Coca-Cola's Volume Returns to Pre-Pandemic Levels; Tax Case Uncertainty Still Looms

With vaccine availability increasing and more economies opening up, Coca-Cola on Monday reported that its total sales volumes in March recovered to levels last seen in 2019 prior to the pandemic.

The firm's beverage volumes had declined as much as 25% in April 2020 when numerous countries implemented synchronized lockdowns. While trends slowly improved throughout the year, Coke was still seeing mid-single-digit volume declines through mid-February.

The company's return to pre-pandemic volumes is especially impressive given Coke's distribution mix. Nearly half of the firm's revenue is generated from away-from-home channels such as restaurants, convenience stores, movie theaters, and event venues.

This part of the business continues improving sequentially but has not yet fully recovered. Even Coke's U.S. restaurant volumes were still down in March despite more consumers dining out. Meanwhile, most offices remain closed, theaters are very slowly reopening, and sports arenas continue to face capacity limits.

The path to a full recovery remains even choppier around the rest of the world, with weekly new cases of COVID hitting an all-time high earlier this month. Europe's vaccine rollout has gone slower than anticipated, and most developing countries are lagging behind in the vaccination race.

Markets outside of North America account for over 60% of Coke's revenue, so management is not expecting a swift recovery in away-from-home demand as many countries continue managing through restrictions. Regardless, it's encouraging to see Coke's total volumes recover fully despite this backdrop.

Citing the company's momentum in March, management had confidence to reaffirm Coke's 2021 guidance. The firm expects high single-digit organic revenue growth and around 10% earnings growth.

Free cash flow is also expected to be at least $8.5 billion, keeping the firm's $7.2 billion dividend covered. If this forecast is realized, Coca-Cola's free cash flow payout ratio would sit near 85% this year, up from around 80% in 2019.

While Coke's payout ratio would be above management's long-term target of 75%, there's a path to return to the firm's preferred level over time. Coca-Cola can lower its payout ratio by growing its dividend at a slower pace than its earnings, which management expects will compound by 7% to 9% per year in the long term.

Coke in February raised its quarterly dividend by a penny, representing 2.4% growth. Investors should expect token dividend increases to continue for at least another year or two, especially until the company resolves a major tax dispute.

In September 2015, the IRS claimed Coca-Cola owed $3.3 billion of additional income taxes for years 2007-09. The IRS believed Coke attributed too much of its profit to its operations in foreign markets where corporate tax rates are lower compared to the U.S.

Coca-Cola quickly filed a petition with the tax court. Then, in November 2020, the court issued an opinion in which it predominantly sided with the IRS. Coke plans to appeal and believes it is "more likely than not" that the firm's tax positions will ultimately be sustained.

But the stakes are high. Under a worst-case scenario in which the IRS's methodology is also applied to subsequent tax years from 2010-20, Coca-Cola said it could face a total liability of $12 billion, or nearly 1.5 years' worth of free cash flow. And the firm's effective tax rate would increase by 3.5% going forward.

Assessing the likelihood of legal outcomes is very difficult, and management would not even venture a guess regarding when the court might make its next ruling on the case (hopefully within the next year).

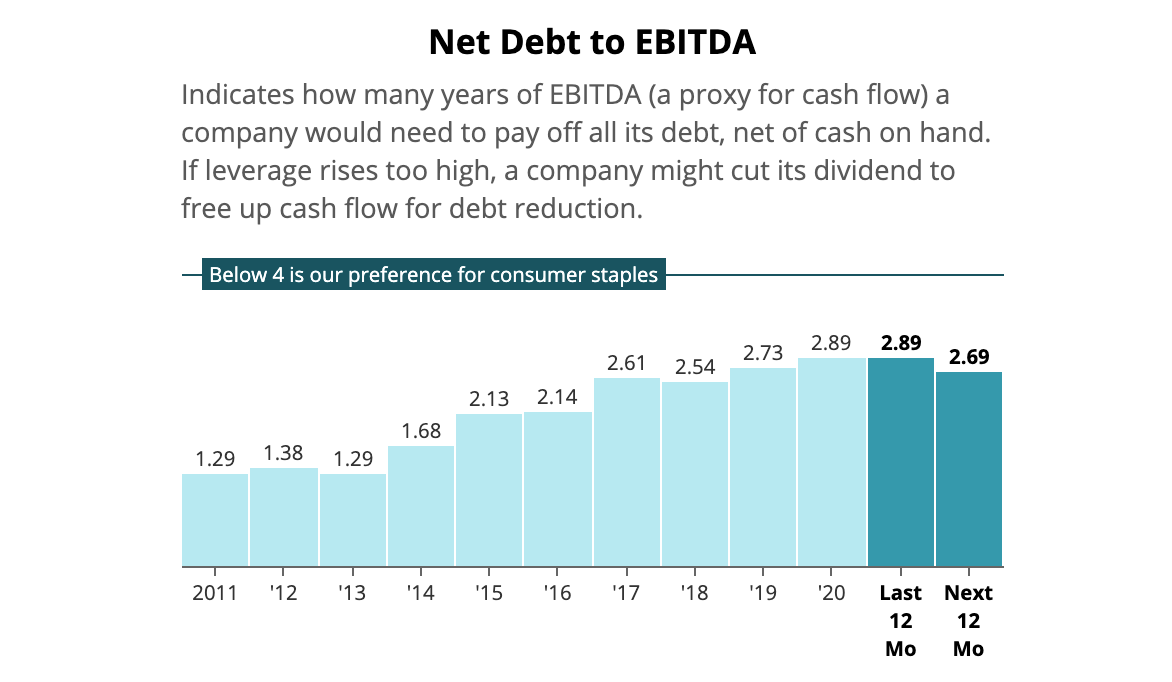

If the worst-case scenario plays out and Coca-Cola is on the hook for $12 billion, we estimate the company's net debt to EBITDA leverage ratio would rise from 2.7x to around 3.7x, its highest level in at least a decade.

Source: Simply Safe Dividends

Coke's elevated leverage would reduce its flexibility but shouldn't pose a major concern thanks to the company's predictable cash flow and capital-light operations.

However, Coca-Cola's deleveraging ability would be slowed by the firm's elevated payout ratio, which limits the amount of cash flow available for debt reduction. Coke would instead need to lean more on earnings growth and asset sales to restore its balance sheet in a timely manner.

S&P already has a negative outlook on Coke's A+ credit rating, which we expect would be lowered at least one notch if the tax court comes back with an unfavorable ruling.

Any credit rating action would also depend on how aggressively Coca-Cola decides to defend its current rating, with S&P noting the possibility of asset sales or even a reduction to the company's "very large dividend".

"Coke's financial policy commitment has taken on increased importance given recent events. Its loss of a tax court case in late 2020 and hiring of counsel to advise the company and its board of directors over transfer pricing litigation with the U.S. IRS signals the long-standing dispute is entering its later stages. There is a wide array of possible outcomes, some of which carry negative rating implications.

"If the company does not win on appeal and clear negative outcomes materialize with respect to very large retroactive tax liabilities and prospective tax payments, we would examine the earnings power of the business post-pandemic and Coke's willingness to take other actions to maintain the rating. These include asset disposals and a reduction of its very large dividend, the latter of which is not factored into the rating."

– S&P Global Ratings, 3/1/21 Report

The wide range of possible tax court outcomes is uncomfortable, but it's worth noting that the IRS has no other significant wins against companies in international tax law, according to The Wall Street Journal. Perhaps the company can win this battle.

Either way, Coke appears reasonably positioned to handle most adverse outcomes. Based on what we know today, we are maintaining Coca-Cola's Safe Dividend Safety Score.

If Coke borrowed $12 billion in a worst-case scenario, increasing its interest expense, and its tax rate jumped by 3.5%, we estimate the company's free cash flow this year would be closer to $7.8 billion rather than management's $8.5 billion guidance.

The $7.2 billion dividend would remain covered, but the firm's free cash flow payout ratio would rise from 85% to around 92%. Coupled with the spike in leverage, would this be enough for Coke to cut its dividend?

We think a dividend reduction would still be unlikely as long as Coca-Cola's core soda business remained stable. This would take pressure off the company to invest more aggressively in other beverage categories while it worked on restoring its financial flexibility.

Management could also find other cash flow levers to pull outside of the dividend, such as further optimizing short-term marketing spending, pursuing more cost efficiencies, and identifying non-core assets for divestment.

Coupled with Coke's well-laddered debt maturities, ability to borrow at low interest rates, and substantial cash flow generation expected over the next few years, management feels "pretty confident we can take care of just about any scenario."

"I think we've got ample flexibility through both the way in which we've been managing the balance sheet and when we think about the cash generation prospects for the next few years to manage any scenario. We continue to believe that we have a very strong case and unlikely to have to consider that worst-case scenario.

"But the work we've done really beginning last year to organize our debt portfolio in a way that gives us more flexibility. And when we take that into consideration, along with the cash we'll generate in the next 2 to 3 years, I think we feel pretty confident that we can take care of just about any scenario."

– CFO John Murphy, February 2021 Earnings Call

We will continue monitoring Coca-Cola's tax case and provide updates as needed. While an adverse ruling could cause the stock to dip and the firm's tax rate to rise, Coke seems likely to retain its long-term reputation as a defensive holding with predictable dividends.