Political Headwinds Remain an Overhang on Con Edison

The defensive utility sector has trailed the S&P 500 by more than 15% over the past year. Shares of Con Edison have been especially weak, slumping around 15% since mid-November to reach a level not far from their pandemic lows seen last March.

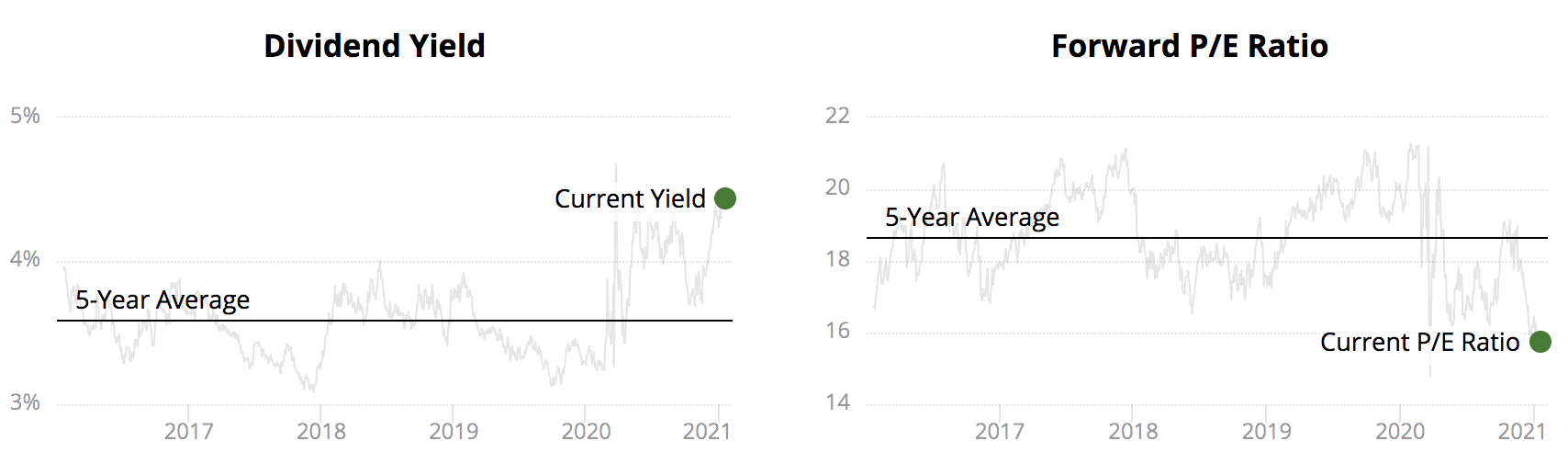

With Con Edison's valuation looking unusually cheap compared to historical norms, some investors may be wondering if the stock is a value trap and could be at risk of changing its dividend policy.

Source: Simply Safe Dividends

Management typically declares (and raises) Con Edison's first-quarter dividend on the third Thursday of January, so we will get an answer on the dividend as soon as tomorrow.

Unless management expects a material deterioration in New York's regulatory framework, which seems unlikely at this stage, we think the dividend remains safe despite the unusual mix of political and demand challenges Con Edison has faced over the past year.

Coupled with many businesses and offices closing, New York City has been the most impacted by the pandemic in terms of reduced electricity consumption. More bad debt expense and loss of late fees have also served as pandemic-related headwinds.

Fortunately, Con Edison's business is largely protected by regulatory policies which ensure its revenue earned is in line with what it needs to cover costs and earn a fair return.

However, this tough backdrop could make it harder for Con Edison to raise rates and grow its business in the future, especially as tensions with politicians and regulators rise.

New York Governor Andrew Cuomo turned up the heat on the state's utilities following extensive power outages caused by Tropical Storm Isaias last August. For more background information, please see our note here.

On November 19, the New York Public Service Commission completed its investigation into the apparent failure of the state's electric utilities to adequately prepare for and respond to the storm.

Con Edison was slapped with a potential penalty of $102 million, and its Orange and Rockland subsidiary was assessed a $19 million potential penalty. While these fines cover more than 30 apparent violations, the majority relates to "allegedly unreasonable weather forecasts."

The utilities believe these proposed punishments are not warranted and filed responses to the commission on December 21.

A final decision has not yet been made. Even if Con Edison must pay these penalties, the record fines would represent only about 4% of the firm's annual operating income.

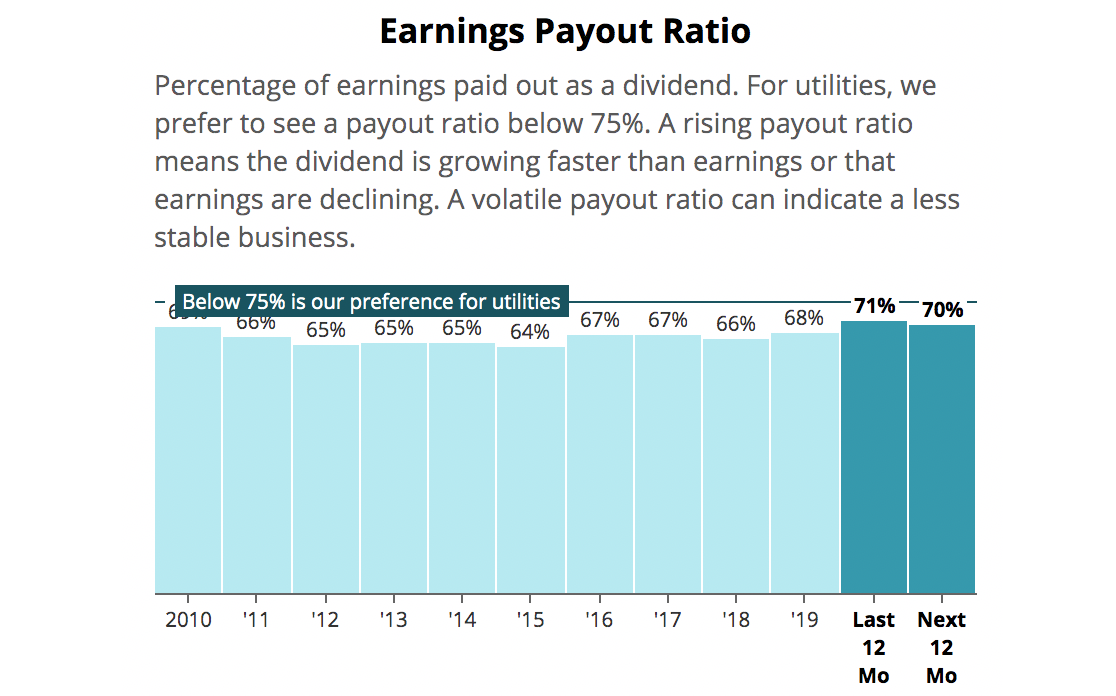

Con Edison's payout ratio in the year ahead is projected to sit at the high end of management's 60% to 70% target range and would move up a few percentage points if earnings were reduced by the potential penalties.

Source: Simply Safe Dividends

Given the temporal nature of a one-time penalty, these fines seem unlikely to threaten the dividend on their own.

Con Edison's payout ratio could also edge higher if the firm sells its gas transmission business. Management has expressed interest in this idea to continue focusing Con Edison on cleaner energy businesses.

Unlike utilities CenterPoint and Dominion, which cut their dividends last year as part of plans to reduce their mix of non-regulated businesses, Con Edison already generates more than 90% of its earnings from regulated utility operations.

Gas transmission represents less than 3% of the utility's earnings and assets (versus about 25% for Dominion), so a potential divestiture would probably only increase Con Edison's payout ratio by a couple of percentage points.

A payout ratio near 75% would be above the high end of management's 60% to 70% target range, but it would be surprising if that was enough to warrant a dividend reduction.

Instead, Con Edison would probably opt to grow its dividend at a pace much slower than earnings until its payout ratio fell to a more comfortable level.

Regulatory challenges represent the main wildcard for the dividend going forward and are admittedly a murky risk to evaluate.

The commission in its November report reiterated the possibility of revoking Con Edison's operating license if it finds that the utility has failed to continue providing safe and adequate service.

If such a scenario materialized, Con Edison would presumably have to sell its infrastructure to another utility company and leave the state. This outcome seems unlikely given the complexities and costs involved, but it would obviously be a high severity event.

Con Edison could also face more pressure to better anticipate storm impacts. For example, having more crews on standby would aid in storm restoration. These costs would be very high though, and regulators may want shareholders to absorb some of the burden.

Ratings agency S&P in November lowered its outlook on Con Edison's A- credit rating to negative from stable, reflecting the increased possibility that political challenges could affect New York's regulatory environment.

S&P said returning to a stable outlook is possible primarily if "the company effectively manages regulatory risk and is not subject to additional overt political interference."

Only time will tell. But for now, S&P's base case assumes Con Edison's dividend growth "averages a little above 5% annually." This further suggests a dividend cut is unlikely since ratings agencies usually speak with management teams about their assumptions.

Overall, Con Edison's outlook has become rather murky as the pandemic continues weighing on New York City's fundamentals and storm events have created tension with regulators. Until these issues show signs of being resolved, Con Edison's valuation may remain weak to reflect these uncertainties.

Assessing regulatory risk as it relates to the dividend is not easy, but based on what we know today, we expect Con Edison's dividend to remain safe but with very moderate growth prospects.

Given the stock's relatively low expectations, we plan to continue holding our shares in our Top 20 and Conservative Retirees portfolios as more information comes in.

Con Edison next reports earnings in February. As always, we will continue monitoring the situation and provide updates as needed.

.png)