Regulated utilities are often a core component of a conservative income portfolio thanks to their predictable earnings, generous dividends, and defensive profile. However, PPL (PPL) has been anything but defensive lately.

The stock has lost 26% over the past year, including dividends. While rising interest rates have weighed on the performance high-yielding, slow-growing companies, the broader utilities sector (XLU) is down just 5% during this time. Meanwhile, the S&P 500 Index (SPY) has returned 16%, outperforming PPL by an astounding 42%.

Simply put, PPL has continued to be a big disappointment.

The one thing PPL has going for it is that management has maintained and even increased its dividend during this period. When combined with its plunging stock price, PPL’s dividend yield rocketed through its previous multi-year high around 5% in early 2018 and now sits just north of 6%.

Even for a utility, that’s a very high yield and suggests investors are worried about something big going wrong.

In these situations, there is often an obvious and substantial risk factor that has emerged.

However, in PPL’s case, it looks to be business as usual at first glance. The company’s first-quarter operating revenue and adjusted EPS grew 9% and 19%, respectively, when PPL released results in early May.

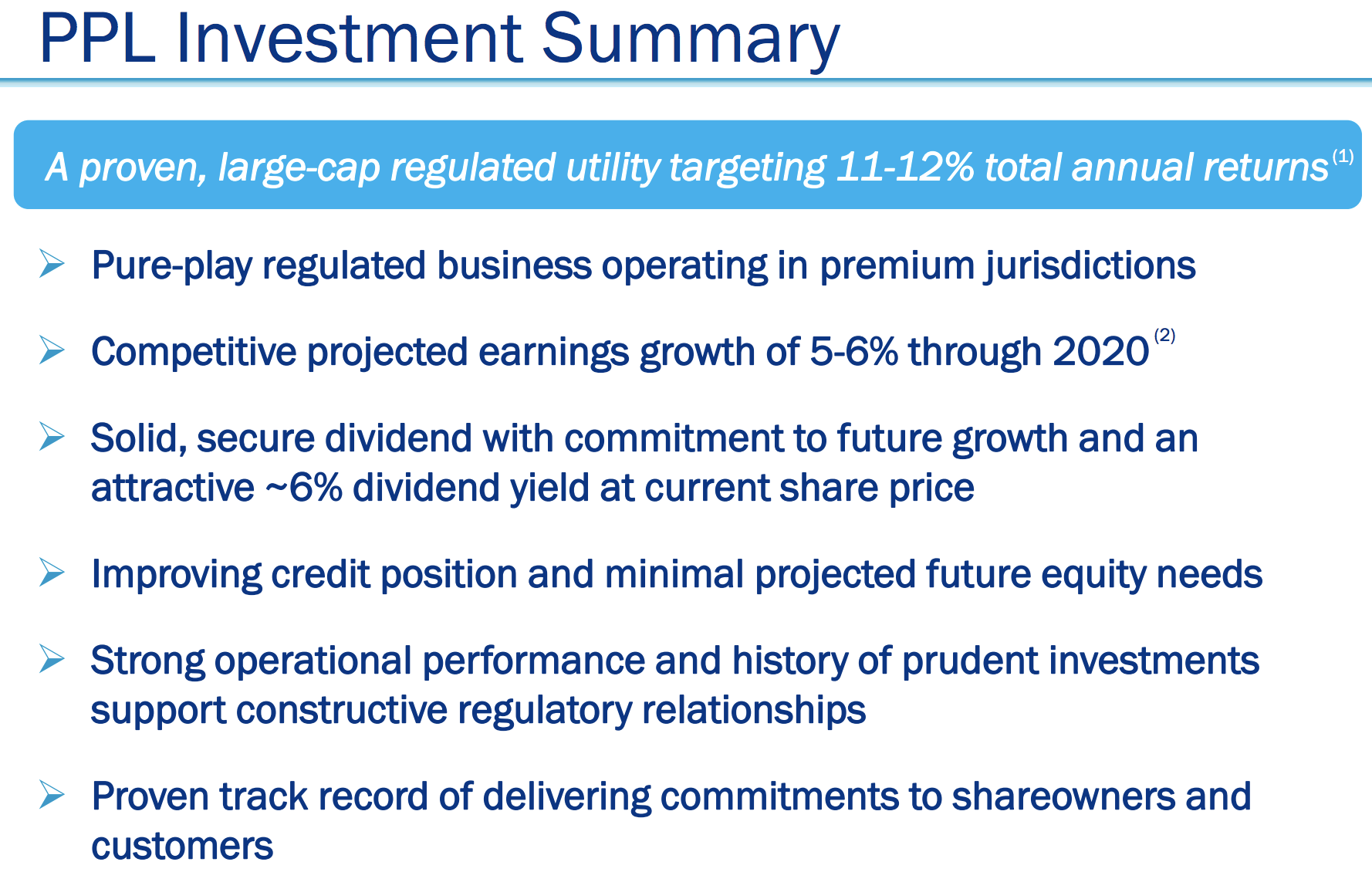

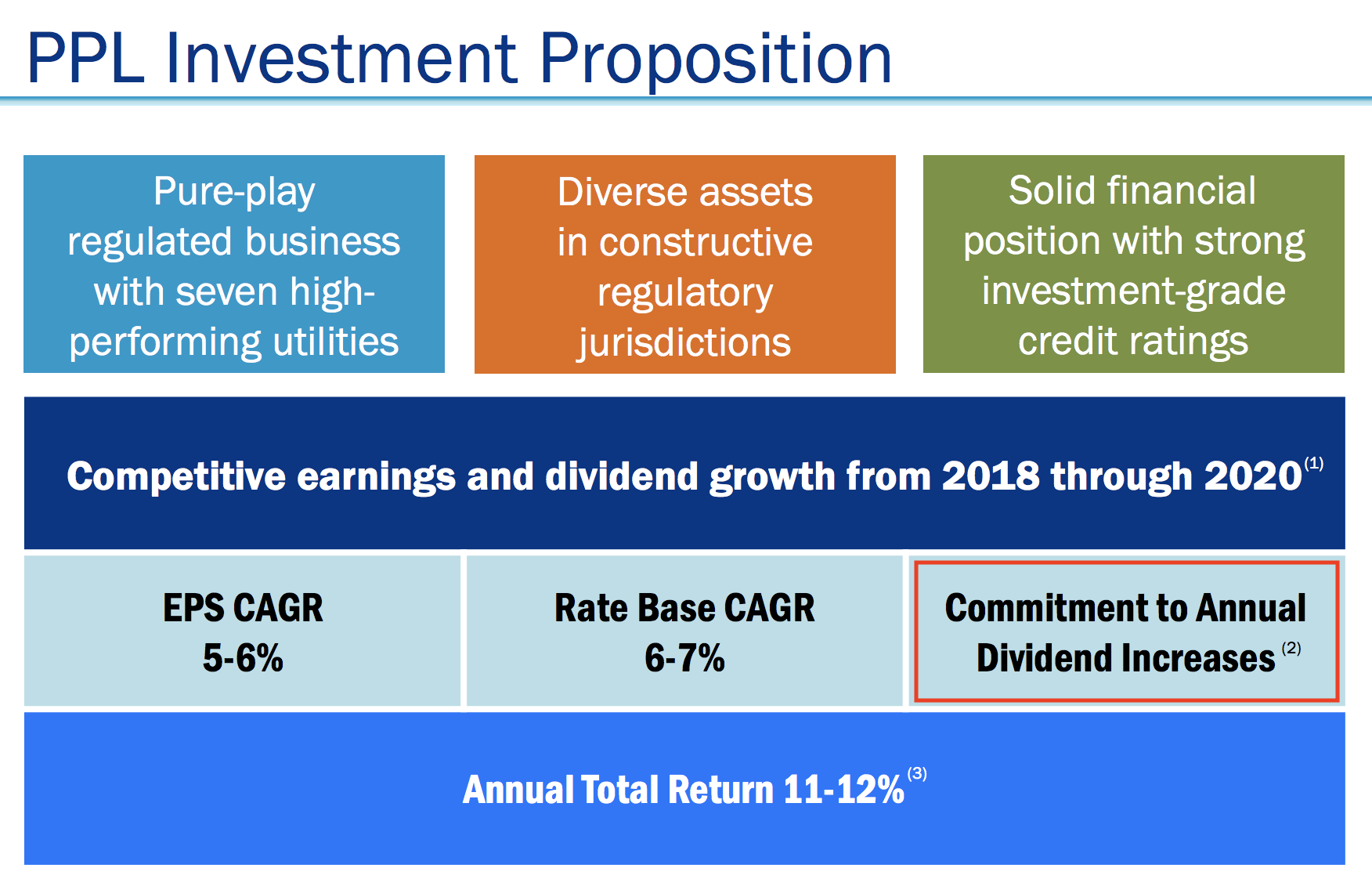

Meanwhile, just this past week management affirmed the company’s 5-6% annual EPS growth target through 2020, backed its commitment to grow the utility’s “solid, secure dividend”, and highlighted the firm’s “improving credit position” (you can download PPL’s latest investor presentation here).

Source: PPL Investor Presentation

Sell side analysts continue to forecast mid-single-digit annual EPS growth for the company over the next few years as well.

But all may not be well for PPL. At least not when you look out past the next five years.

Specifically, in recent years PPL has generated around half of its earnings from the four electricity distribution networks it operates in the United Kingdom (U.K.).

As a regulated utility, PPL’s distribution networks operate in regions where they largely have a monopoly on network services. To ensure consumers pay a fair price and get the reliable energy services they require, the Office of Gas and Electricity Markets (Ofgem) is the U.K.’s energy regulator and sets price controls to cap the revenue PPL can recover from its investments.

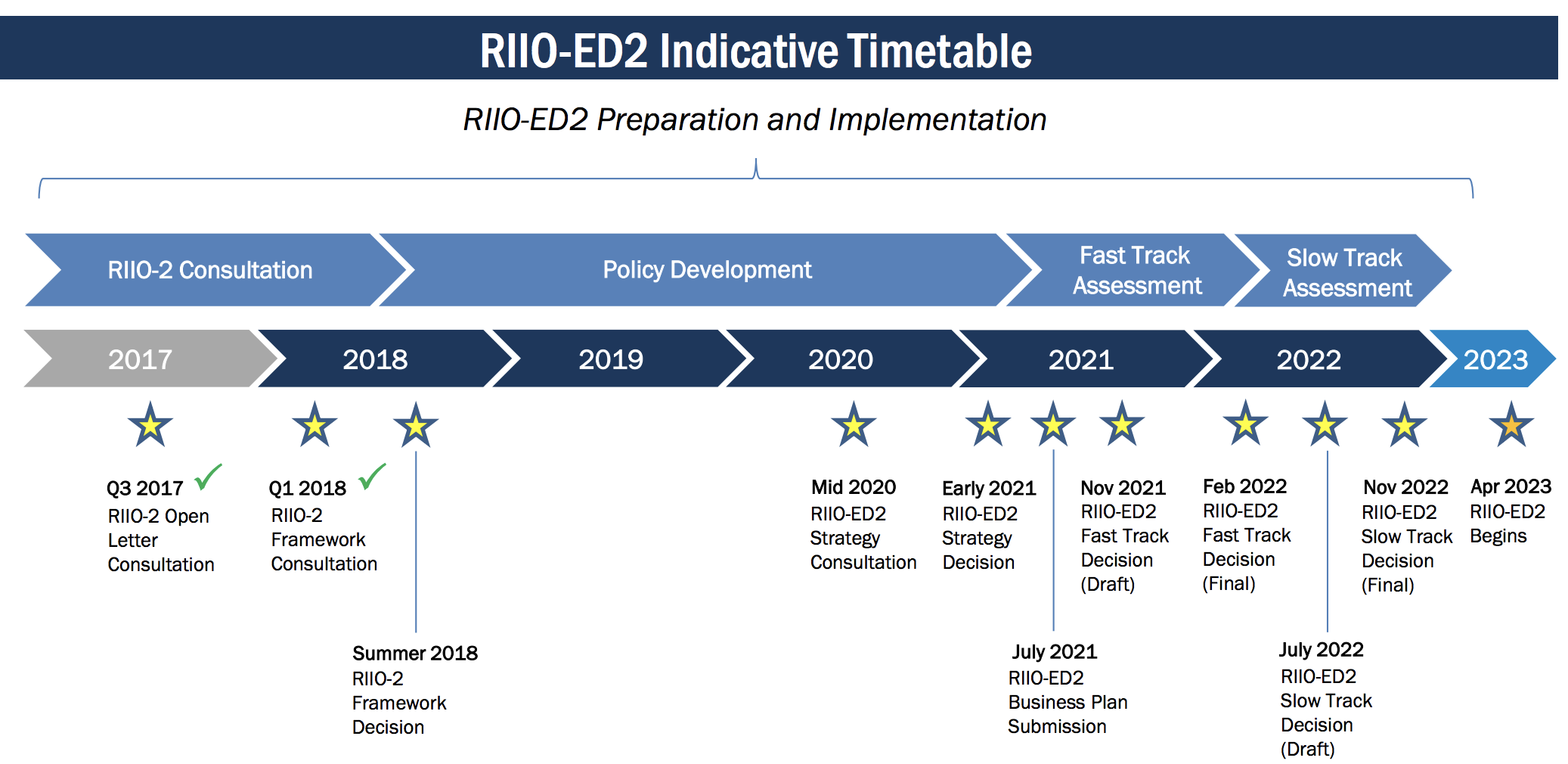

Ofgem sets price controls using the RIIO framework. RIIO involves setting Revenue using Incentives to deliver Innovation and Outputs. In 2015, Ofgem set price controls for electricity distribution over an eight-year period, allowing network companies to recover a set amount of revenues in exchange for providing safe and reliable services.

In other words, the current framework that PPL’s U.K. business has been operating under has effectively set base revenues through March 2023, providing a predictable rate of return on its projects so long as no major revisions are made.

Investors were anxious that Ofgem would decide to hold a mid-period review of the current price control in place for electricity distribution, which is the biggest driver of a utility’s earnings. To help with its decision of whether or not to conduct a mid-period review, during their consultation with various stakeholders in the industry regulators included an evaluation of resetting profitability targets for the country’s utility networks.

The fact that this option was included as part of the mid-period review’s consideration really spooked investors. After all, its intention was to cut network revenues by more than $850 million in an effort to reduce costs for consumers at the expense of utility shareholders.

However, Ofgem worried that the damage such an action would cause to investor confidence in utilities would more than offset the cost benefits. That’s because utilities would face much higher financing costs (lower share price, higher cost to borrow) that would need to be accounted for in their allowed return.

In late April 2018, after consulting various stakeholders, Ofgem announced it would not launch a mid-period review, keeping the current framework (including price controls for electricity distribution) in place for the next five years.

Therefore, PPL’s outlook over at least the next couple of years appears stable, and its dividend seems likely to remain on solid ground. However, the picture has certainly become murkier the further out you go, and I believe that is why the market has punished PPL so severely in recent months.

Specifically, Ofgem is already looking ahead to the next regulatory period that begins in 2023 for electricity distribution networks such as PPL. Plenty of details remain to be worked out, but all signs indicate that the regulatory framework that will ultimately go into place in five years will deliver much lower returns of regulated utilities.

Now on one hand, the government’s price controls have already done a nice job protecting consumers over the years, lowering some of the incentive to really rock the boat. Since the mid-1990’s, the cost of transporting a unit of electricity around Britain has fallen by 17%. The country’s electricity network charges per unit are actually lower than those in France or Germany as well.

Unfortunately, there also appears to be a lot of inefficiency in the system that Ofgem is determined to reduce. There is a fascinating 153-page document overviewing some of the proposals Ofgem has floated out for the next regulatory period that you can read here.

Much of the language is concerning for regulated utilities and their shareholders. Here is one notable excerpt:

“Returns across companies have been higher than we expected and do not reflect the low level of risk these companies face…When companies profit from delivering excellent service or finding new and innovative ways of reducing costs, consumers benefit too because the gains are always shared and they get better serviced. But if companies profit from other factors (such as forecasting errors), then nobody benefits, other than shareholders…This will be a tougher price control for network companies.”

Essentially, investors are probably concerned that PPL and other utilities have been overearning in the U.K. thanks to the various inefficiencies built into the price control models that were implemented by Ofgem around five years ago.

Following Ofgem’s decision to forgo a mid-period review, Victoria MacGregor, director of energy at U.K. charity network Citizens Advice, issued a statement in UtilityWeek.co that gets at this concern:

“Ofgem’s decision not to undertake a mid-point review of the current price controls for electricity distributors is very disappointing. Today’s announcement was a missed opportunity for the regulator to put right decisions that have effectively handed these companies billions in unjustified profits. Electricity distributors have five more years of the current price controls, meaning five more years of excessive profits.”

Ofgem appears very determined to strip any excess profits out of the system, ensuring that these utilities earn no more than a fair return to save consumers as much as possible. Many network companies are earning higher than expected returns operating under the current framework and have voluntarily returned over $800 million to customers in an effort to appease the government.

In fact, PPL’s operating company announced a $100 million voluntary return on April 30, 2018, after one of its infrastructure projects was cancelled (otherwise the company could have pocketed the money without incurring any costs, demonstrating some of the current framework’s weakness).

But no amount of voluntary returns will satisfy Ofgem. The government wants a framework in place that no longer results in a meaningful level of excess profits for utilities in the first place.

In its latest presentation to stakeholders, the regulator proposed a cost of equity range (the amount utilities pay their shareholders) between 3% and 5%. As Ofgem stated, “This is the lowest rate ever proposed for energy network price controls in Britain.” Ofgem also proposed to refine how it sets the cost of debt so that consumers continue to benefit from the fall in interest rates rather than the utilities.

PPL’s operating companies in the U.K. have a cost of equity of 6.4% under the current framework, so Ofgem’s proposal represents a fairly steep reduction. Investors hate uncertainty, and their confidence in PPL’s long-term profitability has certainly been rattled by Ofgem.

Unfortunately, it will likely be a while until final clarity is provided. Ofgem will solidify the framework for setting the next price controls this summer, but the regulator’s final view on price control allowances, including final cost of equity parameters, will not be published until 2020, at the earliest.

Source: PPL Investor Presentation

Management estimates that a 100-basis point change in nominal U.K. returns its utilities can earn would result in a $50 million change in cash from operations when the next regulatory framework begins in 2023.

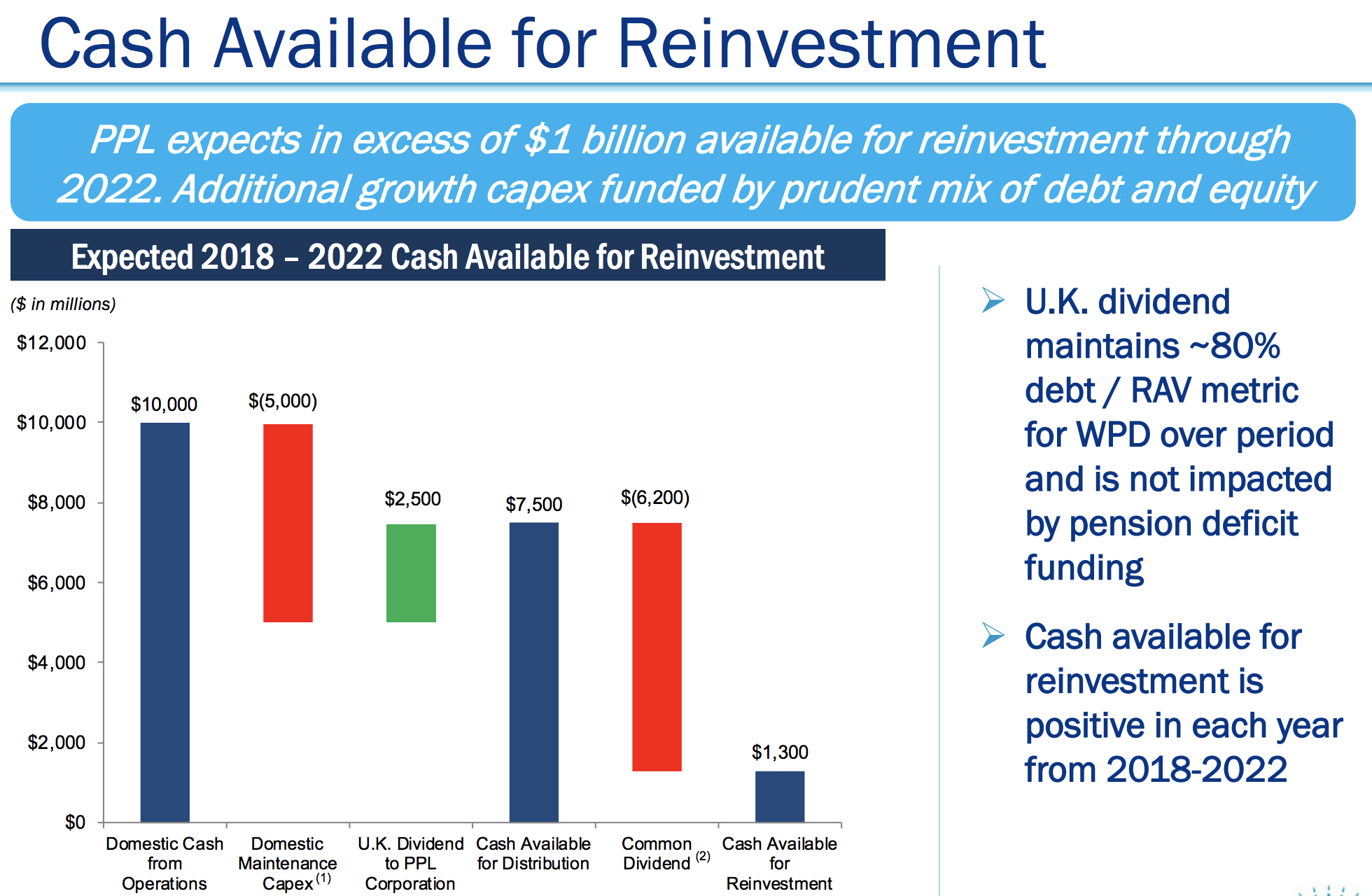

As you can see below, PPL's cash available for distribution more than covers its common dividend, so at first blush it doesn’t seem like a drop in allowed returns of even a few hundred basis points (i.e. $50 million to $150 million impact) would devastate the business by any means.

Source: PPL Investor Presentation

Management expects similar results over the next five years, with cash available for reinvestment expected to be positive each year. In other words, PPL's overall operations are generating enough cash to provide some level of flexibility in a lower-returning U.K. world.

Source: PPL Investor Presentation

However, given PPL’s high payout ratio around 70%, hefty debt load, and need to raise low-cost capital to fund growth projects, there also isn’t a huge margin for error if the U.K.’s next regulatory framework comes in even worse than what’s currently being discussed.

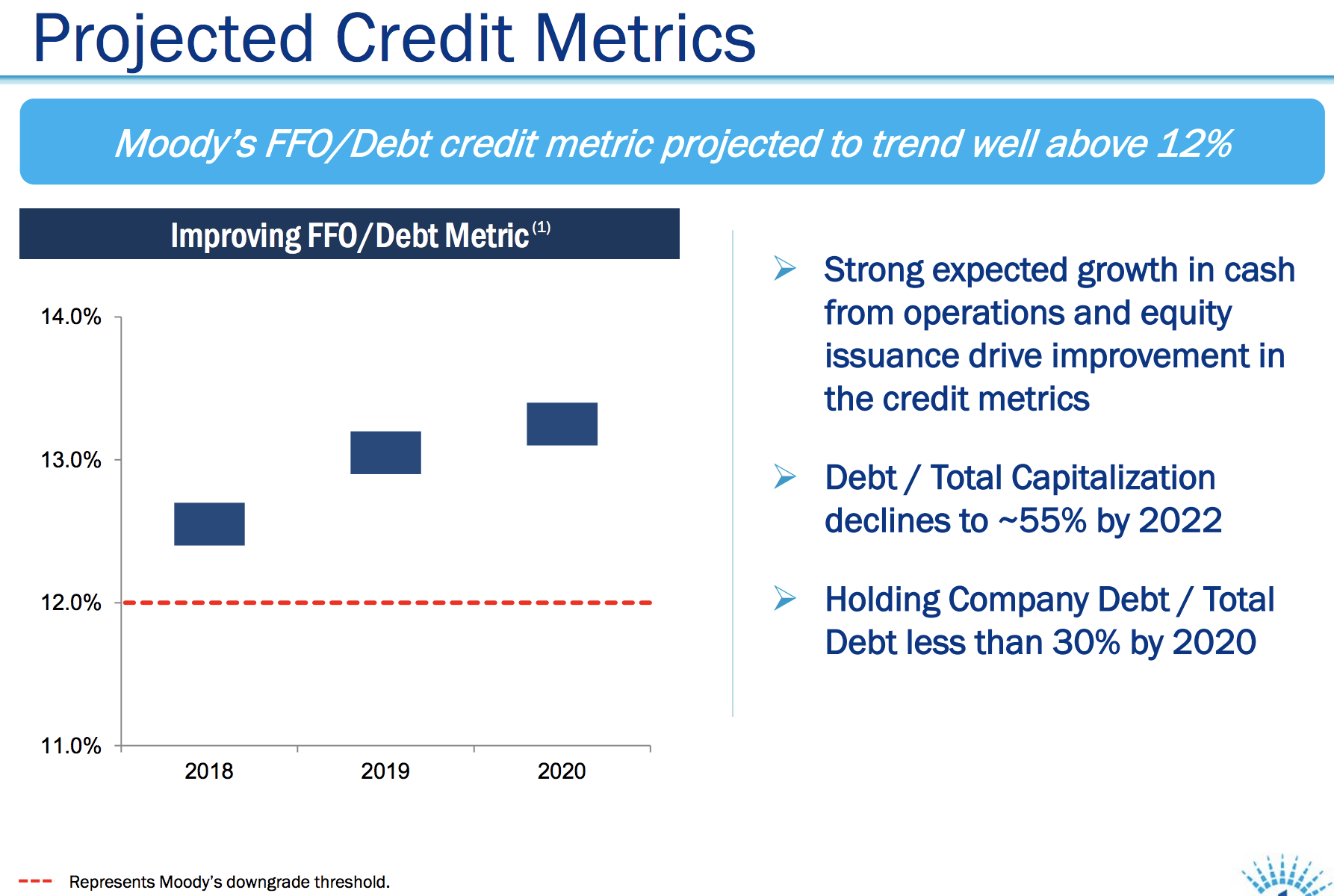

Perhaps the best news is that management has time on their side to prepare PPL for a range of regulatory outcomes in the U.K. Five years is a long time to shore up the balance sheet and get the financial house in order, and you can see that the company expects its credit metrics to strengthen over the next couple of years.

Source: PPL Investor Presentation

If management felt the need to be even more conservative, dividend growth could come in below PPL's 4% annual target, and it was interesting to see that management dropped the explicit 4% dividend growth guidance from recent presentations, simply noting a softer “Commitment to Annual Dividend Increases” instead.

Source: PPL Investor Presentation

Closing Thoughts on PPL’s Underperformance

Putting it all together, PPL’s outlook over the next few years appears to remain intact, and its dividend should remain secure. However, regulatory headwinds are clearly brewing in the U.K. that will result in lower international profits beginning in 2023. How much lower remains to be determined, but investors seem to be bracing for a worst-case scenario type of event with how the stock has traded over the past year.

PPL should be able to meaningfully grow its cash flow and improve its leverage metrics before the U.K.’s next regulatory framework kicks in, positioning its business to handle these headwinds as best as it can. However, dividend growth could come in below management’s 4% annual target if management feels the need to be even more financially conservative until additional information is known.

As far as regulated utilities go, PPL is not for the faint-hearted in light of these developments. Investors are likely years away from having regulatory clarity in the U.K., potentially keeping a lid on the stock, but that could also be an opportunity for income seekers who are comfortable with some of these risks.

PPL represents less than 3% of our Conservative Retirees portfolio’s value, and I plan to hold our position for now given the stock's seemingly low expectations and stable fundamentals over at least the short to medium term. I will continue monitoring any regulatory or financial developments as they emerge.