Enterprise Products Partners: One of the Best MLPs for Income

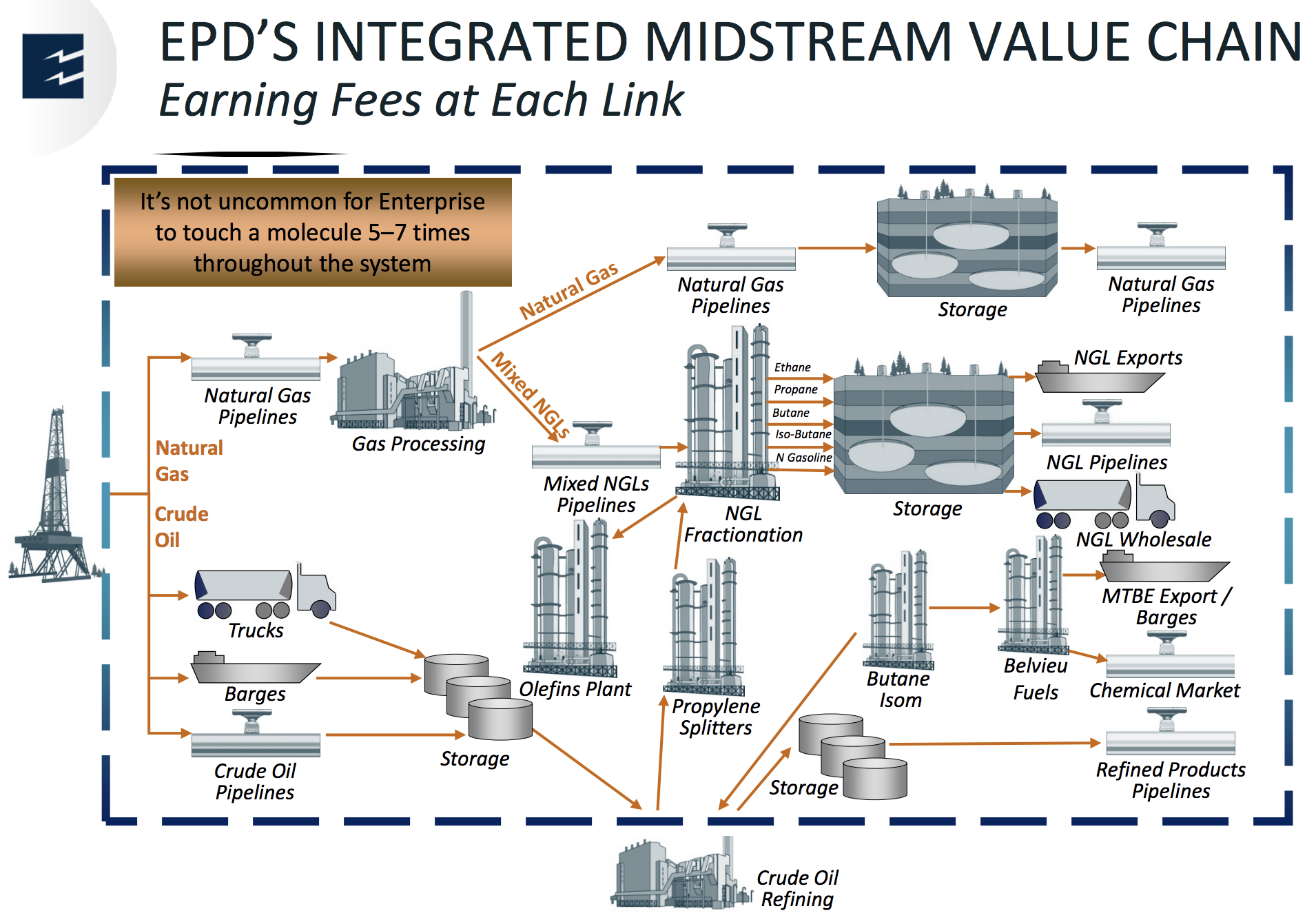

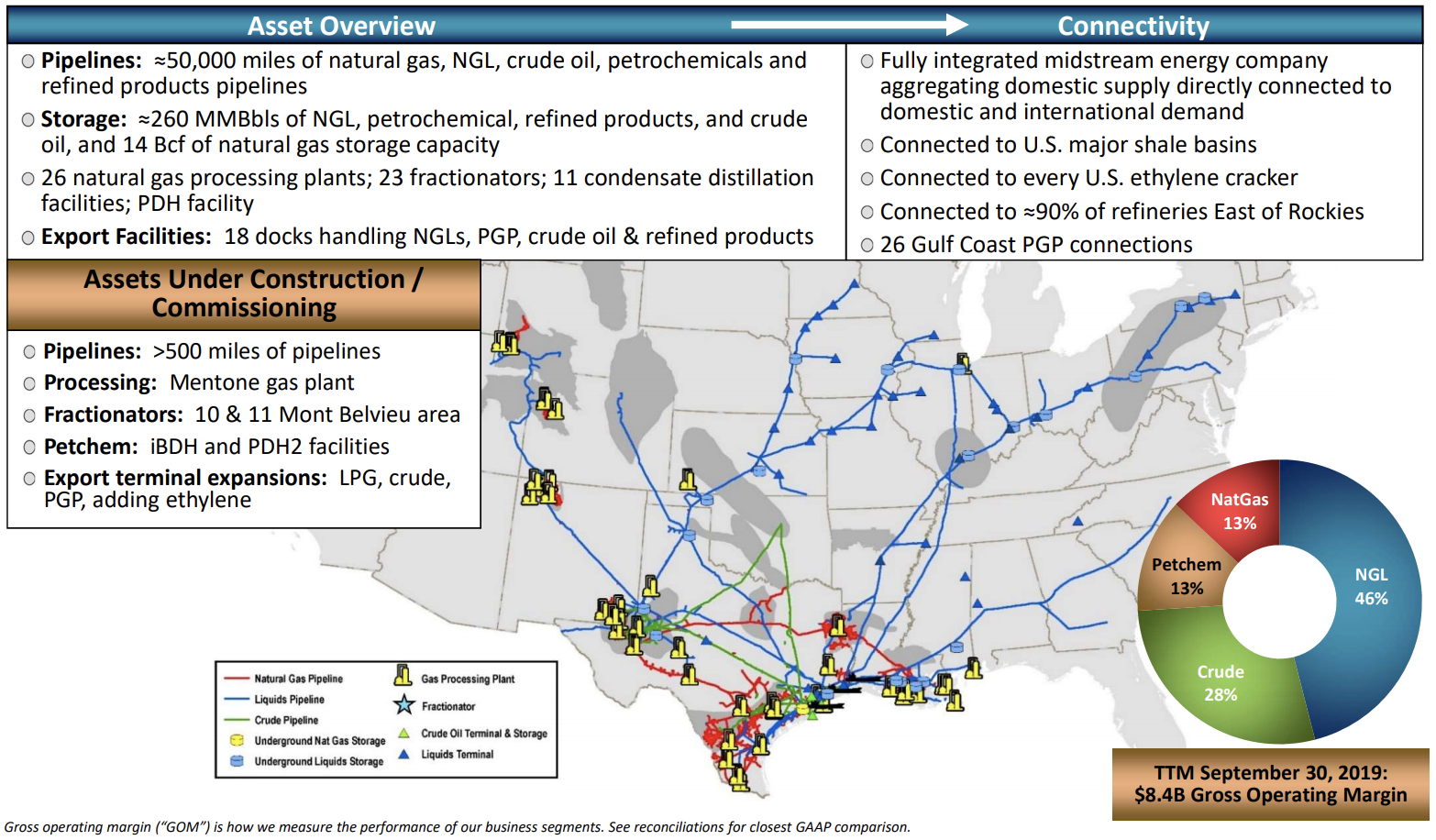

Enterprise Products Partners (EPD) is one of North America's largest midstream master limited partnerships, with about 50,000 miles of natural gas, natural gas liquids (NGL), crude oil, refined products, and petrochemical pipelines. The firm also owns a number of storage facilities, processing plants, and export terminals.

Enterprise’s network of assets is connected to nearly every major U.S. shale basin, helping move different types of energy and fuel from one location to another for upstream exploration and production (E&P) companies. The firm is also one of the largest exporters of crude oil, as well as NGL and NGL-derived products.

Enterprise makes most of its money from fees it charges E&P customers for its transportation and storage services.

Source: Enterprise Investor Presentation

NGL transportation and processing provides the majority of the company’s profits (46%). Crude (28%), petrochemicals (13%), and natural gas (13%) account for the remainder of Enterprise's business mix.

Source: Enterprise Investor Presentation

Enterprise has raised its distribution for 21 consecutive years.

Business Analysis

The pipeline business has a number of appealing qualities. For one thing, constructing a pipeline can cost billions of dollars and take years to complete, resulting in high barriers to entry. Few companies have the capital and industry connections (e.g. oil & gas producers, regulators) to build and operate pipeline systems, which are also highly regulated.

Only so many pipelines are needed within a particular geographic area as well, often resulting in a consolidated market. Pipelines also have few substitutes given their safety and cost-efficiency, along with geographical constraints. (Many oil & gas formations are in hard-to-access areas.)

Furthermore, pipelines enjoy relatively stable demand patterns since many of the products that require refined oil and gas are non-discretionary in nature. In a way, the midstream industry is similar to the utility sector in that it provides an essential service for U.S. oil, gas, and NGL producers, resulting in a stable cash flow stream.

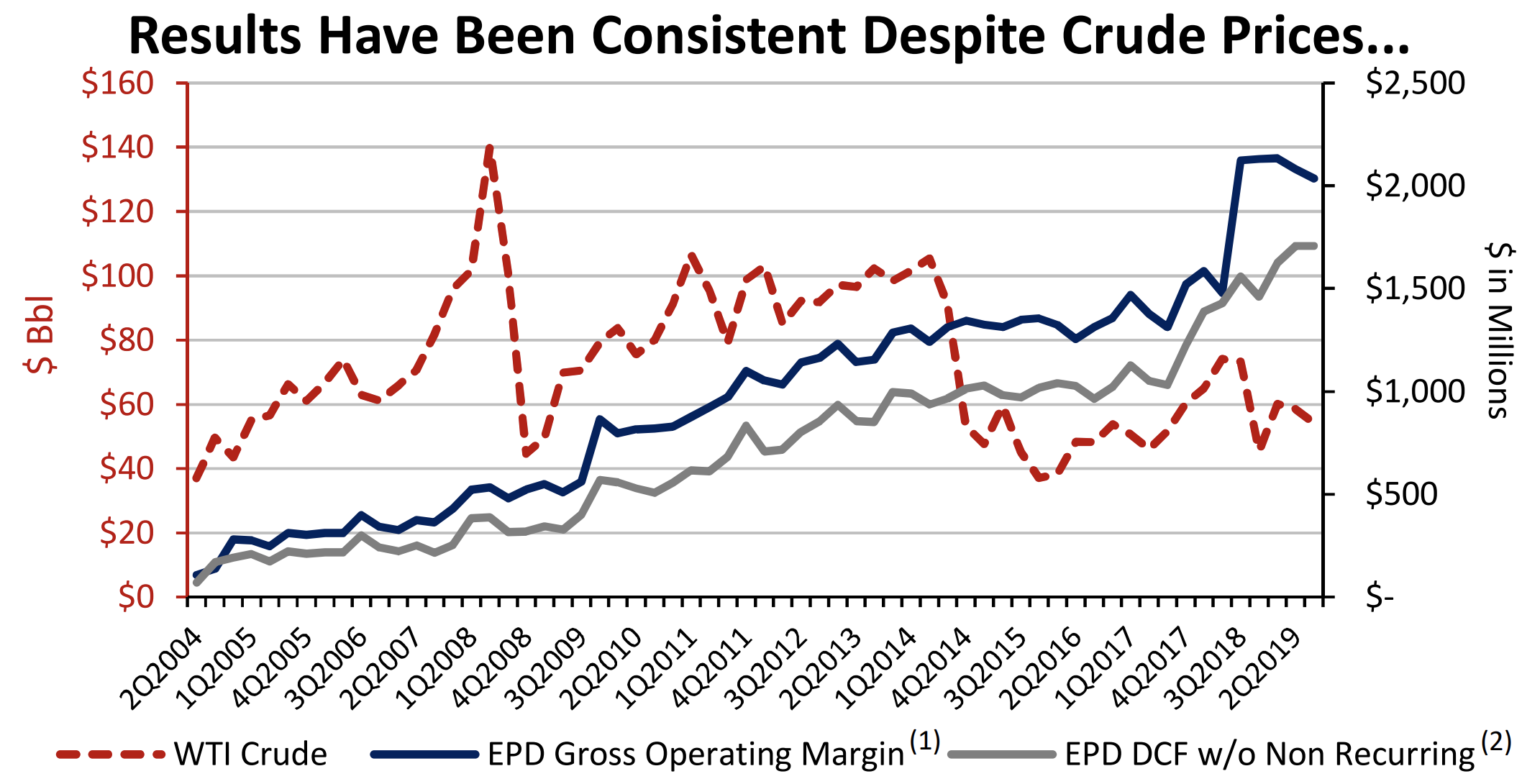

In fact, Enterprise’s claim to fame is its track record of stable growth through all sorts of commodity price, economic, and interest rate environments.

The company has paid uninterrupted distributions since going public in 1998 largely due to its business model, which is less sensitive to oil & gas prices than one might initially think. This is because most of Enterprise’s cash flow is protected by long-term, fixed-fee contracts with minimum volume guarantees and annual rate escalators to offset inflation.

In addition, many of its contracts guarantee a minimum gross margin, which helps to further stabilize cash flows even if energy prices collapse (as long as customers can still pay). As a result, Enterprise's distributable cash flow (DCF) has managed to consistently rise despite wild swings in the price of oil.

Source: Enterprise Investor Presentation

Besides the attractive characteristics of the pipeline business, a major key to the MLP's success is management's well-aligned incentives with unitholders.

Management owns 32% of Enterprise's units (what MLPs call shares). The firm's high insider ownership helps explain why the team has always taken a long-term view to maximize Enterprise's distribution safety and growth potential.

That includes eliminating half of the partnership's incentive distribution rights, or IDRs, in 2002, and then fully in 2011 in a stock-based transaction that avoided both taxes for unitholders as well as a distribution cut.

IDRs send up to 50% of marginal cash flow to the general partner and significantly increase an MLPs cost of capital, making it harder to grow profitably.

In 2018, Enterprise took further action to strengthen its risk profile by implementing a more conservative self-funding business model, which makes the firm's growth plans completely independent of swings in its stock price.

Under this structure, Enterprise no longer needs to issue equity to fund part of its expansion projects. Instead, the firm uses a mix of internally generated cash flow and debt, reducing its financing risk and lowering its cost of capital.

Enterprise's conservative management team has also led the MLP to be cautious with its use of debt. The firm's BBB+ credit rating from Standard & Poor's is tied for the highest in the midstream energy space and further helps Enterprise maintain dependable, low-cost access to debt markets to fund its growth.

Looking ahead, Enterprise sees opportunity to continue expanding its business as the U.S. energy renaissance continues. In the last decade, America has more than doubled its crude output and increased its natural gas production by more than 60%, according to the Wall Street Journal.

America's oil & gas production boom has resulted in strong production growth of NGLs. NGLs are important feedstocks for the petrochemical industry, which uses them to make materials such as plastics.

Low cost U.S. natural gas has resulted in much cheaper NGLs in America compared to Europe and Asia, fueling strong export demand. With domestic production investments expected to continue and exports rising, Enterprise has focused the vast majority of its growth spending on NGLs and petrochemicals.

Overall, Enterprise Products Partners appears to be one of the lower-risk choices in the midstream energy space due to its strong balance sheet, access to low-cost capital, low-risk self-funding business model, and conservative management team.

Key Risks

One of the biggest uncertainties facing the energy sector is how long demand will grow for oil and gas. Naturally, in its investor presentation Enterprise highlights data from the IEA World Energy Outlook showing a forecast for global oil and liquids demand rising for the next 20-plus years, driven by emerging markets.

Source: Enterprise Investor Presentation

However, some investors worry that the world's growing push to reduce carbon emissions and embrace renewable energy will cause fossil fuel demand to peak within 20 years, sooner than many energy executives expect.

Meanwhile, in the short term, weak oil and gas prices due to the U.S. shale boom have significantly hurt the profitability of many fracking-focused energy producers. Shale companies are responding by cutting back on spending and taking actions to strengthen their fragile balance sheets.

These trends could weigh on U.S. oil and gas production or make it more difficult for energy producers to honor their contracts with midstream companies. Over 70% of Enterprise's revenue is from customers with an investment-grade credit rating or backed by a letter of credit, mitigating some of this risk.

However, since pipelines have fixed costs, their profitability is sensitive to the amount of fees they charge and how much product volume they are able to move. If energy production were to fall and remain depressed for a prolonged period of time, the need for pipelines could theoretically decline and dent the economics of Enterprise's growth projects.

Investors should also note that Enterprise's stock price is sensitive to oil prices, even if its cash flow is not. In other words, while Enterprise is effectively an energy utility, it's stock performance is nowhere near as stable as actual regulated utilities.

Finally, investors should note that Enterprise, as an MLP, issues K-1 tax forms instead of 1099s which can cause headaches if the stock is held in tax-deferred accounts such as IRAs.

Management is exploring the idea of converting from a partnership to a corporation which would simplify the tax issues investors deal with and perhaps fetch a higher valuation for the firm. A conversion is unlikely to affect the safety of Enterprise's payout or trigger tax consequences for most investors.

Closing Thoughts on Enterprise Products Partners

Midstream MLPs have experienced a wave of corporate restructuring as falling energy prices raised concerns about the industry's long-term growth potential and the safety of many distributions as capital costs rose sharply.

However, Enterprise remains one of the most conservative businesses an income investor can own in this space. With a long history of distribution growth, a healthy balance sheet, a low cost of capital with a self-funding business model, strong distribution coverage, and tailwinds from U.S. shale production growth, Enterprise represents an intriguing high-yield investment opportunity.