New Residential Investment Corp (NRZ) is a niche residential mortgage REIT, or mREIT, that was spun off from Fortress Investment Group in 2013. The company specializes in acquiring attractively priced, but higher-risk forms of loans including:

Excess Mortgage Servicing Rights: the overflow cash flows derived from servicing of home mortgages that banks originate.

Servicer Advances: providing reimbursable cash payments to the mortgage originator when the mortgage holder fails to pay on time (provides liquidity on the mortgage loan).

Non-agency Residential Mortgage-Backed Securities: higher risk mortgage-backed securities that represent the future cash flow stream of mortgage payments.

Associated Call Rights: New Residential can call in a loan early when the aggregate loan value is greater than the sum of par on the loans, minus any discount from acquired bonds, plus expenses related to such exercise.

New Residential also buys consumer loan portfolios which are bundled securities that derive their income from repayment of consumer loans such as credit cards.

At the end of 2017, the mREIT's loan portfolio was predominantly focused on mortgage servicing rights (MSRs) and excess MSRs.

Source: New Residential Investor Presentation

The risky nature of the loans means that New Residential is able to obtain very high yields on these investments, usually between 12% and 25%.

Business Analysis

Mortgage REITs should not be confused with equity REITs, which own physical commercial real estate properties and derive the vast majority of cash flow from rent.

In contrast, an mREIT obtains financing (from debt and equity markets) in order to raise capital to buy longer duration and higher-yielding real estate related securities.

The difference between these short and long-term yields is called the spread, and combined with higher amounts of leverage (usually about six to eight times assets) allows the mREIT to generate high enough net yields to pay investors the generous dividends for which this industry is known.

However, because both short-term and long-term yields are market-based and cyclical, mREIT spreads can be highly volatile. Combined with large amounts of leverage (which magnify both profits and losses), this makes mREITs a very high-risk industry with greatly fluctuating dividends over time.

That being said, there are three factors that make New Residential one of the most intriguing (though still high risk) mREITs in the space.

The first is the firm's niche focus, which leads to exceptionally profitable investments. New Residential Investment is focused on the massive $25 trillion U.S. residential property market as well as the $2.5 trillion consumer loan industry.

But unlike many of its residential mREIT peers, management doesn't make most of its money simply buying asset-backed securities, which are bundled mortgages that theoretically generate stable income streams as mortgage payments get made.

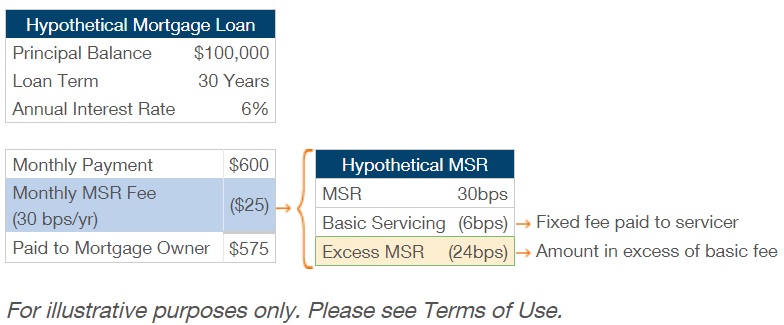

New Residential focuses mostly on mortgage service rights, which are when a bank outsources the servicing of the mortgage payments (collecting them, going after delinquent homeowners, handling foreclosure procedures) to third parties.

What makes New Residential's business model so profitable is that it buys mostly excess mortgage service rights. This means that it outsources its back office costs to a subcontractor to actually collect payments and perform the other duties of a mortgage servicer. It then collects the effectively costless excess cash flow from the MSR fees (the majority of the fee) that mortgage originators pay.

Source: New Residential Investment Corp

If this sounds confusing, complex, and a bit risky, it's because it is. Most mortgages are originated by banks, who own more than 70% of mortgage service rights. However, due to stricter banking regulations, when a bank wants to reduce its risk it can sell its riskier MSRs to get them off its books.

New Residential has proven to be one of the best in the industry at acquiring excess MSRs for incredibly cheap prices (due to their high risk), usually for between 0.3 and 1 penny on the dollar of uncollected principle balance. However, that doesn't necessarily mean that New Residential business model is bad.

The key with all investments is to correctly price and manage risk. In this case, the risk that the MSRs and excess MSRs New Residential buys will either default (home owner can't make payments) or payoff the loan early (refinances the mortgage and pays it off early).

New Residential's track record so far has been very impressive in terms of balancing its risks between finding high-yielding opportunities while minimizing its risks.

Source: New Residential Investor Presentation

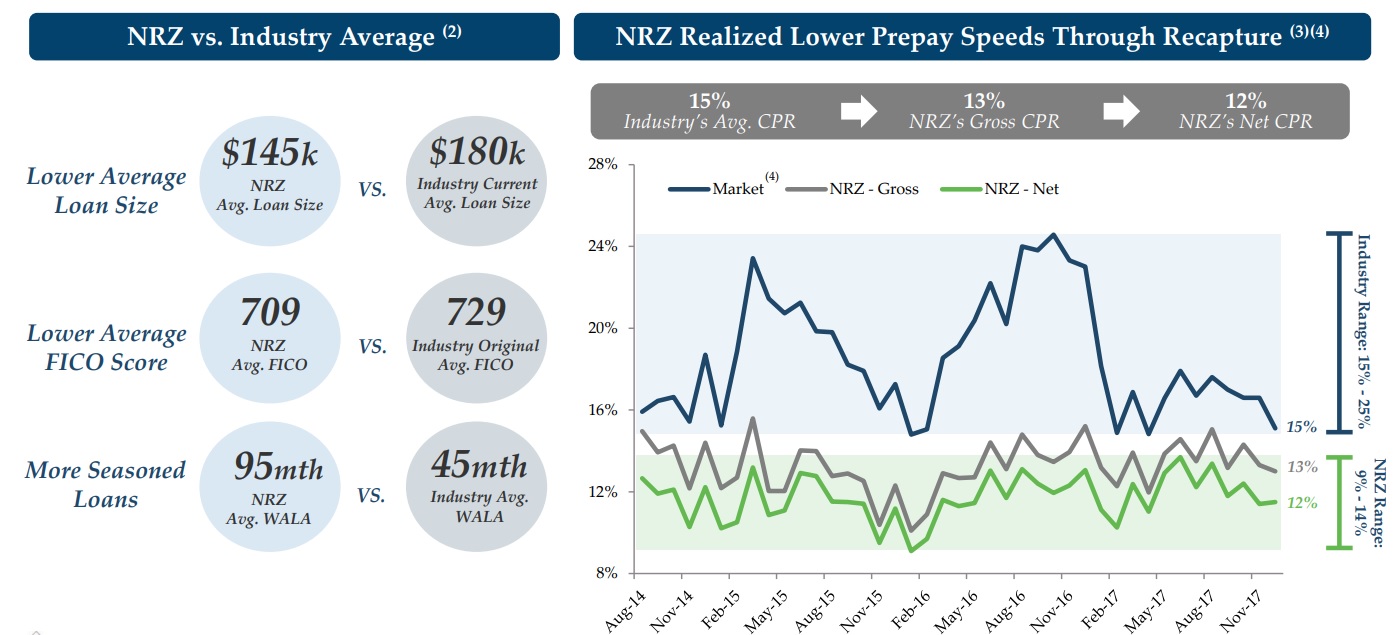

For example, the average New Residential MSR deal is for a loan with a FICO score of 709, which is slightly below the industry average. However, 709 is actually slightly higher than the U.S. consumer average (700) and has been gradually rising over time. This means that while riskier, New Residential doesn't appear to be reaching for yield by purchasing very dangerous loans that are likely to default soon.

In addition, management's track record of being highly selective with its loan purchases has led to its conditional prepayment rate, or CPR, being much lower than its industry average. CPR is bad because if a mortgage that NRZ owns the service rights to gets refinanced and paid off early, then the income stops. This means that the service right or excess service right that NRZ holds becomes worthless.

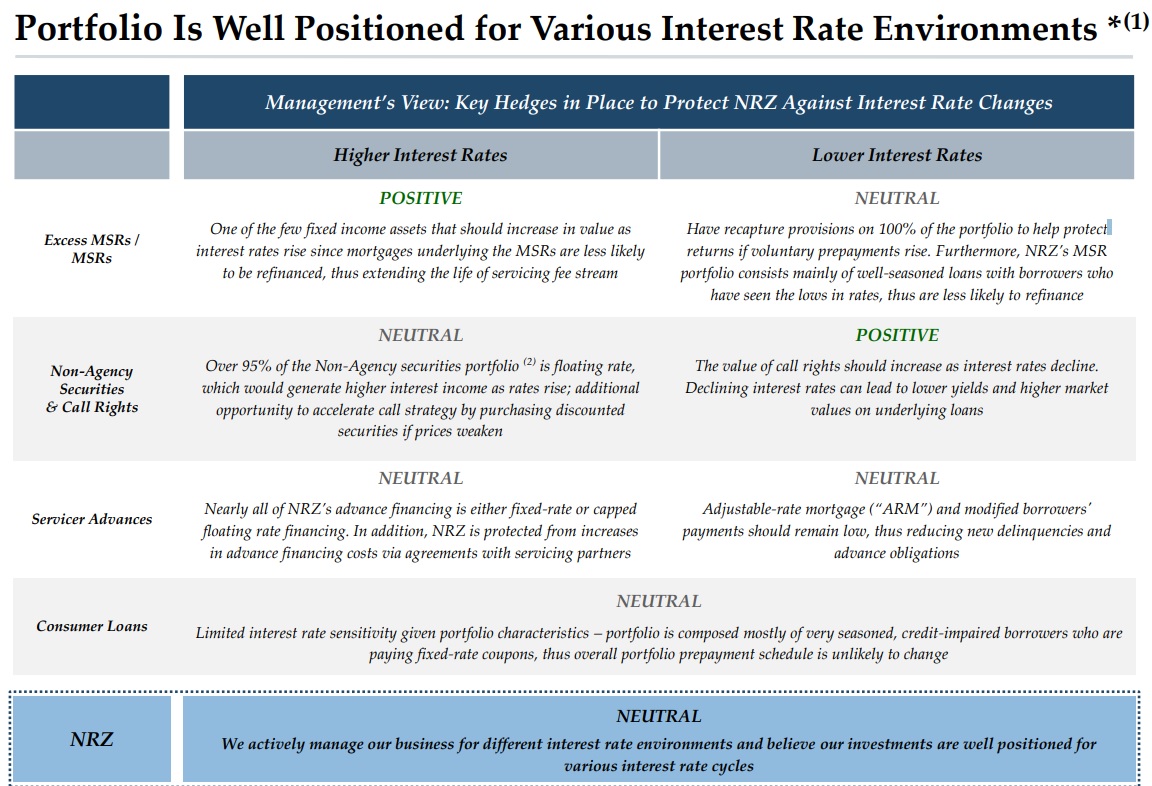

The second major differentiator for New Residential is its industry-leading ability to manage its interest rate sensitivity and lock in low borrowing costs (stabilizing profitability).

The recent rising rate environment has been very challenging to most residential mREITs. That's because short-term rates have been rising much faster than long-term rates, compressing spreads and profitability. Throughout this challenging industry backdrop, New Residential has actually been thriving.

Source: New Residential Investor Presentation

That's because management is very good at managing the company's rate sensitivity, which is why New Residential's earnings are among the least rate sensitive in its industry. When rates rise, usually during a strong economy, mortgage default rates decline. This increases the value of both mortgage loans and their servicing rights.

In addition, higher rates mean fewer homeowners can refinance, so CPR declines, reducing risk and driving up the value of its loans further. As a result, management can also profitably sell an MSR in order to free up capital to invest in a more profitable opportunity if it arises. Combined with a greater use of fixed-rate debt, the mREIT's profitability can become more stable in this type of environment.

The final reason to like New Residential Investment Corp is that, in addition to its strong ability to manage loan risk while maintaining some of the industry's most stable (and high) margins, management has shown an impressive ability to grow the company's assets very quickly.

Source: New Residential Investment Corp

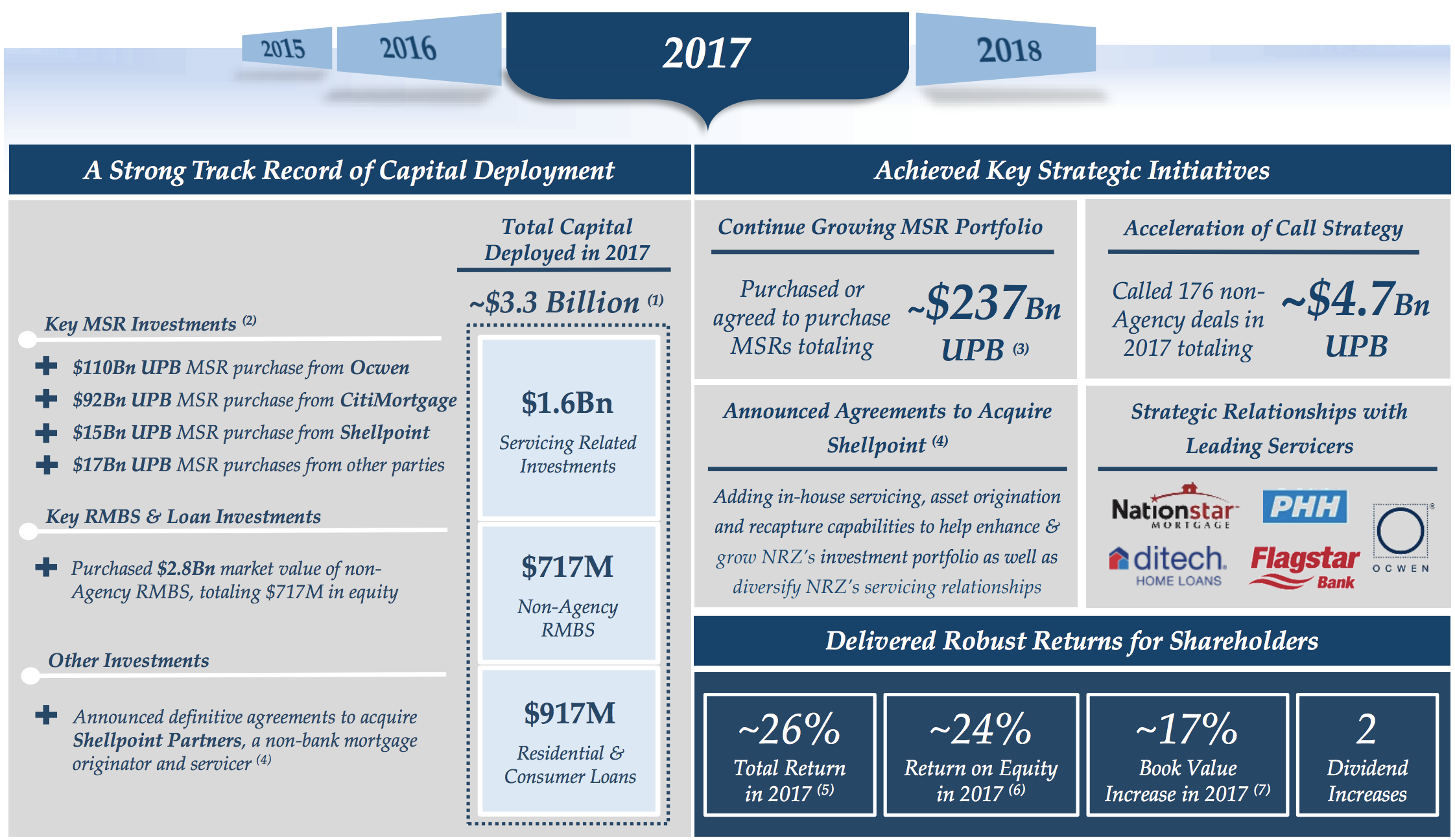

For example, in 2017 New Residential invested $3.3 billion into new high-yielding assets, which drove 32% growth in Core EPS (what pays the dividend). Some of that impressive growth was due to a $440 million deal with one of its excess MSR subservicers, Ocwen Financial (OCN).

Ocwen has been in financial trouble recently, so New Residential bailed it out via a large equity stake. In return, it gets the right to buy much of its MSRs from Ocwen at 0.3 cents on the dollar and drastically lowers its subservicing fees.

Even if you back out this one-time benefit, New Residential's Core EPS ended up rising 9% in 2017, which is very impressive for an mREIT, especially in this challenging rate environment.

Equally important, New Residential saw its book value per share (objective value of its assets) rise about 10% last year (excluding the Ocwen deal), compared to 7% in both 2015 and 2016.

Since its IPO in 2013, New Residential has grown its book value per share by 55%, largely thanks to the appreciating values of its loan book. However, while that might be somewhat due to luck (and perhaps unrepeatable going forward), consider that major rivals Annaly Capital (NLY) and American Capital Agency (AGNC) have seen their book value per share decline by 13% and 23%, respectively, during that same time period.

Book value per share is a very important metric because mREITs are constantly turning over their portfolios and selling new shares to raise growth capital. This is because, like equity REITs, the IRS requires mREITs to payout 90% of taxable net income as dividends, leaving little internally-generated cash flow left for growth.

The constant influx of new equity capital means that many mREITs have a hard time growing profitably, since existing shareholders are being continuously diluted. In other words, book value per share, EPS, and the dividend can actually shrink over time even if an mREIT's assets are increasing.

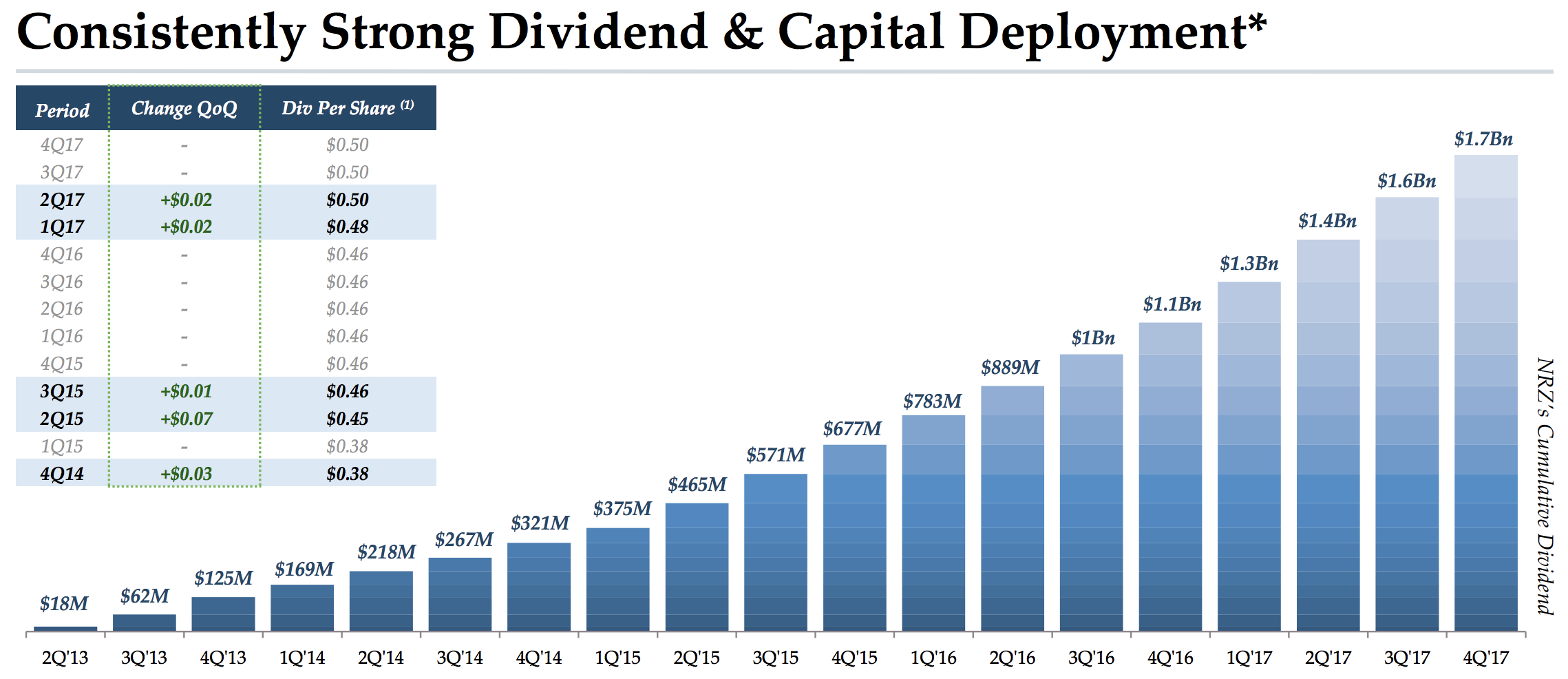

However, New Residential's fast ability to not only lock in profitable loans, but also grow assets at the fastest rate in the industry (apparently without sacrificing disciplined risk management and quality thus far), has allowed it to be one of the only mREITs to consistently raise its dividend since 2013. That's in contrast to most of its peers who have frozen or even reduced their payouts in recent years.

Source: New Residential Investment Corp

In fact, since its IPO New Residential has raised its payout every year, and with an adjusted (to exclude the one-time Ocwen gain) core EPS payout ratio of 85%, which is reasonable for an mREIT, it's likely that investors will continue to see rising dividends over the short term.

New Residential's ability to grow quickly, including its dividend increases, has meant that its shares generally trade at a premium to book value. As a result, management can afford to sell new shares to keep EPS and book value per share growing.

And New Residential shows no signs of slowing down its deal making anytime soon. In fact, in late 2017 it announced it was buying Shellpoint Partners for $190 million in cash. Shellpoint is a mortgage originator and servicer. By acquiring Shellpoint, New Residential is gaining a company that:

Has a $50 billion MSR business

Owns $15 billion in MSRs

Originated $6.6 billion in mortgages annually

In total, New Residential believes this acquisition will allow it to eventually grow its MSR and Call Rights businesses by 23% and 11%, respectively.

Overall, New Residential Investment Corp is a highly specialized mREIT, with an impressive management team that appears to be the best in the business at managing its risks, while generating strong and profitable growth.

As far as high-yield mREITs go, New Residential is arguably one of the best choices for highly risk tolerant investors. That being said, before investors consider buying shares, there are numerous risks to understand and get comfortable with.

Key Risks

This can't be stressed enough - all mREITs are high risk dividend stocks. Even the oldest and most successful mREITs, such as Annaly Capital, which has generated market-beating total returns (11.6% annually since 1997 vs S&P 500's 7.3%), have had wild dividend swings and gut-wrenching share price volatility.

Simply put, the residential mREIT business model is inherently unsuitable for maintaining safe and steadily rising dividends in all economic and interest rate environments.

New Residential could prove an exception to this, owing to the specialized high-margin niche in which it operates. If the mREIT adopts a supplemental dividend model, then perhaps its current, regular dividend could survive the earnings declines that are likely to come in the next recession.

However, that is far from guaranteed, especially since we have no idea when the next downturn might happen. Economic growth is at its strongest levels in years, and appears to be accelerating. However, the current economic expansion is approaching 10 years, which would make it the longest in U.S. history.

New Residential’s management team, though apparently skilled at risk management, borrowing cost control, and putting capital to work quickly, might not be able to overcome the inherent earnings instability of this industry.

Also keep in mind that New Residential is an externally managed mREIT (most stocks in this industry are). As a result, the company is effectively a hedge fund, where management is paid 1.25% of assets and 25% of profits. This means that management is paying itself first, with shareholders getting what's left over.

So far this rich compensation model appears well earned, however it's too early to tell how much of New Residential's success has been mostly due to luck rather than management's investing and risk management acumen. In other words, we can't know if New Residential's previous success is repeatable given its short track record.

That's because much of the mREIT's most profitable loans originated in the financial crisis. With many loan-backed securities looking like they might default, management was able to purchase many of them at fire-sale prices. As the economy improved, default rates steadily declined, resulting in excellent returns on these investments.

However, New Residential's average loan is only for two to five years in duration, meaning that it is constantly having to replace maturing loans with new ones. As the economy improved, the riskiness of loans declined and so does the potential yields on new investments.

For example, the Prosper consumer loan portfolio New Residential began buying in 2016 has thus far generated 16% returns on investment. That's within the 15% to 20% range that management targets but shows that the glory days of super profitable loans are likely behind it, at least until the next recession.

In effect, New Residential needs another recession to reset the mortgage and consumer credit playing field. Another downturn will mean rising default risk that will make bargain hunting possible once again. However, such a downturn could put the existing loan portfolio at risk, including the current dividend.

In other words, until proven otherwise, investors need to assume that New Residential is merely "the nicest house in an unsafe neighborhood." The company's long-term dividend safety remains unproven, and so only highly risk tolerant investors should consider owning a business like this, and only then as a small part of a well-diversified portfolio.

Closing Thoughts on New Residential Investment Corp

Residential mREITs represent one of the highest risk industries for income investors. These businesses are incredibly volatile and complex financial black boxes whose wild earnings swings mean their dividends are almost never sustainable over long periods of time. This makes them poor choices for low risk investors seeking safe and steadily growing income, such as retirees looking to live off dividends.

Thus the majority of conservative dividend investors are better off avoiding this industry. With that said, for investors with a high risk tolerance and a determination to invest in this industry, New Residential Investment Corp could potentially be an intriguing choice.

While the mREIT has yet to face a recession (which will likely hurt earnings due to rising default rates), management's short but impressive track record seems to indicate that the firm may be one of the best run, fastest-growing, and most resilient companies in the industry.

However, that same highly specialized niche business model means that New Residential is even more complex than most of its peers. It's just really hard to get comfortable with this business, especially given its elevated risk of a dividend cut once the economy takes its next downturn.