Becton Dickinson (BDX) was founded in 1897 and is one of the world’s largest medical supplies, devices, laboratory equipment, and diagnostic products manufacturers. Some of the firm's key products include syringes, needles, medication dispensing systems, and catheters, but its portfolio is well diversified. Many products help hospitals deliver medicines to patients. Key customers include hospitals, clinics, physicians’ offices, pharmacies, labs, blood banks, and others.

The company organizes its business into two segments:

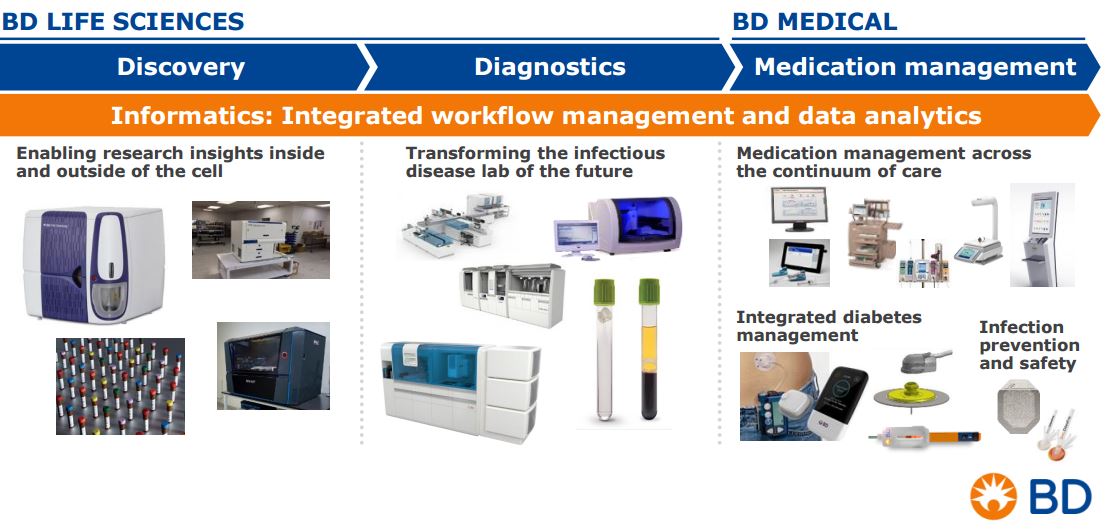

Medical (67% of 2017 sales, 74% of 2017 profits): makes and markets drug delivery systems including syringes, pen needles, IV sets for diabetics, IV catheters, and anesthesia and surgical equipment.

Life Sciences (33% of sales, 26% of profits): specimen collection and diagnostics systems including blood collection and microorganism culturing and diagnosis equipment. Also produces molecular analysis systems for detecting cancer and testing for bacterial drug resistance.

Source: Becton Dickinson Presentation

Following its acquisition of Bard in December 2017, Becton Dickinson now generates 54% of its sales from the U.S., 26% from other developed nations, 14% from emerging markets, and 6% from China.

Business Analysis

With a dominant position in the medical supplies industry, Becton Dickinson enjoys a strong outlook for long-term dividend growth thanks several factors, including a growing and aging world population. In the developed world, such as the U.S. and Europe, aging populations will require greater amounts of drug delivery equipment in the coming years.

Meanwhile, in China and emerging markets, which generate about 20% of company-wide sales, growing wealth and rising standards of living should boost per capita healthcare spending for many years to come.

However, up until recent years, Becton Dickinson was hardly a fast-growing company. That’s because it generally avoided large-scale acquisitions and instead delivered steady but moderate growth.

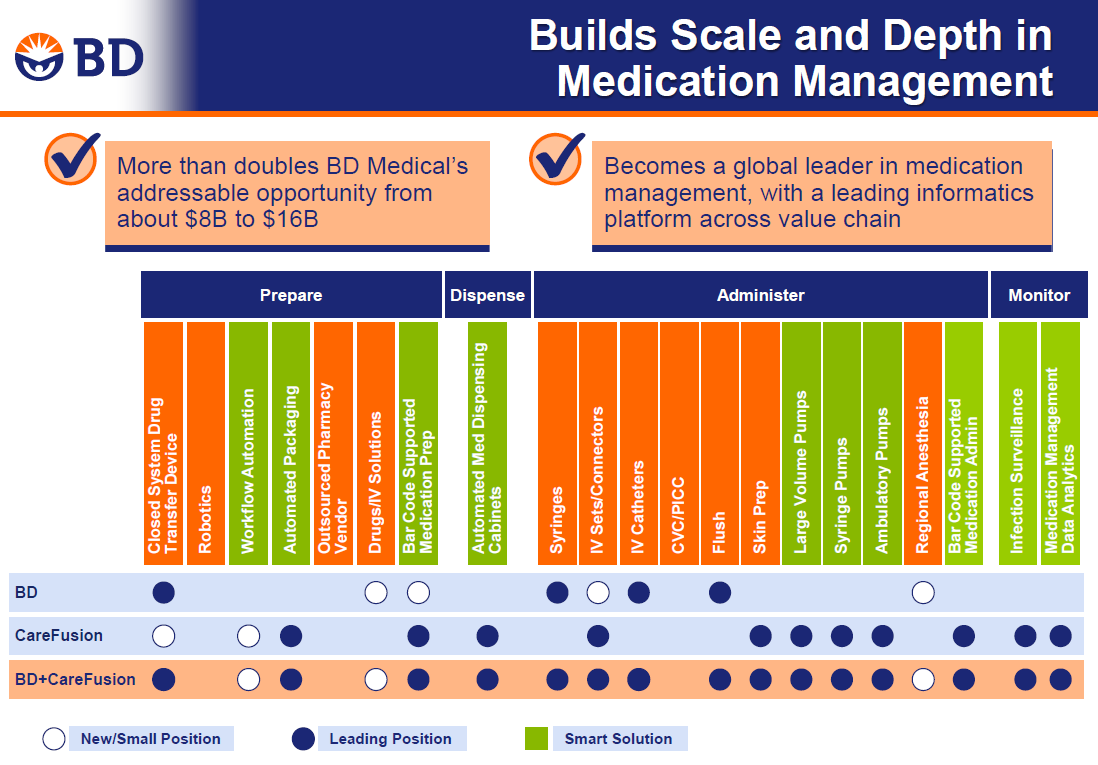

Starting in 2015, Becton Dickinson underwent a significant corporate strategy shift. The company announced its largest acquisition by far (20 times larger than its previous biggest purchase) – the $12.2 billion buyout of CareFusion, a provider of medical devices and diagnostic products to hospitals and physicians.

This purchase doubled the size of the company’s addressable medical products market from $8 billion to $16 billion. Becton Dickinson's extensive distribution channels, which reach all over the world, were a major driver behind the acquisition. CareFusion’s complementary products can be plugged into Becton Dickinson’s existing channels to reach international markets it had never been in before (60% of BDX’s sales were abroad, but 75% of CareFusion’s business was in the U.S.).

Thanks to the deal, Becton Dickinson was now able to offer integrated medication management solutions and smart devices – from drug preparation and pharmacy to dispensing on the hospital floor, administration to the patient, and subsequent monitoring.

Source: BDX Investor Presentation

As hospitals increasingly look to cut costs and improve quality, medical device suppliers will likely continue consolidating. With CareFusion under its belt, Becton Dickinson is able to better help hospitals manage their drug use and cut down on their waste for several reasons.

First, many of their products are complementary and will allow hospitals to save money by only purchasing from one supplier instead of several. For example, CareFusion manufactures equipment that pumps drugs into the catheters that are currently sold by Becton Dickinson and put drugs into patients.

Additionally, CareFusion provided Becton Dickinson with software that helps hospitals track drug usage and the machines they use to store medicines and fill orders. These offerings will become increasingly important as hospitals focus on becoming more efficient.

Other competitors lack the breadth and depth of Becton Dickinson’s portfolio and seem increasingly likely to get squeezed out by the larger players. The company's brand recognition, distribution reach, and economies of scale serve as additional advantages in its markets.

Beyond its comprehensive product portfolio and distribution channels, Becton Dickinson spent over $770 million on R&D in 2017 (over 6% of sales) and has built up an arsenal of patents. The healthcare industry also operates under numerous regulations in every country, further raising barriers to entry.

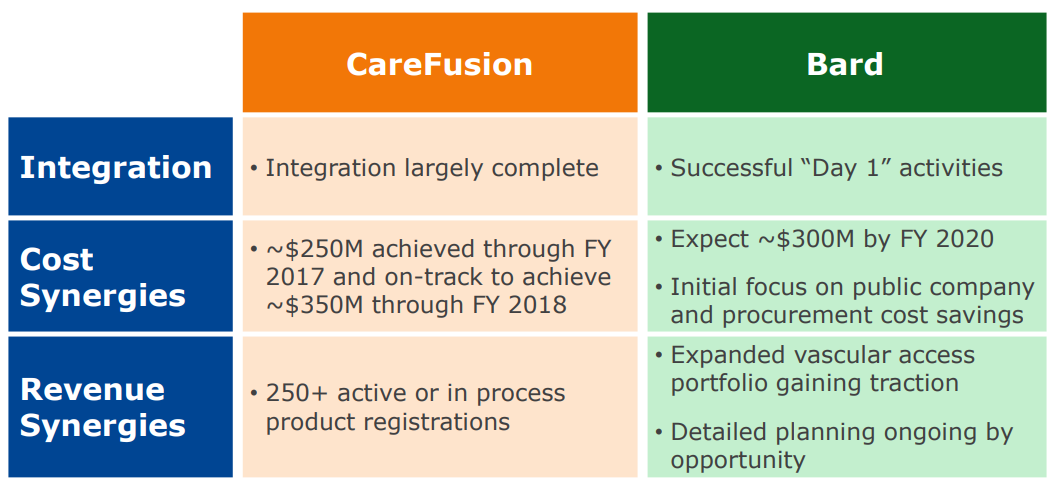

With integration of CareFusion largely complete and revenue and cost synergies on track, Becton Dickinson decided to accelerate its consolidation of the medical supplies industry and further boost its scale with an even larger purchase.

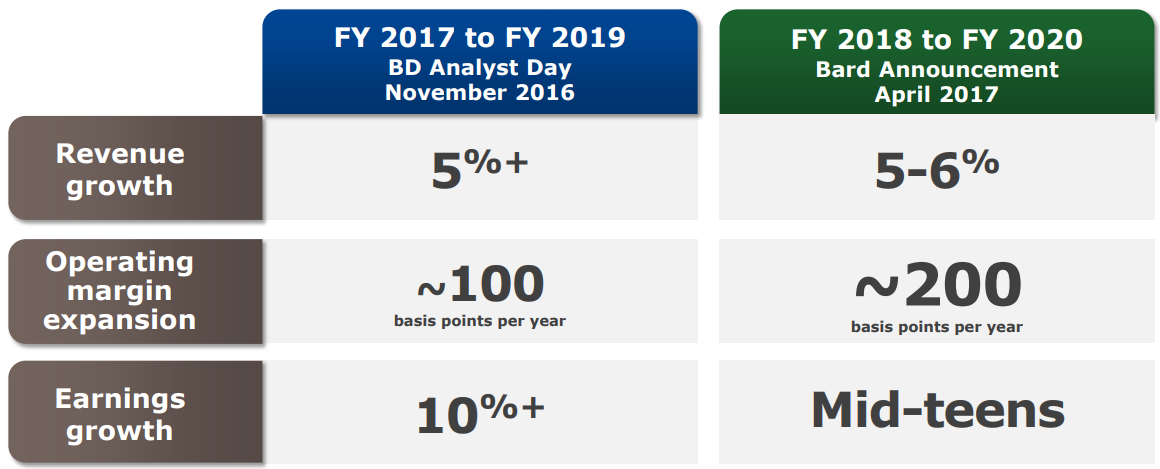

In April 2017, Becton Dickinson announced an agreement to purchase C.R. Bard for $24 billion in cash and stock. The deal closed in December 2017 and is a major game-changer, increasing Becton's workforce from nearly 50,000 to 65,000 employees, adding $20 billion to the company’s addressable market ($70 billion), and giving it a presence in almost every country on earth. The deal will also be immediately accretive to the company’s bottom line and boosts revenue by nearly 30%.

Source: BDX Investor Presentation

Even more important is that the C.R. Bard deal will significantly grow Becton Dickinson’s exposure to key medical supply markets, especially in fast-growing developing markets. Sales in these regions are growing at a double-digit clip (over three times as fast as most developed markets) and now account for a larger proportion of overall revenue mix (around 20%).

The C.R Bard acquisition will open up bigger markets for Becton’s large global supply chains and help the company achieve even stronger long-term top and bottom line growth, which bodes well for future dividend growth.

That’s not just because of the immediate benefit of 27% higher revenue, but also thanks to the $300 million in annual synergistic cost savings that are anticipated.

Management expects the benefits from acquiring Bard, combined with ongoing organic cost savings projects, will boost the company’s overall long-term operating margin by several hundred basis points and result in mid-teens annual earnings growth.

Source: BDX Investor Presentation

Key Risks

While Becton Dickinson has several appealing growth drivers, there are nonetheless several risks to keep in mind.

First, the company's debt levels have been steadily rising in recent years, a trend that has only accelerated now that Becton Dickinson's acquisition of C.R. Bard has closed. A higher debt burden raises the firm's risk profile and makes the company more sensitive to a rising interest rate environment.

Management will need to direct more of the company's cash flow to paying down debt, which will likely result in relatively slow dividend growth over the next couple of years. However, this is the prudent path to take.

As a medical supply company, Becton also faces the ever-present threat of major regulatory changes. This includes the uncertainty regarding the potential repeal of Obamacare, which has resulted in slow growth in hospital consumables as that industry attempts to save as much cash as possible.

Also keep in mind that, though a major player in the industry, Becton still faces stiff competition from major rivals such as Abbott Labs (ABT) and Roche (RHHBY). This, combined with little pricing power in the commoditized surgical equipment divisions, could result in greater margin pressure going forward.

Finally, it's worth repeating that Becton Dickinson has achieved much of its impressive growth in recent years by using a very different business strategy. Specifically, until 2015 the company was known for well-executed but small bolt-on acquisitions.

However, now that management is pursuing large, needle-moving acquisitions, financed largely with cheap debt, there is a lot more execution risk. The company will have to prove that it hasn’t overpaid for CareFusion and C.R Bard and can achieve the synergistic cost savings that were part of the justification for those mega purchases.

The vast majority of large corporate acquisitions have destroyed shareholder value, so Becton Dickinson has its work cut out for it in proving that these were savvy purchases. Management deserves the benefit of the doubt for now, especially with the CareFusion deal having gone so well, but such major capital allocation decisions deserve close scrutiny.

Source: BDX Investor Presentation

All things considered, Becton Dickinson’s diversified portfolio, recession-resistant products, strong business model, long operating history, and disciplined management team lower the company’s overall risk profile.

Closing Thoughts Becton Dickinson

Becton Dickinson is a high quality healthcare company with a number of long-term growth opportunities. Its acquisitions of CareFusion and C.R. Bard significantly expanded its addressable market, and higher healthcare spending in developing countries, as well as the continued aging of the world population, bodes well for future growth.

The company’s dividend appears to remain on very solid ground, even after the C.R. Bard acquisition. While payout growth could remain slow over the short term as management restores Becton Dickinson's balance sheet, the outlook for long-term dividend growth remains strong.

Becton Dickinson has paid an annual dividend every year since 1909 and has raised its payout for more than 40 consecutive years. Those impressive streaks are likely to continue for many years to come.