Southern's Dividend Looks Secure Despite Potential Construction Delay at Nuclear Plant

Southern Company's two nuclear reactors under construction in Georgia may face more delays and require $2 billion of additional costs, according to testimony provided earlier this week by an independent monitor of the troubled project.

Known as Vogtle Units 3 and 4, these plants are America's first new nuclear reactors built in more than 30 years and have faced a number of major complexities and operational setbacks.

The project, which Southern has a 45.7% stake in, was initially expected to be completed in 2016 at a maximum cost of roughly $14 billion. But in-service dates have been delayed over five years and the total budget already exceeds $27 billion.

Don Grace was appointed by Georgia's state utility commission to independently evaluate Southern's ability to complete its nuclear reactors. His latest report suggests Southern's guidance could need to be revised as soon as this summer to better reflect the project's current status.

According to Mr. Grace, Vogtle Units 3 and 4 are likely to miss their regulatory-approved in-service dates of November 2021 and November 2022 by at least 7 to 9 months each.

This is being driven by inefficiencies caused by Southern's decision to accelerate testing prior to completing construction work. Mr. Grace assumes this deviation from "normal industry practice" was caused by management's realization that the firm would otherwise not meet its "aggressive" published milestones.

However, Southern on Wednesday reiterated its expectation that Unit 3 will be completed in January 2022 and stated that Vogtle 4 remains on track to be finished by November 2022, according to Reuters.

Even if Mr. Grace's projections prove correct, we don't believe a setback of this magnitude would pose a risk to Southern's dividend or long-term earnings power.

We estimate Southern would incur roughly $1 billion of additional costs, and management may not be able to recover these expenses from regulators after repeatedly missing the approved in-service dates.

Fortunately, Southern's scale can accommodate a one-time charge of this size. The company would remain profitable with annual pre-Vogtle net income of $3.4 billion. And if management borrowed funds to cover the full charge, Southern's net debt to EBITDA leverage ratio of 5.5x would rise by only around 0.1x.

The stakes would be much higher if the project was cancelled. This is the primary risk that could get Southern's dividend in trouble since the company's shareholders would be forced to shoulder billions of dollars of losses.

The firm's agreement with Vogtle's other owners stipulates that a vote must take place to continue construction following any "project adverse event." Should delays and costs extend significantly beyond Mr. Grace's forecast, this clause could be triggered.

But with both reactors so close to the finish line and the issues pressuring the current timeline appearing temporary in nature, risk of cancelling the project seems very low.

Outside of higher costs, Southern's allowed return on equity on its nuclear construction costs would also be reduced by 0.1% each month if units 3 and 4 are not operating by a certain time.

Mr. Grace's forecast suggests the projects would still be completed within about a year of these deadlines. And given that Vogtle is just one part of Southern's expansive business, a moderate reduction in the project's allowed returns wouldn't materially affect the company's earnings power.

However, S&P warns that any material delays in schedule would "likely result in a lower business risk assessment, and lead to lower ratings." Southern would presumably retain its investment grade status, but its BBB+ rating could be lowered.

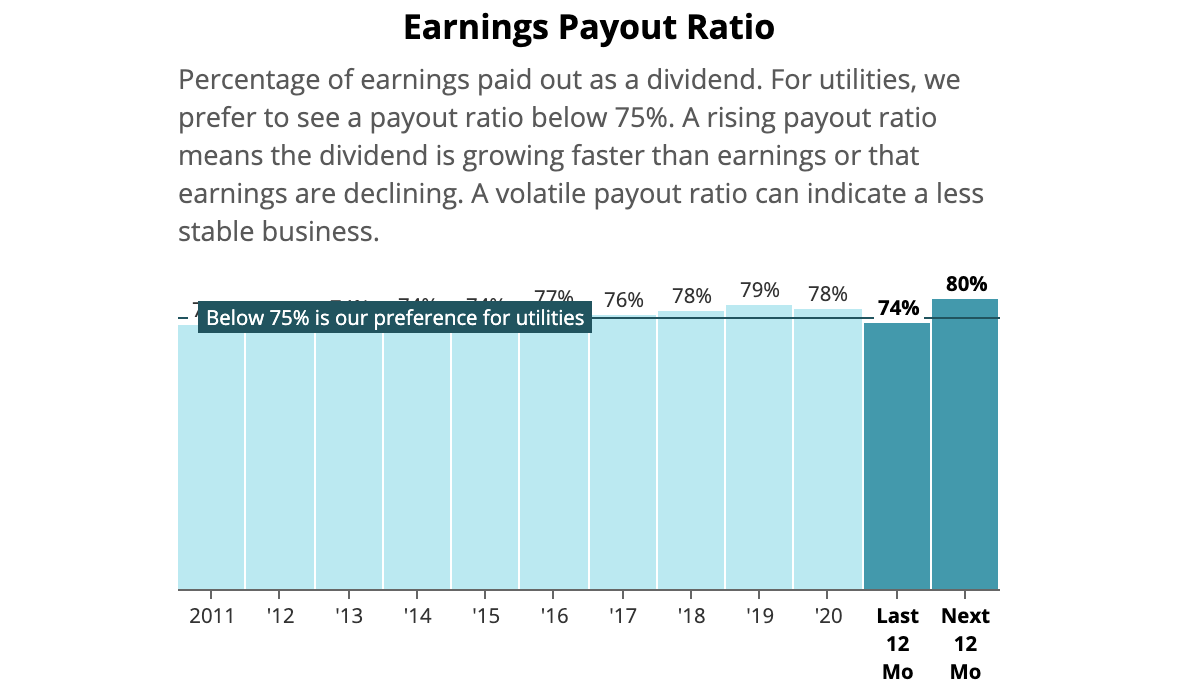

Coupled with Southern's elevated payout ratio (most regulated utilities maintain payout ratios below 70%), the company's annual dividend growth rate could remain in the low single digits for at least the next couple of years.

Source: Simply Safe Dividends

Once Vogtle's challenges are behind Southern, management expects the business to deliver 5% to 7% annual earnings per share growth. This would allow for potentially faster dividend growth and help the firm drive down its payout ratio.

Long-term growth is supported by Southern's favorable footprint from a regulatory perspective. Alabama accounts for around 30% of the utility's net income and has the most constructive regulatory environment of any state, according to RRA rankings. Georgia (over 40% of profits) is also ranked among the top five states.

Southern's geographic footprint gives it one of the stronger underlying growth profiles in the sector as well. Georgia has exhibited top-quartile population growth from 2010 to 2021, and the Southeast region in general has reported job and population growth that outpaces the national average.

Thanks to these qualities, plus the essential nature of utility services, Southern has paid uninterrupted dividends since 1948 and raised its dividend every year since 2002.

Despite lingering headline risk caused by Southern's nuclear reactor projects, we expect this trend to continue and will provide updates if any new material developments occur.