On Tuesday, a federal appeals court issued Qualcomm a favorable ruling, reversing a May 2019 victory for the U.S. Federal Trade Commission which had accused the chipmaker of charging excessive royalty rates for its patents.

The 2019 ruling threatened to disrupt the lucrative licensing practices that historically generated over 70% of the company's operating profits.

As we discussed in December 2019, an unfavorable ruling had potential to harm Qualcomm's ability to pay dividends and invest in future technologies such as 5G.

This week's news officially removes a worst-case outcome for Qualcomm's core licensing business model, stabilizing the firm's cash flow outlook going forward.

In addition to its legal victory, Qualcomm in July resolved its royalty rate dispute with Huawei, the largest seller of smartphones in the world, and entered into a new long-term patent license agreement.

With its settlement with Apple also behind the company, CEO Steve Mollenkopf said that Qualcomm is now entering a period in which it has multiyear license agreements with every major phone maker, providing solid visibility for the foreseeable future.

As a result of these developments, which remove the firm's final legal overhangs, we are upgrading Qualcomm's Dividend Safety Score from Borderline Safe to Safe.

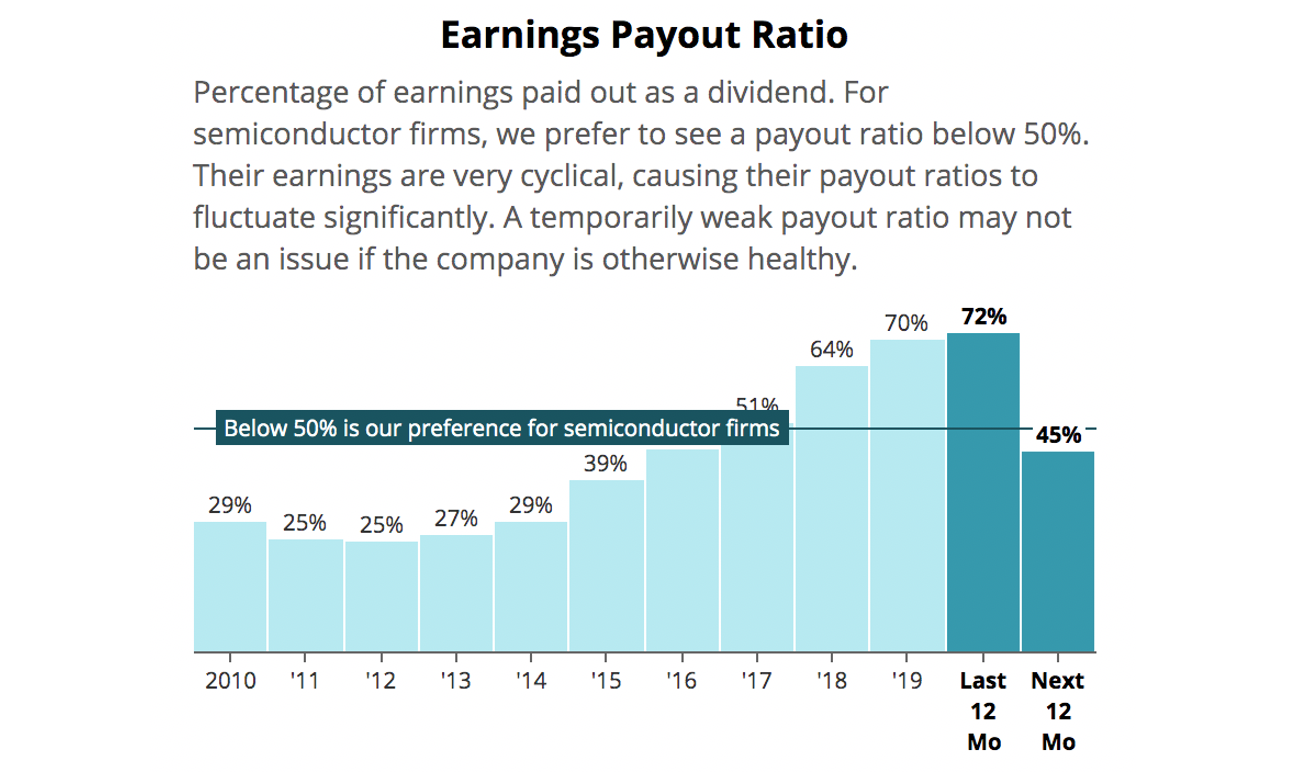

Looking ahead, analysts expect Qualcomm's earnings per share to jump about 60% over the next year, driven by a surge in demand for the firm's 5G smartphone chips.

Should this forecast materialize, Qualcomm's payout ratio would fall from more than 70% today to approximately 45%, a very reasonable level.

Source: Simply Safe Dividends

Coupled with the company's low leverage and strong investment grade credit rating, we expect Qualcomm's dividend to remain on solid ground going forward.

The firm's leading position in next-generation 5G technology could improve its dividend growth prospects, too. (Management last raised the dividend by 4.8% in April.)

While Qualcomm expects the overall phone market to shrink 10% this year due to COVID-19, increasing 5G penetration is expected to help the firm offset some of this weakness.

Qualcomm believes the addressable market for its chips has potential to grow 10% annually as 5G unlocks more opportunities across mobile, automotive, computing, and Internet of Things markets.

As orders continue ramping for 5G handsets and other applications, Qualcomm should be one of the largest beneficiaries and could see its earnings and dividend growth rates tick up to perhaps a high single-digit pace in the medium term.

With legal and growth challenges fading quickly after several challenging years, Qualcomm is reinforcing its status as a dominant cash cow and finally enjoying a strong run of performance in the stock market.

Investors who decide to continue the ride just need to be comfortable with the changing nature of Qualcomm's growth drivers (more dependent on chip sales with licensing revenue expected to stay flat) and the industry's general complexity (5G pace of adoption, market size, technological changes, etc).