Founded in 1992, Omega Healthcare (OHI) is the largest U.S. skilled nursing facilities REIT, with over 900 properties rented to 67 operators across America and the United Kingdom (U.K.).

Approximately 83% of the company's total rental revenue is derived from skilled nursing facilities, or SNFs, which are Omega Healthcare’s specialty; senior housing accounts for the remaining 17% of rental revenue.

Patients discharged from hospitals are sent to SNFs when they still require care or rehab before they can be sent home. Compared to hospitals, SNFs can provide short-term care on a more affordable basis to save healthcare costs.

About 87% of Omega Healthcare’s total revenue is from rent paid by its tenants, who primarily receive revenues through reimbursement of Medicare (34.8%), Medicaid (52.7%), and private pay (12.5%) for their services.

The remaining 13% of Omega’s revenue comes from loans and mortgages it finances to construct third-party facilities.

Omega has paid uninterrupted dividends for 16 consecutive years and recorded dividend growth each calendar year since 2003. However, due to challenges with some of its tenants, the REIT was forced to freeze its dividend in 2018 so its dividend growth streak is likely to end.

Business Analysis

Omega Healthcare is the largest SNF-focused REIT with more than twice as many properties as its next largest competitor. The business has played the role of consolidator in this large and fragmented market, compounding its gross investment base by more than 20% annually over the last decade.

Omega boosted its property count by nearly 50% in April 2015 with its $3.9 billion acquisition of Aviv, which helped the company gain operating, growth, and cost of capital efficiencies. Importantly, the deal also increased Omega’s diversification by state and operator. The firm's largest tenant, Ciena, accounts for 11.9% of annual rent. No other tenant represents over 10% of revenue, and Omega's top 10 customers make up 58.7% of total rent.

Omega's expansion has been overseen by Taylor Pickett, who has 25 years of industry experience and joined Omega in 2001 during one of the most challenging times in the SNF industry. Specifically, major Medicare reimbursement changes caused a large number of SNF chains to declare bankruptcy and forced Omega to suspend its dividend to survive (see the risk section).

Omega's acquisition strategy is made possible by its main competitive advantages which include management experience, scale, and thus access to more low-cost capital than its peers. In January 2019, these qualities enabled Omega to announce it was buying rival REIT MedEquities Realty Trust (MRT) for $600 million (including debt). The deal is expected to be immediately accretive to funds available for distribution, or FAD, when it closes in the first half of 2019.

In addition to acquiring additional SNF and senior housing facilities, the MedEquities purchase will give Omega its first exposure to acute care hospitals leased under triple-net terms to strong tenants such as Baylor University. Acute care hospitals, while facing their own challenges, have struggled far less than SNF and SNH operators in recent years and will represent a more stable source of revenue and cash flow.

CEO Taylor Pickett explains that this acquisition is a natural continuation of the REIT's long-term diversification strategy:

“This acquisition reinforces our commitment to the skilled nursing and senior housing industry while adding new asset types to our portfolio furthering our strategic objectives.”

However, skilled nursing facilities will remain Omega's key business driver for the foreseeable future. While the skilled nursing industry certainly has its share of risks (more on that later), there are also several attractive elements. Most notably, the industry’s long-term supply and demand fundamentals appear attractive.

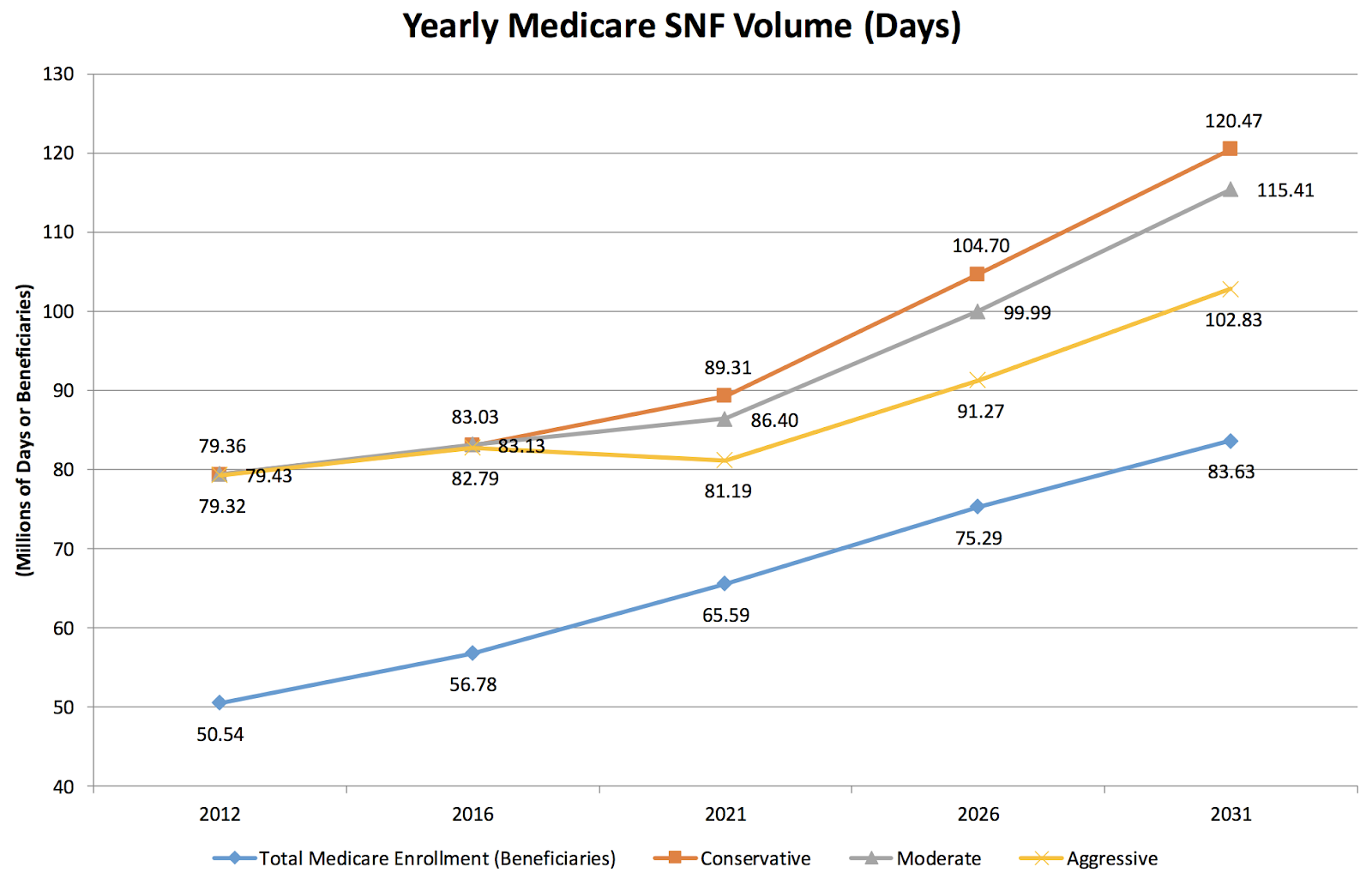

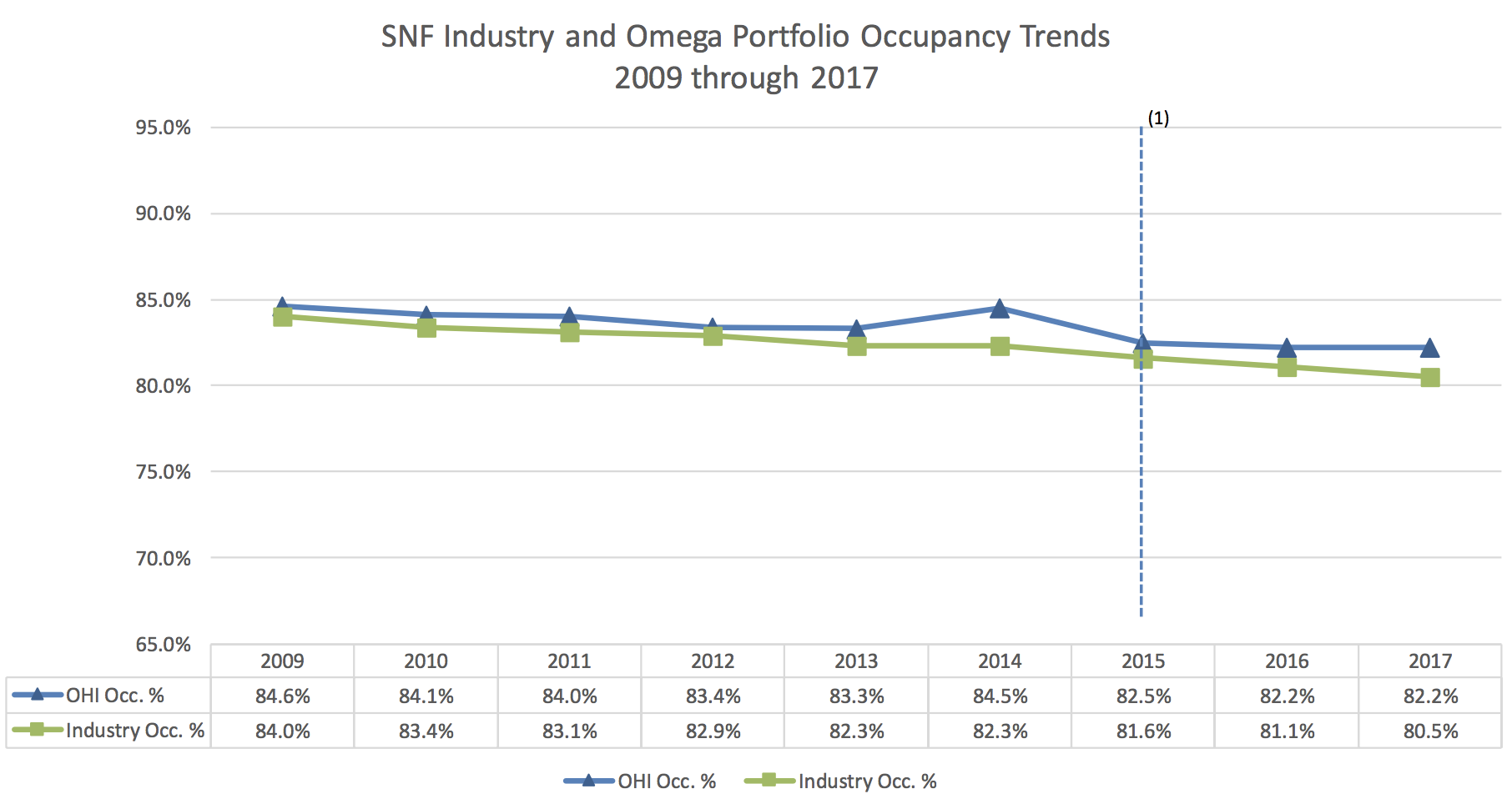

From a demand standpoint, Omega’s occupancy rate has consistently remained in excess of 80% thanks in part to the non-discretionary and recession-resistant nature of its operators’ services. More importantly, despite various changes in Medicare and Medicaid, which have affected rates and shortened lengths of stay, the continued aging of America’s senior population means that overall patient volume and pay per day is expected to increase in the future.

Source: Omega Healthcare Investor Presentation

Furthermore, SNFs seem likely to remain a primary choice for post-acute care because they offer one of the most cost-effective environments for rehab services due to their relatively smaller footprints and lower staff counts. As a result, SNFs have received just under 50% market share of patients sent to post-acute care in recent years.

Add to this the natural demographic wave of an aging U.S. population and Omega is theoretically well situated to experience an improvement in its business in the coming years.

Source: Omega Healthcare Investor Presentation

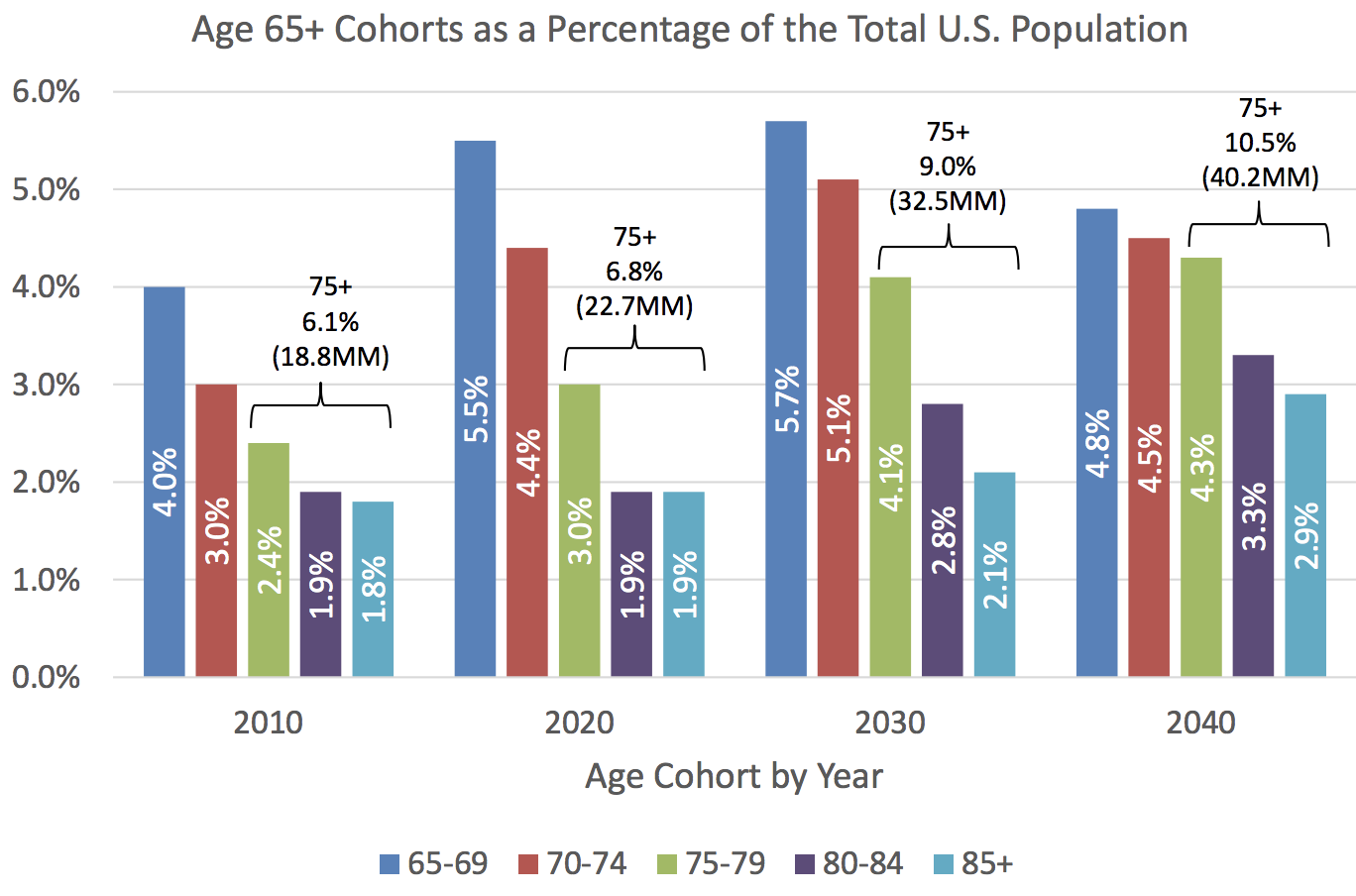

Simply put, the older a person gets the greater their need for skilled nursing facilities becomes. The sweet spot for Omega is Americans over the age of 75, where demand for these facilities begins to significantly increase.

Source: Omega Healthcare Investor Presentation

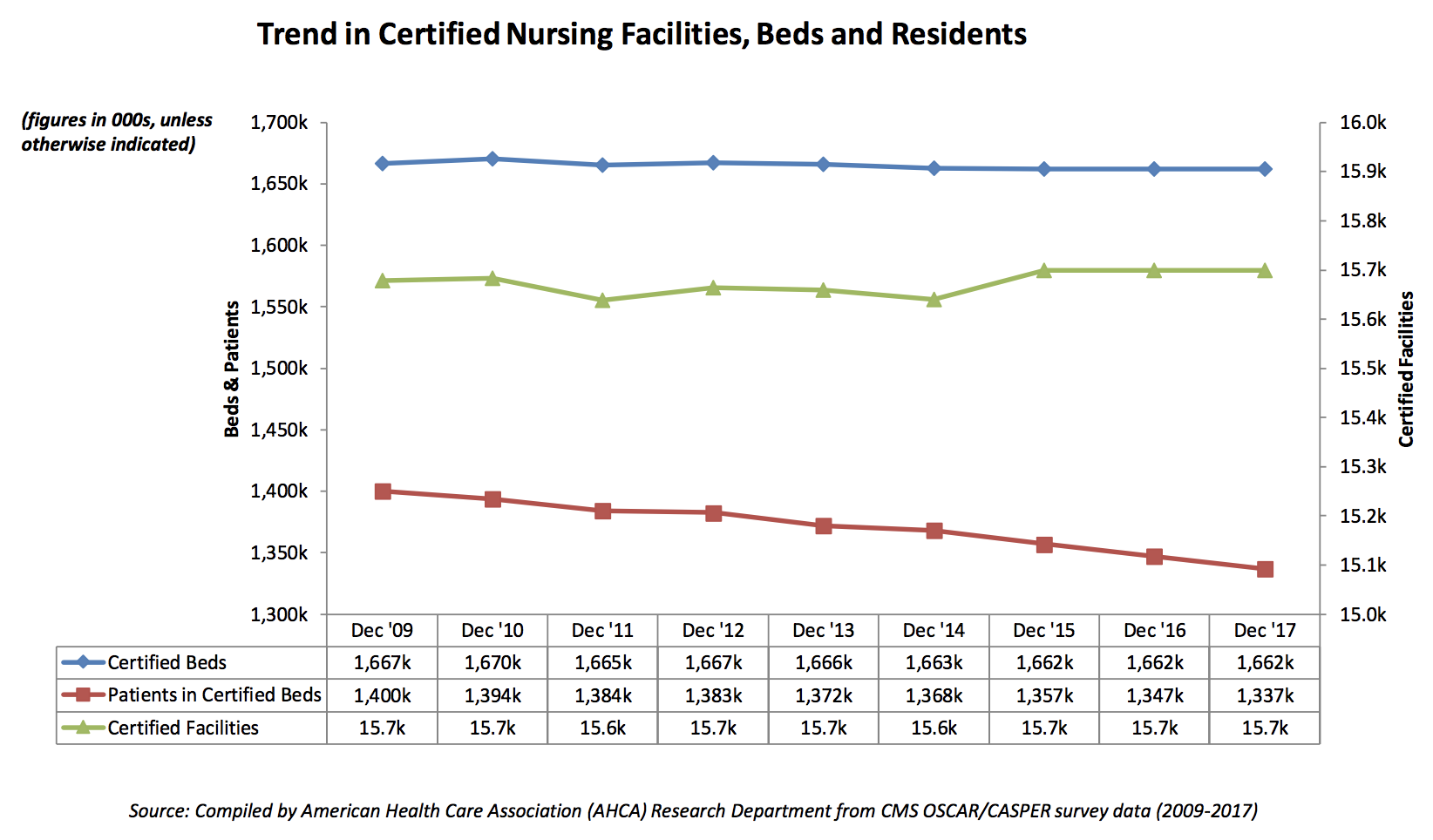

Looking at industry supply, the number of facilities and beds to meet increasing future demand has been limited in part due to Certificate of Need (CON) restrictions, which are aimed at restraining health care facility costs and have helped support industry occupancy rates.

In fact, these certifications, combined with struggles among industry tenants, have resulted in SNF capacity remaining stable over the past decade, even in the face of this large demographic trend looming in the future.

However, it’s also true that there just hasn’t been a big need yet for more supply with the industry’s occupancy rate hovering around 80% and the number of patients in certified beds down slightly since 2009. Many of the expected demographic benefits have yet to show up in the numbers.

Source: Omega Healthcare Investor Presentation

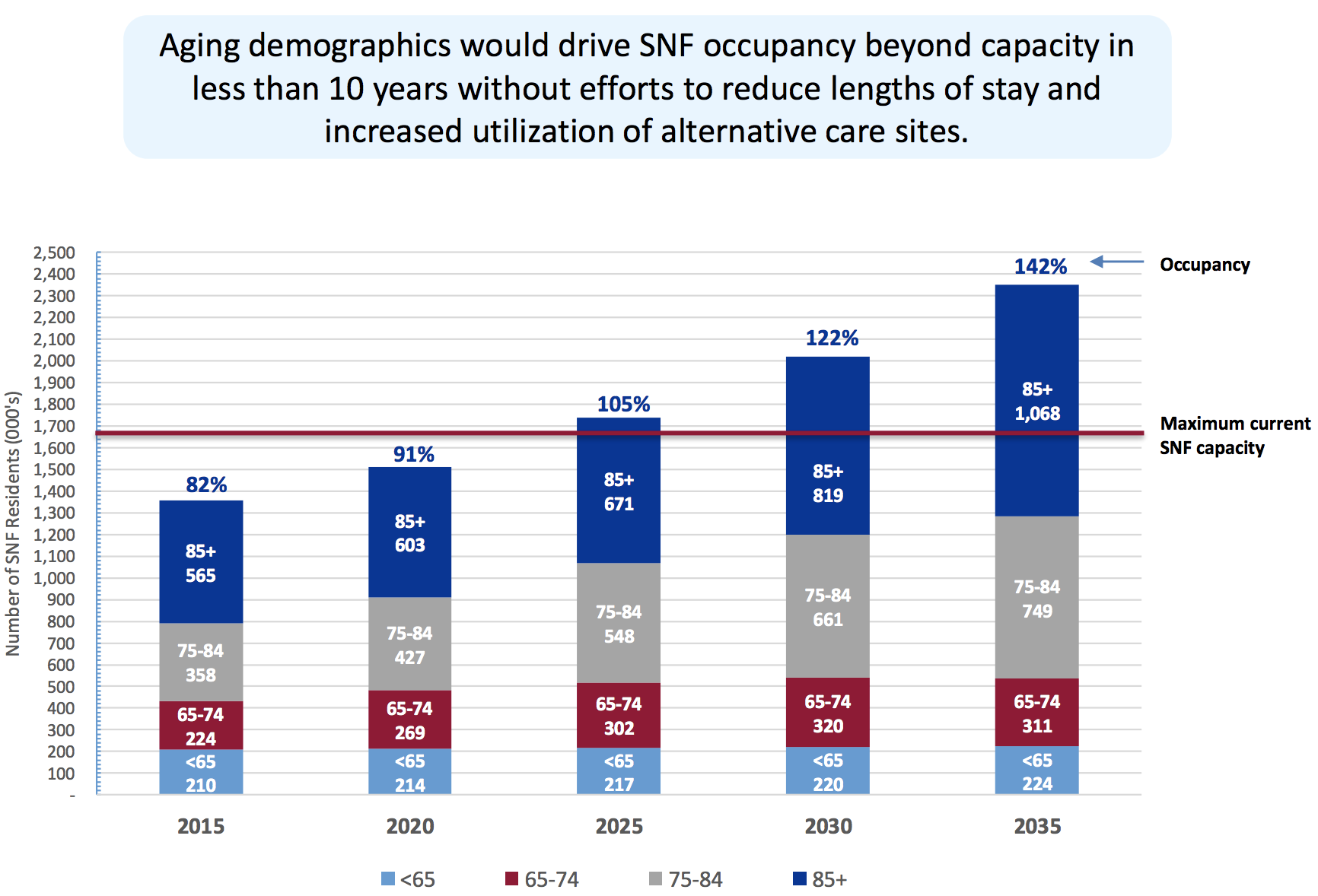

For now, Omega still estimates that SNF occupancy will exceed industry capacity in less than 10 years without efforts to reduce lengths of stay and increase utilization of alternative care sites. As you can see below, the number of SNF residents is expected to increase substantially in the years ahead as the population continues aging.

Source: Omega Healthcare Investor Presentation

But if the demographic trends are so favorable to SNFs, why is Omega facing challenges with some of its major tenants and thus in need of a turnaround effort at all? Several factors are at work.

First, occupancy rates have actually been trending steadily downward. The industry's occupancy rate was near 86% in 2004 but slipped to 84% in 2009 and sits close to 80% today. The major demand growth many industry insiders expected has not yet materialized.

Source: Omega Healthcare Investor Presentation

In addition, Medicare and Medicaid are the primary payers for this industry, and in recent years (starting in 2010) the Center for Medicare & Medicaid Services, or CMS, has enacted new policies designed to both cut costs and improve patient outcomes. The big changes CMS has made have resulted in shorter patient stays and ultimately lower reimbursement rates for SNF operators.

Meanwhile, thanks largely to faster growing wages, operating costs for Omega's tenants have outpaced revenue growth in each of the past five years, on average by 0.2% per year. In 2017, growth in expenses (+2.0%) outpaced revenue growth (+1.3%) by its strongest pace in more than five years.

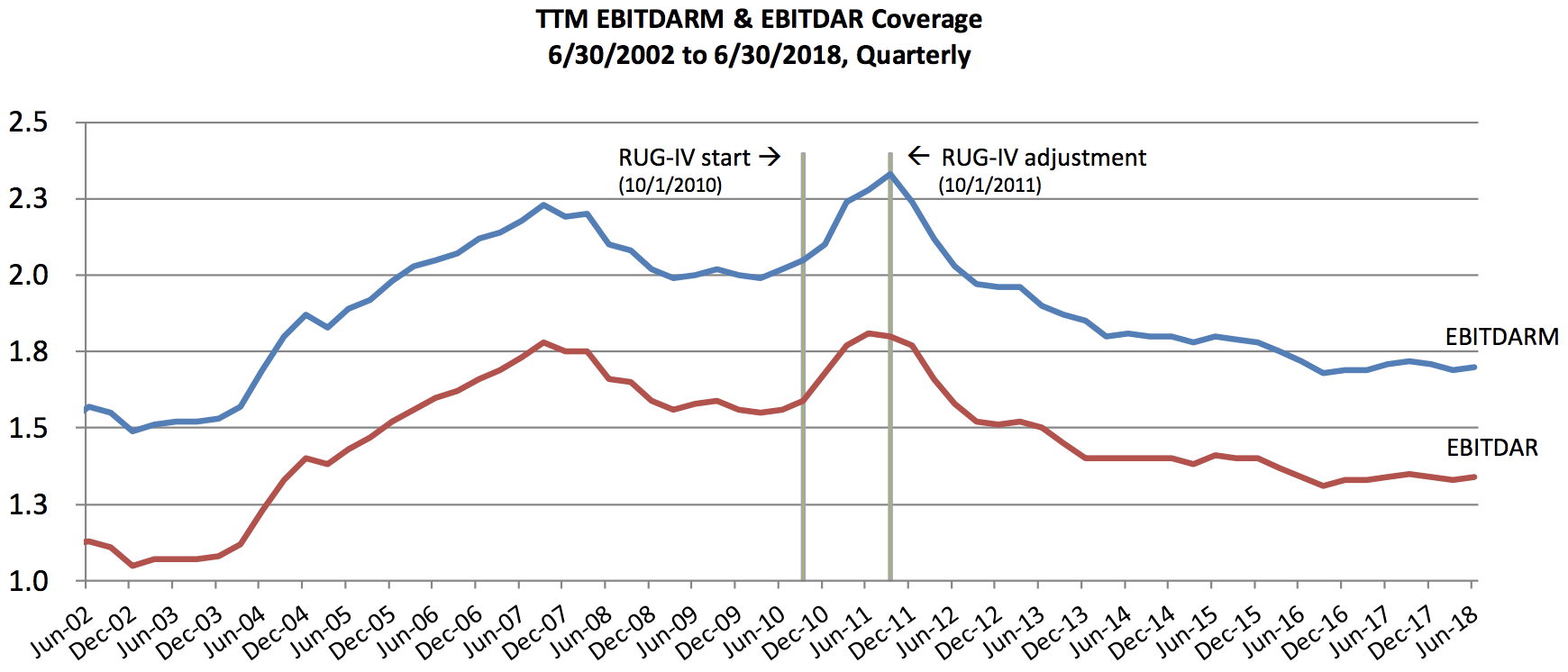

These negative factors have combined to create falling rental coverage ratios as measured by EBITDAR, or earnings before interest, taxes, depreciation, amortization and rent. The EBITDAR ratio shows how well Omega's tenants are able to cover their rent (which rises each year automatically per the firm's leases).

In this industry, a rental coverage ratio of 1.3 or higher is preferred. Omega's portfolio rental coverage peaked at 1.8 in late 2011 which is when CMS began its latest major round of policy changes.

Omega's portfolio rental coverage ratio then fell to a low of 1.3 in late 2016 as the REIT's tenants struggled to adapt to falling occupancy and revenues in the face of rising expenses. The rental coverage ratio has recently been stable in the low 1.3s which is right at the border of safe levels.

Source: Omega Healthcare Investor Presentation

The good news is that America's aging population is still expected to help boost SNF tenant coverage ratios in the coming years, and by a significant amount.

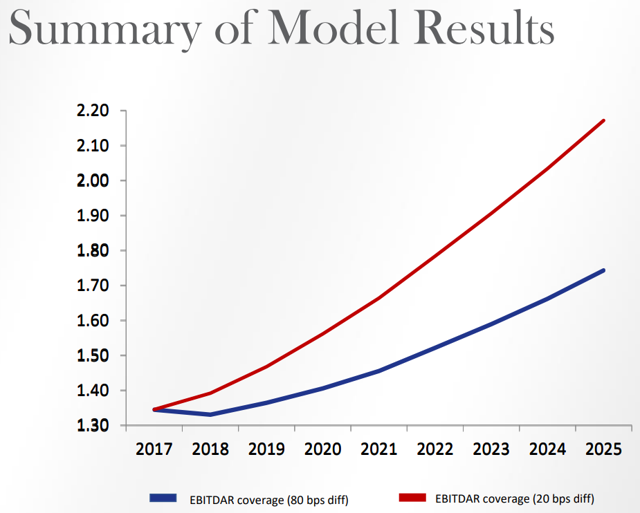

The REIT's internal models, which include presumably conservative assumptions such as cost growth outpacing revenue growth per patient indefinitely, still show rental coverage ratios bottoming in 2018.

By 2025 Omega expects its portfolio rental coverage ratio will rise to between 1.7 to 2.2, which would be its highest levels ever. Again that's not due to a reversal of the negative trends the industry faces, but purely due to rising patient counts driving stronger revenue growth for SNF operators that are expected to offset these headwinds.

Source: Omega Healthcare Investor Presentation

However, with the theoretical boom times still in the future, Omega had to address numerous challenges that SNF operators faced while they waited.

Most notably, many of Omega's major tenants faced such financial distress (unsustainable rental coverage ratios) that they required lease adjustments to stay in business.

Some operators like Orianna actually did go bankrupt, forcing management to either find new tenants for those facilities or sell them to recycle the capital into new locations leased to stronger tenants.

Combined with several such negotiations, management embarked on a two-year turnaround that involved a large amount of asset sales including $290 million in 2017, $340 million through the first three quarters of 2018, and an additional $78 million planned (the Orianna facilities tied up in bankruptcy court and 10 to 15 additional properties).

Management believes that its asset sales, designed to leave it with a stronger and healthier property portfolio, are now essentially complete. Here's what the firm's CEO told analysts on the third-quarter 2018 earnings conference call.

“We have substantially completed our strategic disposition program and... in the coming 12 months we would envision returning to our historical growth model where acquisitions meaningfully exceed dispositions.” - CEO Taylor Pickett

While a return to growth would be welcome news, investors should not expect Omega to get back to its historical pace of double-digit cash flow per share growth. In fact, the industry's headwinds are so great that analysts currently expect only low single-digit cash flow per share growth from Omega in the long term.

Overall, the SNF industry offers some interesting long-term growth potential as America's population ages and properties continue consolidating. Omega Healthcare has done its best to run its business conservatively as it waits for more significant demographic tailwinds to kick in, rewarding investors with generous dividends as they wait.

However, the industry still faces a number of uncertainties that could cause real problems. Omega is a high-risk stock that investors should only consider owning if they are comfortable with its complex risk profile.

Key Risks

While Omega Healthcare should have the wind at its back when it comes to acquisition-fueled growth and favorable demographic trends, there are nonetheless several important risks to keep in mind.

Most notably, skilled nursing generally has higher reimbursement risk than other areas of healthcare because its operators depend more on reimbursements from the government. As a result, changes in federal policies and increased scrutiny over billing practices of SNF operators have the potential to materially impact the ability of Omega’s tenants to meet their lease obligations.

It can't be overstated just how big of a headwind CMS changes that began in 2010 and escalated in 2011 have been for the SNF industry. Occupancy rates have steadily fallen by significant amounts and are just now apparently bottoming, as the aging demographic trend finally starts to assert itself.

In 2018 CMS increased Medicaid SNF reimbursement rates by 1.8%. While that's certainly a positive for the industry, keep in mind that from 2003 to 2018 the average annual increase was 3.8%. This shows that in the future, the ever more cost sensitive Federal government is likely to be far less generous with its pay increases to Omega's tenants.

What's more, Omega's proprietary tenant coverage model, which represents the core of the bull case for the stock, is based on assumptions that SNF expenses will only outpace daily patient revenues by no more than 0.8% per year (because that was as bad as things got over the last 5 years). However, the tightest job market in decades means that wages are rising at an accelerating rate, especially at the lower end of the spectrum which includes many SNF employees.

Therefore, it's possible that Omega's internal models won't prove conservative enough, and that the firm's improved property portfolio will merely allow its overall rental coverage to remain stable.

In fact, CEO Taylor Pickett even told analysts on the third-quarter 2018 earnings conference call that Omega's turnaround plan (now largely complete) was merely designed to buy the REIT time for demographic benefits to kick in. When asked if Omega expected to see stronger coverage in 2019, Pickett replied:

"I think coverages will be relatively stable, but I don't see them improving. I think the headwinds of labor and the ongoing battle around occupancy, which I’ll note that our operators have held occupancy fairly stable...So, I think, we're going to see general stability as we continue to battle the headwinds and we do have the benefit of a decent Medicare increase October 1st, some decent Medicaid rate increases. So, it’s not all headwinds even in the next 12 months, but certainly, I don't expect coverages to come rebounding up into the 1.4s over the next 12 months. We think post-PDPM and the demographics really taking hold, we'll start to see some positive momentum in ‘20 for sure." - CEO Taylor Pickett

The company’s percentage of revenue from private payers has been gradually climbing over time, thanks to management’s decision to decrease its reliance on government healthcare funding. The acquisition of hospitals that comes with MedEquities will further help diversification efforts. But Omega’s prosperity is unfortunately at the mercy of Washington for the foreseeable future (private pay only accounts for 12.5% of tenants' revenue).

By now, the murky risks of the SNF industry should be clear. Due to the industry’s challenges and reimbursement uncertainties, in recent years many healthcare REITs have exited the SNF space. Some of the biggest names include Ventas (VTR), HCP (HCP), and Sabra Healthcare (SBRA), which are all seeking greater portfolio quality and cash flow predictability.

Given the riskier nature of SNFs, it also may not come as a surprise to learn that Omega was forced to cut its dividend in 2000. But why did the company have to cut its dividend, and could that same risk reemerge in the future?

The answer comes from Omega’s 2001 annual report. The Balanced Budget Act of 1997 introduced a new payment system for the reimbursement of Medicare patients in SNFs.

A major shift took place in which a cost-based reimbursement system that was historically used was essentially abandoned in favor of a reimbursement system that capped payments per service at a fixed amount. This was done by the government to save money and attempt to balance the federal budget by 2002.

While some of these payments changes were reversed by subsequent legislation in 1999-2000, the result was a major reduction in payments made to nursing home operators.

Many of Omega’s tenants were forced to declare Chapter 11 bankruptcy and could no longer make their rent payments. They had generally been levering up to fund acquisitive growth in the years leading up to the legislation and were not prepared for the substantial reimbursement reductions. Basically, the reforms made to the Medicare reimbursement system in the late 1990s were nothing short of transformational.

While federal policy is still characterized by a healthy dose of uncertainty today, new legislation will likely be relatively more incremental, phased in over a long period of time, and will not result in bankruptcies like those that occurred over 15 years ago.

Simply put, another transformational shift seems unlikely, and Omega's management has commented that today's proposals, which are more about fixing policies to prepare the healthcare system for the demographic wave that's coming, are incomparable to the challenges the industry faced in the late 1990s. Getting more efficient with patient lengths of stay and making sure people have access to care are larger priorities than the dollar amounts paid.

However, the situation is worth monitoring as we all know how unpredictable governmental policies can be, and it's never desirable for an investment thesis to bank on neutral or favorable legislative outcomes.

Even if Medicare and Medicaid policy doesn’t end up shifting severely, the main growth catalyst for the SNF industry (an aging population) will still take time to bear fruit given the low occupancy rates today, meaning that the next few years could remain trying for many of Omega’s customers.

Finally, there's Omega's dividend safety to consider. The firm's FAD payout ratio came in at a troubling 97% in the third quarter of 2018, although management noted that backing out one-time charges associated with the turnaround (and Orianna's bankruptcy proceedings) it would have been 91%.

Regardless, Omega has historically had a FAD payout ratio of around 85%, so the dividend has a smaller margin of safety compared to the past. And given the large amount of policy risk and cost inflation the REIT's tenants are exposed to, Omega's dividend may not be a sure bet.

While it looks likely that Omega will return to cash flow per share growth in 2019, especially thanks to its recent acquisition, investors have to realize that Omega's payout ratio is likely to remain elevated for several more years. In other words, shareholders shouldn't necessarily expect a return to dividend growth in the next year or two.

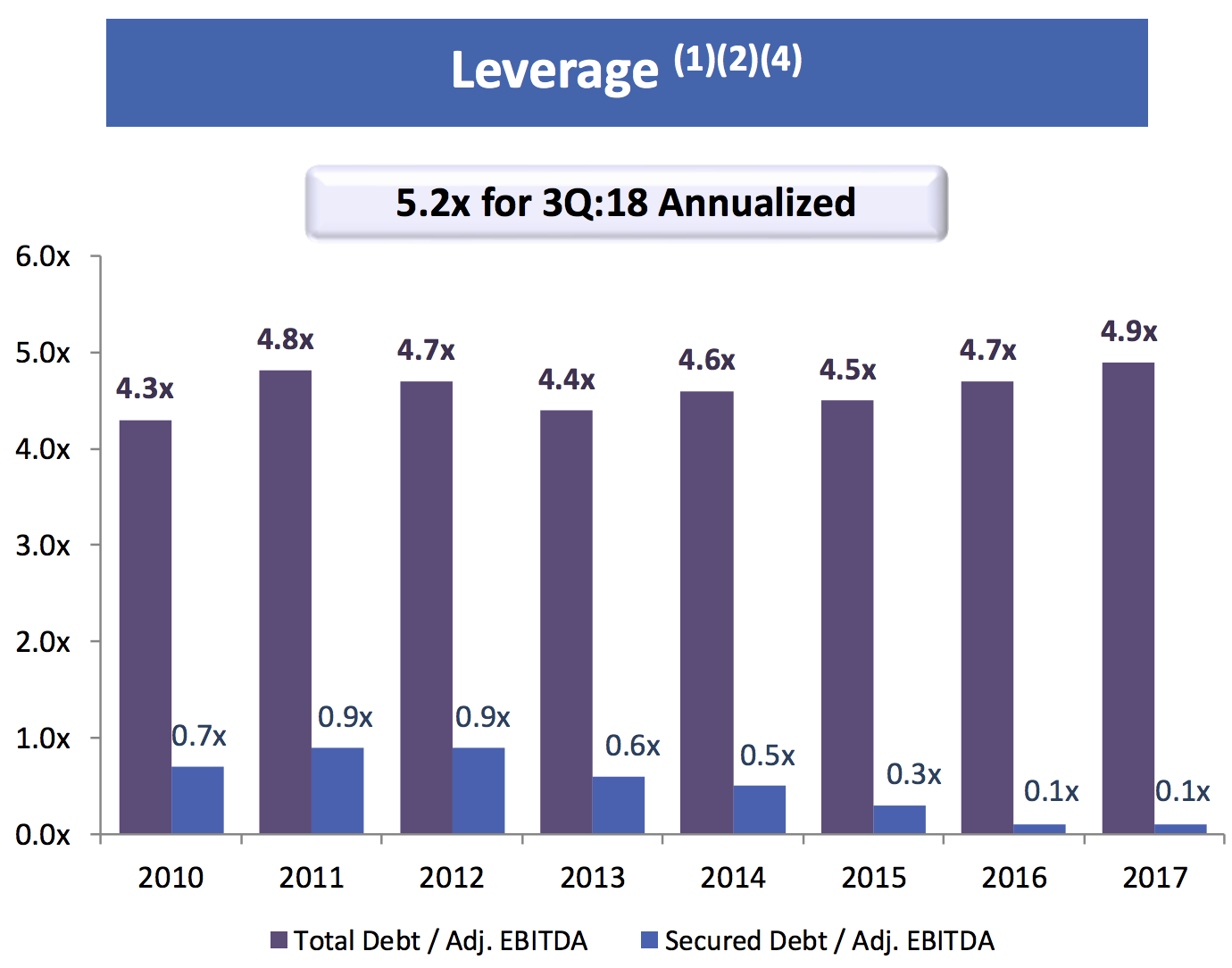

Dividend growth prospects are especially dim since during the turnaround Omega's leverage ratio (debt/Adjusted EBITDA) rose above 5.0 and now exceeds management's long-term target of 4.0 to 5.0.

Improving its leverage ratio is critical to Omega maintaining its BBB- investment grade credit rating and access to low-cost borrowing. The REIT is going to have to reduce its leverage ratio in 2019 and beyond in order to avoid risking a downgrade to junk bond status which would increase its cost of capital and make profitable growth that much harder.

Source: Omega Healthcare Investor Presentation

Given its need to deleverage, Omega is likely to have to continue lowering its payout ratio to at least 85%. Retaining more cash flow is also important to give the firm some cushion in case its share price were to weaken, making accretive equity-financed acquisitions more challenging.

Even assuming that the SNF industry's fundamentals do finally turnaround for the better, investors can likely expect dividend growth in line with cash flow growth, which is currently forecast at close to 2% per year. That's a far cry from the company's historic pace of payout growth.

Closing Thoughts on Omega Healthcare

Omega Healthcare appears to be a well-managed firm operating in a very difficult industry that faces many risks outside of management's control. The company seems to have some cushion to absorb some unfavorable developments with its operators for now, but income investors interested in the stock need to keep a very close eye on these developments.

Monitoring occupancy and rent coverage metrics closely over the coming quarters will help determine how isolated the recent cases of Omega's troubled tenants really are (i.e. are recent issues isolated to a few underperforming operators, or is the tide starting to go out on all SNF players?).

There is certainly risk that Omega Healthcare turns into a value trap, so maintaining appropriate position sizes and healthy portfolio diversification are very important to acknowledge the wide range of outcomes that Omega faces. It's unlikely the uncertainty that's facing the industry will lift anytime soon, making Omega Healthcare a higher risk stock.