JPMorgan's Dividend Remains Covered But Economic and Regulatory Uncertainty Persists

On September 30, the Federal Reserve extended through the fourth quarter its capital preservation measures on America's biggest banks.

Banks with more than $100 billion in assets are not allowed to repurchase shares, and their dividends cannot be increased or exceed net income generated over the past year.

Capping the amount of capital that can be returned to shareholders provides more cushion for banks against loan losses and supports lending during these uncertain times.

Given the Fed's control over big banks' dividend policies and the uncertain shape of this recession, we have assigned Borderline Safe Dividend Safety Scores to most large banks (including JPMorgan).

If the economy tracks towards a worst-case scenario, or political pressure mounts, the Fed could follow the European Central Bank's decision to temporarily ban bank dividends.

For now, it's still a waiting game.

JPMorgan reported third-quarter earnings on October 13, providing the latest look at how the country's largest bank by assets is faring during the downturn.

On the bright side, JPMorgan did not see a need to increase its $34 billion allowance for potential loan losses after having built its reserves by $8.9 billion in the second quarter.

In other words, management feels the bank's assumptions about the economy and future credit performance did not need to materially change compared to last quarter.

Without needing to build more reserves, coupled with strong results in investment banking and trading, JPMorgan's earnings were better than expected.

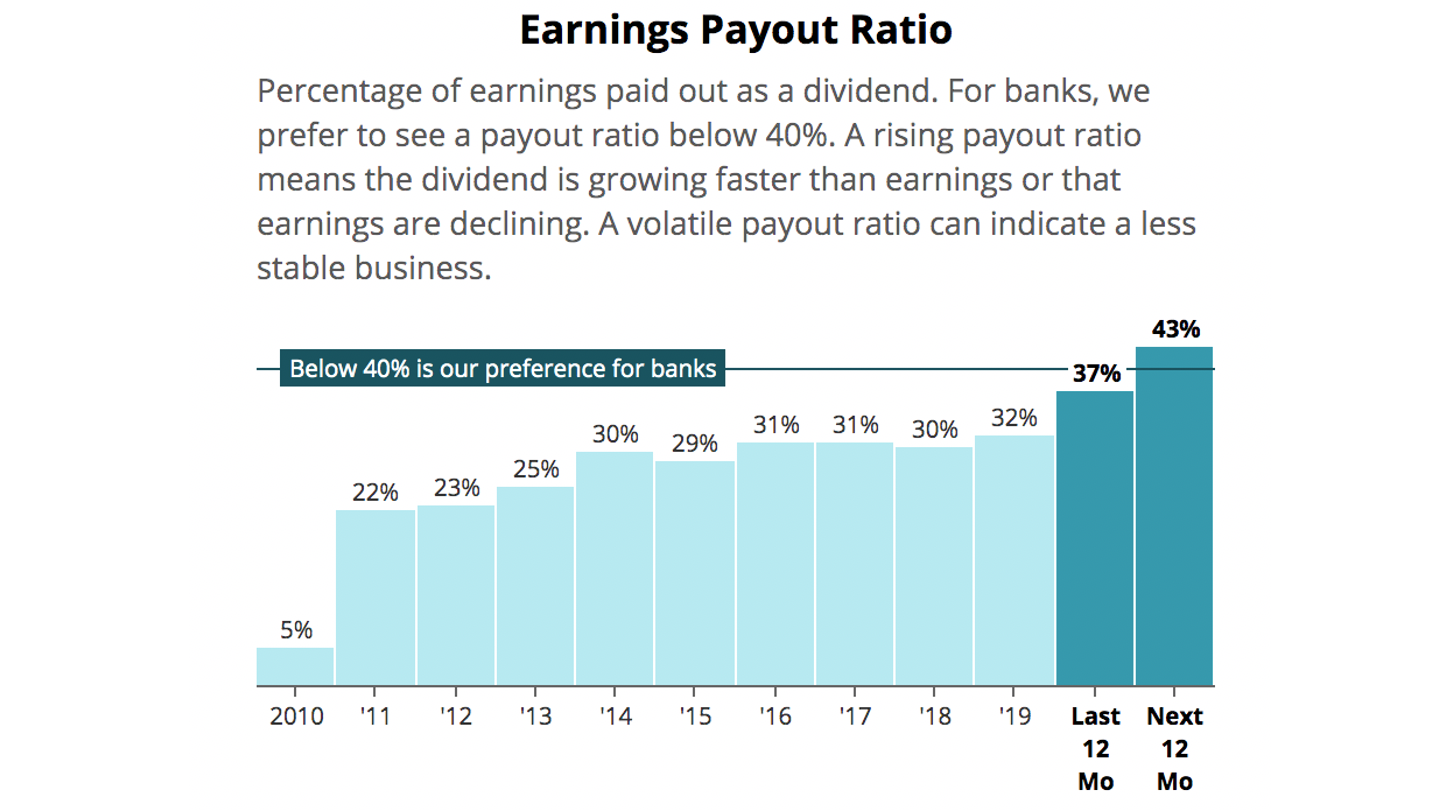

This helped JPMorgan's third-quarter payout ratio fall to about 30%. The bank's dividend coverage seems likely to remain well in compliance with the Fed's current restrictions, which essentially limit banks to a trailing payout ratio of 100%.

Source: Simply Safe Dividends

Despite some short-term stability in the loan book's performance, JPMorgan made it clear that a wide range of economic outcomes remains.

Management acknowledged that loan delinquencies haven't ticked up much yet thanks to the "extraordinary support" provided by the stimulus package passed earlier this year.

But assuming no additional stimulus beyond 2020, JPMorgan believes loan delinquencies will pick up in early 2021 with charge-offs materializing later in the year.

CEO Jamie Dimon estimated that JPMorgan has set aside $10 billion more in reserves than it needs to cover bad loans if the economy tracks its base case, but the bank may need another $20 billion in reserves if a worst-case scenario plays out.

For context, JPMorgan's 2019 net income totaled about $36 billion.

Additional stimulus measures would give JPMorgan more confidence that the economy can deliver on the firm's base case scenario, but it's too soon to say what will happen and how effectively policymakers will continue responding.

"The question [is] whether the [stimulus] bridge will be long enough and strong enough to bridge people back to employment and bridge small businesses back to normalcy. I think it remains to be seen.”

– CFO Jennifer Piepszak, 10/13/20 Q3 Earnings Call

Despite this uncertainty, JPMorgan remains confident it can weather an "extreme adverse" recession scenario based on its internally-run stress test, which has a higher peak unemployment rate and a deeper GDP trough compared to the worst-case scenarios in the Fed's stress test.

While the bank projects it may need to put up another $20 billion in reserves in such a scenario, those reserves would likely be built over several quarters, smoothing out the financial impact.

As a result, Mr. Dimon believes JPMorgan would still be positioned to pay the dividend and potentially buy back stock while remaining conservatively capitalized.

But it's anyone's guess how bank regulators would respond to such a shock. Just because JPMorgan remained financially healthy and capable of paying dividends does not mean the Fed would allow it to in such an unusual environment.

Overall, JPMorgan this quarter showed why it remains one of the strongest and most conservatively managed banks, but it's not immune from these external pressures.

Until this regulatory uncertainty is resolved, which could take at least several quarters, we expect to maintain JPMorgan's Borderline Safe Dividend Safety Score.

We will continue monitoring the industry as banks grapple with rising loan losses, low interest rates, and the Fed's second round of stress tests, which will be released by year-end.

.png)