Chevron Expects Dividend to Remain Safe Through at Least 2021 Even if Oil Remains Weak

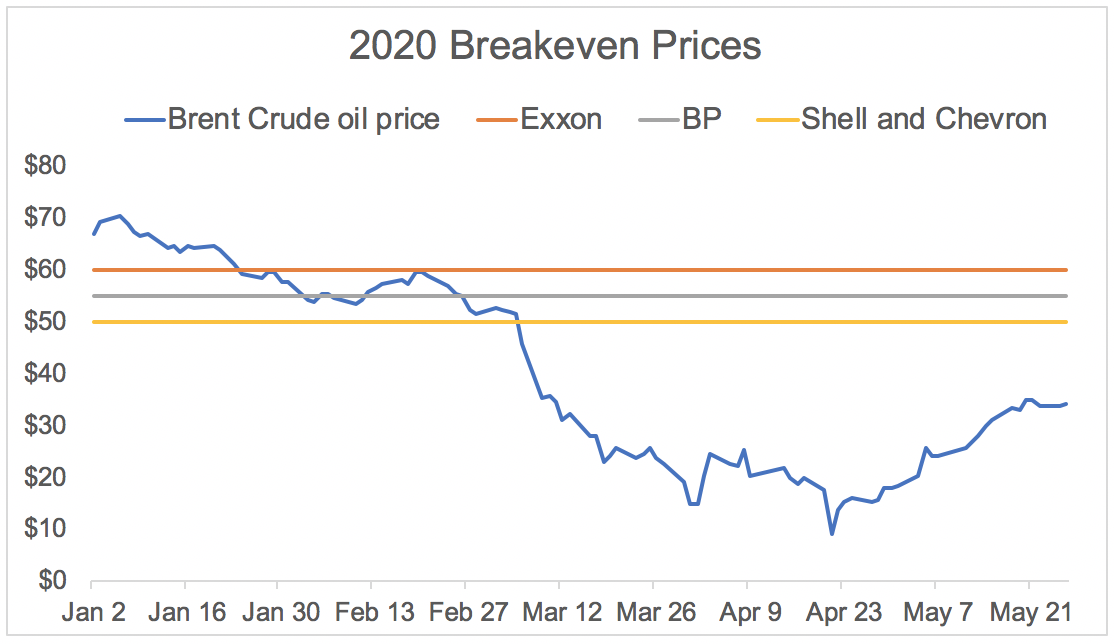

None of the oil majors can cover their capital spending and dividends at today's oil price, even after slashing their investment plans.

Oil needs to be closer to $50 to $60 per barrel for these companies to breakeven on their obligations, according to data from Bloomberg.

Source: Bloomberg, U.S. Energy Information Administration, Simply Safe Dividends

The price of oil has started to rebound off its April lows with lockdowns being lifted and supply falling. But at today's price near $39 per barrel, the oil majors will continue burning through cash.

With a breakeven price near $50 per barrel, Chevron is no exception.

Facing these realities, Shell on April 30 announced its first dividend cut since World War II. Investors are worried other oil majors may soon follow suit.

Chevron is the only oil major with a Safe Dividend Safety Score, driven by the firm's strong balance sheet.

The dividend aristocrat has not cut its dividend since 1912, and even in the current oil price environment, we continue to believe a dividend cut is unlikely for the foreseeable future.

Chevron backed up this view in May following its first-quarter earnings report and annual shareholders meeting.

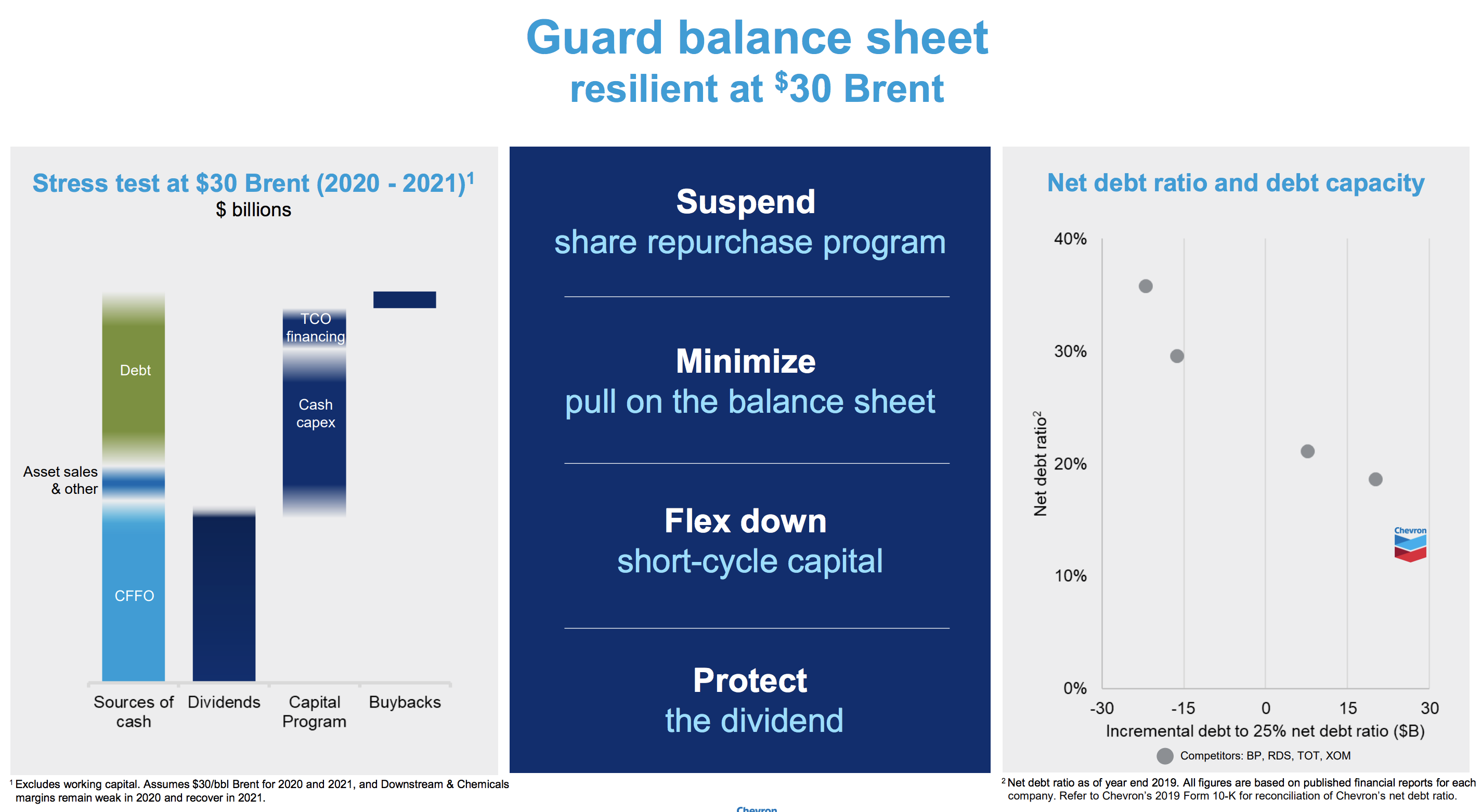

Knowing dividend safety would be a hot topic, management shared the results of a cash flow stress test Chevron conducted.

The test assumed Brent oil averaged $30 per barrel in 2020 and 2021 and the firm's current dividend was maintained.

While cash flow from operations (CFFO) would cover the dividend in this environment, debt and asset sales would be required to cover the company's capital spending.

The chart on the left shows Chevron's estimated sources and uses of cash under its two-year stress test.

Source: Chevron Investor Presentation

Chevron maintained low leverage prior to the pandemic. As a result, management is willing and able to take on more debt to cover its cash flow deficit and protect the dividend.

At the end of the first quarter, Chevron's net debt to capital ratio was 14%. For perspective, the firm's peers have ratios closer to 20% to 30%.

Chevron estimates that its net debt to capital ratio would remain under 25% even after the incremental borrowing required in its two-year stress test.

Management said "that is not an uncomfortable level to be at" and noted that over time the firm had planned to move its gearing into the 20% to 25% range anyway.

After all, only a few years ago Chevron's net debt to capital ratio was above 25%. The company has demonstrated it can manage leverage in this range, should the price of oil remain lower for longer.

Chevron's financial assessment seems reasonable. In March, we estimated that Chevron could potentially maintain its dividend for two years or longer before the firm's net debt to capital ratio would reach an uncomfortable level.

In addition to its balance sheet capacity, Chevron has strong liquidity. The company holds $8.5 billion of cash and has over $20 billion of available borrowing capacity through its credit facilities. (For context, the dividend costs $9.6 billion.)

The company maintains an AA credit rating from Standard & Poor's as well, helping it continue accessing debt markets on reasonable terms. With less than $5 billion of debt maturing through 2021, refinancing risk is low, too.

And unlike some of its peers, Chevron has also been very vocal about prioritizing its dividend, which management said is "vital" to the firm's shareholders:

"We've got a long-standing financial framework that has the dividend as our #1 financial priority...

"On our first quarter earnings call about a month ago, we laid out a stress test, where we showed the financial state of the company and our balance sheet if we have 2 years of $30 Brent crude pricing, continue to invest in our business, sustain the dividend and it shows that we still exit 2021 with a very strong balance sheet and good financial health [including a net debt to capital ratio below 25%]. So that was an attempt to lay out for investors the the safety of our dividend and the actions we're taking to protect it."

– Chairman and CEO Mike Wirth, Chevron's Annual Shareholders Meeting

Overall, we expect to maintain Chevron's Safe Dividend Safety Score due to the firm's solid balance sheet.

This positions the company to endure a couple of years of really tough pricing without threatening its dividend, as long as management remains comfortable increasing leverage to a reasonable level.

But like the other oil majors, Chevron eventually needs higher oil prices to sustain its capital spending program and dividend. No business can increase leverage forever, especially for the sake of maintaining a dividend.

Oil prices above $60 per barrel are required by most major oil-producing nations to balance their budgets, but how long it takes for fundamentals to normalize is anyone's guess.

Supply side dynamics are extremely complex thanks to disruption caused by U.S. shale players, and demand recovery is still in the early days as the pandemic's impact lingers.

For the dividend's sake, it's important that conditions in the oil market improve meaningfully by the end of next year.

Should a price recovery fail to occur or Chevron's balance sheet runway materially shorten for any reason, we would consider downgrading its Dividend Safety Score.

For now, income investors can rest a little easier knowing that Chevron is arguably the best positioned oil major to protect its dividend and has made that its first priority.