Founded in 1911, International Business Machines (IBM) is one of the world's oldest tech companies. Today IBM is the largest IT provider for businesses around the world. It operates in five main business segments.

Technology Services & Cloud Platforms (43% of revenue, 25% of operating income): provides cloud and project-based outsourcing services to help improve clients' IT infrastructure. This segment also offers technical support for integrated software solution products the company sells.

Cognitive Solutions (23% of revenue, 48% of operating income): includes Watson, the cognitive computing (artificial intelligence) platform that uses natural language, processes big data, and learns from interactions with people and other computers. This segment offers data and analytics solutions, cloud data services, enterprise social software, talent management solutions, and software tailored to various industry-specific needs, including banking, airlines, and retail industries.

Global Business Services (21% of revenue, 11% of operating income):business consulting services, system integration, application management, maintenance, and support for packaged software applications, as well as outsourcing services. As clients transform themselves in response to market trends like big data, social and mobile computing, IBM helps clients use these technologies to reinvent relationships with their customers and realize new standards of efficacy and efficiency across their businesses.

Systems (10% of revenue, 6% of operating income): the legacy hardware business that provides server and data storage infrastructure for various corporate clients. This segment has experienced revenue declines over the last decade due to product cycles, client losses, and certain clients migrating to the cloud.

Global Financing (2% of revenue, 9% of operating income): finances company sales via lease, installment payment plans, and loan financing. Also provides short-term inventory and accounts receivable financing to suppliers and distributors.

IBM has been in a multi-year turnaround, refocusing its business from legacy hardware and IT software to what it calls "strategic imperatives," or SI. These are increasingly subscription-focused cloud computing, data analytics applications, and cybersecurity products that IBM believes represent the future of global IT. SI accounted for 50% of IBM's total revenue in 2018 and grew 9%.

IBM has raised its dividend for 23 consecutive years meaning it will become a dividend aristocrat in 2020.

Business Analysis

IBM has long been known for its legacy IT services, which have been the backbone of corporate IT departments around the world for decades. This created a highly stable and recurring revenue source since there are huge challenges with switching IT vendors, including the potential for meaningful business disruption that most companies would rather not face.

Warren Buffett famously invested in the stock in 2011 for many of these reasons. His familiarity with IBM goes back a long way – he says he has read every annual report since 1961. In early 2018 Berkshire (BRK.B) completed exiting its position in IBM.

While Buffett ultimately exited his losing position in IBM by early 2018, his past public comments suggest he was initially attracted to IBM’s trusted brand name and the stickiness of its customer relationships:

“I imagine as you go around the world that there are – there’s a fair amount of presumption in many places that if you’re with IBM, that you stick with them, and that if you haven’t been with anybody, you’re developing things, that you certainly give them a fair shot at the business.”

“The IT departments, you know, we’ve got dozens and dozens of IT departments at Berkshire. I don’t know how they run. I mean, but we went around and asked them and you find out that there’s – they very much get working hand in glove with suppliers. And that doesn’t mean things won’t change but it does mean that there’s a lot of continuity to it… Now, I would imagine if you’re in some country around the world and you’re developing your IT department, you’re probably going to feel more comfortable with IBM than with many companies.”

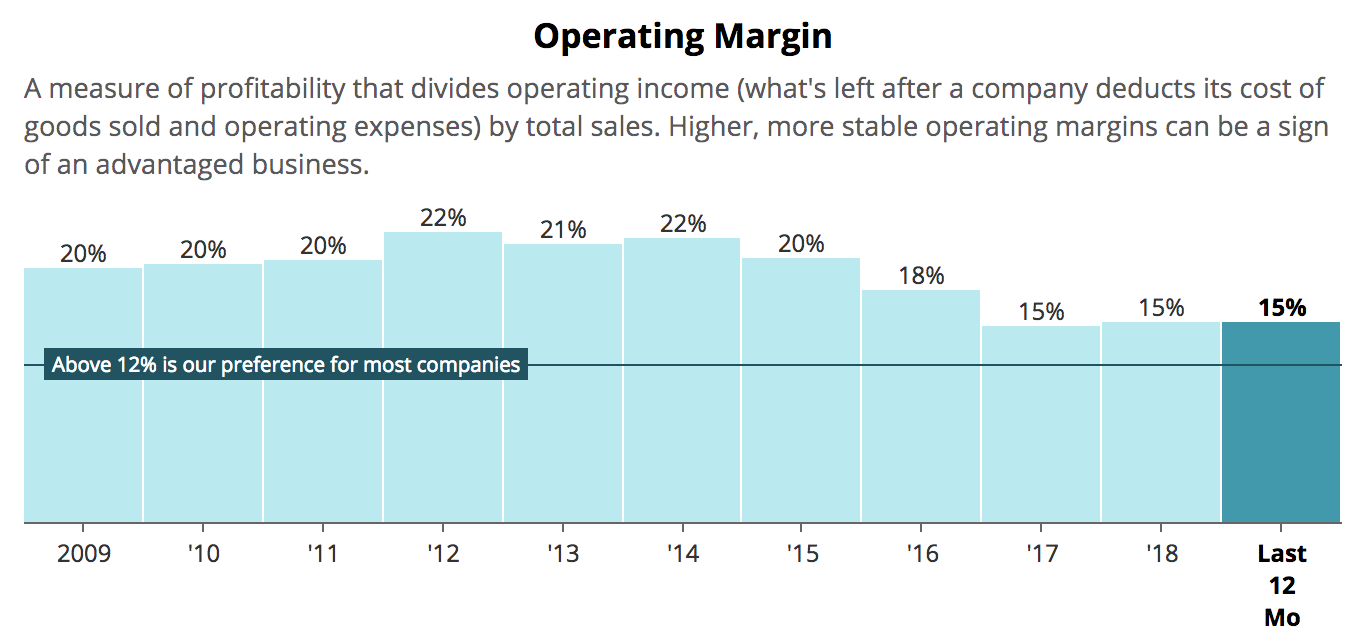

In other words, IBM has historically enjoyed a wide moat, thanks to high switching costs that allowed its legacy businesses to command strong pricing power and generate gross margins of 55% to 60%.

While IBM's legacy IT and server business remains large (with a backlog of nearly $120 billion), in recent years the trend has been for companies to shift more and more of their IT needs to the cloud, especially software applications that help boost efficiency and cut costs.

IBM took a long time to accept this new reality, but in 2012 the company, under new CEO Virginia Rometty, embarked on a massive turnaround plan (one of several it's done over the past century). The new focus would be on strategic imperatives, specifically cloud computing, AI-driven software applications, and cybersecurity offerings.

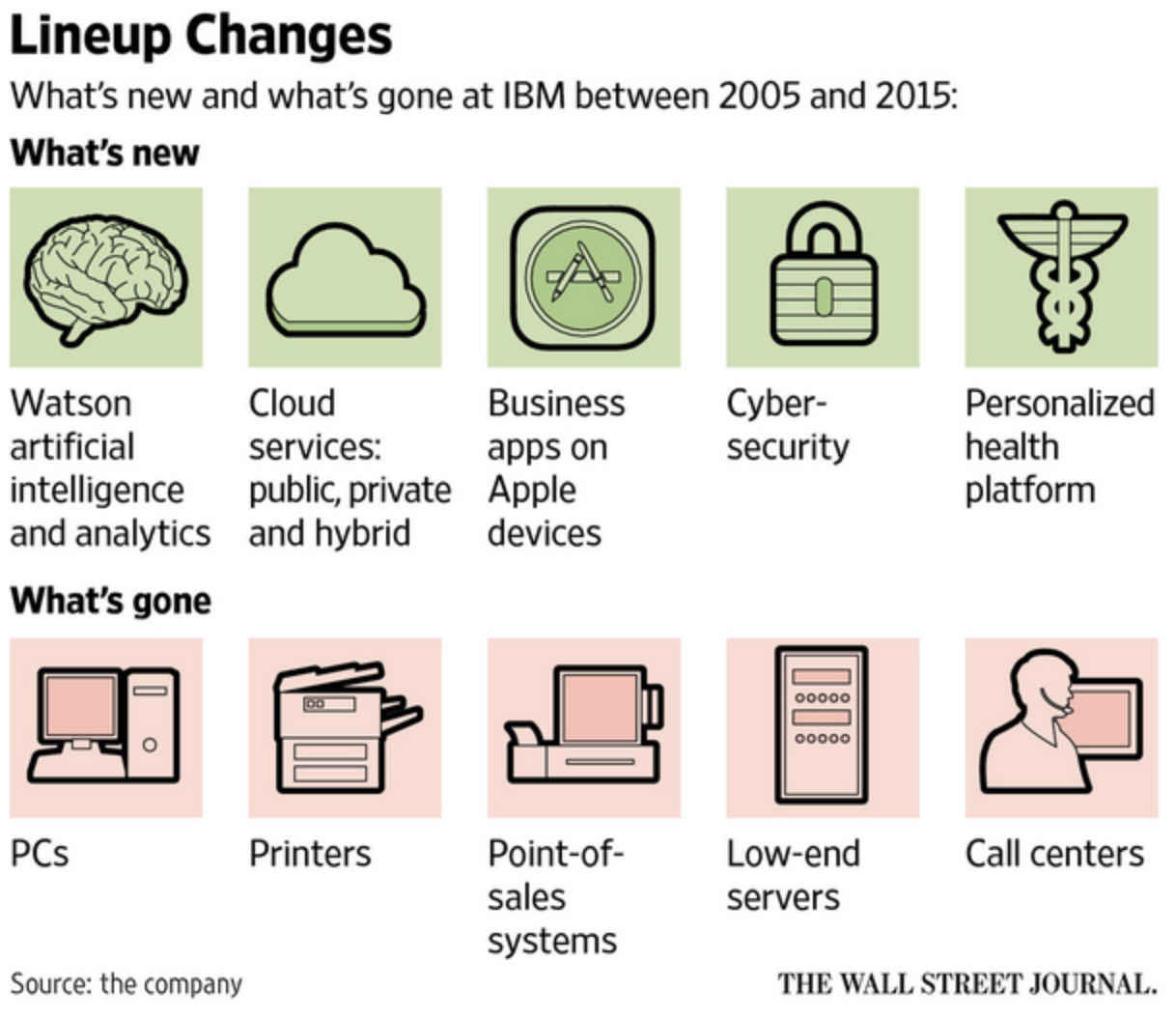

As you can see below, IBM has divested many of its legacy hardware lines as well, which were once lucrative businesses for the company, but later became unprofitable and uncompetitive. Perhaps these divestitures serve as examples of a once-dominant company sitting on its laurels for too long, forgetting how to profitably innovate to maintain a strong market position.

Source: The Wall Street Journal

The company has relied on its R&D operations to help drive this pivot into the most important tech markets. In 2018 IBM was granted a record 9,100 patents, marking the 26th consecutive year in which the firm received the most patents of any corporation in America.

Between 1993 and 2018 alone the company obtained over 110,000 patents, including over 5,000 in 2018 for critical fields such as cloud computing, artificial intelligence, and cybersecurity. IBM generally spends $5 billion to $6 billion per year on R&D, or about 6.5% of revenue.

IBM's R&D facilities have helped generate a number of impressive products and services for the company. For example, the Watson cognitive computing (AI) deep learning platform, which underpins IBM's cloud computing business, has already been adopted by hundreds of corporate clients around the world, in dozens of industries.

In fact, according to CEO Virginia Rometty, Watson is a potential game-changer for IBM "touching a billion people...and be able to address, diagnose, and treat 80 percent of cancer in the world." Along with its other capabilities, IBM calls Watson "one of the most powerful tools our species has created."

IBM has integrated Watson into various aspects of its cloud computing and IT offerings while partnering with companies around the world, both as customers and partners in developing new applications.

Source: IBM Investor Presentation

The market for services which help companies make various business decisions is expected to reach about $2 trillion per year by 2025, meaning that IBM could have huge growth potential, especially given its global reach.

Source: IBM Investor Presentation

In an effort to maximize market share in this large and fast-growing industry, in October 2018 IBM announced a $34 billion deal to acquire Red Hat, a leader in hybrid cloud software. According to CEO Virginia Rometty:

"The acquisition of Red Hat is a game-changer. It changes everything about the cloud market. IBM will become the world's number one hybrid cloud provider, offering companies the only open cloud solution that will unlock the full value of the cloud for their businesses." – CEO Virginia Rometty

Redhat has been in business for over 20 years and essentially provides corporations with software they need to manage their applications across their in-house data centers and with cloud providers such as Amazon (AMZN), Microsoft (MSFT), and IBM.

IBM claims that 80% of enterprise workloads have yet to migrate to the cloud. The idea is that many companies will opt to keep some of their computing on their own servers while migrating other programs to various cloud providers. Red Hat helps make that work easier for software developers.

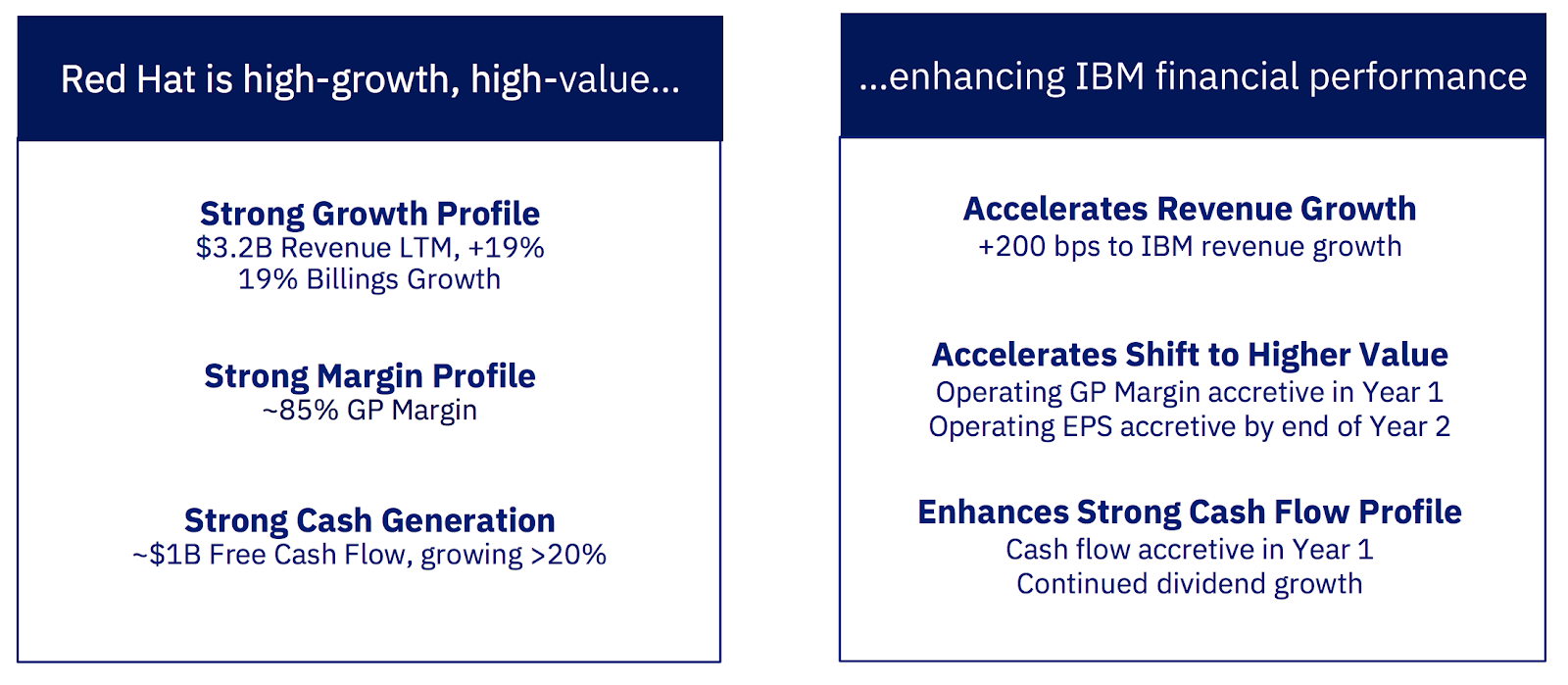

Red Hat's business model is certainly appealing. Mature software companies are known for their impressive profitability and excellent cash flow generation. Red Hat sports an 85% gross margin, does business with 90% of the Fortune 500 companies, enjoys strong double-digit revenue growth, and has a free cash flow margin north of 20% (compared to IBM's 8%).

Source: IBM Investor Presentation

In other words, IBM appears to be buying a thriving and fast-growing business. While Red Hat will account for less than 5% of IBM's total sales, management believes it will boost IBM's revenue growth rate by 200 basis points and improve its gross margin and cash flow per share in the first year after closing.

Source: IBM Investor Presentation

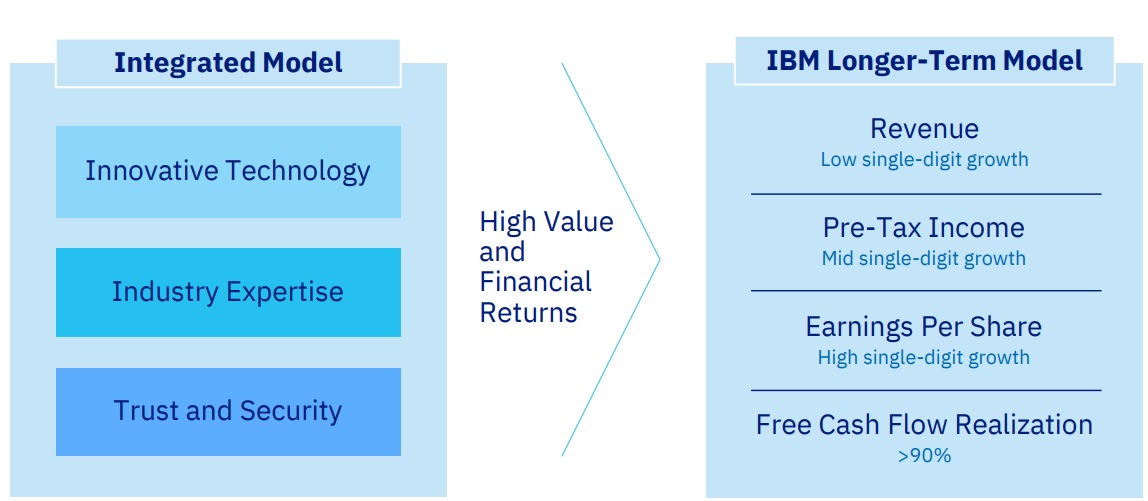

In theory, owning Red Hat should improve the company's chances of achieving its goal of achieving high single-digit EPS and free cash flow per share growth in the long term. If successful, IBM's dividend could grow at a similar pace.

Source: IBM Investor Presentation

In the meantime, the company's legacy businesses, while in gradual decline, continue to generate significant free cash flow ($13.3 billion in 2018) from which IBM can pay its generous dividend ($5.7 billion in 2018).

So at first glance, IBM may seem like a potentially good choice for yield-seeking tech investors. However, IBM's future may not be as bright as management might have you believe.

Key Risks

The way management describes it, IBM has a bright future powered by a leading position in hybrid cloud computing and SI businesses, which are supported by the firm's mountain of patents related to buzz-worthy tech such as quantum computing and artificial intelligence. Yet Buffett has now sold all of his position in the company.

At Berkshire Hathaway’s annual shareholder meeting in May 2017, Buffett said:

“I don’t value IBM the same way that I did six years ago when I started buying. I’ve revalued it somewhat downward…they’ve run into some pretty tough competitors.” – Warren Buffett

Buffett's comments highlight the biggest reason for IBM's languishing sales and profits in recent years. IBM's legacy hardware, which has historically been very profitable, is declining steadily while growth in its relatively new SI units has been slowing.

Simply put, IBM's R&D efforts appear to be far less effective at actually delivering superior technologies compared to its rivals. The company's mountain of patents has not translated into stronger sales or cash flow growth for many years.

Source: Simply Safe Dividends

The company's Cognitive Solutions business, which generated 48% of IBM's 2018 operating profits and is where the majority of Watson's sales are recorded, is a primary example of IBM's futile efforts to innovate.

Despite the company's hype about the amazing capabilities of its Watson AI platform, in the fourth quarter of 2018 the Watson business segment posted just 5% revenue growth in its cloud operations, suggesting that corporate clients are not that impressed with its abilities.

In contrast, Microsoft's (MSFT) Azure cloud platform has been growing at nearly 100% for several years, and the worldwide cloud infrastructure market grew 46% in late 2018. As a result, IBM's could market share is minimal and declining, which bodes poorly for the future given the strong network effects of the cloud as rivals' platforms becoming increasingly developed with data analysis applications.

Source: Canalys

Amazon, Alphabet, and Microsoft are extremely formidable competitors in this market and others. It's hard to see any unique advantages IBM brings to the table to significantly improve its market position.

Even if the company's all-important "Strategic Imperatives" accelerate their growth rate, there is a potential downside to this. Specifically, while IBM's legacy servers may be a declining business, they still represent the company's second most profitable segment. Only Watson-based Cognitive Solutions generates greater gross margins.

In other words, as IBM transitions away from legacy businesses and towards an ever-larger percentage of revenue from SI, margins could continue declining. For example, what if IBM catches up to Amazon, Microsoft, Google and other cloud providers only to find that industry profitability has been completely eroded in a race to the bottom? Double-digit price cuts are not unheard of in these markets.

Source: Simply Safe Dividends

Business applications, security, and analytics are also much more dynamic markets than mainframes, making it more difficult to forecast future cash flows. Even if the margins end up being there, it could take a decade before IBM’s new businesses are generating the same level of sales and income as the legacy businesses they are intended to gradually replace.

These questions will likely remain unanswered for quite some time and shrouded in uncertainty given IBM's recent results and spotty capital allocation track record.

Which brings us to Red Hat, which IBM's CEO calls a "game changer" that will flip the script and make IBM a dominant player in cloud. There are reasons to be skeptical that this huge M&A deal (the largest software acquisition in U.S. history) will turn out nearly as well as management hopes.

First, note that IBM paid over 10 times trailing sales and more than 30 times free cash flow for Red Hat. Red Hat's fourth-quarter 2018 revenue growth moderately slowed to 17%, and that's off a relatively small revenue base (less than $3 billion in annual sales).

If Red Hat doesn't continue its growth trajectory, or the hybrid cloud landscape shifts in a way management did not expect, shareholders will be regretting this risky deal, which will meaningfully weaken IBM's balance sheet and overall financial flexibility.

S&P has already downgraded IBM's credit rating from A+ to A over the large amount of debt the company will have to take on to complete this deal. Moody's has put IBM's credit rating on watch for a downgrade citing:

"a substantial increase in leverage... and a departure from IBM's historical acquisition philosophy of making small, tuck-in acquisitions that limit integration risk." – Moody's

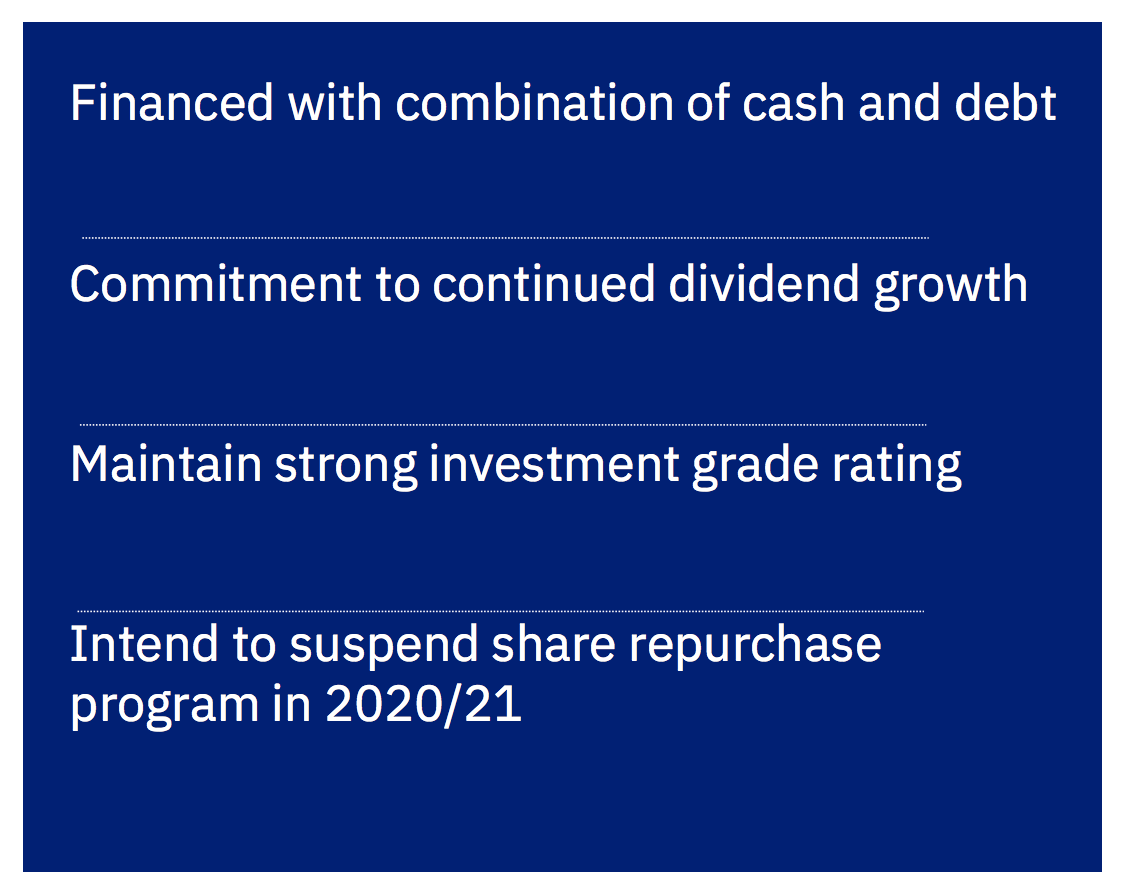

IBM has said that due to the need to deleverage the balance sheet (Moody's estimates net debt/EBITDA is going to roughly double) it is suspending its buybacks for 2020 and 2021. In recent years only aggressive share repurchases have allowed IBM's earnings and free cash flow per share to remain relatively stable.

Management expects these actions to allow IBM to continue growing its dividend, albeit at a very moderate pace for the foreseeable future. Based on the information we know today, the company's expectation appears reasonable.

Source: IBM Investor Presentation

Regardless, large acquisitions are risky endeavors. IBM is counting on the successful integration of its currently fading SI businesses with Red Hat's in order to achieve management's long-term 7% to 9% EPS and free cash flow per share growth rate. For now, based on the "cheap" multiple IBM trades at, it's clear that investors believe such guidance is wildly optimistic.

At the end of the day, IBM is saying all the right things about its SI-focused future and the large Red Hat acquisition appears to make strategic sense, at least at first glance. However, the company has a long way to go to demonstrate that it can effectively compete with giant rivals that have already proven themselves far more innovative and adaptive to the fast-changing pace of technology.

For now, IBM's management continues to struggle with its six-year (and counting) turnaround efforts that always promise a strong growth future is right around the corner, but thus far the company's track record on execution has been poor.

Closing Thoughts on IBM

IBM has traditionally been seen as a relatively safe, high-yield dividend grower, and for now it continues to be just that.

However, whether or not IBM can retain this status over the long term is still questionable. That's especially true because of major technological advancements (e.g. the cloud) and management's struggles with execution on its seemingly never-ending turnaround, which is now entering its seventh year.

Even if IBM is finally able to return to sustainable revenue, earnings, and free cash flow growth, management's inability to deliver on its timelines and cost-cutting promises calls into question the company's culture and just how profitable that future growth will be.

In addition, unless IBM is able to somehow accelerate its pace of strategic initiatives and cloud growth (and win greater market share), it's likely to end up a small player in the dominant tech industries of the future. As a result, the company could ultimately lose the competitive IT position it currently enjoys, which has been the basis for its long track record of strong and steady dividend growth.

Only time will tell if IBM’s bold $34 billion acquisition of Red Hat will pay off, but over the next few years the large amount of debt needed to close that deal will likely mean even slower dividend growth (low single digits) than the company has delivered in the past (4.7% in 2018 vs. 20-year average of 14% per year).

Conservative dividend investors may be better off sticking with other companies that have clearer paths to profitable long-term growth, have stronger dividend growth profiles, and operate in markets with a slower pace of change.