Waste Management: the Largest Player in the Slow-Changing Trash Collection Industry

Founded in 1968, Waste Management (WM) owns the largest network of recycling facilities, transfer stations, landfills, and processing plants in North America. The company makes money by entering into contracts with customers to collect, transport, process, store, and dispose of their waste.

In just 30 years of operation, the company has built an impressive and diverse base of more than 22 million customers spread across municipal, residential, commercial and industrial segments in the U.S. and Canada.

During 2018, WM’s biggest customer represented just 1% of its annual revenues. The public sector (municipal customers) accounts for 21% of the firm's revenue, and the largest private industries are retail and offices at 10% each.

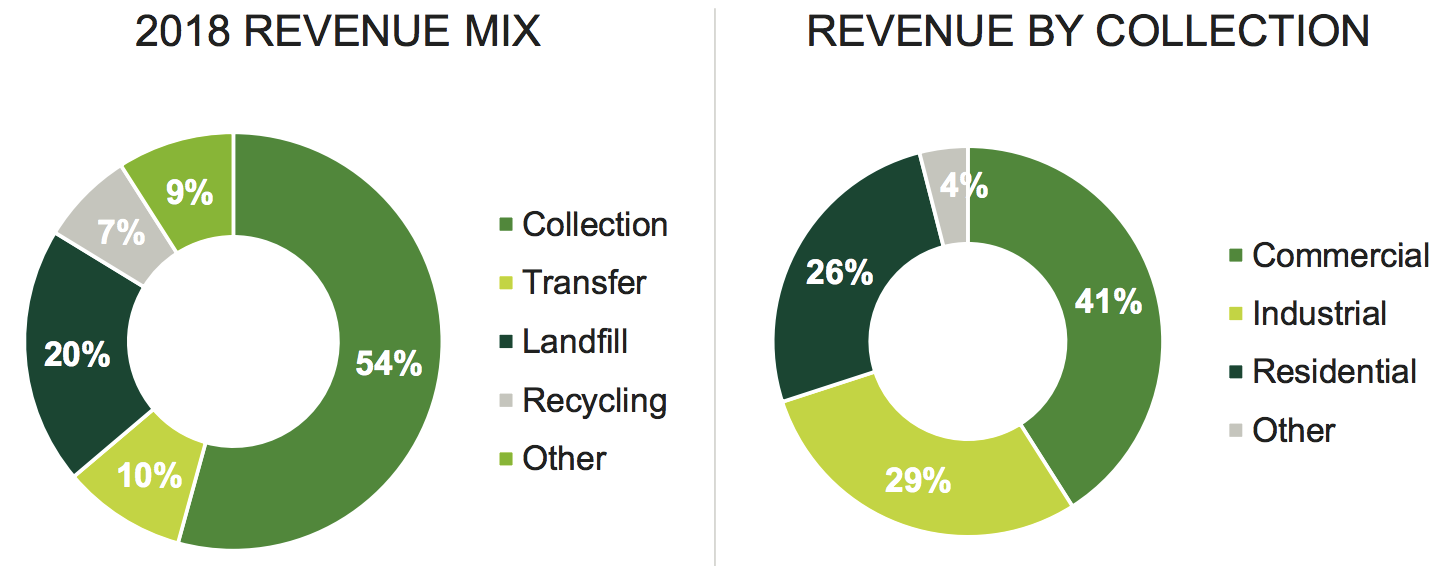

Waste Management’s revenues can be segregated into collection (54% of 2018 revenues), landfill (20%), transfer (10%), recycling (7%) and other services (9%). Commercial is the largest segment accounting for 41% of collection revenues, followed by industrial (29%), residential (26%), and other (4%) segments.

Source: Waste Management Investor Presentation

The commercial and industrial businesses are more lucrative customers for Waste Management because they typically have multi-year contracts in place, making cash flows more predictable and stable.

Waste Management has paid higher dividends every year since going public in 2004.

Business Analysis

The trash collection business might look easy, but it actually has substantial barriers to entry. As the largest player in the market, Waste Management also carries several additional advantages.

First, there just aren’t any viable alternatives to trash disposal today. Consumers and businesses alike need to have their garbage collected and taken off-site. With the average American generating a couple pounds of trash each day, there is a constant need for Waste Management’s services.

But why does Waste Management have such a strong market position? This is when the company’s valuable, hard-to-replicate network of assets comes into play.

Waste that is not recycled or processed into forms of energy is taken to transfer stations, which consolidate waste into larger, long distance trucks. These trucks then take the waste to disposal facilities and landfills that are usually located somewhat far away.

Waste Management owns over 280 landfills, about as many as its next two largest competitors combined. The number of landfills has fallen from over 7,600 in the mid-1980s to about 2,500 today. That’s over a 65% decrease in less than 30 years!

Government regulations, neighborhood restrictions, high start-up costs, and environmental concerns have all played a factor in the decline of available landfills.

While the remaining landfills are larger and more efficient than their predecessors, there are only so many places that waste management companies can park trash. As a result, Waste Management’s competitors must pay the company a “tipping fee” to deposit waste at its landfills and use its transfer stations.

Waste Management’s ownership of key assets, dense trash collection network, and tipping fees allow it to maintain a lower cost profile than its peers. The company then attracts more waste volume from customers, which results in greater route density and higher returns on its invested capital compared to peers.

In addition to the toll-taking advantage Waste Management has at its landfills, new entrants also have a challenging time winning enough business to justify the significant investment needed to construct for their own disposal facilities.

Waste Management and other players already have contracts with customers, which typically last anywhere from two to seven years. In fact, the company has noted that more than 80% of its commercial and industrial customers have a contract length greater than three years, and the typical customer stays with Waste Management for 10 years.

New entrants have a difficult time securing the cash flow streams necessary to build their own trash disposal network, especially since they cannot compete on price.

Furthermore, Waste Management’s large network of recycling facilities, transfer stations, and landfills make its business more flexible to meet the needs of virtually any customer segment – municipalities, construction sites, healthcare facilities, commercial buildings, and many others. Generally speaking, customers prefer to contract with proven operators that can meet a variety of needs.

While Waste Management might look like a mundane business in a commodity industry, this is good from a long-term investment perspective since the company’s business model is less prone to technology disruption and possesses several hard-to-replicate advantages.

Key Risks

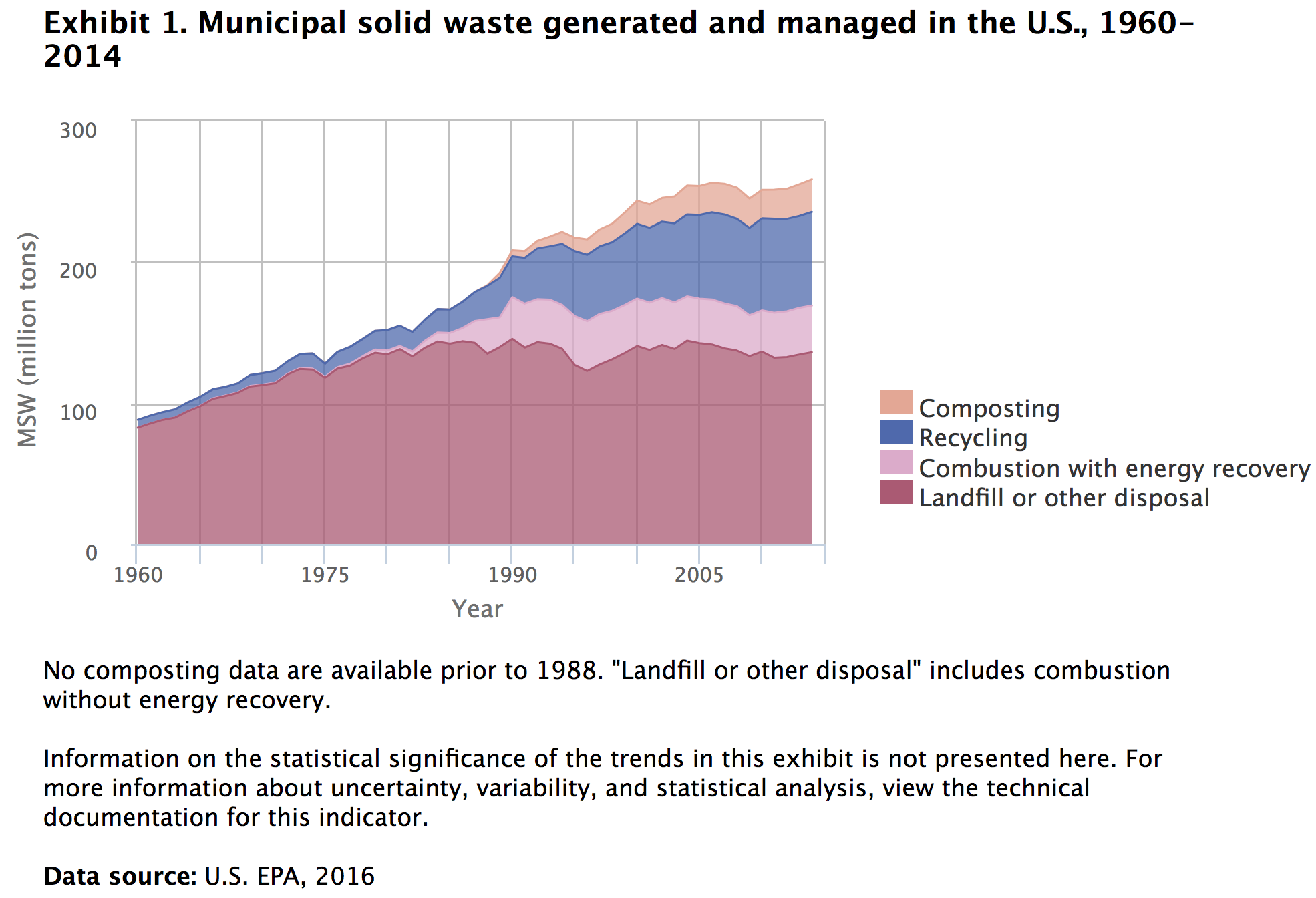

Rising environmental concerns and customer consciousness have increasingly diverted waste to other alternatives such as recycling and composting.

You can see that municipal solid waste generation has noticeably slowed in growth over the last decade and declined slightly on a per capita basis.

Source: EPA

Today customers are clearly more aware and working towards reducing the amount of waste they generate. Large customers such as grocery stores and restaurants are choosing to divert their organic waste from landfills to other alternatives, for example.

With increasing awareness about recycling, product packaging has also become more efficient these days. People are going green and paperless which has cut down a lot of paper waste.

All these in turn reduce the waste that needs to be collected, processed, and stored in landfills by Waste Management. You can see that solid waste going to landfills is down slightly from 1990 while recycling and composting have experienced strong growth.

Importantly, Waste Management is the largest residential recycler in North America and has the financial firepower to invest in whatever operations are needed to maintain its moat. The company is also a leading renewable energy provider.

If anything, the (slowly) increasing shift towards recycling and renewables could further strengthen the market positions of the biggest players because smaller competitors are unable to make the vertical integration investments needed to compete. Whether or not these activities will be equally profitable is another question, but Waste Management should find a way to stay relevant with its scale and collection of assets.

Besides the ongoing shift to more recycling, Waste Management’s business can be impacted by reduced levels of consumption that result from lower economic activity. When economic activity slows, less trash is produced by consumers and businesses, so Waste Management is not as busy. However, its trucks still run their routes and incur the same operating costs, somewhat crimping profitability.

Overall, the company's management team seems likely to remain conservative with how they run the business and adapt it to meet evolving waste management trends. Although the industry remains fiercely competitive, Waste Management is in a position of strength thanks to its leading market share, superior technology, and economies of scale. The business should benefit from continued industry consolidation and any improvement in economic activity.

Closing Thoughts on Waste Management

Waste Management has a Teflon-coated business model in an industry which is almost immune to economic cycles.

As the industry’s largest player, the company possesses strong operational and technical capabilities with economies of scale that result in significant advantages over its competitors.

From its dense network of well-placed assets to its annuity-like revenues (the average commercial and industrial customer stays with WM for 10+ years) and ownership of increasingly scarce landfills, Waste Management is a business built to last.

Thanks to its defensive profile, excellent free cash flow generation, investment grade credit rating, and wide moat, the company seems very likely to continue growing its dividend at a healthy clip going forward, something Waste Management has done every year since 2004.