Rising Leverage Puts More Pressure on Energy Transfer's Distribution

On May 8, we published a note discussing the fragile state of Energy Transfer's Borderline Safe Dividend Safety Score.

While the firm's distribution is expected to remain covered by cash flow, we were concerned about lower pipeline volumes and counter-party credit risk resulting from weak oil and gas prices.

These issues could materially impact Energy Transfer's ability to deleverage, threatening the firm's investment grade credit rating which sits one notch above junk and was issued a negative outlook by Standard & Poor's on May 12.

While likely a measure of last resort, reducing the distribution would free up more cash flow for debt reduction to protect the rating.

A couple of months have passed since then, and several developments have further clouded the outlook for Energy Transfer's distribution safety.

While an imminent distribution cut may be unlikely, we believe Energy Transfer's overall risk profile has increased.

In light of the developments discussed below, we are downgrading Energy Transfer's Dividend Safety Score from Borderline Safe to Unsafe.

Most recently, on July 6 a federal court ordered the Dakota Access Pipeline (DAP) to be temporarily shut down by next month in order to undergo an environmental review.

Energy Transfer owns a 38% stake in this $3.8 billion pipeline, which went into service in June 2017 and carries crude oil from North Dakota's Bakken shale basin to refining markets across the country.

As expected, Energy Transfer is fighting the ruling. Your guess is as good as mine regarding the final outcome and whether or not the pipeline will be allowed to operate during what could be a lengthy judicial process.

A yearlong closure would obviously reduce Energy Transfer's EBITDA, though perhaps not severely.

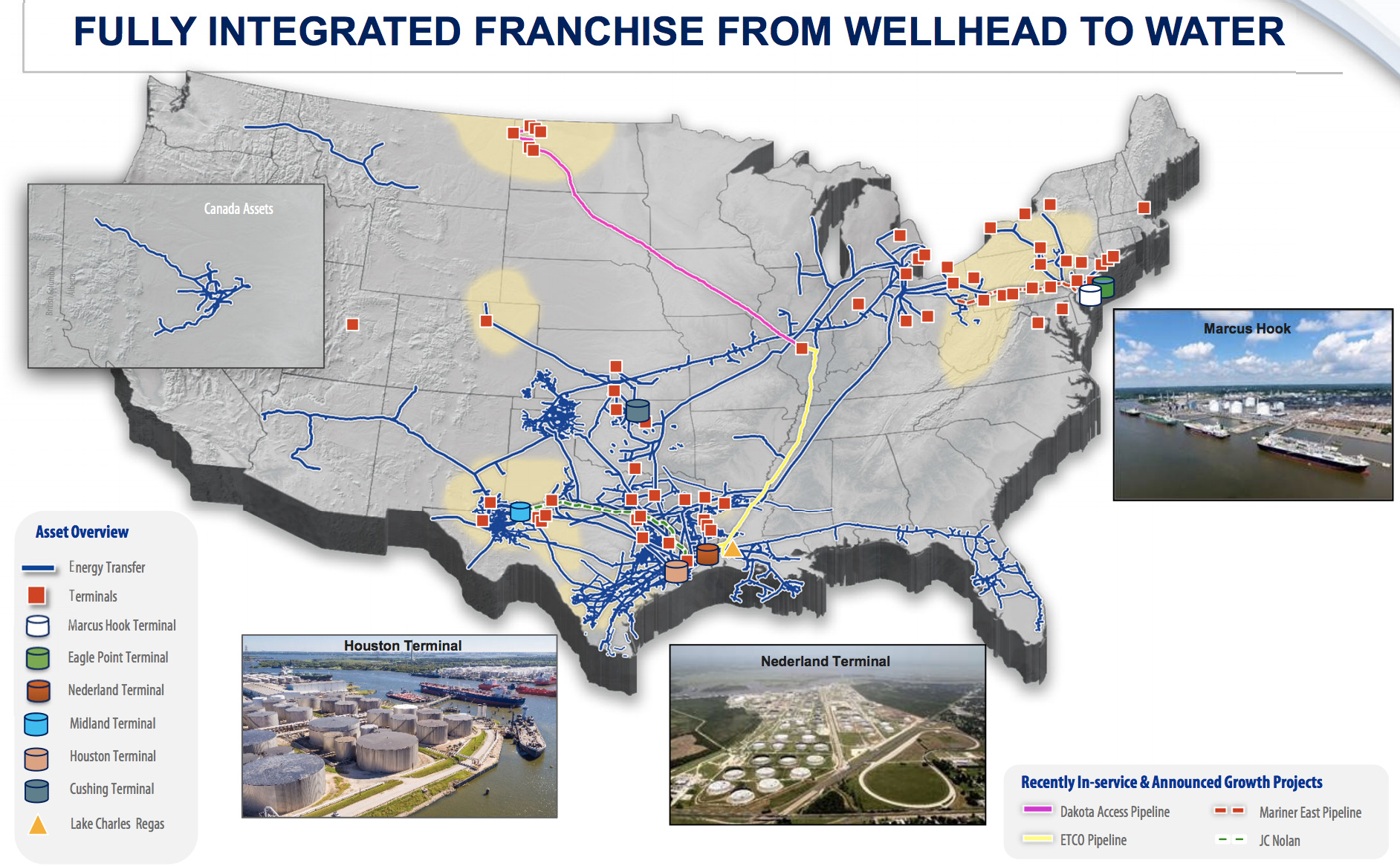

As you can see, the DAP (the purple line below) is just one part of Energy Transfer's expansive operations. Source: Energy Transfer Investor Presentation DAP's results are part of Energy Transfer's crude oil segment, which accounted for 25% of firm-wide EBITDA in 2019.

DAP represents about 11% of that segment's total pipeline miles, and closer to 17% if the connecting ETCO pipeline (yellow line above) is included.

In other words, while Energy Transfer may also have some assets on the Gulf Coast that touch products originating from the DAP, it's hard to imagine the firm's overall exposure to the DAP exceeding perhaps 5% of total EBITDA.

Losing that cash flow would slow Energy Transfer's deleveraging path, but this headwind alone probably would not necessitate a distribution cut.

The broader energy industry backdrop seems like the bigger swing factor, and the outlook for many shale producers remains dim.

Deloitte recently issued a study finding that about 30% of the major listed U.S. shale operators are "technically insolvent" at $35 per barrel oil, meaning their discounted future value is lower than their net liabilities.

Another 20% of those companies have "stressed financials" at $35 per barrel oil.

The worst of the shale bankruptcies and more extreme cost-cutting measures are probably yet to come.

As this plays out, distressed energy producers may increasingly try to cancel or renegotiate their midstream contracts to reflect the current commodity price environment.

In fact, on June 28, Chesapeake Energy, a fracking pioneer which filed for bankruptcy earlier this year, asked to cancel about $290 million of pipeline contracts it had with Energy Transfer.

The Federal Energy Regulatory Commission, which regulates U.S. pipelines, barred Chesapeake from changing its agreement with Energy Transfer.

More cases could be on the horizon, though. About 20% of Energy Transfer's customers already have junk credit ratings, and another 31% were only a notch or two away as of May.

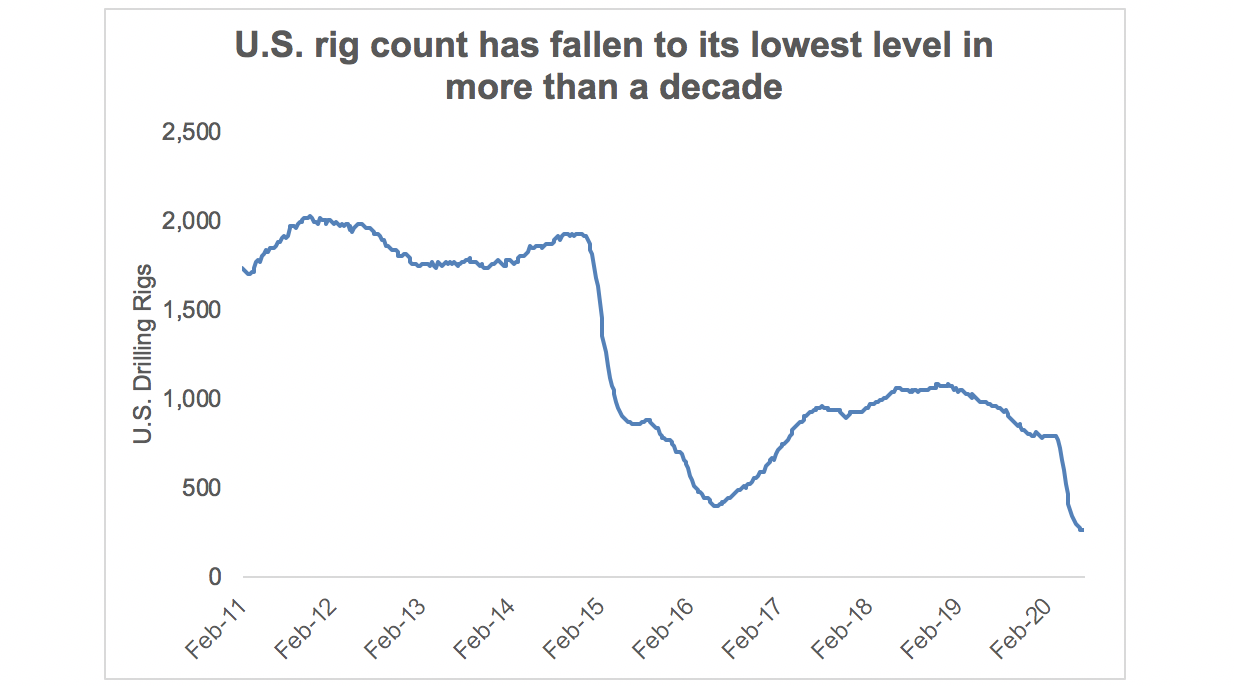

Falling energy production remains another concern. As measured by rig count, U.S. drilling activity for oil and gas has plunged to its lowest level in more than a decade, per data from Baker Hughes. Source: Baker Hughes, Simply Safe Dividends Without investing in new wells, many companies' output would decline by as much as 50% in just a year, according to data cited by The Wall Street Journal.

In other words, even if existing wells restart sooner than expected with oil now sitting near $40 per barrel, future production seems likely to continue decreasing or at least remain at weak levels.

(As of June 26, U.S. oil production was down 16% from its all-time high reached in mid-March.)

This means Energy Transfer's infrastructure will be less utilized, and some of its business segments such as Midstream (15% of EBITDA) and NGL & Refined Products (25%) are exposed to volumetric risk.

Overall, Standard & Poor's now believes Energy Transfer's leverage ratio will be about 5.5x this year, up from its previous view of 4.8x.

That does not include any impact from a potential temporary closure of the Dakota Access Pipeline, which we estimate could increase leverage by 0.1x to 0.2x.

The ratings firm sees leverage improving to about 5x in 2021 as Energy Transfer's growth projects come online and it begins generating positive cash flow after distributions and capital spending, directing excess cash towards debt reduction.

However, Standard & Poor's also warned that they could strip Energy Transfer of its investment grade rating if they thought its leverage ratio would be above 5x and the partnership "would not aggressively take steps to reduce its leverage" (i.e. cut the distribution).

Coupled with Dakota Access Pipeline uncertainty, the increasingly challenging backdrop for U.S. shale, and Energy Transfer's relatively poor reputation for executing cleanly on its growth projects, that's a low margin for error.

As we said in May, investors should understand the risks posed by Energy Transfer's balance sheet. Even if distributable cash flow covers the distribution, that doesn't necessarily mean that it's a safe bet, especially in this environment.

Given the persistent headwinds facing shale operators and Energy Transfer's more limited financial flexibility, conservative investors may want to move on if safe income is their top objective.

.png)