Lowe's Remains Open; Dividend Continues to Look Safe

According to the Wall Street Journal, over 38,000 stores around the U.S. have temporarily closed in response to the coronavirus outbreak.

Deemed to sell essential products, Lowe's has not.

In fact, two associates we spoke to (including one in Chicago where a shelter-in-place order had gone into effect) described their stores as "slammed" and "really busy".

At this point, the greatest risk to Lowe's near-term outlook appears to be the prospect of a recession, which could result in less foot traffic and fewer sales. Lowe's revenue is sensitive to consumer spending.

But a recession — perhaps especially one where people are more likely to want to stay home and work around the house — seems unlikely to threaten the dividend.

Impressively, Lowe's has grown its dividend for 57 years in a row, a stretch during which Lowe's business would've experienced many challenges.

For instance, Lowe's same-store sales declined around 7% in 2008 and 2009 after the housing bubble burst (a tremendous shock to Lowe's customer base), but Lowe's was still strong enough to grow the dividend each of those years.

Of course, this time around could be different. The forthcoming downturn may turn out to be more severe than the financial crisis, or Lowe's customer base (homeowners, renters, professional contractors) may be affected even more than they were during the financial crisis.

No one knows yet — we're still in the early innings. But based on what we do know, Lowe's dividend still appears safe.

Indeed, Lowe's declared its regular quarterly dividend last Friday. Management had time to assess the current environment and felt confident going ahead.

Whatever may come, supporting Lowe's dividend during this potential rough stretch is the firm's healthy payout ratio and balance sheet coming into the crisis.

In February, management projected that the business would generate $4.9 billion in free cash flow this year. Lowe's dividend costs $1.6 billion, which implies a 33% payout ratio. There's decent room for Lowe's to underperform before the firm would need to take on additional debt to cover the dividend.

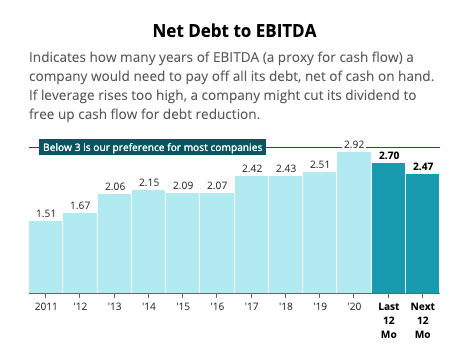

If Lowe's did need to tap debt markets to shore up funding for the dividend, the company's investment grade BBB+ credit rating and reasonable leverage ratio would give management that flexibility.

Source: Simply Safe Dividends

Equally important, Lowe's long-term outlook remains bright. Lowe's scale yields significant competitive advantages, and e-commerce poses less of a threat to the company than to many other retailers.

As a result, so long as conditions don't deteriorate significantly, management should feel comfortable remaining committed to the dividend.

That said, the world doesn't have a playbook for addressing pandemics in modern society. It's unclear how far governments will go to stop the spread of the novel coronavirus and what the economic consequences will be of their decisions.

We will be monitoring Lowe's earnings results and the broader economic outlook. For now, Lowe's dividend continues to look safe.