ADP: One of the Fastest-Growing Dividend Aristocrats

Automatic Data Processing (ADP) was founded in 1949 and is one of the largest providers of human capital management (HCM) solutions in the world. ADP offers a wide range of cloud-based software solutions and services, which companies use to pay, recruit, staff, manage, and retain employees.

Over 40 million people around the globe depend on ADP for accurate pay, reliable benefits administration, effective performance management, or other human resource services.

The company generates most of its revenue on a recurring basis from providing payroll services (handles the preparation of employee paychecks, pay statements, journals, and summaries), including paying 1 out of every 6 workers in the U.S., but has expanded its suite of products over the last decade to cover most of the HCM spectrum.

The HR Business Process Outsourcing market has been a major focus. In this market, ADP offers fully integrated outsourcing solutions that enable companies to outsource their HR, time and attendance management, payroll, and benefits administration functions to ADP.

Overall, ADP provides solutions to more than 740,000 clients in over 110 countries and territories. The company's clients range from single-employee companies to some of the world’s largest enterprises. In fact, over 80% of Fortune 100 companies use at least one ADP service. No client accounts for more than 2% of total revenue.

ADP organizes its business into two segments:

Employer Services (72% of revenue; 86% of earnings): provides a wide range of business outsourcing and technology-enabled HCM solutions, including payroll services, benefits administration, recruiting and talent management, HR management, insurance services, retirement services, and compliance solutions.

Professional Employer Organization Services (28% of revenue; 14% of earnings): provides employment administration outsourcing solutions through a relationship in which employees who work for a client are co-employed by ADP and the client. ADP also helps small and mid-sized businesses with HR management and employee benefits functions. Such employees enjoy ADP's 401(k) and other benefits, which the client pays for but at lower rates ADP is able to negotiate (say with health insurance companies) due to its scale.

By geography, approximately 86% of ADP’s sales are generated in the U.S., 9% in Europe, 2% in Canada, and 2% in other countries.

Automatic Data has raised its dividend 44 consecutive years, making it a dividend aristocrat and putting it on track to become a dividend king in 2025.

Business Analysis

ADP’s primary competitive advantages are derived from its scale and long-standing customer relationships.

The company has the most complete suite of products and services in the HCM market and is over twice as large as its closest pure-play HCM competitor. ADP also boasts the broadest market coverage by geography and client size. In fact, ADP services more than 110 countries and covers 99% of multinational employees.

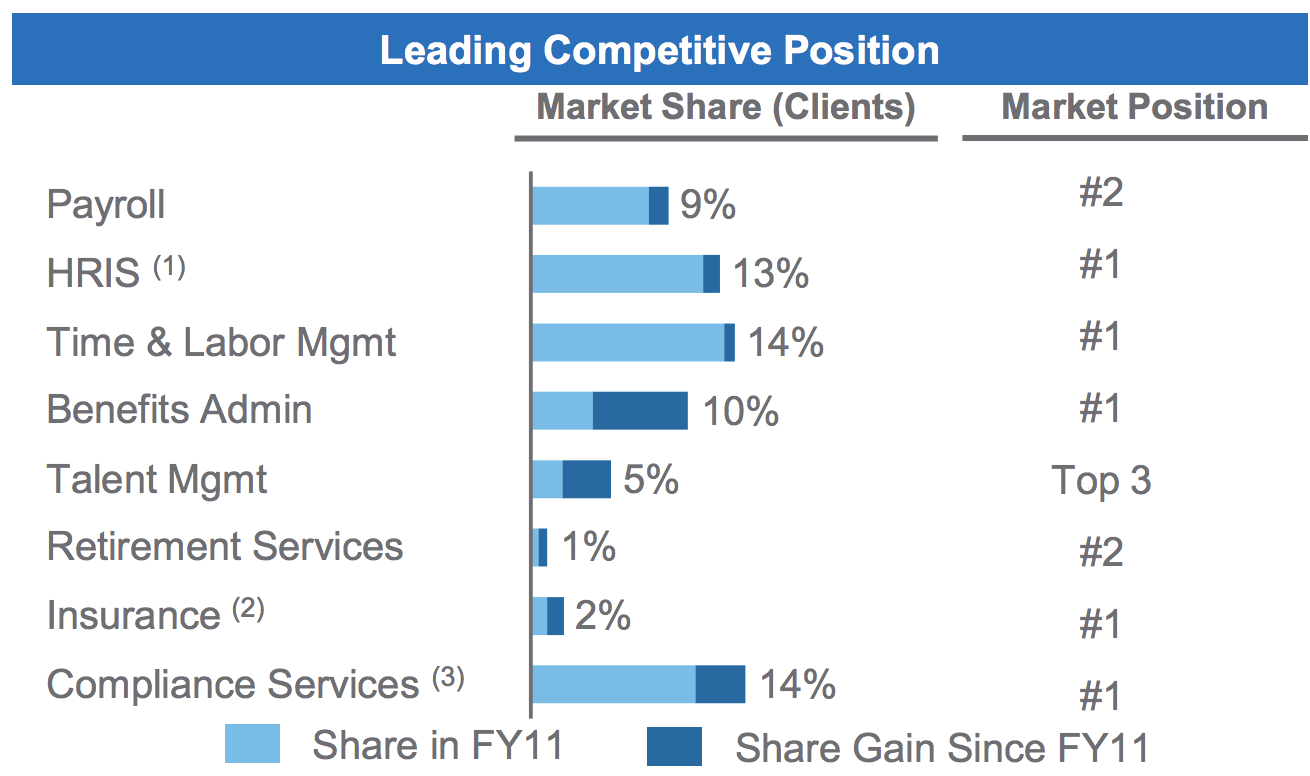

As a result of its scope, ADP can offer a more complete suite of cloud-based HCM solutions to expand its existing client relationships, which has helped it gain client share across every major category of the HCM market from fiscal year 2011 through 2017 (latest data available).

Source: ADP Investor Presentation

ADP is also uniquely positioned to serve larger clients with operations spread around the world. This is no small task thanks to the different regulations, languages, and integration issues from one country to the next.

With more than $13 billion in annual revenue and little capital required to run its business (capital expenditures average less than 1.5% of revenue), ADP has the luxury to reinvest heavily in the latest solutions and technology as well.

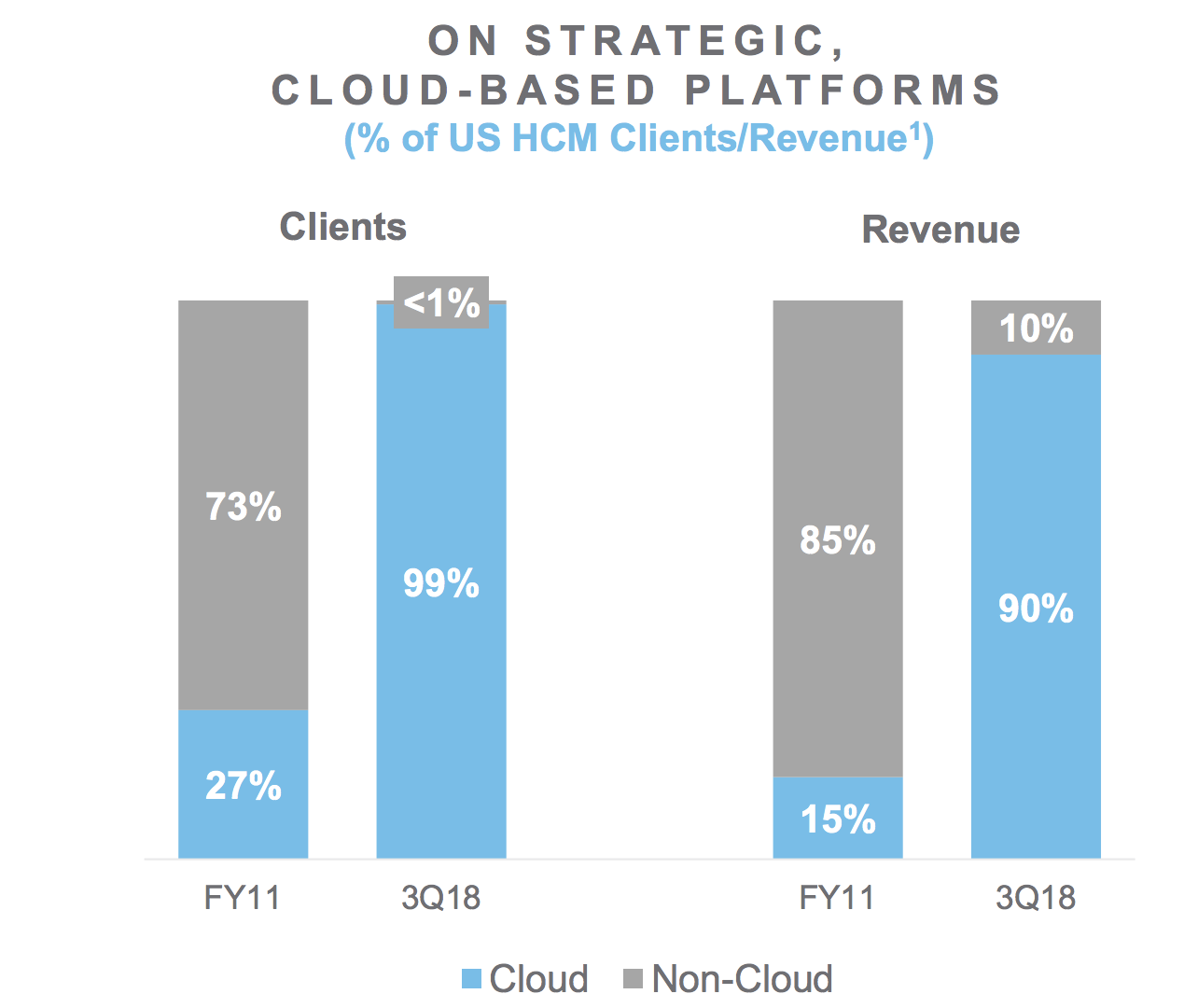

The company has spent several decades building out the depth and breadth of its solutions and invested approximately $1 billion in fiscal 2018 for systems development and programming to further improve its offerings.

These investments have helped the company transition nearly all of its HCM customers to cloud-based software (up from 27% in fiscal 2011) and get over 5 million people using its mobile app.

Source: ADP Investor Presentation

ADP can also acquire smaller companies with solutions or technologies it can use to further broaden its suite of HCM solutions to appeal to more customers. These include two recent bolt-on acquisitions:

Workmarket in early 2018 for $125 million, a leading provider of cloud-based freelance management solutions (to help ADP better serve the gig economy)

Global Cash Card in October 2017 for $490 million (a fast-growing digital payment processor)

As ADP becomes more ingrained with clients, switching costs rise because users are trained to use more of ADP’s software solutions.

Additional switching costs are created by many of the challenges ADP solves for clients. ADP manages complex regulatory environments for many businesses to make sure they remain compliant with the law.

ADP handles employment taxes, tax credits, unemployment claims, workers compensation, and healthcare reform issues. Its clients must comply with each regulation to remain in business and avoid fees, increasing their dependence on ADP’s expertise and ability to manage complex transactions.

Over the years, ADP has established a relationship built on trust and reliability with clients. After all, ADP handles some of the most sensitive information about its clients’ employees (tax statements, social security numbers, healthcare information, etc.).

Building up the necessary security systems and technology infrastructure to safeguard this data takes many years of heavy investments, but winning clients’ trust takes even more time.

As a result, ADP's overall client retention rate has remained above 90% every year since fiscal 2011. Client retention is estimated at approximately 10 years in Employer Services and 7 years in Professional Employer Organization Services, highlighting the important role ADP plays for its clients.

Long-lasting relationships with hundreds of thousands of businesses have provided another advantage that will likely become increasingly important over the coming years – big data analytics.

Big data is transforming virtually every industry today, and human capital management is no exception. Companies are constantly looking for ways to better identify talent, hire the right people, retain them for longer, and make them more productive.

ADP has more employee records than all of its competitors, providing it with a treasure trove of data that can be used for more detailed and insightful benchmarking for clients.

Management is also opening up the company’s platforms via APIs to add further value for clients. This action allows clients to integrate ADP’s HCM platforms with the rest of their enterprise suite. Third-party developers can also create applications that exchange data with ADP’s core HCM systems to further improve productivity and gain new insights.

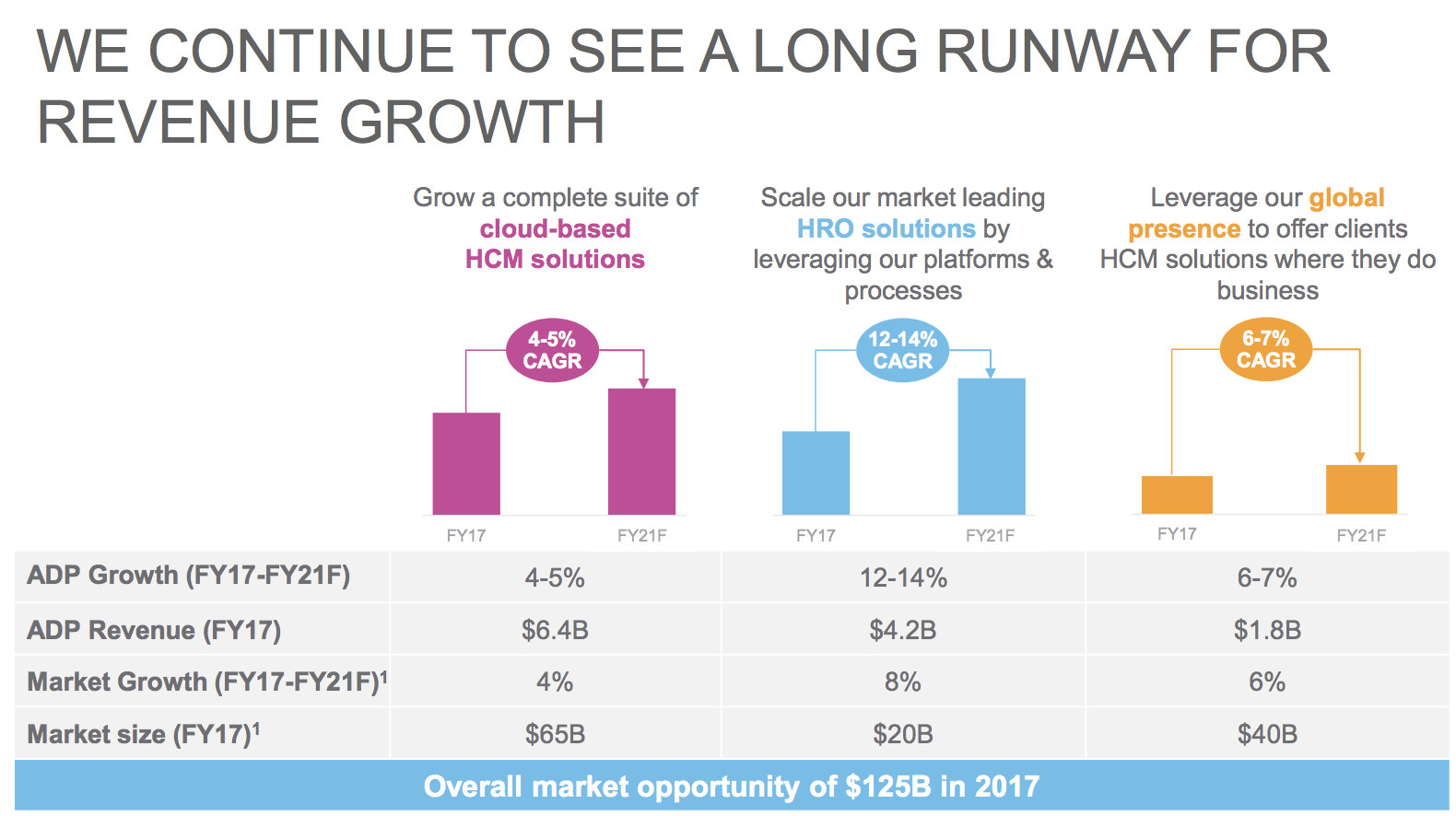

While data and analytics could further solidify ADP’s market position and provide new growth opportunities, the HCM market is still attractive as it stands today. The market is estimated to be over $125 billion in size, which gives ADP a market share close to 10%.

The fragmented HCM market is also growing around 5% annually, providing plenty of opportunity for ADP’s sales team of more than 5,000 employees to continue expanding the company.

Management is especially optimistic about its Professional Employer Organization Services segment. ADP believes this business could gain an additional 25 million to 30 million new clients, just from upselling its existing customer base. This is why the firm believes that it can grow this segment by 12% to 14% annually over the long term.

Source: ADP Investor Presentation

Meanwhile, the global market, which the company has barely tapped into despite operating internationally for over 40 years, is $40 billion in size and growing at about 6% per year. Management believes international expansion can help ADP continue driving solid company growth for the foreseeable future.

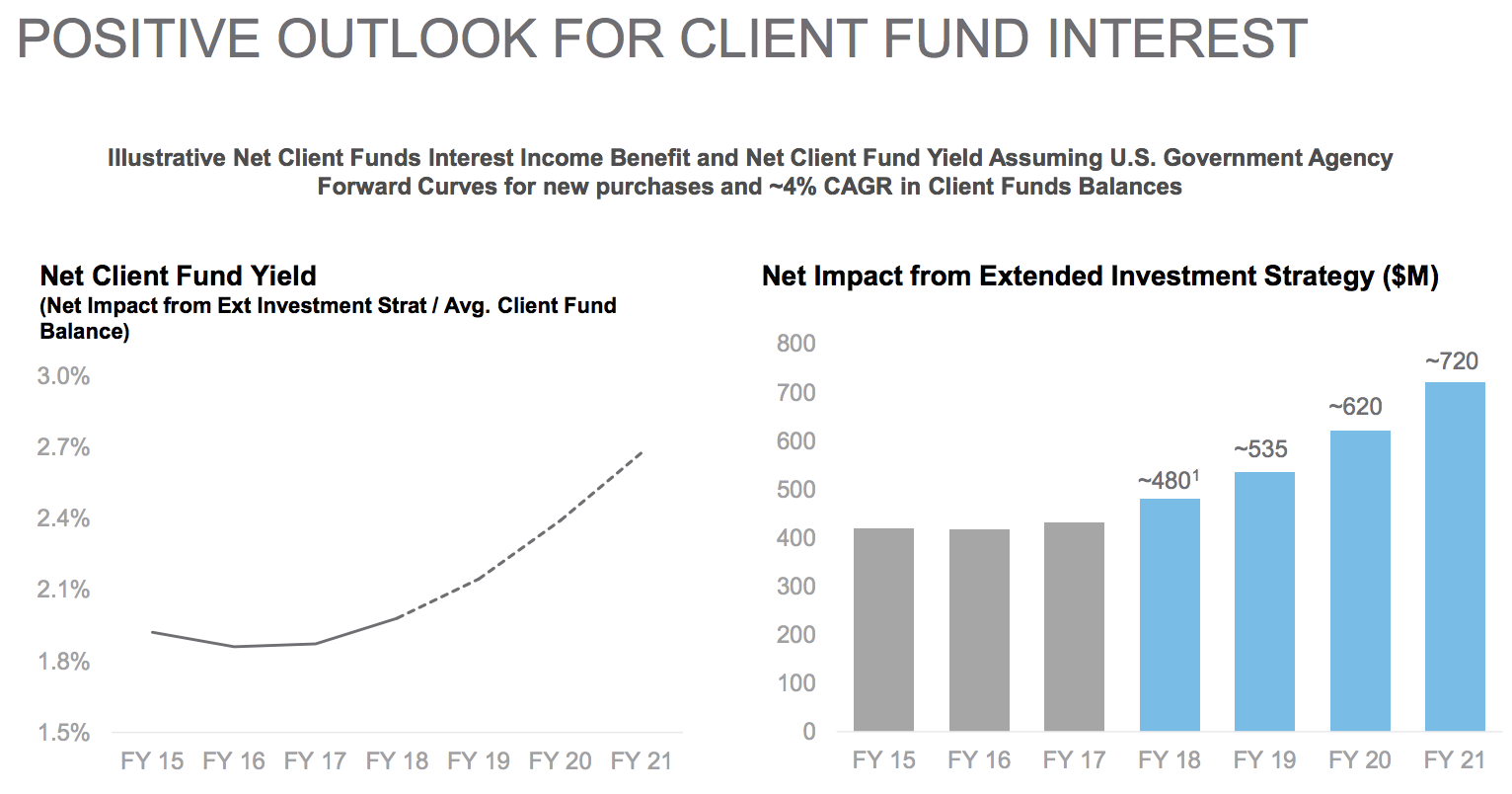

A final unique element about ADP’s business is its holding of client funds. ADP holds over $22 billion of client funds that are primarily used to pay clients’ employees as part of ADP’s payroll processing services.

ADP invests these funds (the equivalent of insurance company float) predominantly in AAA/AA-rated fixed-income securities to earn interest income until the funds need to be paid out. Declining interest rates have limited the amount of high-margin interest income ADP can earn. If short- and intermediate-term interest rates rise, ADP should enjoy a moderate boost to earnings growth.

You can see this in the past year when a 0.3% increase in average yield on these funds resulted in net earnings from this portfolio jumping 13%. And should long-term yields rise over time (even to historically low levels like 2.7%) ADP estimates it could nearly double the net profit from its client fund portfolio. If that were to happen, ADP's total operating income would increase by around 10% to 15%.

Source: ADP Investor Presentation

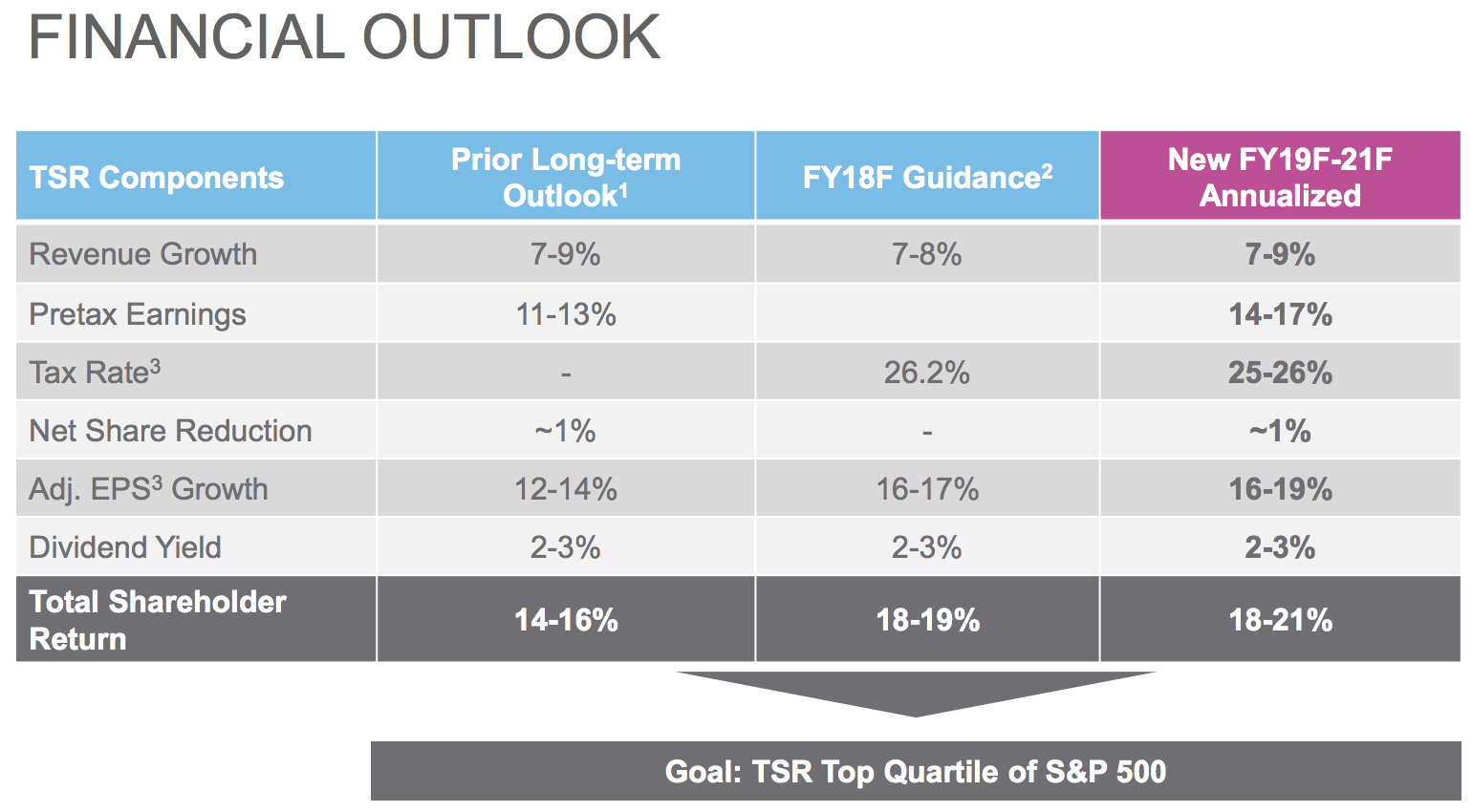

Even without higher interest rates, management believes the company's strategic plans can deliver double-digit annual earnings per share growth from fiscal 2019 through 2021, which would continue fueling strong dividend increases in the years ahead.

Source: ADP Investor Presentation

If management can deliver on its long-term earnings growth, then the company should not only be able to easily continue its impressive dividend growth streak (12% average annual dividend growth over the past 20 years), but also offer some of the fastest payout growth of any dividend aristocrat.

But how realistic is management's growth guidance? ADP has delivered about 11% annual earnings growth over the past 12 years, and a key part of the company's expected acceleration comes from improving profitability.

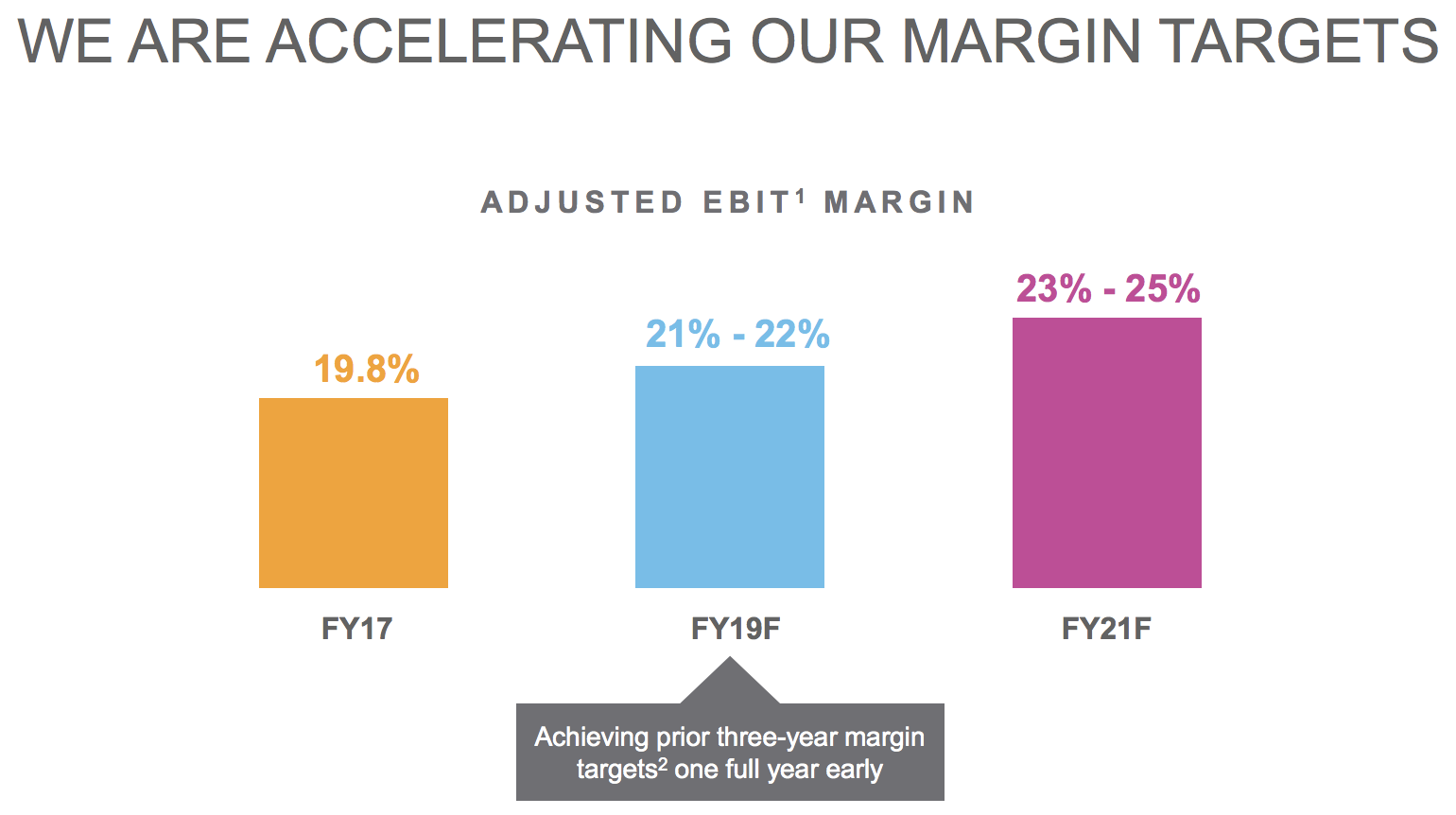

That's thanks to ADP's strong and growing economies of scale, which in 2018 helped the company to achieve its long-term EBIT (earnings before interest and taxes) guidance growth a year earlier than expected and raise its long-term profitability forecast.

Source: ADP Investor Presentation

ADP exceeded its margin guidance faster then expected thanks to the successful integration of previous IT platforms (from earlier bolt-on acquisitions) which allowed it to stop serving legacy infrastructure that is now redundant. The firm also instituted an early retirement program for employees which helped it decrease headcount, without sacrificing customer service quality (due to the improved software platforms its using).

The company achieved 7% bookings growth (new business) in 2018 as well, keeping it on track to deliver 7% to 9% annual revenue growth as management expects. With relatively low incremental costs, a rising revenue base, and a solid track record, ADP's margin improvement plan appears reasonable.

Overall, Automatic Data Processing appears to be a well-positioned business with numerous strengths. The company provides mission-critical services, is a trusted partner with clients, requires little capital, enjoys high recurring revenue and client retention, and has a long runway for growth in a large and fragmented market.

Key Risks

It’s difficult to identify many risks that could impair ADP’s long-term earnings power. The company’s continual investments in programming and people help it maintain its leading market position.

However, new entrants are always looking for ways to deliver a similar quality of service at a lower price and in a more user-friendly format. As the pace of technology advancements accelerates, this could become increasingly true.

Zenefits, which gives away free software that automates payroll and health insurance for small businesses, has been the big name mentioned as a potential disruptor in the space (the startup launched in April 2013 and was valued as much as $4.5 billion). However, the company has hit a wall of challenges that have severely disrupted its growth path.

But ADP has seen some customer losses to Ultimate Software and Workday, also new industry entrants, who are targeting enterprise clients with over 1,000 employees. This highlights that, while ADP has a relatively wide moat among corporate giants now, management will need to remain nimble with upgrading its service offerings if the firm is to retain market share and keep retention at historically high levels.

Technology advancements could also make it easier for new entrants to try and disrupt the industry’s pricing structure. However, given clients’ need to make sure their businesses remain 100% compliant and fully functional, any such change seems likely to be gradual.

ADP has the resources to remain relevant, too – either by building or buying the technology or capabilities it needs to maintain its dominant market positions. The company also has something very important that new entrants lack – trust (many of its customer relationships span decades).

Changing laws and regulations could also pose a challenge, especially if the Affordable Care Act is ultimately repealed (which looks unlikely though the Department of Justice is suing to do just that). After all, ADP primarily makes money because its clients do not want to internally deal with complex tasks that don’t add direct value to their businesses.

While there is not much ADP can do to combat this risk, the company has increasingly diversified its business across an entire suite of HCM solutions, which helps reduce the risk of any single product line causing the firm to miss its long-term guidance.

Closing Thoughts on Automatic Data Processing

Automatic Data Processing appears to be a very high-quality company with an impressive track record of paying higher dividends for more than 40 consecutive years.

Few companies have a more dependable business model and dividend growth track record than ADP, and the future continues to look bright thanks to the large and highly fragmented nature of the HCM market.

With the potential to continue delivering double-digit earnings and dividend growth for the foreseeable future, ADP is one of the fastest-growing dividend aristocrats and should be considered by long-term investors at the right price.