Procter & Gamble: A Dividend King With Uninterrupted Payouts Since 1890

In business since 1837, Procter & Gamble (PG) has grown into one of the world’s largest manufacturers of consumer goods. The company currently sells 65 product brands in more than 180 countries.

Procter & Gamble's leading brands include Luvs, Pampers, Tampax, Charmin, Downy, Tide, Cascade, Dawn, Febreze, Head & Shoulders, Old Spice, Pantene, Gillette, Braun, Crest, and Oral-B.

Source: Procter & Gamble

Over 70% of earnings are generated by the company's Fabric & Home Care; Baby, Feminine & Family Care; and Beauty segments. Here's a complete breakdown of Procter & Gable's business segments and their contribution to 2019 financial results:

Fabric & Home Care (33% of sales, 29% of earnings): Fabric enhancers, laundry detergents, and cleaning products under brands like Ariel, Downy, Gain, Tide, Cascade, Dawn, Febreeze, Mr. Clean, and Swiffer

Baby, Feminine & Family Care (27% of sales, 23% of earnings): Baby wipes, diapers, incontinence products, feminine care, paper towels, tissues, and toiler papers. Major brands include Luvs, Papers, Always, Tampax, Bounty, Charmin, and Puffs.

Beauty (19% of sales, 22% of earnings): Hair care (Head & Shoulders, Herbal Essence, Pantene, Rejoice) and skin/personal care (Olay, Old Spice, Safeguard, SK-II, Secret)

Health Care (12% of sales, 13% of earnings): Toothbrushes/toothpaste (Crest, Oral-B) and personal health care (Metamucil, Neurobion, Pepto Bismol, Vicks)

Grooming (9% of sales, 12% of earnings): Shaving products and appliances under brands like Braun, Gillette, and Venus.

Procter & Gamble's business is well-diversified geographically. North America accounted for 45% of sales in fiscal 2019, followed by Europe (23%), Asia Pacific (10%), Greater China (9%), Latin America (6%), and India, Middle East and Africa (7%).

With 62 consecutive years of dividend growth, P&G is a dividend king. The company has also paid uninterrupted dividends for since 1890.

Business Analysis The strength of Procter & Gamble's business begins with the firm's deep understanding of and continuous adaptation to evolving consumer trends.

Each year, P&G spends close to $2 billion on research and development, carrying out thousands of studies to gain consumer insights and develop relevant product technologies.

With the right products under its wings, P&G cranks up its advertising budget, which regularly exceeds $7 billion per year (more than 10% of sales). It’s no wonder why consumers are so familiar with most of the company’s brands.

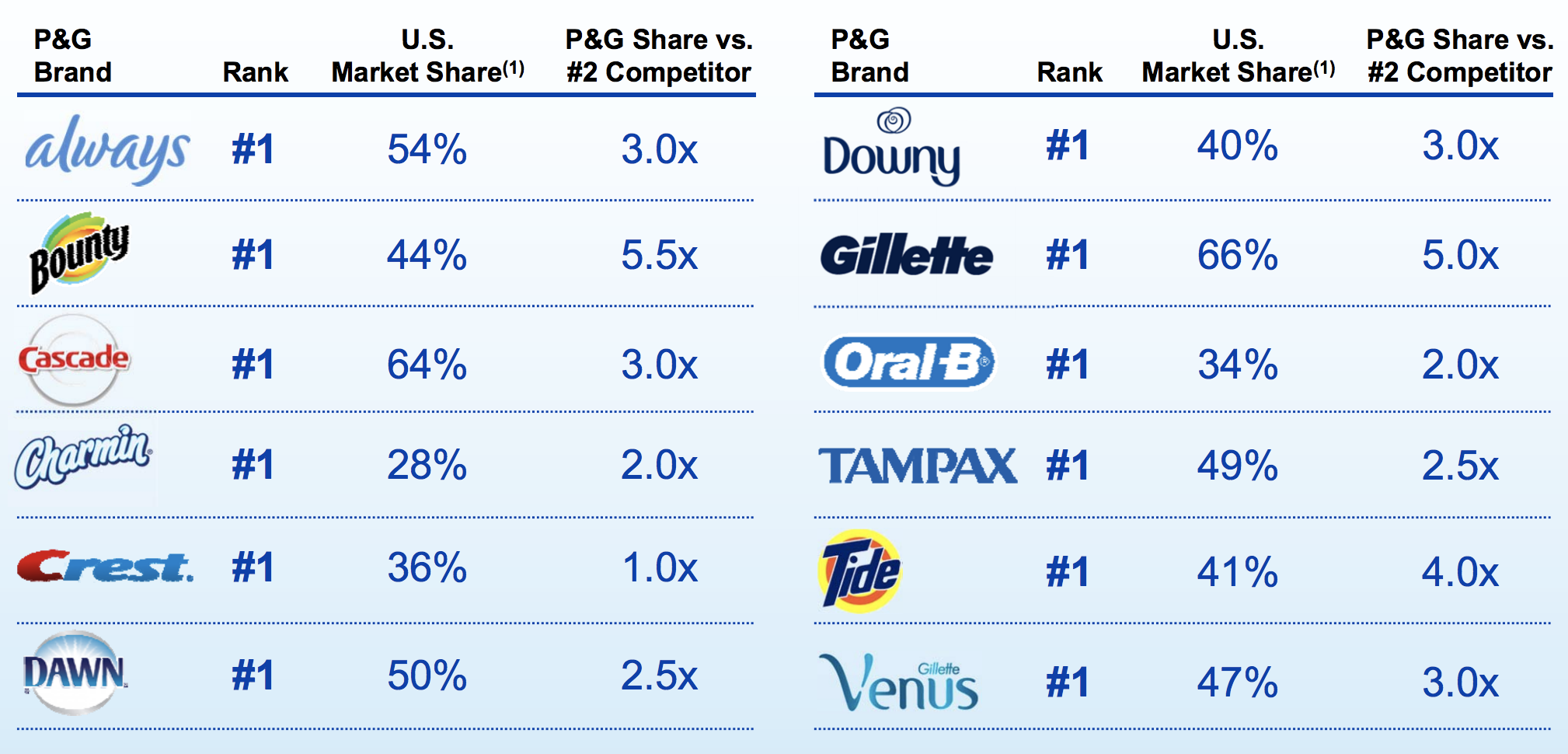

As a result, P&G’s products dominate the shelves at many retailers. Most of the company’s 21 billion-dollar brands boast No. 1 or No. 2 positions in their category or segment, and P&G is No. 1 in seven of its 10 categories.

Source: 2017 Procter & Gamble Investor Presentation

Incredibly, P&G’s products touch approximately 5 billion consumers daily!

The company also boasts the largest amount of e-commerce sales in its industry. In fiscal 2019 online sales grew 25% and now account for 8% of total revenue. Many of P&G's brands have leading positions among Millennials as well.

Procter & Gamble's success in e-commerce is due to the ease with which its products can be shipped and to the firm's strategic shift in advertising. In 2007 just 8% of the company's ad budget went to online marketing, a figure that hit 42% in 2018 and is expected to exceed 50% within a few years.

Besides investing in the right brands and marketing channels, P&G is an enduring business due to the very nature of its industry. Simply put, non-food consumer products have historically been very sticky, resulting in a relatively slow pace of change.

In fact, roughly 85% of households in America are constantly filled with the same 150 items, according to IRI Market Advantage.

At the same time, new product launches tend to have a high rate of failure, which makes it difficult for smaller rivals with fewer financial resources to break into P&G’s market share (though P&G must still contend with private label and giant rivals' brands).

Operating on an impressive global scale, P&G is also able to invest heavily in automation at its factories and supply chain efficiencies to lower costs of production. As a result, P&G's operating margin (22% most recently) is among the highest in the industry.

Looking ahead, the consumer staples industry is forecast to expand 3.5% annually to exceed $540 billion by 2022, according to P&G. The industry's growth is expected to benefit from a rising world population as well as an increase in the number of middle-class households, boosting demand for consumer staples products.

Management is targeting long-term sales growth in the low-to-mid single digits and modest margin expansion, a goal P&G met in 2019 with 5% organic sales growth.

Combined with steady share buybacks, management's financial goals are expected to drive mid-to-high single digit EPS growth. As a result, P&G's dividend has potential to grow at a mid-single-digit annual pace (4-6%), which would be somewhat faster than P&G's dividend has grown in recent years.

Overall, P&G is a giant in the consumer staples sector and appears to have strong staying power. With nearly $10 billion of spending on R&D and advertising each year, extensive global distribution networks, recession-resistant products, and plans to further improve productivity, Procter & Gamble should continue generating reliable cash flow for many years to come.

Key Risks While the consumer goods and healthcare industries are defensive and enjoy a relatively slow pace of change, they are rife with cutthroat competition.

For instance, Proctor & Gamble has to square off against growth-hungry rivals such as Unilever (UL), Kimberly-Clark (KMB), Clorox (CLX), and Colgate-Palmolive (CL), not to mention countless startups launching new products every day.

In fact, in a Q&A session at a trade conference in December 2019, P&G's Chief Brand Officer had this to say about disruption in the consumer staples industry:

...we know we operate in a perpetual state of disruption: thousands of start-ups form every day; TV reach keeps declining; trust in digital media is eroding and over-the-top streaming grows exponentially; e-commerce keeps expanding; omni retailers are creating new media and entertainment ecosystems; and data, analytics and technology dominate our work.

Consumers are also getting smarter with how they shop, using their smartphones to compare prices and check out reviews on new, less expensive brands. Private label products continue closing the gap as well, with Costco's (COST) Kirkland brand one of the most visible examples across numerous categories.

As a result, Procter & Gamble must constantly develop new and improved versions of current hit brands in order to maintain its premium prices and strong market share.

However, cost-cutting has been and is expected be an important means of growing profits at Procter & Gamble. The need to cut costs to boost earnings leaves management at risk of underinvesting in product innovation and marketing.

For example, P&G's employee count has dropped 25% over the past five years, helping to improve the firm's profitability but potentially at the expense of innovation, and long-term earnings power. Only time will tell.

Put another way, P&G might become so fond of cost-cutting to grow short-term earnings that the company could end up shedding not just unnecessary fat but also muscle and bone. This is essentially what has happened to IBM over the past decade (combined with financial engineering gimmicks).

In fact, P&G's revenue declined each year between fiscal 2013 and 2017 as the company failed to make appropriate investments in its brands and lost market share. Management launched a multiyear transformation plan that refocused the firm's resources and has since reinvigorated growth, but continuing to justify the higher prices charged by name brand products could be difficult as consumer shopping habits evolve.

Over the short term, input cost inflation and currency exchange rate volatility (60% of sales come from overseas) can hurt the firm's reported sales and earnings growth. However, these factors shouldn't threaten P&G's long-term outlook.

Closing Thoughts on Procter & Gamble Procter & Gamble has long been a favorite of conservative dividend investors. With a track record of paying a dividend every year since 1890, including 62 consecutive years of payout increases, the company's reputation as a dependable income investment is well-earned.

However, as with all mature businesses, P&G's sheer size makes it difficult to meaningfully grow the company's top and bottom line. All the while, the company is contending with numerous competitors, both old and new, as well as changes in how consumers shop.

That said, management's growth plans appear to be playing out well, though it'll take time to see whether the organic sales and earnings growth seen in recent years persists.

Meanwhile, this blue-chip dividend king should continue delivering safe income and steady payout growth in the years ahead, and in all economic environments.