On Thursday, management finally found a buyer. PPL will sell its U.K. business to National Grid in a transaction valued at $19.4 billion.

PPL shares jumped 5% on the news as the assets achieved a higher value than expected; Reuters previously suggested the business could fetch a valuation of up to around $16 billion.

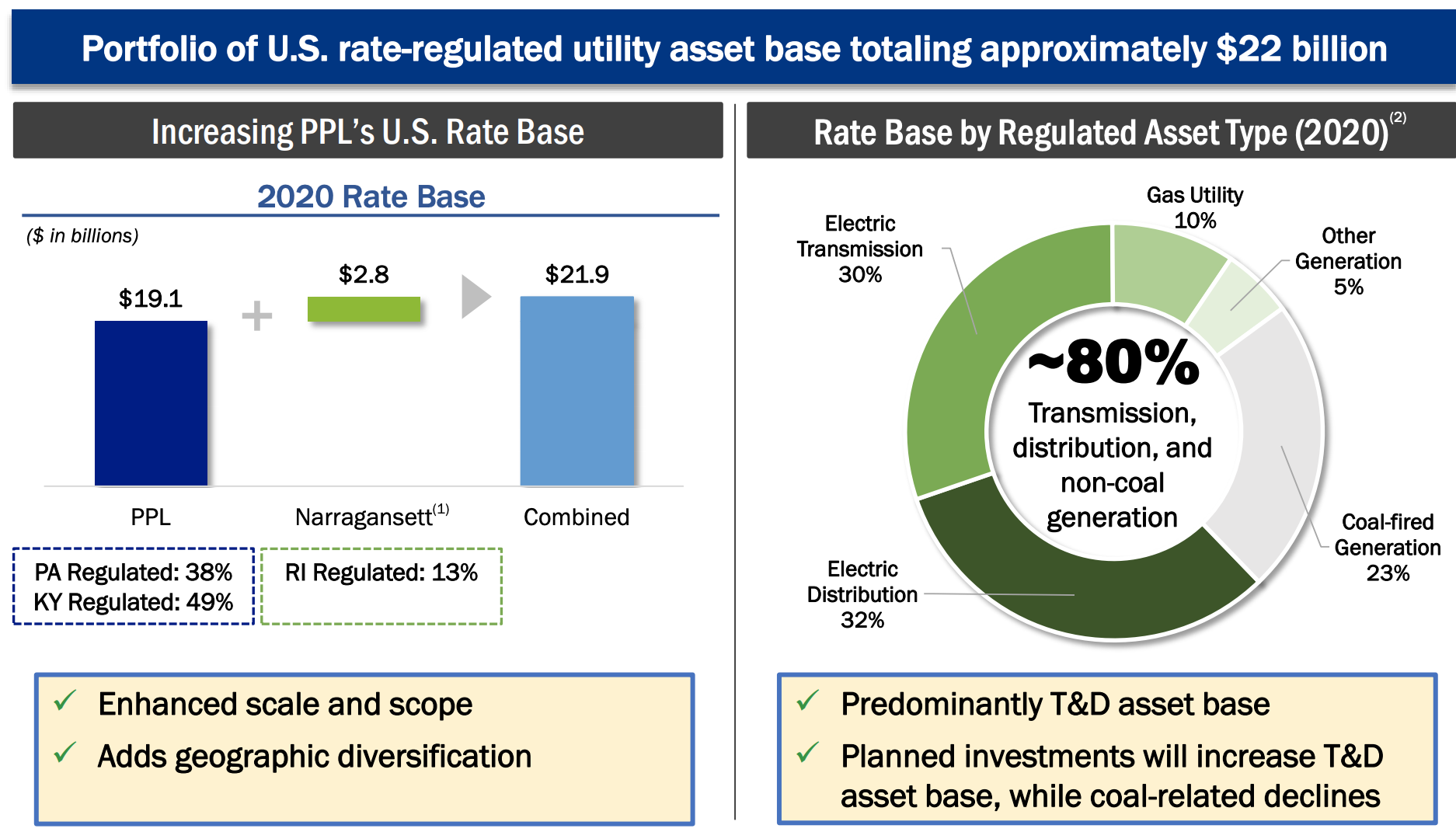

Management expects net cash proceeds of $10.2 billion once the deal closes within four months. PPL will use $3.8 billion of these funds to acquire Narragansett Electric, a regulated utility in Rhode Island owned by National Grid.

Following these transactions, PPL will consist of regulated utilities across Pennsylvania, Kentucky, and Rhode Island. About 80% of its rate base will be focused on electric and gas transmission and distribution, with coal-fired generation shrinking in importance (less than 20% of earnings going forward).

Source: PPL Investor Presentation

After paying for Narragansett, residual net cash proceeds of $6.4 billion will be used to strengthen PPL's investment-grade balance sheet, with $3 billion to $3.5 billion earmarked for debt reduction.

The remaining $3 billion will be used opportunistically for potential acquisitions, share repurchases, or other investments. Management said they are not under any set timeline to deploy these funds.

As for the dividend, PPL said it will maintain its regular quarterly dividend of 41.5 cents per share until the acquisition of Narragansett closes, which is expected to happen within 12 months.

Then, PPL will target a 60% to 65% payout ratio and reset its dividend accordingly.

We estimate PPL's U.S. regulated utilities generated around $1.10 per share in annual earnings in 2020. Narragansett could add around 20 cents per share based on its adjusted net income over the past year.

That would bring PPL's ongoing EPS to $1.30 before accounting for any interest expense savings from debt reduction, earnings accretion from potential buybacks, and any additional acquisitions.

We estimate that PPL's $3 billion of debt reduction could increase EPS by around 10 cents. Deploying the remaining $3 billion of funds could add another 20 cents or so, though it's uncertain how and when PPL will invest that money.

Overall, we believe these uses of residual cash could contribute 10 cents to 30 cents to EPS, and the underlying business is expected to grow moderately this year as well.

While the financial picture remains a little fuzzy until PPL deploys all of the proceeds from these deals, we'd guess that the company's pro forma adjusted EPS may sit between $1.40 and $1.60.

Applying a 60% to 65% payout ratio suggests an annual dividend per share between 84 cents and $1.04, or a reduction of 37% to 49% compared to the current payout of $1.66.

This would put PPL's dividend yield around 3% to 3.5% based on its intraday share price of $29.30 as of March 18.

Management expects the dividend to grow in line with PPL's earnings growth, which is projected to "be competitive with U.S. utility peers post transactions."

We would assume that means PPL's earnings and dividend have potential to grow at a mid-single-digit annual pace going forward, an improvement compared to the low single-digit growth recorded over the past decade.

Until PPL's new, lower dividend is announced sometime in the next 12 months, we will maintain the firm's Unsafe Dividend Safety Score. Income investors considering the stock should understand that PPL's dividend yield will fall from 5.6% to around 3% to 3.5% within 12 months.

Once the rebased dividend is in place, we will likely upgrade PPL's score to Safe, reflecting the company's strong balance sheet, healthy payout ratio, and predictable earnings derived from U.S. regulated utility operations.

While acknowledging PPL's dividend risk, we've held onto our small position in our Conservative Retirees portfolio under the belief that the stock's low valuation could begin to improve once the firm reached a deal for its U.K. assets.

We felt that the stock's short-term performance would be driven by how much value PPL receives in a sale and how management reinvests the proceeds (rather than any change in the dividend). Today's news was a step in the right direction.

We plan to continue holding our shares for now. However, we may consider evaluating replacement ideas in the months ahead to see if any can beat PPL's forward-looking yield (3% to 3.5%) and long-term growth potential.