Southern Company: Uninterrupted Dividends Since 1948

In business for more than 100 years, Southern Company (SO) is a major regulated utility involved in selling electricity and distributing natural gas, primarily across the Southeastern U.S. The firm's eight vertically integrated electric and gas utilities serve customers across Georgia, Alabama, Florida, and Mississippi.

Southern Company’s mix of business and service territories significantly changed after the company's 2016 acquisition of natural gas utility AGL Resources for $12 billion. AGL Resources owns more than 80,000 miles of pipelines and over a dozen storage facilities it uses to transport and distribute natural gas to businesses and households across Illinois, Georgia, Virginia, New Jersey, Florida, Tennessee, and Maryland.

Source: Southern Company Factsheet

After acquiring AGL Resources, Southern Company's customer count roughly doubled to 9 million, and its business mix shifted from 100% electric to a 50/50 mix of electric and gas. The utility services a diversified blend of residential, commercial, industrial, and wholesale customers.

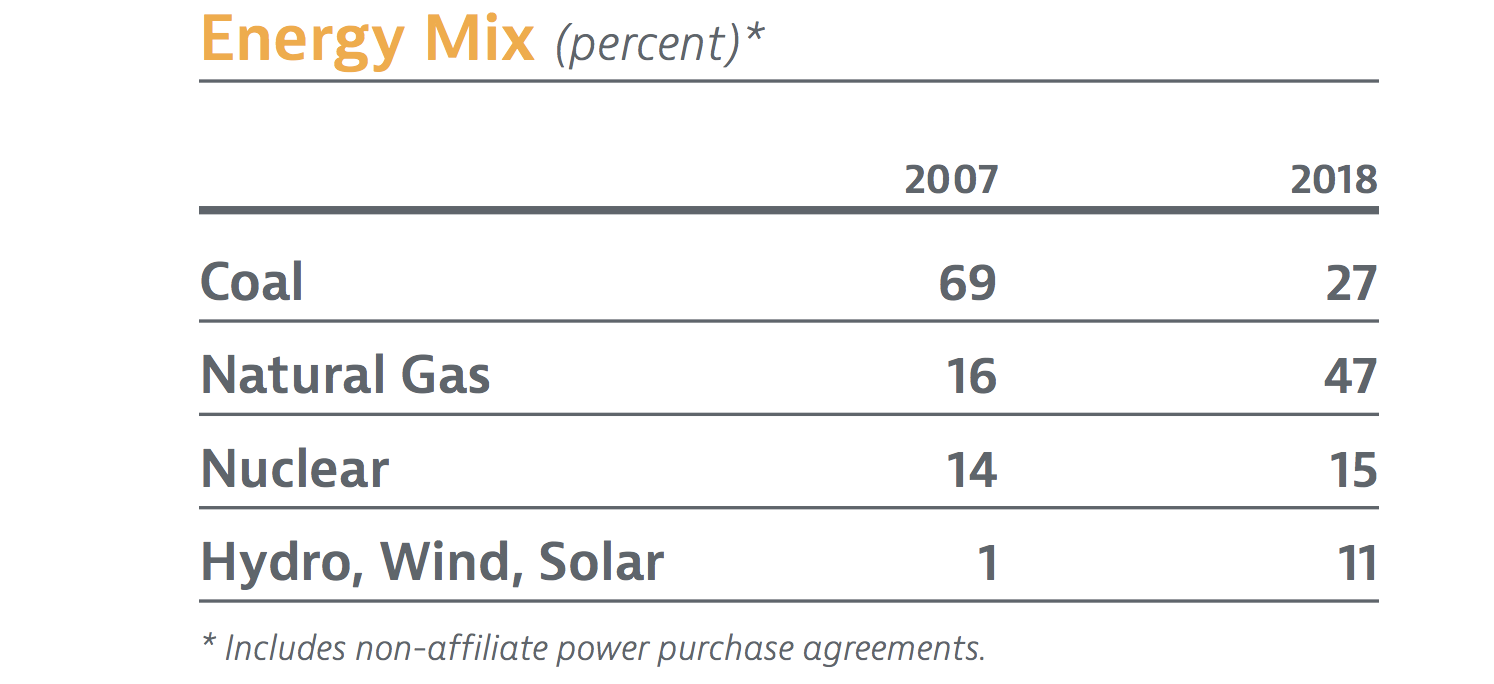

Approximately 95% of the company's earnings are funded by state-regulated utilities and businesses with long-term contract models, providing predictable cash flow. Southern Company has also made great strides in transitioning its energy production mix from 69% coal in 2007 to nearly half from natural gas today, with a significant portion also now coming from renewable sources.

As the industry keeps moving toward cleaner power generation, by 2030 the firm wants to reduce its CO2 emissions by 50% from 2000 levels. Even more ambitious, by 2050 Southern Company plans to generate all of its power from low emission (gas) or no emission (nuclear and renewable) sources.

Source: Southern Company Annual Report

Southern's dividend has grown each year since 2002, and the utility has paid uninterrupted dividends since 1948, indicating a good track record of generating stable and rising income. Though the firm is focused on deleveraging and completing nuclear units Vogtle 3 and 4 (more on this later), management still targets about 3% annual dividend growth going forward.

Business Analysis Utility companies spend billions of dollars to build power plants, transmission lines, and distribution networks to supply customers with power. Given their economies of scale, it usually isn’t practical to have more than one utility supplier in most regions because the base of customers is only so big relative to the investments required to provide them with electricity and gas.

These capital-intensive businesses must also comply with strict regulatory and environmental standards, and state utility commissions further reduce competition since they have varying degrees of power over the companies allowed to construct generating facilities in various service territories.

In other words, most utility companies are essentially government regulated monopolies in the regions they operate in. However, the monopoly status of most regulated utilities has a major downside – the price they can charge for their services is controlled by state commissions.

The government controls the rates that regulated utilities can charge customers to ensure they are fair while still allowing the utility company to earn a reasonable return on their investments to continue providing quality service.

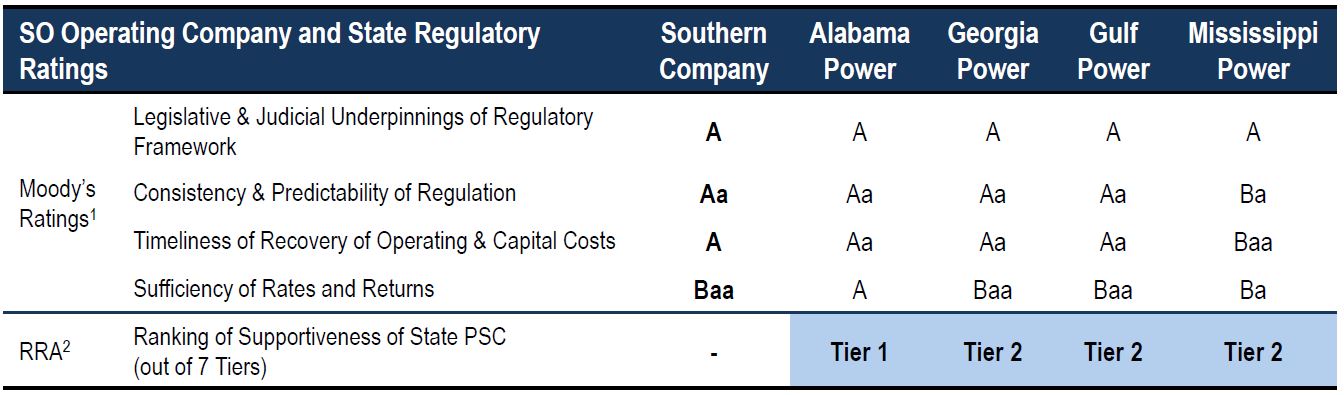

Each state’s regulatory body is different from the next, and some regions have been better to utilities than others. The Southeast region has historically been friendly to businesses, and Southern Company's electric utilities operate in four of the top eight most constructive state regulatory environments in the U.S. according to RRA:

Source: Southern Company Investor Presentation

Southern also maintains strong relationships with regulators in part due to its reputation and the reasonable rates it charges, which are below the national average and perceived as being more customer-friendly. As a result, Southern's traditional electric operating companies have enjoyed an average return on equity over 12% during the last five years, which is slightly above the level that most utilities earn.

The South is also one of the fastest-growing regions in the country, which makes Southern Company a relatively more attractive utility than many others, all else equal. In fact, according to the National Real Estate Investor, "the Southeast region would form the sixth largest country in the world with a growth rate that would exceed any in the top five."

Southern Company has historically enjoyed annual customer growth near 1% in its electric and gas businesses. However, retail electric sales growth is still only projected to be flat to slightly positive going forward. Despite continued population and job growth in the region, increasing energy efficiency continues reducing the amount of electricity that needs to be consumed.

As a result, Southern's earnings were growing by about 3% per year over most of the past decade. In late 2015, management announced plans to acquire AGL Resources for $12 billion. AGL is one of the largest natural gas distribution operators in the U.S., serving 4.6 million customers in seven states and generating over 70% of its earnings from regulated operations.

Most of AGL's rates are set through cost-based regulatory mechanisms, including base rate cases and infrastructure investment programs. The business is expected to continue delivering healthy returns on equity of approximately 10% over the long term, providing another important yet predictable stream of cash flow for Southern Company.

Owning AGL Resources opened up a new array of growth projects for the company to invest in as well. Advancements in natural gas drilling techniques have resulted in historically high and growing supplies of natural gas and relatively low gas prices in the U.S. Not surprisingly, this business is enjoying much faster growth rates than Southern's electric utility operations.

As a result, this merger was expected to boost Southern Company's long-term earnings growth rate by a full percentage point to 4% to 5% annually. Importantly, this deal about doubled the company's customer base shifted about half of its customer mix into natural gas, provided some regulatory diversification (operations expanded into new states), and somewhat reduced the impact from Southern's large construction projects that have been delayed (more on that later).

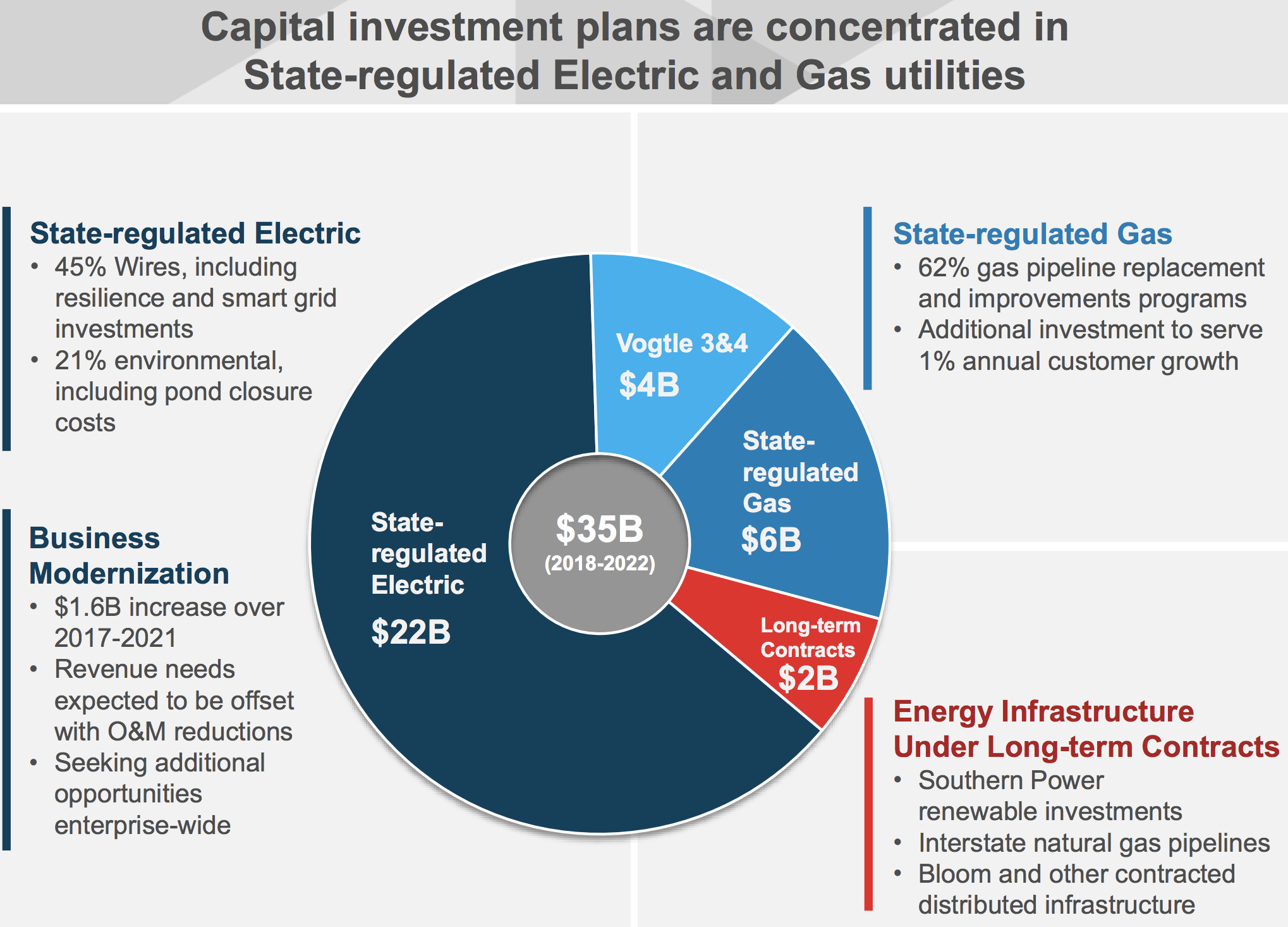

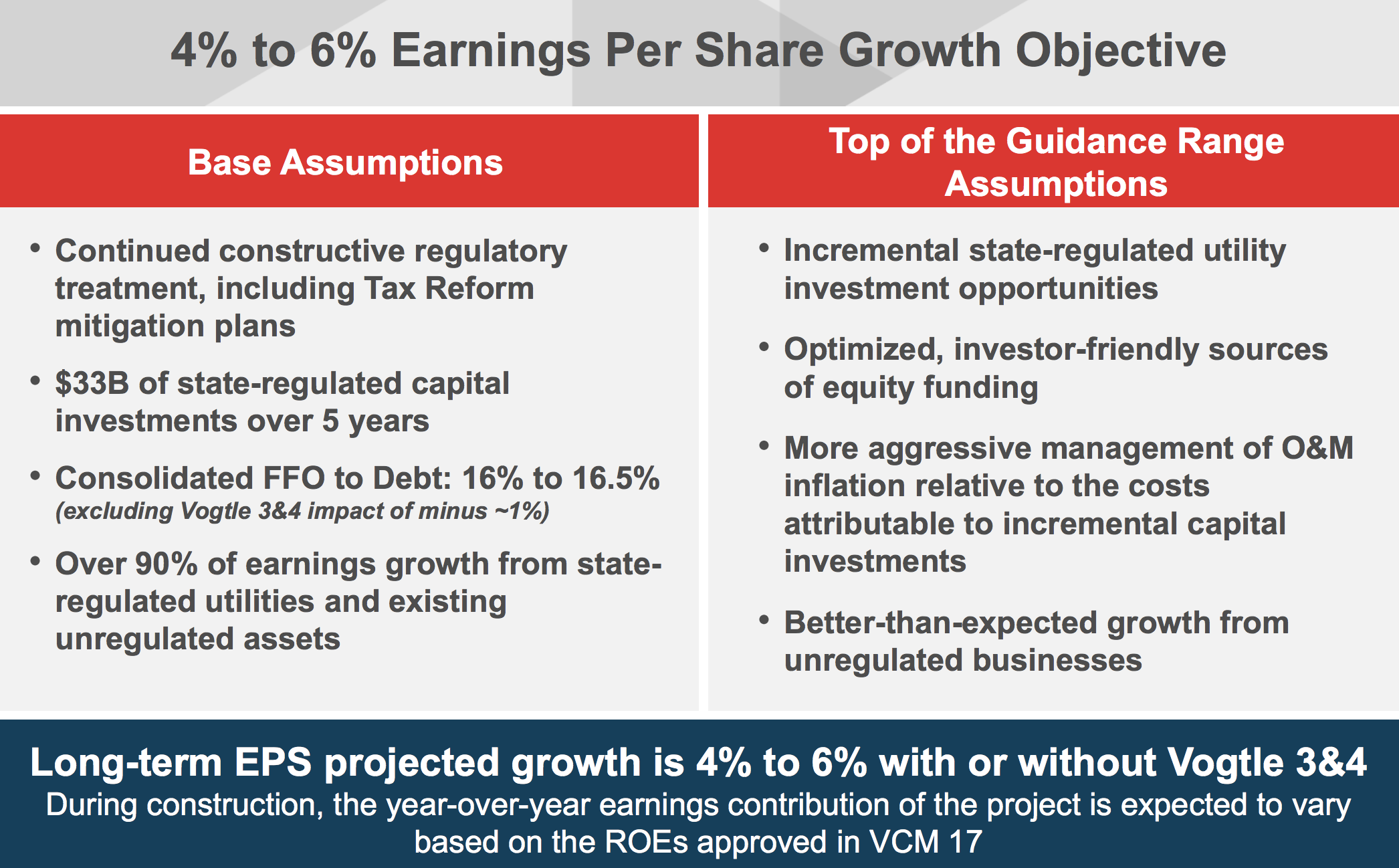

Going forward, Southern Company has plans to invest $35 billion between 2018 and 2022, with the bulk of its money going into state-regulated electric (4% invested capital growth) and gas (9% invested capital growth) utilities. Approximately $8.4 billion of that spending is Georgia Power's share of the Vogtle 3 and 4 nuclear reactors, with about half that money having already been spent.

Source: Southern Company Investor Presentation

As a result, management expects Southern Company to generate 4% to 6% annual earnings per share growth (with or without its troubled Vogtle nuclear projects). Continued deleveraging and regular dividend growth is expected as well, though with dividends growing slower than earnings in order to allow the company to improve its balance sheet.

Source: Southern Company Investor Presentation

Finally, it’s worth mentioning that the company plans to invest up to $1.5 billion annually in growth projects to continue developing its portfolio of long-term contracted assets in wind, solar, natural gas, and biomass.

The company’s mix of resources is expected to become more diversified over the years ahead. Its use of coal has already fallen from 69% of generating capacity in 2007 to just 27% in 2018 (the firm exceeded its goal to be below 30% by 2020). A diverse generation fleet reduces the company’s risk of being overly dependent on any one source of energy, and the strong focus on low emission power sources should continue to lead to favorable relationships with regulators.

Overall, there are several key reasons why Southern Company has been able to reliably reward income investors with uninterrupted dividends since 1948. Most importantly, the business operates in regions with generally favorable customer demographics and has maintained constructive relationships with regulators.

With almost all of its earnings derived from regulated activities and businesses operating under long-term contracts, Southern Company should be able to continue investing in profitable and predictable projects to continue expanding its reach over time. That's especially true thanks to its meaningful presence in natural gas distribution and renewables.

However, even large and diversified regulated utilities can face risks, and Southern Company has experienced its fair share of operational challenges.

Key Risks Despite its impressive track record, Southern Company has fallen on hard times in recent years that have caused significant financial strain and even led some dividend investors to question the safety of its payout.

The company's biggest challenges have stemmed from the multibillion-dollar cost overruns and years of delays it has experienced while working on its coal-gasification plant in Mississippi (Kemper) and two nuclear reactors in Georgia (Vogtle).

When projects run over budget, regulated utilities are largely at the mercy of state regulators to recoup their additional costs from retail customers in the form of higher rates. If regulators are unwilling to play ball, the utility company's shareholders can be on the hook for its cost overruns, potentially jeopardizing its dividend if the situation is severe enough.

Kemper was initially expected to cost less than $3 billion and go into service in 2014, but its price tag eventually ballooned to approximately $7.5 billion. The plant's construction time was also delayed by more than four years, and Southern Company ultimately had to scrap its clean coal plans, running the plant using natural gas instead. As a result, Kemper ended up being the most expensive natural gas plant ever constructed.

Regulators ruled not to allow Southern Company to recover its higher costs from electricity customers and demanded lower rates (customers' rates had jumped 15% in 2015 due to the project). Southern's shareholders had to eat a loss of more than $6 billion (for comparison, Southern's net income has averaged about $2.4 billion in the last few years), but fortunately, the rate recovery issue is now behind the company.

Southern Company faced even bigger challenges from its Plant Vogtle Units 3 and 4, two nuclear reactors it is building that are now about $13 billion over budget and five years behind schedule (the plant was supposed to cost $14 billion in 2008 but is now projected to cost $27.3 billion).

Management claims the project is now 77% finished and on track for completion in November 2022. That's based on the latest report filed with the Georgia Public Service Commission on April 30, 2019, which indicates that under Southern's management (the old contractor went bankrupt) the project's notorious delays appear to be behind it.

The trouble with Vogtle highlights a major risk that shareholders in utilities like Southern can face, specifically executing on time and on budget for mega projects that represent a significant portion of their future growth potential.

For example, Vogtle 3 and 4 are actually a joint venture between Southern's Georgia Power and three other utilities. When the company announced another $2.3 billion in projected costs in August 2018, it triggered a contract clause that required 90% participant approval to even continue construction.

Cancellation of the project would have forced Southern to take a major loss because it wouldn't have been able to pass on construction costs to consumers (also a $5 billion 25-year government loan would have had to be repaid ahead of schedule).

Fortunately, Southern was able to strike a deal, in which its partners agreed to vote to keep the project going, but at the cost of having to swallow an above average share of any future cost overruns. For example, despite owning 46% of Vogtle 3 and 4, Southern will now be responsible for

55.7% of cost overruns between $800 million and $1.6 billion

65.7% of cost overruns between $1.6 billion and $2.1 billion

In the event that costs continue to spiral higher (above $2.1 billion), Southern might have to buy out its partner's stakes in the project and assume their share of the extra expenses.

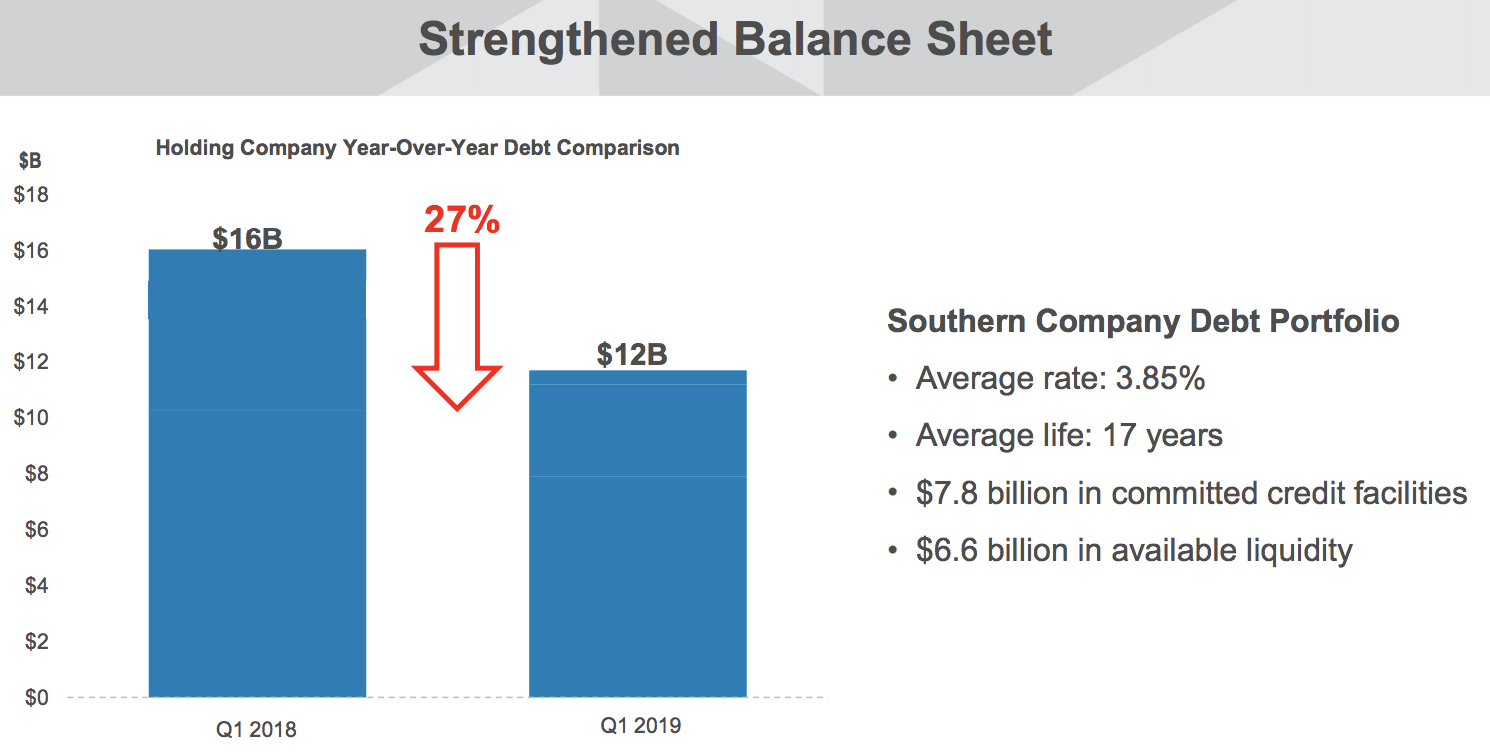

As a result of cost overruns and its $12 billion acquisition of AGL Resources, Southern's debt increased from $29 billion in 2015 to nearly $47 billion in the first quarter of 2019. And that's after striking a deal to sell its Florida gas subsidiary Gulf Power to NextEra Energy for $6.5 billion, which represented over half its asset sales and financing deals struck in 2018.

Fortunately, the company has committed to lowering its debt levels in the future, and after the Vogtle 3 and 4 deal was struck in September 2018, Moody's reaffirmed its Baa2 investment grade credit rating on Southern with a stable outlook.

S&P currently rates the company A-, helping the utility achieve an average borrowing cost of just 3.9%, far below its allowed returns on equity. Southern Company has made good progress over the past year in reducing parent level debt, thus improving its balance sheet and improving its security of its dividend.

Source: Southern Company Earnings Presentation

Despite Southern's gradual progress improving its risk profile, future Vogtle cost overruns could potentially threaten the company's credit ratings and borrowing costs, as Moody's explained in its September 2018 note:

"Southern's rating could be downgraded if Georgia Power is downgraded below Baa1; if either of its other major subsidiaries (Alabama Power or Southern Gas) is downgraded; if there is a material debt financed acquisition further increasing parent company leverage; if there are additional delays or cost increases at the Vogtle nuclear project."

Southern's recent asset sales ($11 billion of such deals in 2018 with another $1 billion pending or completed in 2019) were necessary to maintain its credit ratings, but the utility will also need to balance future funding between debt and equity markets (by selling new shares) to maintain a reasonable leverage ratio.

Over the next four years, management expects to need to finance about $2.5 billion of its growth budget with equity. This is normal for utilities but creates risk in that, should Southern's share price fall to especially low levels (as it was during the peak uncertainty surrounding Vogtle), the company's cost of capital might increase, resulting in lower earnings growth than expected.

Fortunately, the company's aggressive asset sales and pursuit of alternative financing (e.g. private equity deals on its clean power assets) have significantly reduced this risk going forward.

Essentially, management is trying to improve the company's financial health in the most shareholder-friendly way possible while maintaining Southern's ability to meet its long-term earnings growth guidance, finish its nuclear projects, and continue paying and growing its high dividend.

On that front, Southern Company's payout ratio is likely to be in the 80% range for a period of time over the next five years, which is on the higher side for utilities. Once Vogtle goes into service, Southern expects its payout ratio to drop back into the 70% range. Assuming management executes on the company's growth projects and is able to raise equity as expected, the dividend should remain safe.

However, through 2022 (the completion of Voglte) investors need to be prepared for 3% dividend growth to continue. That timeline might be extended should the company once more run into problems with that highly complex project.

Closing Thoughts on Southern Company Southern Company is a favorite holding in retirement portfolios due to its defensive nature and track record of paying uninterrupted dividends for more than 70 consecutive years, including 18 straight years of higher payouts.

The last decade brought with it a number of major project execution missteps, ringing up billions of dollars in cost overruns and casting some doubts over the company's financial health in recent years.

Fortunately, much progress was made in recent years, including the Vogtle nuclear reactor projects which were 77% complete as of April 2019 and appear to be on track to avoid future cost overruns. The company has also significantly reduced its debt thanks to asset sales, the last of which will be completed this year ($12 billion in total sales and financing deals).

However, Southern's relatively high payout ratio is still a reminder that the firm does not have a large margin for error in the years ahead. To continue improving its dividend safety profile, management needs to successfully execute on its growth projects (especially Vogtle) and capital-raising plans. Investors should monitor Vogtle's construction progress over the next couple of years to make sure that Southern Company continues its return to being a low-risk utility stock.