Warren Buffett's Dividend Portfolio

Warren Buffett’s Berkshire Hathaway outperformed the S&P 500 by 9.5% per year from 1965 through 2024, generating an overall gain of 5,502,284% compared to the market’s total return of 39,054%.

It’s no wonder why investors closely monitor Warren Buffett’s portfolio. He is arguably the greatest investor of all time, and he has doled out some of the best investment advice over the years.

Here's a list of all the dividend stocks owned by Warren Buffett:

Over half of Berkshire's holdings pay a dividend, and several of them have yields near 4% or higher.

It’s no wonder why investors closely monitor Warren Buffett’s portfolio. He is arguably the greatest investor of all time, and he has doled out some of the best investment advice over the years.

Here's a list of all the dividend stocks owned by Warren Buffett:

Over half of Berkshire's holdings pay a dividend, and several of them have yields near 4% or higher.

A dividend is often the sign of a financially healthy and stable business that is committed to rewarding shareholders. These are some of the qualities Warren Buffett looks for when he invests.

Warren Buffett's Latest Notable Trades

With the strong bull market providing few whale-sized bargains, Berkshire has spent recent years retaining earnings and trimming positions. Cash now represents around 30% of the company's total assets.

Notably, Berkshire Hathaway has trimmed its stake in Apple (AAPL) by over two-thirds since the beginning of 2024. Despite these cuts, the iconic iPhone maker remains Berkshire's largest holding (roughly 23% of the portfolio).

In the fourth quarter of 2025, Warren Buffet also continued reducing his stakes in Bank of America (BAC), Amazon (AMZN), Aon (AON), and Pool Corp (POOL).

Berkshire did still do some buying, initiating a nearly 3% stake in the New York Times (NYT) and adding to positions in Domino's Pizza (DPZ), Chubb (CB), and Chevron (CVX).

New Positions

Notably, Berkshire Hathaway has trimmed its stake in Apple (AAPL) by over two-thirds since the beginning of 2024. Despite these cuts, the iconic iPhone maker remains Berkshire's largest holding (roughly 23% of the portfolio).

In the fourth quarter of 2025, Warren Buffet also continued reducing his stakes in Bank of America (BAC), Amazon (AMZN), Aon (AON), and Pool Corp (POOL).

Berkshire did still do some buying, initiating a nearly 3% stake in the New York Times (NYT) and adding to positions in Domino's Pizza (DPZ), Chubb (CB), and Chevron (CVX).

New Positions

- New York Times (NYT) – publishing

Added To

- Domino's Pizza (DPZ) – restaurants

- Chubb (CB) – property and casualty insurance

- Chevron (CVX) – integrated oil and gas

- Lamar (LAMR) – advertising REIT

Trimmed

- Amazon (AMZN) – e-commerce

- Liberty Braves (BATRK) – movies and entertainment

- Aon (AON) – insurance brokers

- Pool Corp (POOL) – distributors

- Bank of America (BAC) – diversified bank

- Liberty Latin America (LILA) – alternative carriers

- Apple (AAPL) – tech hardware and services

- Constellation Brands (STZ) – distillers and vintners

Five of Buffett's Highest-Yielding Stocks

Here's a look at some of the dividend stocks with the highest yields in Berkshire's portfolio.

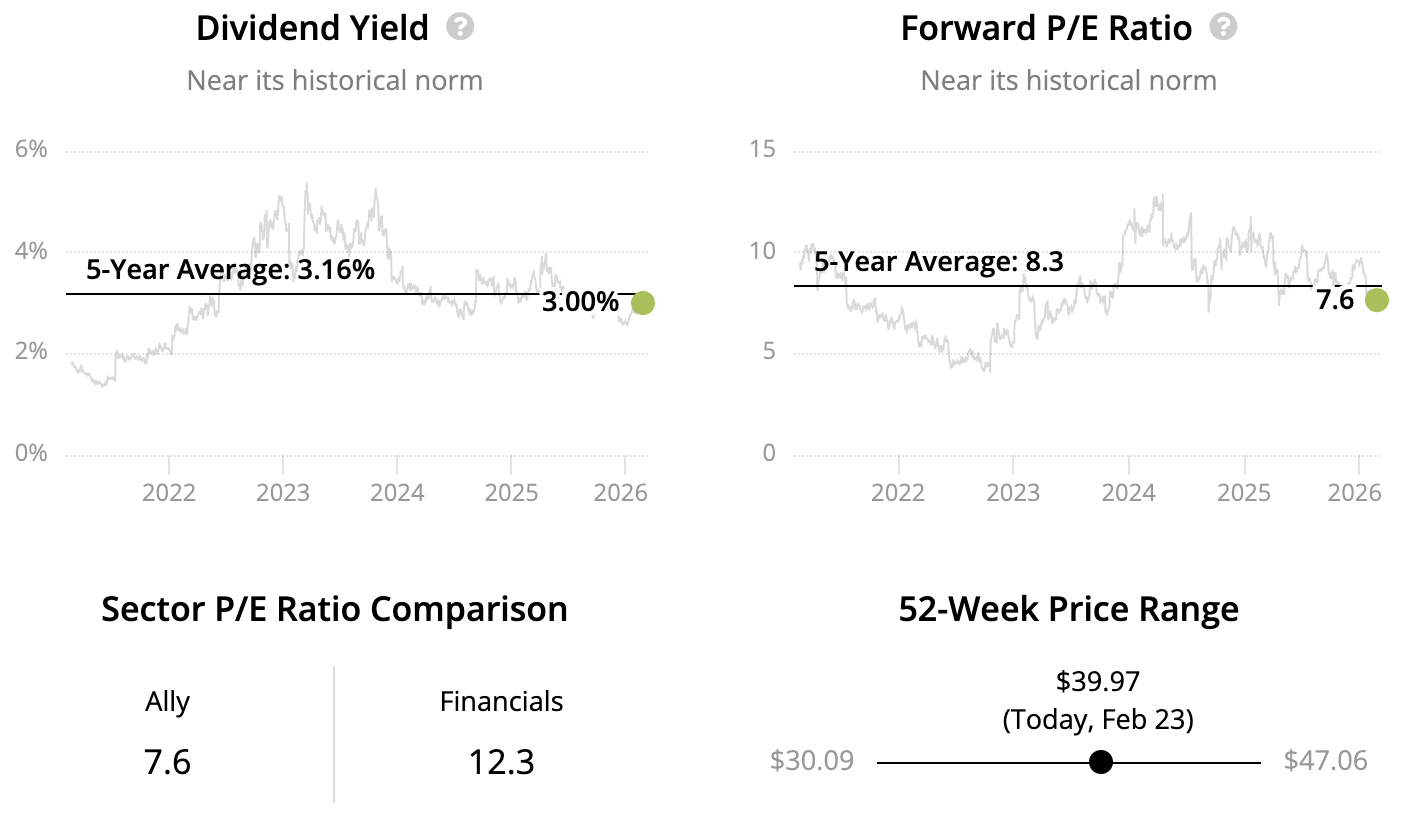

High-Yield Buffett Stock #1: Ally Financial

Sector: Financials – Consumer Finance

Dividend Growth Streak: 0 years

Dividend Safety Score: Borderline Safe

Dividend Yield: 3.0%

Berkshire has owned shares of Ally (ALLY) since the first quarter of 2022, making the financial services company approximately 0.5% of its portfolio.

Buffett has likely followed Ally for a long time as it was founded in 1919 by General Motors (another Berkshire holding) to provide financing to automotive customers.

Ally is still one of the largest car finance companies in America but has evolved to become a full spectrum provider of consumer and banking services as well.

Rising interest rates squeezed the BBB- rated bank's profitability shortly after Buffett's initial purchase. But he likely expects deposits to continue rising over the long run, fueling earnings growth as Ally invests these funds into loans and other interest-earning assets.

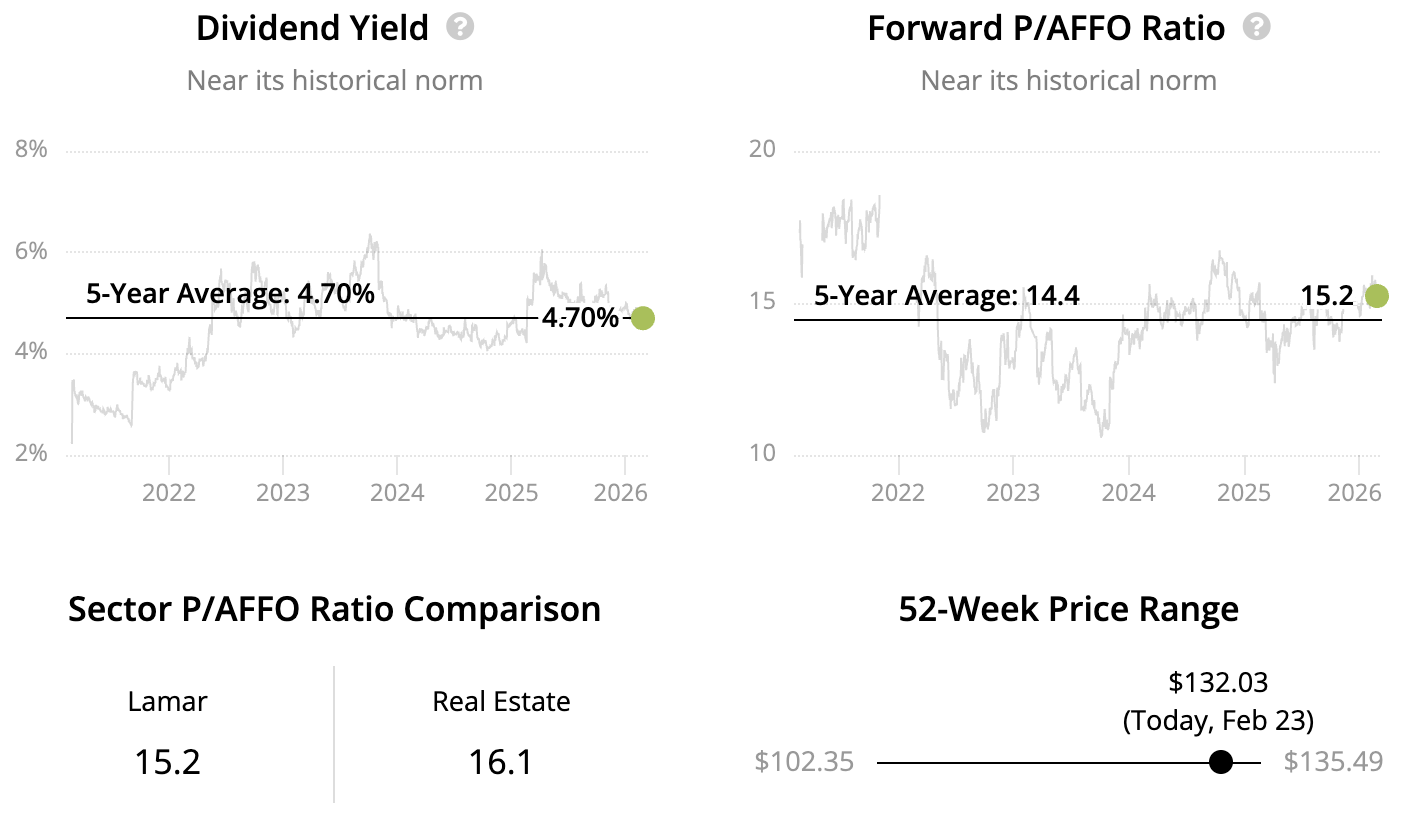

High-Yield Buffett Stock #2: Lamar

Sector: Real Estate – Other Specialized REITs

Dividend Growth Streak: 5 years

Dividend Safety Score: Borderline Safe

Dividend Yield: 4.7%

Berkshire Hathaway established a small position in Lamar (LAMR) in the second quarter of 2025.

Lamar controls one of the largest networks of billboard locations in North America, effectively owning scarce roadside real estate that is difficult to replicate because of zoning limits and permitting barriers. These constraints create durable, localized advantages and allow Lamar to generate recurring, rental-like revenue from advertisers.

Once a billboard is installed, maintenance needs are modest and cash flow can be highly predictable, giving the company an asset-heavy but steady model similar to other infrastructure-like businesses Buffett has favored over the years.

Advertising spending can ebb and flow with the economy, but Lamar has enhanced returns by converting more of its inventory to digital displays, increasing revenue per location without needing significant new land or structures.

The position is very small, but its durable assets and straightforward economics fit well within Buffett's traditional circle of competence.

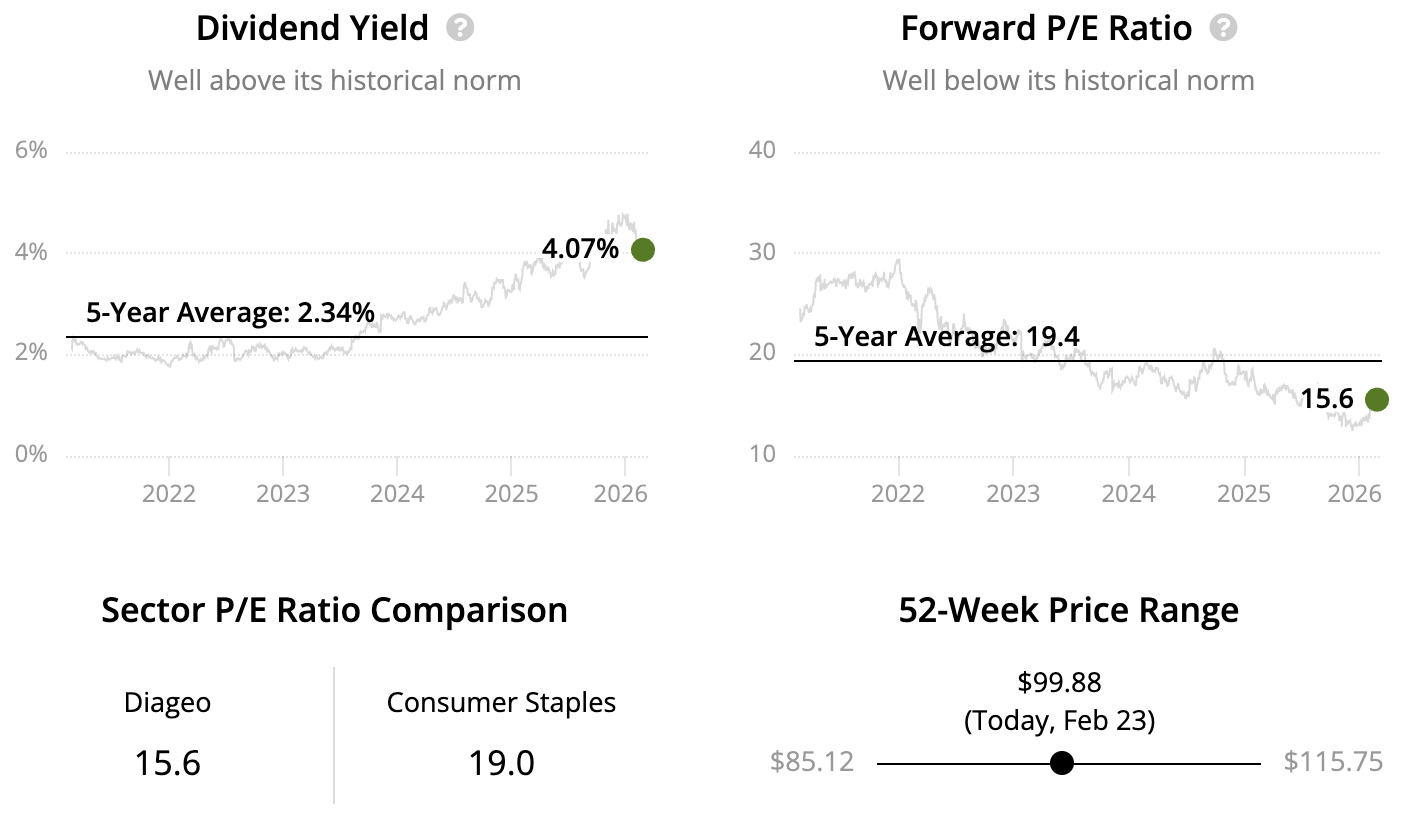

High-Yield Buffett Stock #3: Diageo

Sector: Consumer Staples – Distillers and Vintners

Dividend Growth Streak: 0 years

Dividend Safety Score: Very Safe

Dividend Yield: 4.1%

Warren Buffett initiated a small position in Diageo (DEO) in early 2023.

Diageo owns a collection of leading global spirits brands, including Johnnie Walker, Crown Royal, Smirnoff, and Guinness, many of which have been household names for generations.

These labels derive much of their value from reputation and customer loyalty rather than heavy ongoing capital investment, giving the business strong margins and consistent cash generation.

Alcohol consumption has historically been steady across economic cycles, and the industry's long-term shift toward premium products has historically allowed companies like Diageo to grow through pricing and mix rather than relying solely on higher volumes.

Berkshire's position is modest, but the company closely resembles the type of branded consumer franchise Buffett has favored throughout his career.

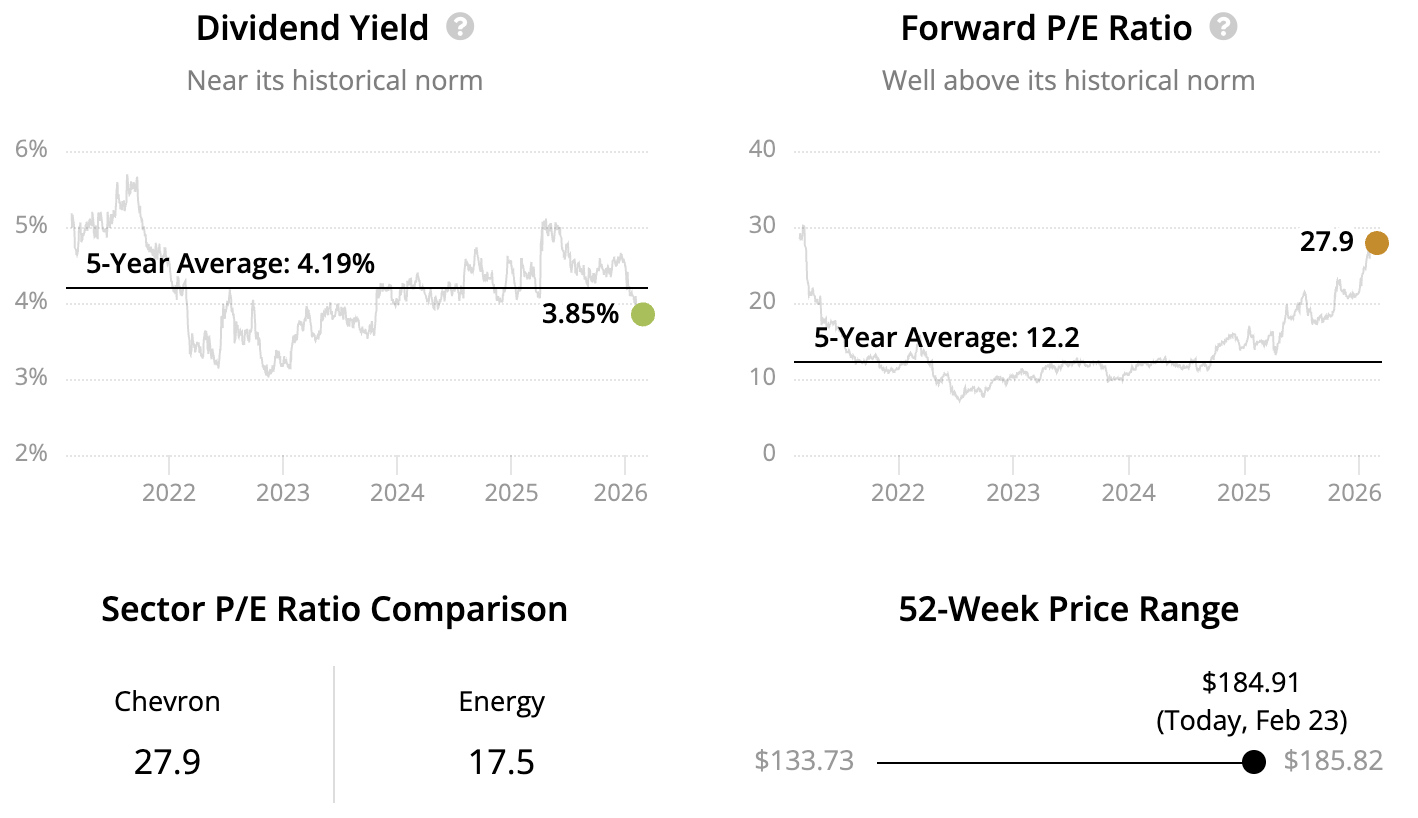

High-Yield Buffett Stock #4: Chevron

Sector: Energy – Integrated Oil and Gas

Dividend Growth Streak: 38 years

Dividend Safety Score: Very Safe

Dividend Yield: 3.9%

Buffett bought into Chevron (CVX) in late 2020 when the market was worried about the safety of dividends across the oil patch. Chevron's dividend yield was nearly twice as high back then, approaching 8%.

Energy demand has since boomed as the global economy rebounded from Covid lockdowns while supply has shown more restraint, contributing to today's inflationary environment while bolstering profits across the industry.

Chevron is one of the highest-quality companies in this space, with a pristine balance sheet and low breakeven oil price required to cover its capital expenditures and dividend. The stock accounts for around 7% of Buffett's equity holdings.

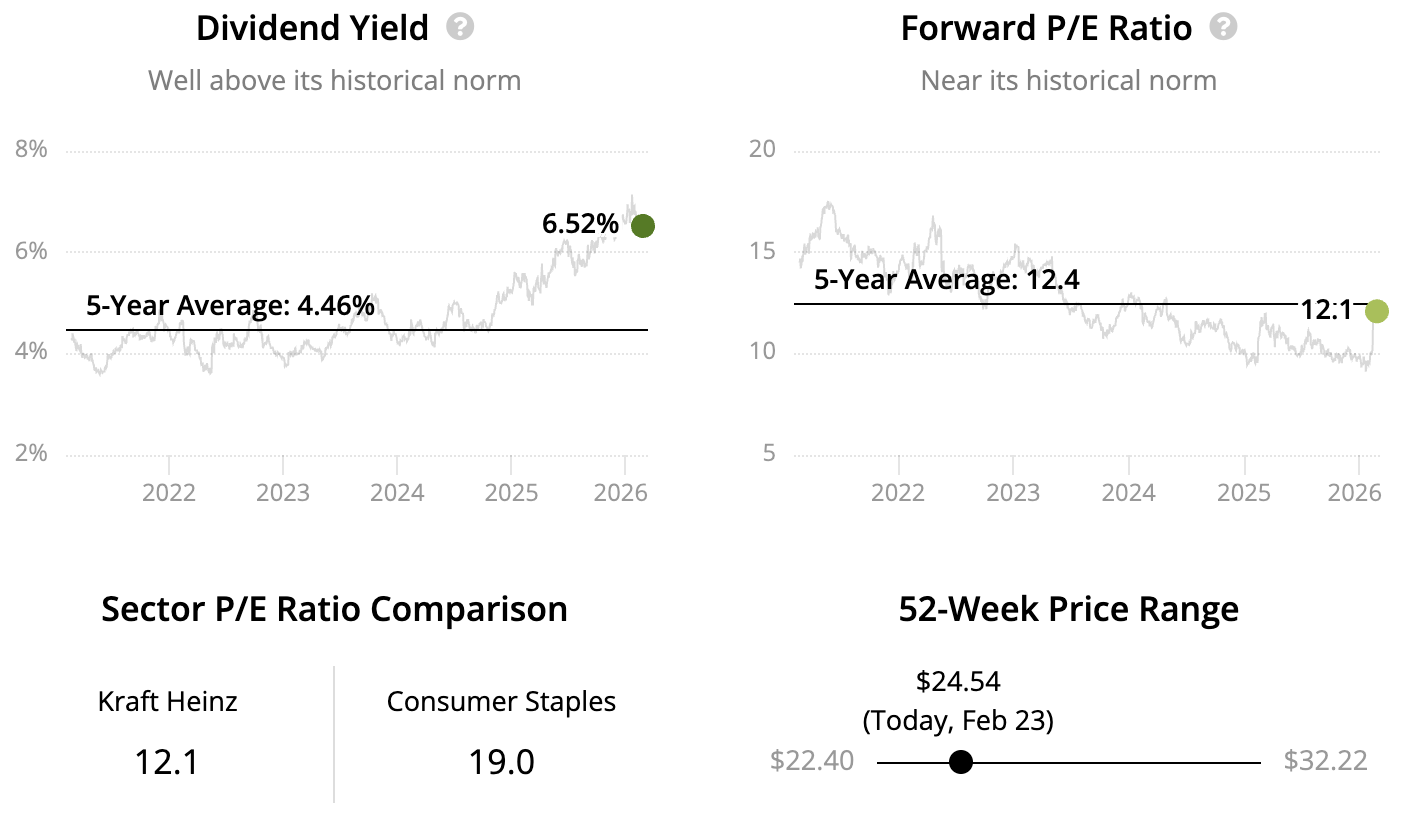

High-Yield Buffett Stock #5: Kraft Heinz

Sector: Consumer Staples – Packaged Foods and Meats

Dividend Growth Streak: 0 years

Dividend Safety Score: Borderline Safe

Dividend Yield: 6.5%

Kraft Heinz (KHC) represents about 3% of Berkshire Hathaway's portfolio and is one of the firm's less successful investments, with roots tracing back to a 2013 deal Buffett struck with 3G Capital to take Heinz private.

Kraft Heinz got into trouble after its private equity owners cut costs too far, leaving the maker of condiments, sauces, frozen meals, and other packaged foods more vulnerable to competition and healthy eating trends.

Coupled with a bloated balance sheet, Kraft Heinz slashed its dividend in 2019 and has struggled to achieve consistent, profitable organic growth. This is one of the less interesting investments in Berkshire's portfolio, even though it is among Buffett's highest-yielding dividend stocks.

Under new CEO Greg Abel, Berkshire has also signaled a desire to divest its stake in Kraft Heinz, capping a largely disappointing investment.

Warren Buffett’s Investment Strategy

Warren Buffett has evolved as an investor since launching his original partnership in 1956.

Back then, Warren Buffett’s portfolio was much smaller in size and allowed him to pursue the greatest inefficiencies he could find in the market almost regardless of the stock’s market cap. He focused intensely on finding stocks trading at cheap valuations.

Buffett was not afraid to make a single position account for more than 25% of his portfolio and stated that he would be comfortable investing up to 40% of his net worth in a single security if the probabilities were deemed to be extremely in his favor, limiting risk.

Warren Buffett’s portfolio remains concentrated today, with Apple representing over 20% of Berkshire Hathaway’s portfolio.

The idea behind running a concentrated portfolio is that there are relatively few excellent businesses and investment opportunities in the market at any given time, and owning too many positions reduces the impact from your few best ideas.

Back then, Warren Buffett’s portfolio was much smaller in size and allowed him to pursue the greatest inefficiencies he could find in the market almost regardless of the stock’s market cap. He focused intensely on finding stocks trading at cheap valuations.

Buffett was not afraid to make a single position account for more than 25% of his portfolio and stated that he would be comfortable investing up to 40% of his net worth in a single security if the probabilities were deemed to be extremely in his favor, limiting risk.

Warren Buffett’s portfolio remains concentrated today, with Apple representing over 20% of Berkshire Hathaway’s portfolio.

The idea behind running a concentrated portfolio is that there are relatively few excellent businesses and investment opportunities in the market at any given time, and owning too many positions reduces the impact from your few best ideas.

Importantly, Warren Buffett’s investment strategy has always been focused on the concept of staying within one’s circle of competence. Buffett has said that “risk comes from not knowing what you’re doing.”

In other words, never invest in a business or industry that is too hard for you to understand. The reality is, most investment opportunities fall outside of our circle of competence and should be ignored.

Since the days of his initial partnership, Buffett’s strategy has evolved to concentrate more on buying up wonderful businesses at reasonable prices rather than digging through the bargain bin for “cheap” stocks. He looks for companies that have strong economic moats and numerous opportunities for growth.

When Warren Buffett makes an investment, he has said that his favorite holding period is “forever.” The idea is to buy excellent companies with solid long-term growth prospects and let them compound over the long run.

Not surprisingly, our dividend investment philosophy shares many similarities with Warren Buffett’s.

By remaining focused on simple, high quality businesses trading at reasonable prices, we can construct a sound dividend portfolio that can deliver safe, growing dividend income for years to come.