Solar's Dividend Safety Score Upgraded on Portfolio Resilience, Expected Payout Ratio Improvement

Solar Senior Capital is an externally managed business development company that invests primarily in loans of private middle market firms to generate income.

The company's portfolio is valued at around $500 million and diversified across 215 borrowers in over 115 industries, with an average issuer exposure of less than 0.5% of the portfolio.

No industry accounts for more than 25% of the portfolio either. Diversified financial services represents 22.5% of Solar's investments, followed by healthcare providers (18%), professional services (9.3%), insurance (8.6%), and communications equipment (5.4%).

Solar has had a Very Unsafe Dividend Safety Score for years, reflecting the firm's high payout ratio and small size, as well as the generally risky nature of business development companies' operations.

After all, investing in loans with double-digit yields in a zero interest rate world is a dangerous game that's only magnified with the use of leverage.

In May, Solar cut its dividend by 17% in response to the lower interest rate environment (almost all of its loans have variable interest rates), but its portfolio's performance has remained resilient despite the pandemic's stress on many credit investments.

As of June 30, all of the firm's borrowers had made their interest payments.

First lien senior secured loans account for almost all of Solar's portfolio, reducing its risk profile. Management also believes the majority of its portfolio companies provide essential services in non-cyclical sectors which will continue to be required during periods of regional stay-in-place mandates.

Solar has also managed its leverage conservatively compared to many other business development companies.

The firm's net debt-to-equity ratio is only 0.68x, providing a cushion to its regulatory limit of 2.0x debt-to-equity as well as its target leverage ratio of 1.25x to 1.50x.

Management plans to increase leverage as it takes advantage of various investment opportunities to grow the portfolio, which is expected to result in net investment income that exceeds Solar's current dividend.

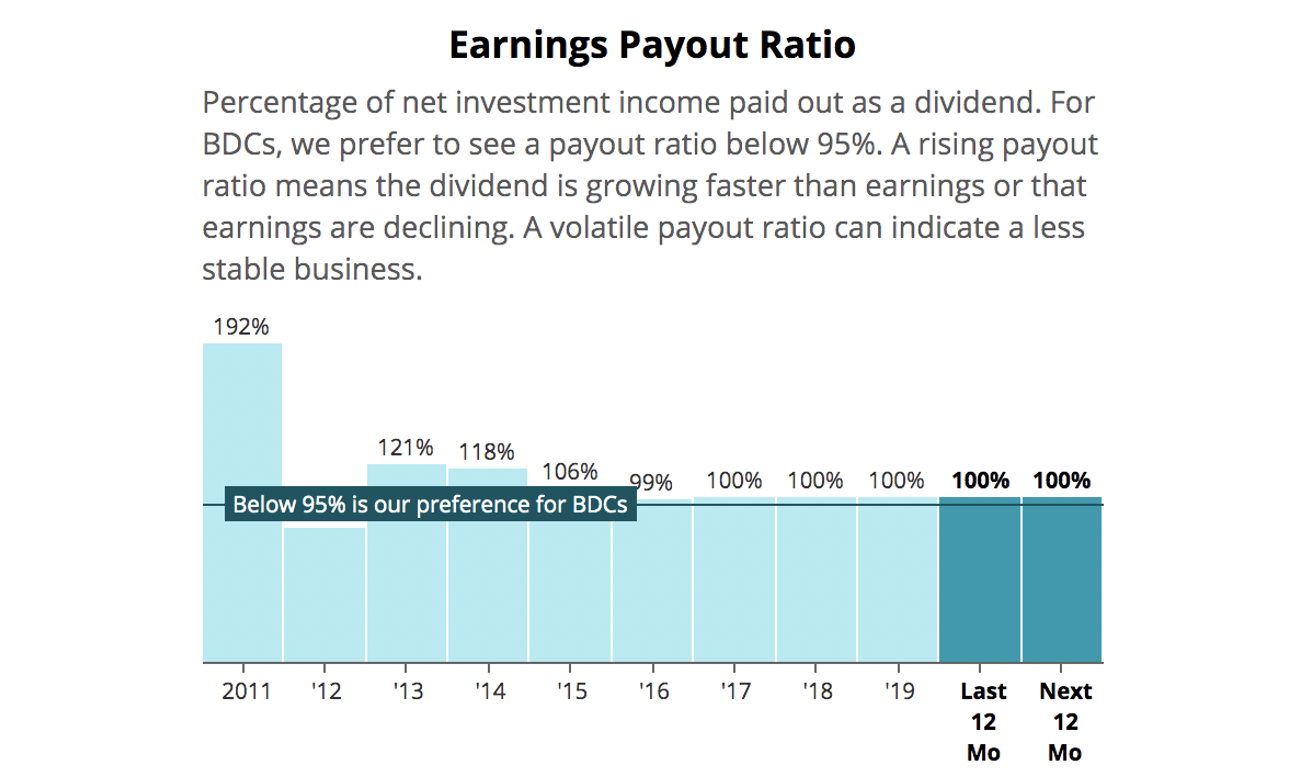

As you can see, the firm's payout ratio is otherwise expected to remain near 100% with its current portfolio of investments: Source: Simply Safe Dividends

Even if net investment income growth is realized slower than management expects, Solar's investment adviser has agreed to waive management incentive fees to the extent necessary for net investment income to cover Solar's current rate of monthly distributions throughout 2020.

With Solar's earning power (and payout ratio) expected to improve, coupled with the resilience of its loan portfolio thus far, we are upgrading the company's Dividend Safety Score from Very Unsafe to Unsafe.

Looking ahead, while over 80% of Solar's loans have interest rate floors tied to LIBOR, lower for longer interest rates will keep pressure on its interest income, and using leverage to grow the portfolio will reduce the firm's financial flexibility.

Until Solar's payout ratio improves to a healthier level and its loan investments demonstrate further resilience, an upgrade to Borderline Safe is unlikely given our long-term view of dividend risk.