Sharp Decline in Elective Procedures Places Pressure on Stryker's Payout

The outbreak of the novel coronavirus is coming head-to-head with Stryker's 28-year track record of paying uninterrupted dividends.

Stryker (SYK) designs and manufactures devices and supplies used in a wide variety of medical procedures. 73% of Stryker's sales are generated in the U.S.

In March, the Centers for Medicare and Medicaid Services (CMS) recommended that elective surgeries and other non-essential medical procedures be postponed in order for hospitals to preserve space and equipment for COVID-19 patients.

Recently, many hospitals have begun resuming non-essential procedures. But it's possible, if not likely, that many people will continue to avoid hospitals to reduce their risk of exposure to the coronavirus.

So far, the shock to sales of many medical supplies has been extraordinary.

Quest Diagnostics (DGX), a supplier of diagnostic tests for everything from cancer to allergies, reported last week that volumes in April had declined 50-60%.

While Stryker and Quest have different products, both generate much of their revenue from elective procedures. As a result, it wouldn't be surprising if Stryker were experiencing similar volume declines on the order of 50%.

Moreover, Stryker generates a little less than a third of revenue overseas, where countries hit hard by the pandemic like China and Italy saw elective surgeries plummet as much as 90% in February and March, according to MassDevice.

Fixed costs are high for Stryker, making profits highly susceptible to even moderate swings in revenue. Large manufacturing facilities must be maintained regardless of demand, and there's significant overhead in personnel.

In 2019, operating expenses totaled about $7 billion, a little less than half of the Stryker's $15 billion in revenue. Costs of good sold (raw materials, manufacturing labor, etc) accounted for another $5 billion but are more variable in nature.

Assuming most of Stryker's operating expenses aren't easily reduced in the short term, it's not hard to see how a sharp decline in revenue could greatly strain profits this year.

For context, Quest's CEO said he doesn't expect Quest to turn a profit in 2020, though the range of outcomes are wide. Much depends on how eager people are to treat their aches and pains against the perceived risk of leaving home.

Stryker is working to design and market important products for COVID-19 patients such as beds and respirator decontamination devices. At this point, however, it doesn't seem likely that these products will make a big impact on sales.

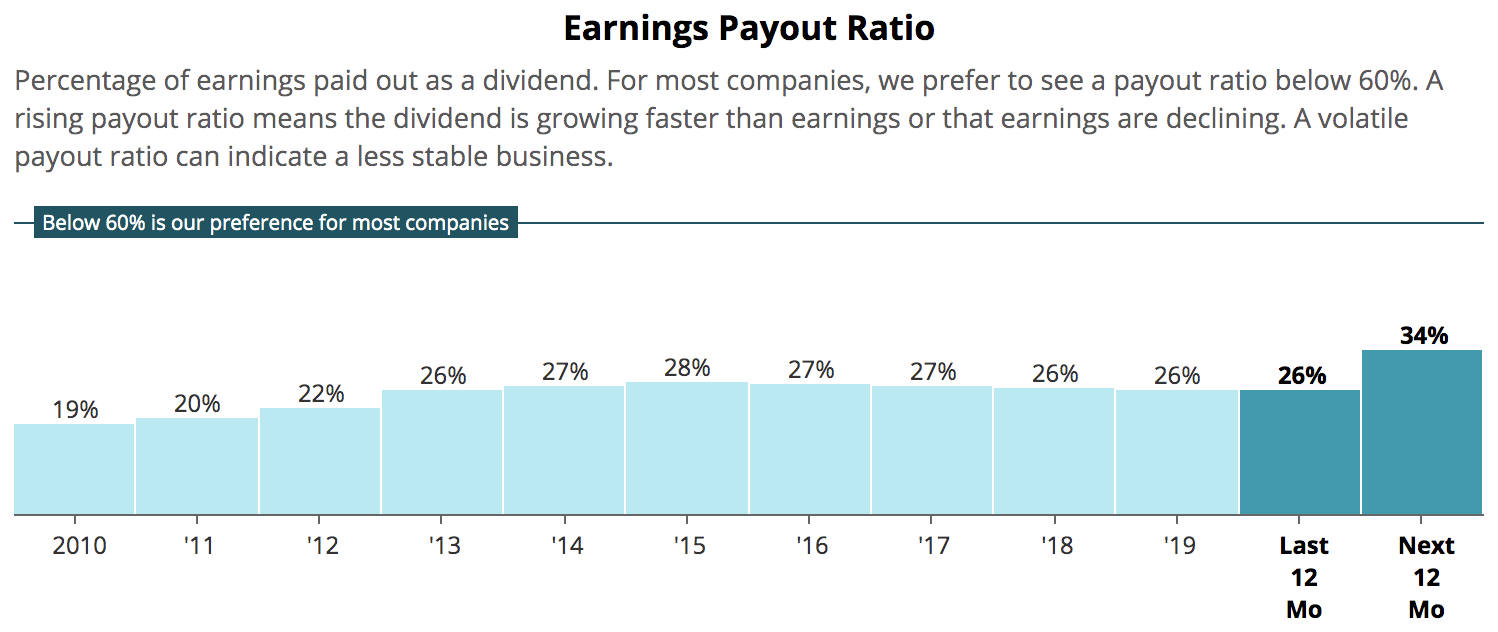

The dividend hasn't been a major strain on Stryker's cash flow in the past, as evidenced by the firm's low payout ratio prior to the pandemic.

Source: Simply Safe Dividends

In addition, Stryker had $4.4 billion in cash on hand as of January, while the current dividend costs just $900 million annually.

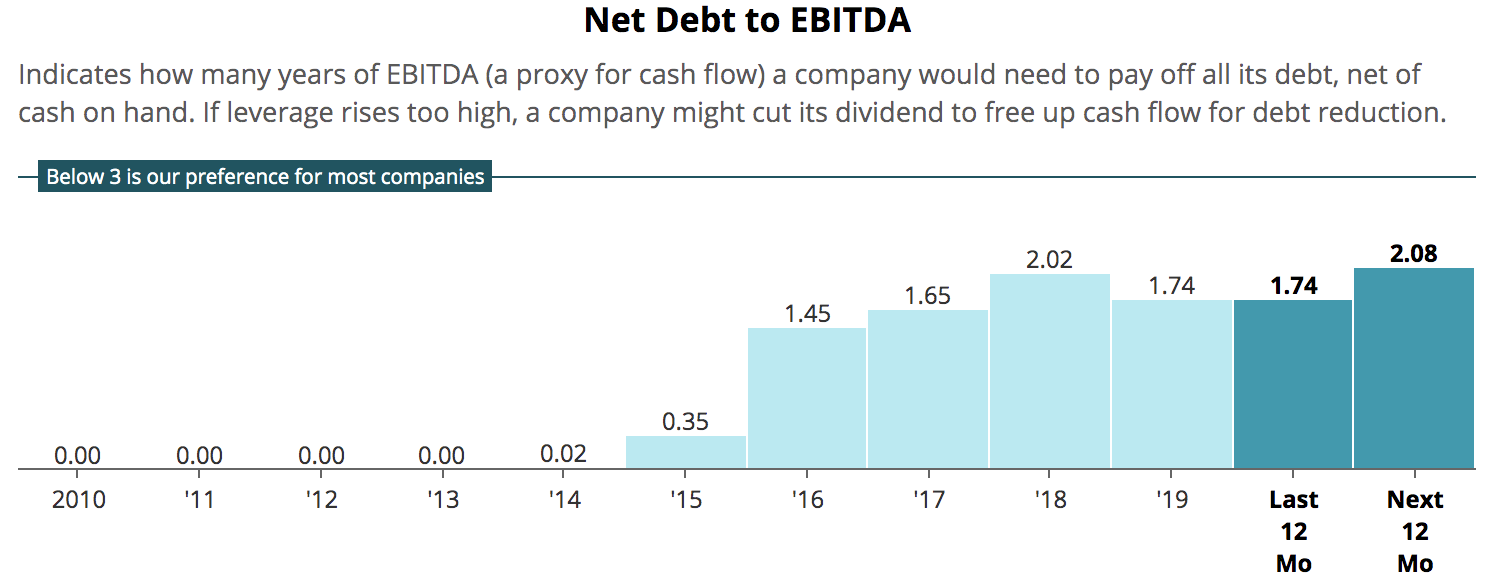

However, Stryker agreed in November to acquire Wright Medical Group for $5.4 billion. Once closed later this year, the debt-funded deal is expected to raise Stryker's leverage (debt to adjusted EBITDA ratio) from under 2x to 3x.

Source: Simply Safe Dividends

Due to the increase in leverage, Standard & Poor's downgraded Stryker's credit rating from A to A-. While A- is still an excellent credit rating, management said that paying off debt would be a near-term priority for the company.

If management sees cash flow take a major hit and isn't optimistic about a quick rebound, Stryker may decide to cut the dividend to prioritize deleveraging.

In recognition of the increased likelihood of a dividend cut resulting from an unprecedented shock to the firm's cash flow and near-term needs to deleverage, we are downgrading Stryker's Dividend Safety Score to Borderline Safe.

While Stryker has a long track record of paying growing dividends, the company's commitment to the dividend has never been tested as it is now.

This downgrade isn't necessarily a reason to sell. With a dividend yield just north of 1%, Stryker's dividend isn't a major contributor to the stock's total return.

Furthermore, Stryker's long-term outlook arguably hasn't changed. The pandemic will eventually end, and elective procedures can only be put off for so long.

A swift rebound in sales in the next couple years seems likely, and 2020 may turn out to be nothing more than a blip in the company's long-term trajectory.

Stryker reports earnings this Thursday, April 30. If results over the next quarter or two come in better than expected, we would consider upgrading Stryker's Dividend Safety Score quickly.

.png)