Investors Await Update on PPL's Asset Sale Plans; Dividend Could Face a Moderate Cut But We Plan to Hold

PPL last August announced plans to sell its U.K. utility operations, which generate a little over half of the firm's earnings.

No deal has been announced yet, but the fate of PPL's regular dividend depends on how much of these earnings management can replace by using some of the proceeds from a potential sale to acquire a U.S. utility.

For more information on PPL's divestiture plans, please see our note here.

When PPL announced its plans, management expected to reach a deal in the first half of 2021.

The company has not issued any updates on the sale process since August, but in November Reuters warned that a deal could be delayed due to uncertainty over whether the U.K. will leave the European Union without a trade deal.

Following another nationwide lockdown announced earlier this month, the U.K. economy is projected to contract again in the first quarter of the year.

Needless to say, the U.K.'s investment appeal has weakened due to the triple threat posed by a more challenging regulatory environment for utilities, the latest round of pandemic-driven lockdowns, and post-Brexit economic growth uncertainties.

Management previously expected PPL's U.K. utility business "to command a premium valuation," but that could prove challenging given the current backdrop and the limited number of bidders for the firm's assets, per sources cited by Reuters.

Reuters suggested the business could fetch a valuation of up to around $16 billion, including debt. If PPL invested an equivalent amount into a U.S. utility company at the sector's current P/E ratio of 17.5, we believe it would come up a little short of replacing its U.K. earnings in full.

That's important because management's target payout ratio range suggests PPL needs to replace all of its U.K. earnings to justify keeping its regular dividend intact.

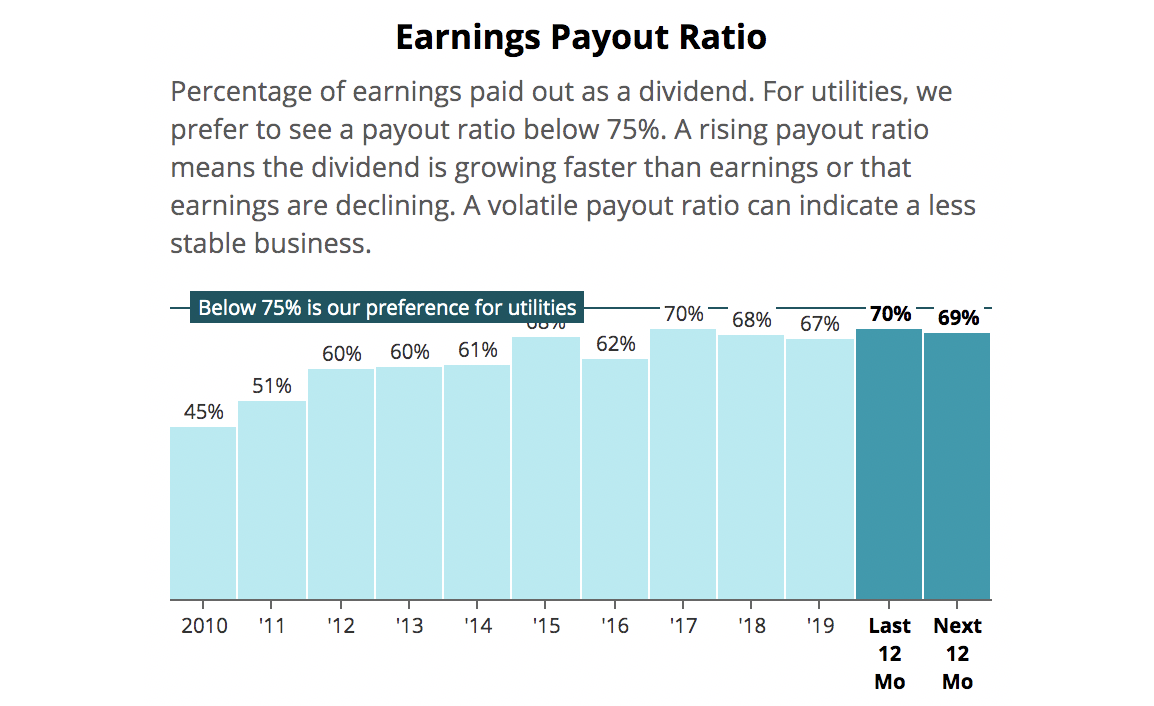

Management wants to maintain a payout ratio around 60% to 70% after divesting the U.K. business, and PPL's payout ratio already sits near 70% today.

Any reduction to ongoing earnings would put PPL over its target payout ratio range. To get back in line, the dividend would either need to be reduced or grown at a much slower pace than earnings.

Source: Simply Safe Dividends

PPL also faces potential transaction costs and taxes, not to mention PPL's plans to use some of the proceeds to strengthen its investment-grade balance sheet and return capital to shareholders through buybacks or a special dividend.

These outlays reduce the amount PPL can invest into a U.S. utility company to help offset the loss of earnings from selling its U.K. utilities.

Barring a rich sale price of PPL's U.K. assets, which seems increasingly unlikely in today's environment, or a great deal to acquire a large U.S. utility, the company's regular dividend appears more at risk of being reduced whenever a transaction is announced.

While we don't have a deal to analyze yet, out of conservatism we are downgrading PPL's Dividend Safety Score from Borderline Safe to Unsafe to reflect the somewhat wide range of outcomes facing the regular dividend.

We estimate PPL's U.S. regulated utilities generate around $1.10 per share in annual earnings on a standalone basis, which is insufficient to cover today's annual dividend of $1.66.

If PPL chose not to acquire another utility company with the sale proceeds, we estimate it would need to reduce its regular dividend by around 50% to 60% to return to management's target payout ratio range.

We think that scenario is very unlikely as PPL would like to keep growing its business. But if this played out, investors would presumably receive a large special dividend, and perhaps PPL would then look to be acquired by another utility.

Assuming PPL uses most of the proceeds to buy another U.S. utility, we'd guess the company would not need to reduce its regular dividend by more than around 20% to 30%. But again, this depends on how much the U.K. business sells for and the size of an acquisition PPL makes to rebuild its earnings power.

Another path could see PPL using most of the cash proceeds from a sale to buy back its own shares, which trade at a meaningful discount to the utility sector, and acquire another U.S. utility.

If PPL sold its U.K. assets for $16 billion, the cash proceeds might be around $8 billion (the U.K. division held $8 billion of debt last year). Perhaps PPL would set aside a couple billion for debt reduction and use $6 billion to buy back shares.

At a share price of $30, that would be enough to retire around 25% of shares outstanding, though executing such a large transaction may not be practical.

But if this did occur, we estimate PPL's U.S. regulated utilities would see their annual EPS rise from $1.10 to nearly $1.50.

If PPL then used the other $8 billion from the deal to buy a utility at the sector's current P/E ratio of 17.5, that could add another $0.80 or so to earnings.

Together, these actions would cover the current $1.66 per share dividend, though PPL's payout ratio would sit close to 75%. And this simple exercise fails to account for any transaction-related costs while also making a number of other assumptions that may be unrealistic.

PPL will maintain its regular quarterly dividend of 41.5 cents per share at least until a deal is announced. But income investors should not hold PPL banking on its regular dividend being kept at its current level after the U.K. business is sold. A transformation is underway.

This isn't necessarily a reason to sell, though. We continue to believe that the stock's short-term performance will be driven by how much value PPL receives for its U.K. business, and how management decides to reinvest the proceeds.

PPL also remains committed to paying a meaningful dividend after a potential sale occurs, and we think the stock's seemingly low valuation lends some support to management's sum-of-the-parts thesis.

We plan to continue holding our shares of PPL in our Conservative Retirees portfolio and will wait to reevaluate the situation until either PPL's valuation strengthens or a transaction is announced.

.png)