Chevron: A Quality Dividend Aristocrat in the Energy Sector

Chevron (CVX) was born from the discovery in 1879 of an oilfield near Los Angeles that yielded 25 barrels of oil per day. Today, Chevron is one of the largest oil companies in the world and produces nearly 3 million oil-equivalent barrels each day.

The firm's upstream operations (77% of 2018 earnings) explores for, produces, and transports crude oil, natural gas, and liquefied natural gas (LNG).

Chevron also owns refineries that use crude oil to make petroleum products such as gasoline, jet fuel, diesel, lubricants, additives, and petrochemicals. The company's downstream operations were responsible for 22% of earnings in 2018.

With major operations in over 30 countries and non-U.S. profits accounting for about 68% of the firm's bottom line, Chevron is a highly multinational enterprise.

Chevron and its predecessors have paid uninterrupted dividends since 1912. The oil giant has also raised its dividend for 32 consecutive years, making Chevron one of the few dividend aristocrats in the energy sector.

Business Analysis Energy producers sell commodity products and have virtually no ability to differentiate themselves based on quality. After all, it doesn't matter where you fill up your gas tank, only which gas station on your drive home is charging the least.

To make matters worse, energy prices are notoriously volatile and subject to numerous unpredictable factors outside any company's control, such as the outlook on global economic growth, weather patterns, and geopolitical conflicts.

For instance, unforeseen advances in fracking technology led to a staggering increase in the production of shale oil in the U.S over the past decade. The resulting oversupply pushed oil prices down to record lows in 2015, prompting many financially-weak producers to file for bankruptcy — a sign of just how ruthless the oil industry is to operate in.

How, then, has Chevron managed to overcome the oil industry's boom-and-bust cycles for more than a century, all the while maintaining a pristine dividend record, including 32 consecutive years of dividend increases?

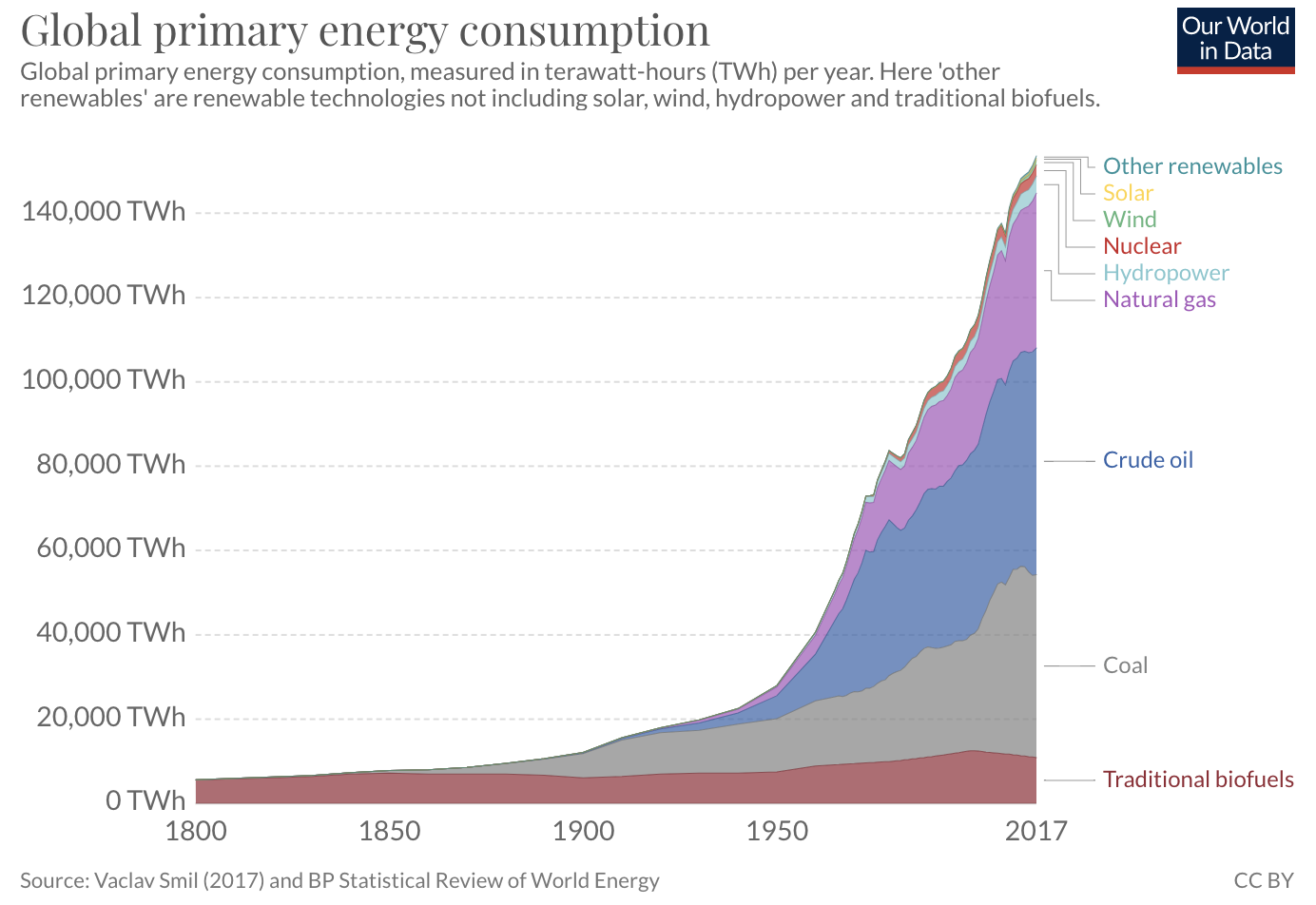

For one, the world's thirst for oil has grown exponentially, with global energy consumption witnessing a remarkable five-fold increase since 1950. Naturally, Chevron has thrived in this environment, as few companies are fortunate enough to experience such explosive demand for their products.

Source: OurWorldInData.org

Of course, many other oil-and-gas producers have come and gone during Chevron's time, highlighting the skill it's taken for Chevron to flourish. In short, Chevron has proven adept at managing costs (a must since profits are at the mercy of commodity prices) and making wise capital allocation decisions.

By acquiring rivals during downturns and continuously reinvesting profits to expand exploration and production of new oil and natural gas sources, Chevron has achieved a massive scale that gives the firm a lasting advantage over rivals.

For example, Chevron has developed a diverse portfolio of resources that include heavy oil, deepwater, natural gas, conventional oil, and shale. Moreover, Chevron's operations span the entire globe, with key production zones in North America, South America, Australia, Asia, and Africa.

This diverse asset base helps Chevron optimize its profitability through various commodity cycles and reduces the risk that any single project failure has a material impact on the firm, a luxury not afforded to smaller competitors.

Further strengthening the oil giant's competitive position is the firm's vertical integration. Chevron participates in all aspects of the fossil fuel business, such as manufacturing refined products like gasoline, diesel, and petrochemicals. These "downstream" operations use crude oil as an input and benefit from low oil prices, helping stabilize the company's cash flow during lean times.

Importantly, Chevron has managed to scale and diversify without sacrificing financial flexibility. The company maintains one of the strongest balance sheets in the industry and has earned a AA credit rating from Standard & Poor's.

As a result, Chevron enjoys a low cost of capital to finance new projects and is able to prioritize returns to shareholders. Chevron has raised its dividend 7% each year on average over the last twenty years, all the while plowing tens of billions of dollars back into new production.

In contrast, startup energy producers find themselves in precarious financial positions from the outset due to lack of scale, diversification, and reputation. Often, these new, speculative energy enterprises wind up in bankruptcy.

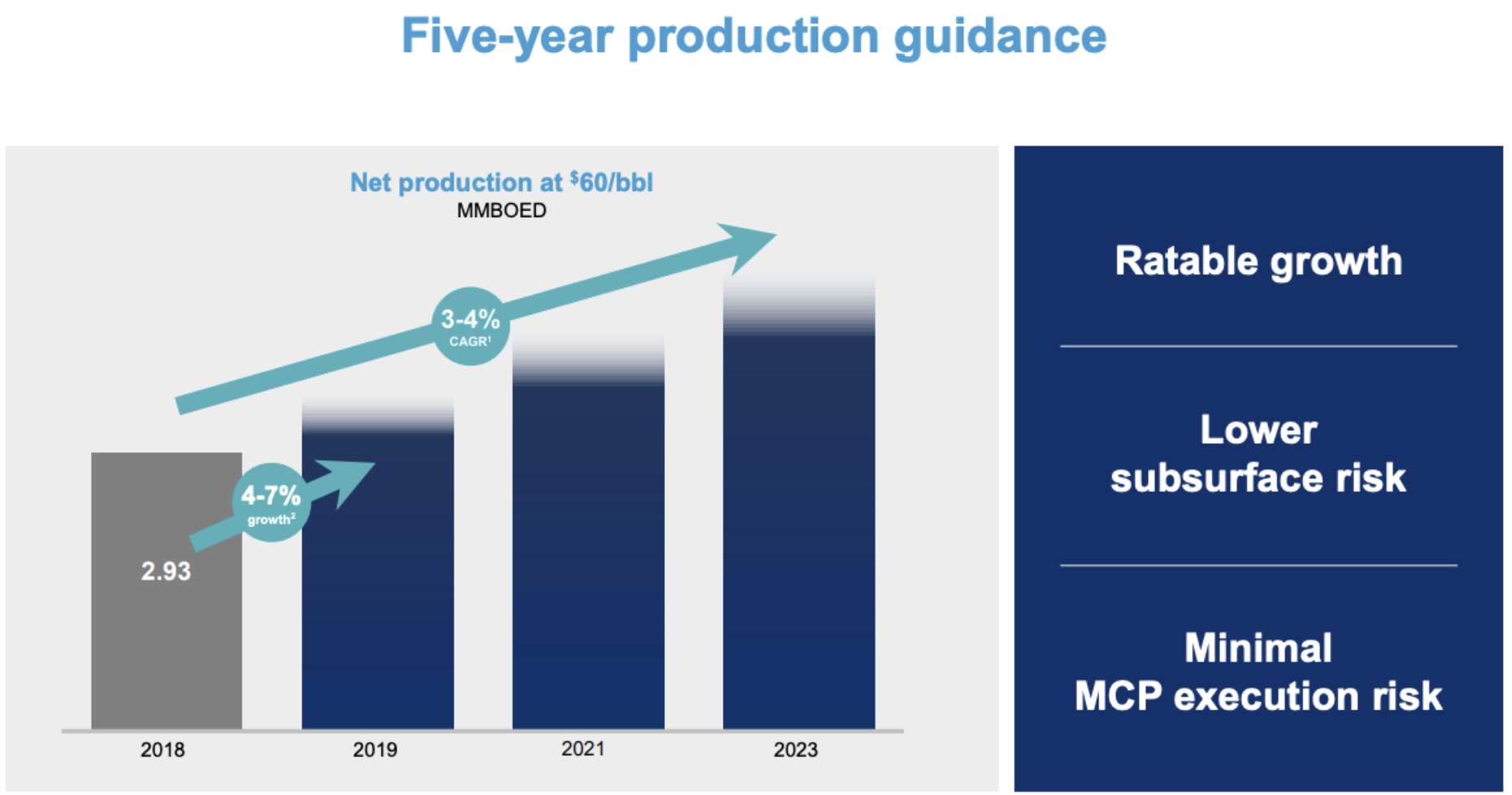

Going forward, Chevron is planning to spend about $20 billion annually to replenish oil wells, expand production further, and ultimately grow total production about 20% over the next five years.

Source: Chevron Investor Presentation

Investments in the Permian basin (home of the U.S. shale boom) are expected to drive much of Chevron's growth, though Chevron isn't betting solely on the future of U.S. shale.

New facilities in Australia are processing liquefied natural gas (LNG) destined for fast-growing Asian economies like China, where demand for a cleaner energy source than coal is expected to rise substantially in the coming decades.

LNG makes up only 13% of the firm's total production today, but as a more easily-transportable form of natural gas that can be shipped overseas, LNG is expected to contribute meaningfully to Chevron's growth in the years ahead.

Overall, Chevron's investments, scale, diversified portfolio, vertical integration, and strong financial position should enable the firm to remain a powerhouse in the energy industry and continue paying a safe, growing dividend.

That said, investors should consider several risks before jumping in.

Key Risks All oil giants are exposed to several risks, starting with a dependence on selling commodity products whose prices can crash in a hurry with no warning.

The price of oil plunged 70% in less than eight months during the financial crisis, for example. The oil crash in 2014 saw prices cut in half in a few months. And from October 2018 through December 2018, crude tumbled 45%.

Naturally, share prices of oil producers followed suit. Chevron and other industry stalwarts were financially-sound enough to weather these storms, but investors still needed to have strong stomachs to endure these unpredictable bouts of volatility.

Wild rides aside, Chevron's size is a double-edged sword. While the firm's scale gives it a leg up over competitors, it also makes incremental growth challenging. Since oil and gas wells deplete over time, billions must be invested annually to discover or acquire new wells in order to replace existing reserves.

Indeed, Chevron's output has mostly stagnated over the past two decades at a little under 3 million barrels of oil per day, which raises the question of whether management's growth plans are somewhat ambitious.

Perhaps Chevron's growth challenges are best illustrated by the firm's presence in Venezuela and Africa, troubled parts of the world that a multinational oil producer might pass on if not for the need to extract every drop of oil available.

Even if management is able to deliver on its promises, the oil industry faces a wide spectrum of possible futures in the next several decades.

In one future, the demand for oil and gas will continue to march upward as the global population rises and standards of living improve, especially in developing nations. This is the story on which Chevron's management team is basing plans.

But in a different future, renewable energy sources become economically viable — or are otherwise embraced in a effort to curb carbon emissions — and replace much of the demand for oil, drying up Chevron's profits.

For now, the world's energy mix seems likely to remain diverse with fossil fuels as the most abundant, cost-effective source, at least for the foreseeable future.

And while changes in the global energy landscape play out, Chevron has the financial strength to withstand short-term volatility in commodity prices, make large investments as needed, and continue to pay a safe, growing dividend.

Closing Thoughts on Chevron Every time a company announces a dividend raise, management is making a promise to investors it expects to keep. That's why the oil and gas industry, with its wild swings in revenue and profits, is generally not conducive to reliable dividends.

Yet from 25 barrels of oil produced per day at its first well in California to 3 million barrels per day extracted at sights around the world, Chevron has withstood the test of time. The firm's scale, financial strength, and disciplined management have combined to crown Chevron as one of the few dividend aristocrats in the energy sector.

While there's uncertainty in what lies ahead for fossil fuels, Chevron has proven itself capable of overcoming many challenges in its long history. So long as any shift from fossil fuels to renewable energy is gradual, Chevron has ample resources to adapt.

All said, Chevron may be a good choice for income investors who are comfortable with the energy sector's unpredictable volatility and long-term outlook.