Oxy's Dividend Should Continue Being Restored as Balance Sheet Strengthens

Occidental Petroleum (OXY) has used the strong oil price environment to pay down nearly half of the debt it took on in 2019 to fund its pricey, ill-timed acquisition of independent oil and gas producer Anadarko.

With net debt falling from about $35 billion nearly two years ago to an expected $20 billion this quarter, we now expect Oxy's leverage ratio to remain at a reasonable level even at an oil price of $50 or $60 per barrel.

Management intends to continue using free cash flow to deleverage the business until Oxy's net debt falls closer to $15 billion. At that time, the BB+ rated shale oil producer hopes to regain an investment grade credit rating.

In recognition of Oxy's debt reduction progress, we are upgrading the company's Dividend Safety Score to Borderline Safe.

A shrinking debt balance reduces Oxy's interest costs, frees up more cash flow for share repurchases, and provides more financial flexibility during periods of weak energy prices.

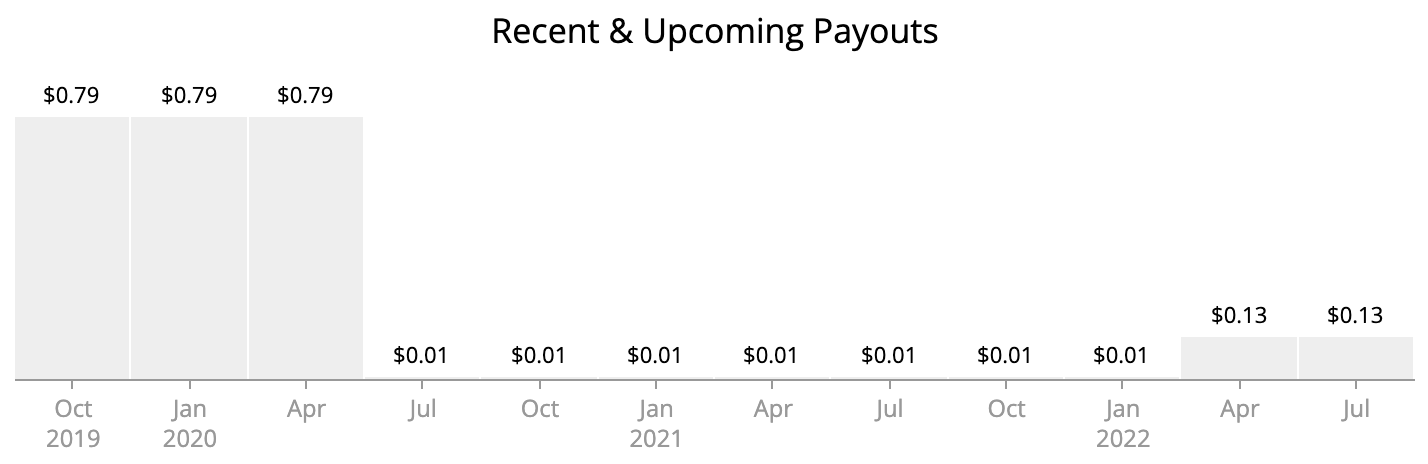

All of these qualities bode well for income investors. After slashing its dividend by 99% in March 2020 when the cratering price of oil stressed Oxy's stretched balance sheet, the company held its token dividend flat until bumping it up earlier this year.

Source: Simply Safe Dividends

Oxy's payout remains well below its pre-pandemic level but should continue being restored, albeit at a "moderate" pace, according to management.

Oxy wants to maintain a dividend that is sustainable over a full cycle, and part of that plan includes keeping its breakeven price – the price of oil necessary to fund sustaining capital expenditures and the dividend – around $40 per barrel.

Based on Oxy's historical payout ratio levels and assuming oil prices eventually retreat closer to $50 a barrel, we could see the company's quarterly dividend gradually rising from 13 cents per share to as much as 50 or 60 cents.

That would push Oxy's dividend yield closer to 3.5% based on the stock's current price, but management may take a conservative approach towards dividend growth given Oxy's desire to continue paying down debt.

Regardless, Oxy has made solid progress getting its financial house back in order after a tumultuous and uncharacteristic period for the company. Prior to its 2020 dividend cut, Oxy had paid uninterrupted dividends since 1991, reflecting management's historical conservatism.

Looking ahead, Oxy's performance will remain driven by the Permian Basin, which is the largest shale oil producing formation in America and accounts for nearly half of Oxy's total output.

With more acres of land in the Permian than any other oil company, Oxy's vast, low-cost inventory should support profitable growth for the foreseeable future.

Income investors considering the stock just need to remain patient for larger dividends as Oxy balances free cash flow deployment between debt reduction, share repurchases, and moderate payout increases.