Government Aid Supports Omega's Tenants and Dividend For Now But Longer-term Uncertainty Remains

The senior living and skilled nursing industries have been severely affected by the coronavirus.

Not only are their residents more vulnerable if they contract COVID-19, but these facilities are designed for communal living, making it more difficult to control transmission of the virus.

As a result of the financial challenges caused by the pandemic, several healthcare REITs have already announced dividend cuts, including Ventas, Welltower, and Sabra.

With a dividend yield near 10%, Omega Healthcare has some income investors wondering if it could be next to slash its payout.

An imminent dividend cut seems unlikely, but the payout's safety beyond the next couple of months will depend on the depth and duration of the health crisis.

Unlike Ventas and Welltower, which generate around 30% to 40% of their income from operating their own facilities (exposing them directly to the industry's ups and downs), Omega's cash flow is driven almost completely by its ability to collect rent from its tenants.

This provides the REIT with some insulation from facility-level economics.

Omega's mix of business is also more focused on nursing homes (over 80% of revenue), which are receiving financial support from the government (unlike private-pay senior housing).

That aid is critical since operators of skilled nursing facilities (Omega's tenants) had razor-thin margins heading into the crisis, with around half of them failing to turn a profit.

Years of falling occupancy (oversupply), rising labor costs, and reimbursement drops contributed to the industry's decline in profitability.

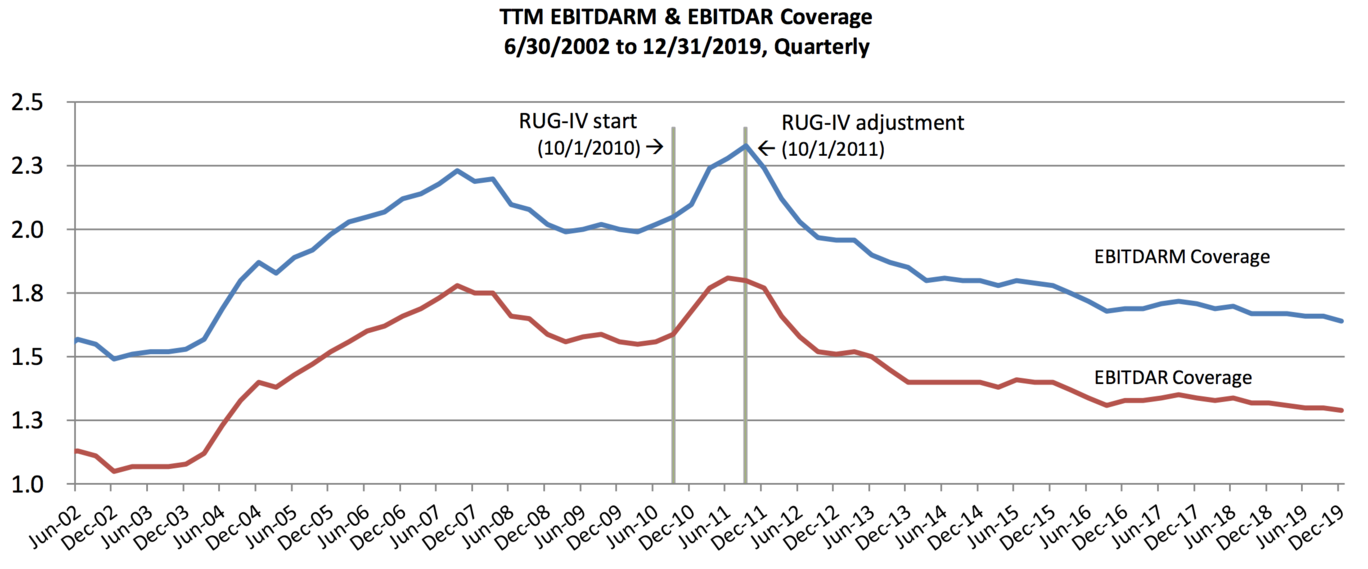

As a result, Omega's tenants have seen their rent coverage ratio (i.e. cash flow, or EBITDARM, to rent expense) decline steadily over the past decade.

Source: Omega Healthcare Investor Presentation

At the end of 2019, Omega's 70 tenants (largest is about 10% of rent) had EBITDAR coverage of 1.29x. All else equal, this implies that their pre-rent cash flow could fall by around 20% before they could no longer cover rent.

Unfortunately, the COVID-19 pandemic has potential to push many operators over the edge (before accounting for government relief packages).

As of early May, Omega said its skilled nursing tenants have already seen their occupancy decline by 3% to 6% since the health crisis started.

Canceled or deferred elective procedures reduced new residents coming from hospitals, and self-imposed admission bans at facilities with COVID-19 cases (about 38% of Omega's facilities have at least one case) weighed on occupancy the most.

Tenants have also experienced a surge in costs in the form of increased overtime and bonus pay, greater usage of personal protective equipment, enhanced cleaning and sanitation, increased testing, and less efficient modes of providing therapy in order to avoid the grouping of patients.

One of Omega's operators, Diversicare Healthcare Services, reported recently that it expects COVID-related expenses to account for around 2.5% of its revenue.

With many nursing facilities already operating with low single-digit profit margins or struggling to breakeven, these challenges could call into question their financial viability.

Fortunately, the federal government is stepping in since skilled nursing operators primarily receive revenue through reimbursements from government programs like Medicaid and Medicare (over 85% of Omega tenants' revenue).

The Coronavirus Aid, Relief, and Economic Security Act, or the CARES Act, was passed on March 27. That stimulus program included several programs for the nursing home industry.

Omega said the impact of this aid is approximately $150,000 to $175,000 per facility that provides Medicare services. Management believes this is enough to cover a couple of months of COVID-related operating expenses at most facilities.

So far, Omega hasn't had trouble collecting rent. On its May 5 earnings call, Omega said it had collected 98% of April rent, and the first week of May was tracking similarly.

However, management acknowledged that its tenants could be strained later this year if the virus still isn't contained and the government isn't as generous with continued aid.

"We know that there's still a fair amount of CARES Act money that hasn't been distributed. If that's distributed reasonably consistently with what we've seen and the pandemic clears out by some point in the summer, I think, put all that together, the impact isn't going to be that dramatic. But if things stretch out into the fall, it's going to be difficult without another round of government support, which, obviously, we can only guess whether that would happen or not."

– CEO Taylor Pickett

If such a scenario unfolded and increased pressure on the industry beyond the summer, we believe Omega's dividend could find itself on the chopping block.

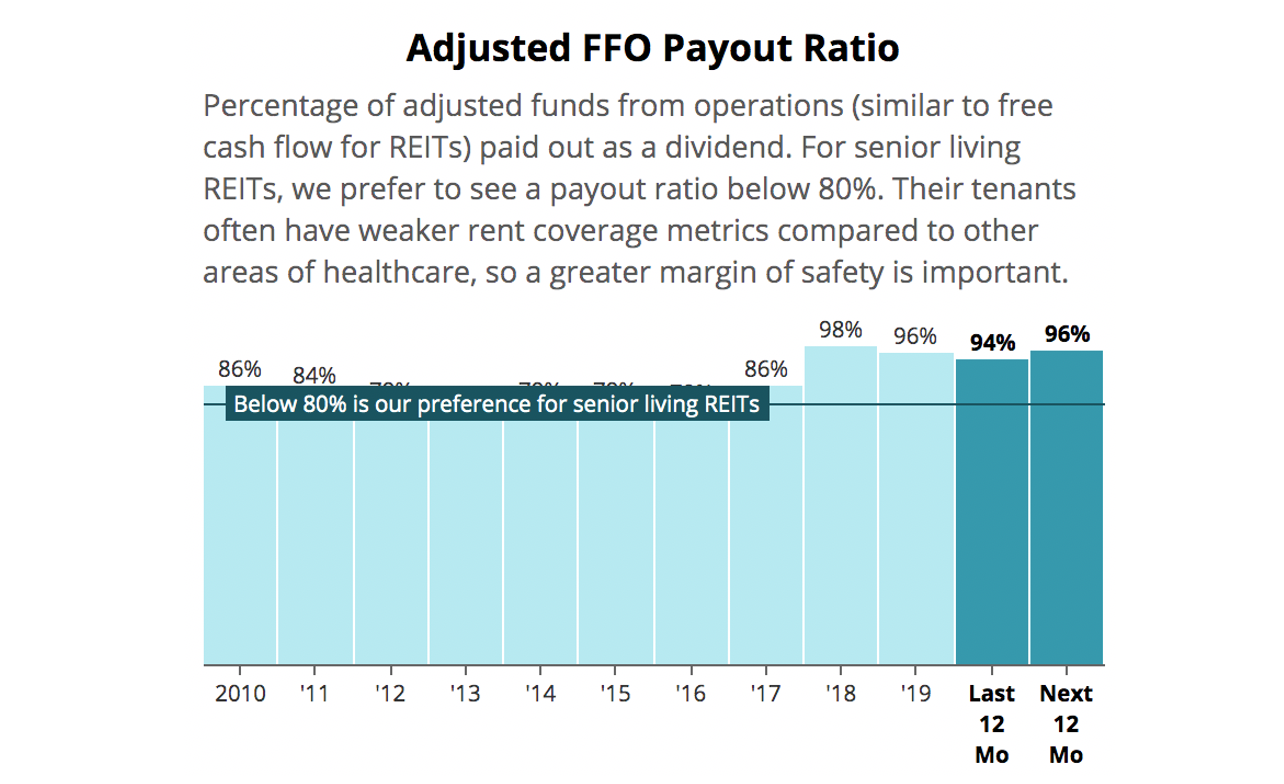

Based on the company's first-quarter results, we estimate that Omega's rent could fall only around 10% before its dividend would no longer be covered by cash flow.

Ratings firm Fitch estimated in late March that 7.5% of Omega's rent will be deferred in 2020, with a lesser impact in 2021. While there's a wide range of potential outcomes, that would put Omega's payout ratio near 100%.

Source: Simply Safe Dividends

Fortunately, Fitch doesn't expect that scenario to jeopardize Omega's BBB- investment grade rating, which helps the REIT maintain access to debt markets but sits only one notch above junk.

Omega's overall financial position looks reasonable, too. The firm had about $1.1 billion of cash and credit facility availability as of April 30.

Omega also has no material debt maturities until 2022, and the firm's capital needs are minimal since it's unlikely to make major growth investments in this environment.

Less than 1.5% of Omega's leases expire through 2021 as well, and the company has significant cushion with all of its debt covenants.

Given this backdrop and its stable rent collection rates so far, Omega "comfortably" declared its regular dividend payment in April.

Management will likely continue down that path so long as government-sponsored relief funds can offset the impact of the pandemic on its tenants (and keep most of them healthy enough to pay rent).

However, the unknown timeframe of the pandemic and the unknown level of future government support make this a delicate situation, which Omega's low Borderline Safe Dividend Safety Score reflects.

Omega's valuation doesn't appear very demanding, providing some compensation for these uncertainties, but current shareholders should decide how comfortable they are with these risks.

Conservative income investors may want to look at other stocks. We will continue monitoring the situation and will provide updates as needed.