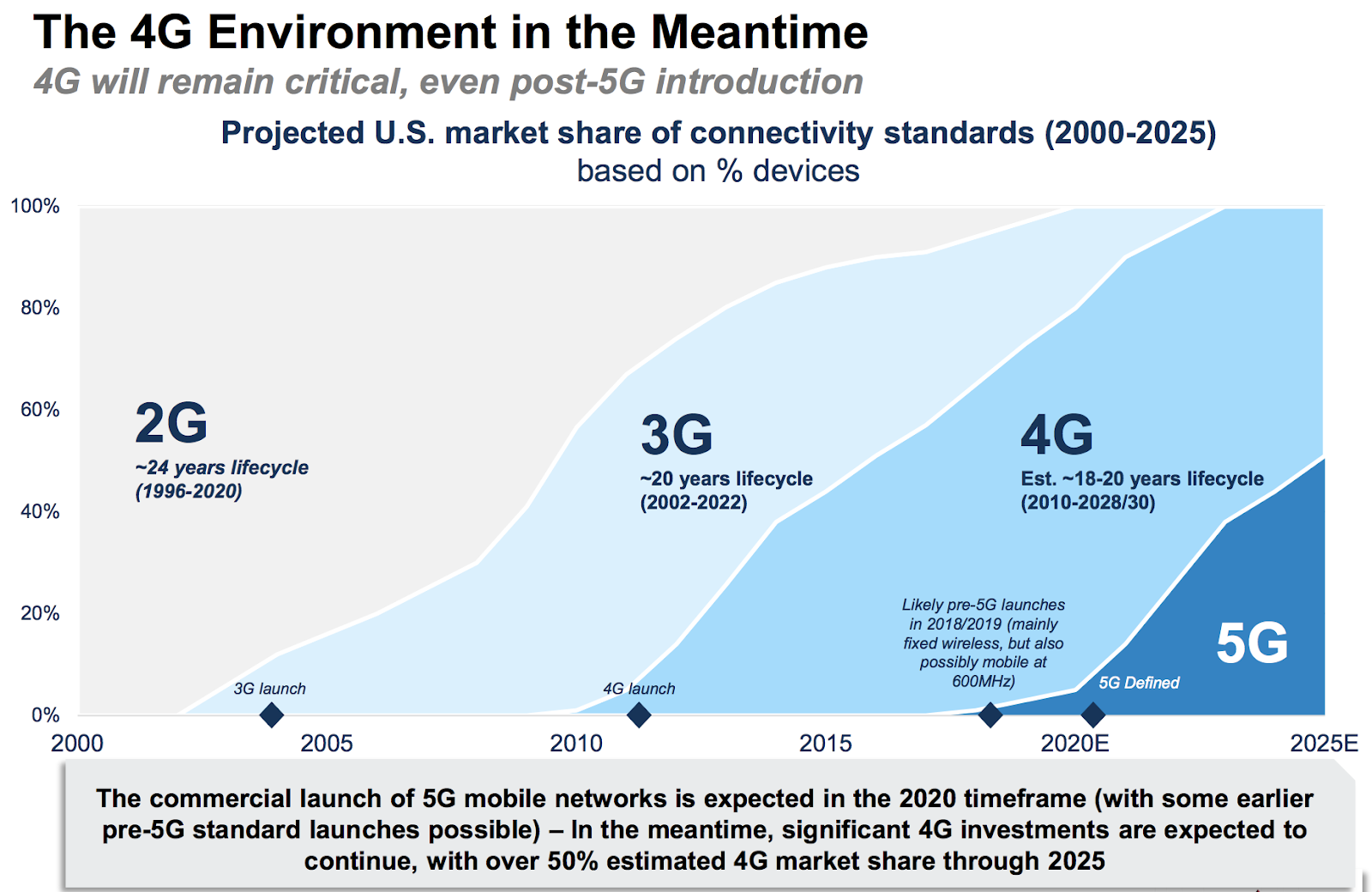

Importantly, 4G infrastructure is expected to maintain market share over 50% through 2025 as 5G begins to gradually ramp up. As you can see, while new generations of network technologies have been introduced in the past, the lifecycle of legacy technologies has continued to be 15-20 years or more.

Source: American Tower Investor Presentation

However, the risk is that improved future 5G technology might eventually make that competing technology a good alternative to towers. The 5G threat overseas is also going to rise over time, as urbanization packs more people into large cities where small cells are likely to prove more economical than towers.

Somewhat related to technology risk, it’s no secret that the major wireless carriers in the U.S. are struggling to grow their revenue. Their lack of growth is causing them to more closely scrutinize their deals with tower companies, who enjoy strong economics today.

According to Steel In The Air, “wireless carriers aren’t sitting idly by but are instead actively seeking to relocate some of their more expensive sites. Whether these efforts are selective and focused primarily on “scaring” the tower companies, or they represent actual and significant savings on operating expenditures going forward, we don’t know."

American Tower’s scale, lease renewal schedule, and geographic diversification help, but this is still a risk to keep in mind.

Similarly, tower companies can be adversely affected when carriers merge together, which allows the combined companies to rationalize overlapping parts of their networks, share equipment, and decide not to renew certain leases.

The Sprint/T-Mobile merger, which is still waiting for regulatory approval, would leave American Tower dependent on the much larger T-Mobile for 18% of its revenue. That might lead to less generous lease terms in the future when contracts are up for renegotiation.

However, it's important to remember that such a merger, if it happens, won't necessarily hit the REIT's revenues. Citing the Sprint-Nextel, AT&T-Cingular, and Verizon-Alltel mergers, American Tower claims it has enjoyed 20-25% more business from each combined entity 12 to 18 months after the deal compared the amount the company was receiving from the individual entities.

How can this be? Essentially, the combined company now has to service an even broader base of customers, even on overlapping towers. Combining businesses also tend to result in more capital that can be reinvested in the network for the long-term, which is what T-Mobile has vowed to do as it plans to ramp up its 5G network, much of which will require traditional towers due to the spectrum the company plans to use.

International wireless markets are much more fragmented, so this could be a bigger consolidation risk in those regions. This has been especially true in India, where significant M&A in recent years has caused a spike in churn rate among tenants that has hurt short-term results. Fortunately, analysts expect churn rates to drop in the coming years.

The final risk to consider is management’s capital allocation decisions. American Tower has made a number of major acquisitions in recent years, deepening its presence in a number of international markets, such as India and Nigeria.

It’s extremely important that American Tower can generate strong returns from international markets as they continue maturing and capacity fills up on the company’s tower sites. That's to offset the mature U.S. market where organic growth has slowed to about 6%.

Fortunately, thus far the company has done a good job earning strong returns on its international towers, meaning that American Tower is delivering the kind of foreign profitability that caused management to expand globally in the first place.

Closing Thoughts on American Tower

For investors seeking long-term dividend growth and capital appreciation, American Tower appears to be an interesting candidate to consider. The economics of the tower business are quite favorable, and the earnings potential of American Tower’s existing tower base in developing markets is substantial.

As a result, management believes the company can deliver 20% annual dividend growth in 2019, which would be one of the fastest rates in the entire real estate sector. Beyond this year American Tower is likely to remain one of the fastest growing REITs in the market, making it a potentially attractive choice for investors who are content with the low current yield and have a long enough time horizon to let the growth story play out.