Duke Energy Rebuffs Activist Investor's Call to Split Into Three Companies

Activist investor Elliott Management on May 17 published a letter to Duke Energy's board urging the utility to break itself into three separately traded companies.

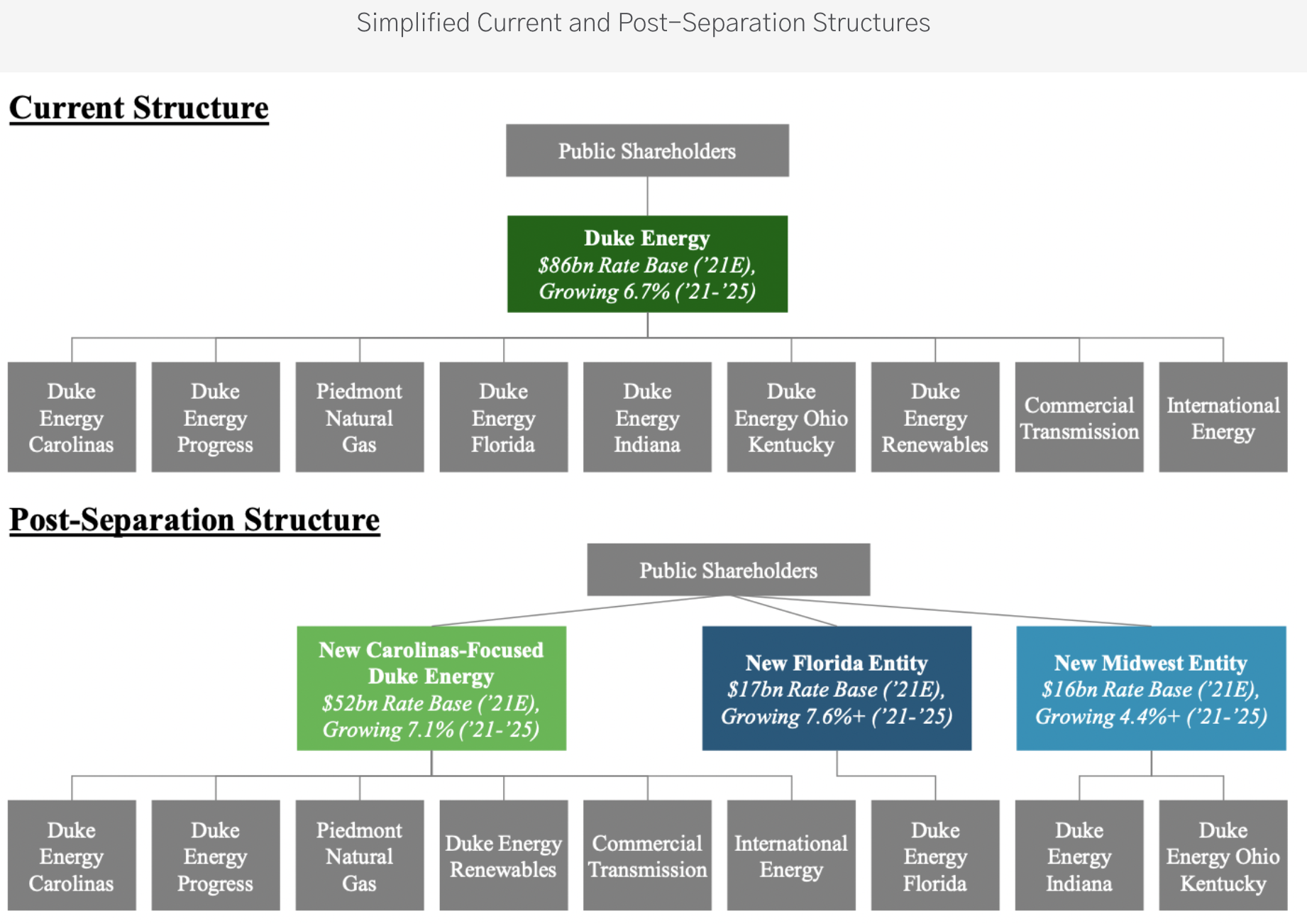

Source: Elliott Letter

Elliott argued that Duke's sprawling portfolio of utilities, which spans parts of the Midwest, Florida, and the Carolinas, "has burdened shareholders with a conglomerate discount relative to the value of Duke's utility franchises."

If each of these utilities was separated into its own publicly traded company, Elliott argues they would improve their operating performance due to additional management focus and achieve a higher valuation compared to Duke's consolidated structure.

In fact, Elliott believes the combined value of the three standalone utilities would reach $90 billion to $93 billion compared to Duke's current market cap of about $79 billion, representing a premium of nearly 20%.

However, splitting up Duke's utilities could muddle the picture for income investors. Duke's dividend would need to be divided between the three companies since none of them could support the full payout on their own.

Each utility would need to determine its optimal capital structure, address new financing needs, and account for any dis-synergies that come from having less scale. These issues could cause total dividends to decrease versus Duke's current payout.

For now, income investors do not need to worry. Duke responded with its own statement and wrote that its "business is stronger and more impactful as a consolidated, standalone entity that remains as one."

Management argued that Duke's size, scale, and geographic diversity contribute to its strong credit rating and lower cost of capital. Standing up smaller, independent utilities would reduce the firm's ability to effectively finance capital investments and risk incurring more costs.

Overall, Duke is skeptical of Elliott's proposal and believes the plan's incremental costs could even threaten the dividend, which management is proud to have increased for 15 consecutive years.

"Given the performance of the company, there is no strategic logic to breaking the company apart, and there is serious risk of dis-synergies that would weigh down the various spun-off entities and raise questions about the viability of the dividend to shareholders."

– Duke Energy, 5/17/21 Statement

Duke said it would review Elliott’s latest proposals, but we would be surprised if management moved forward in this direction.

The firm's recent performance has been solid (DUK shares have outperformed the utility sector over the past year), a five-year investment plan is in place that requires no new equity, and few management teams are interested in overseeing a smaller enterprise.

What Elliott and Duke can agree on is that the business owns a quality set of assets.

Elliott wrote that Duke benefits from "some of the strongest underlying organic growth in the regulated utility sector" based on population growth trends.

Duke's utilities are also supported by constructive regulation. Weighted by rate base, Elliott noted that "Duke operates in the top 20% of jurisdictions in the country."

These qualities attracted takeover interest from Florida-based utility NextEra last fall. NextEra is the world leader in electricity generated from the wind and sun, and Duke's regulated assets would help balance NextEra's growth in renewables.

Duke's management turned down NextEra's merger advances, which would have created the nation's largest utility. But unlike Elliott's proposal, which has no guarantees to unlock value, a higher bid from NextEra to acquire some or all of Duke's assets is something the firm may consider to create an immediate and guaranteed return for shareholders.

While a deal with NextEra could also create uncertainty for the dividend, investors would presumably lock in a healthy gain based on the premium NextEra would be paying.

Overall, we continue to believe Duke is a quality long-term investment for conservative income portfolios. A little activist pressure could help sharpen management's focus, but we believe it is unlikely to affect Duke's long-term outlook or dividend policy.