Pembina Pipeline: A Canadian Midstream Firm Paying Uninterrupted Dividends Since 1997

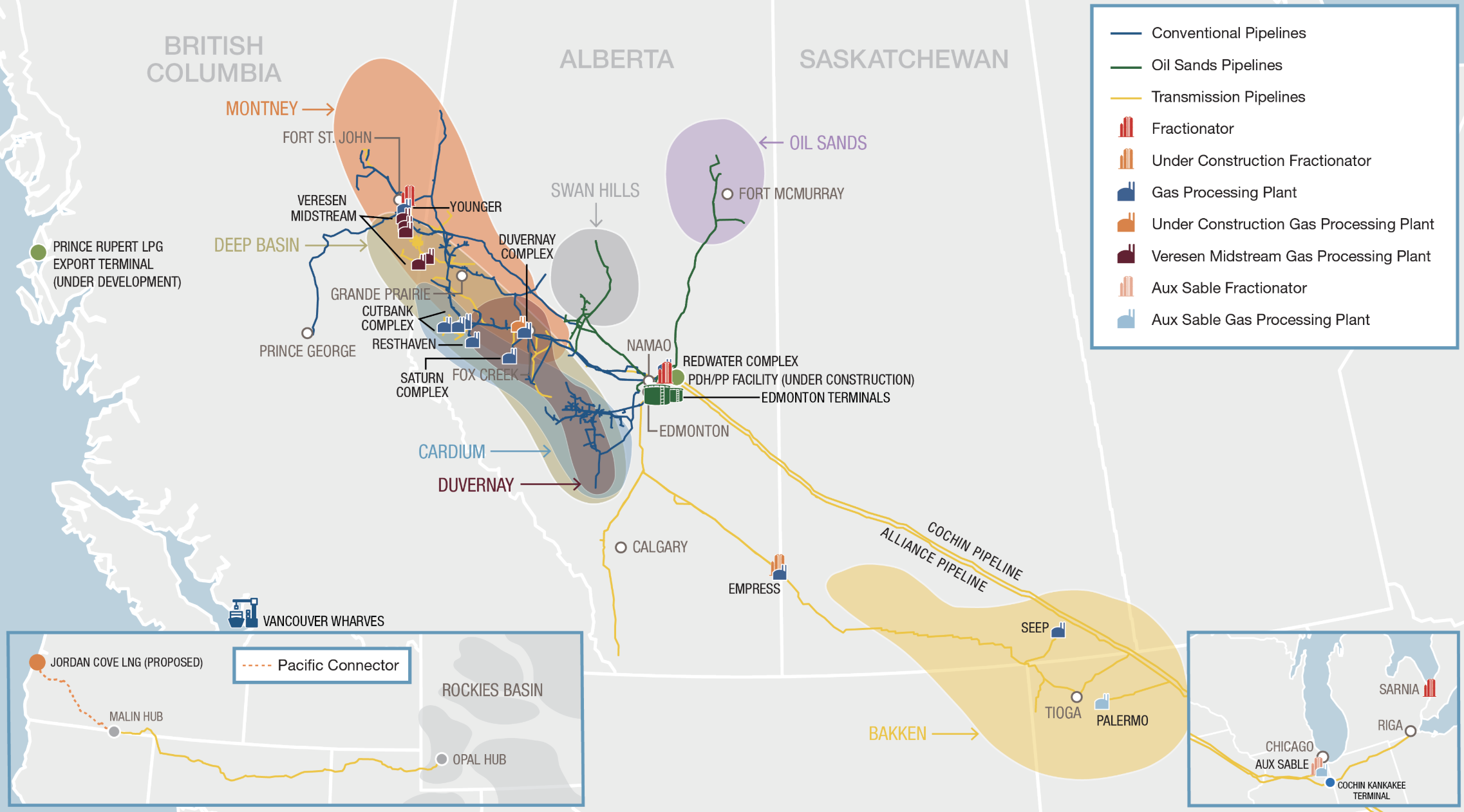

Founded in 1954, Pembina Pipeline (PBA) is a major transportation and midstream service provider with a network of oil and gas pipelines, storage facilities, and processing plants located primarily in western Canada.

The firm's energy infrastructure helps the hydrocarbons produced in western Canada reach the highest value markets throughout the world.

Source: Pembina Investor Presentation

Pembina's asset base is predominantly supported by long-term, fee-for-service, take-or-pay contracts which are underpinned by investment-grade counterparties. Approximately 85% of the firm's adjusted EBITDA is fee-based, reducing Pembina's sensitivity to volatile oil and gas prices.

Pembina organizes its operations into three business segments:

Pipelines (58% of EBITDA): transports crude oil (mostly conventional but some heavy oil), natural gas liquids, condensate, and natural gas across much of Alberta, as well as parts of British Columbia and the U.S. (including the Bakken).

Facilities (29% of EBITDA): owns natural gas processing and natural gas liquids (NGL) fractionation facilities that provide customers with natural gas, condensate, and NGL services. Segment profit is split equally between gas services (gathering, compressing, processing, etc.) and NGL services.

Marketing & New Ventures (13% of EBITDA): undertakes commodity marketing activities including buying and selling products (gas, oil, NGLs, etc.), commodity arbitrage, and optimizing storage opportunities to maximize the value of hydrocarbon liquids and natural gas in its key basins.

Pembina has paid uninterrupted dividends since 1997 and raised its payout each year since 2012. The firm's dividend is paid monthly.

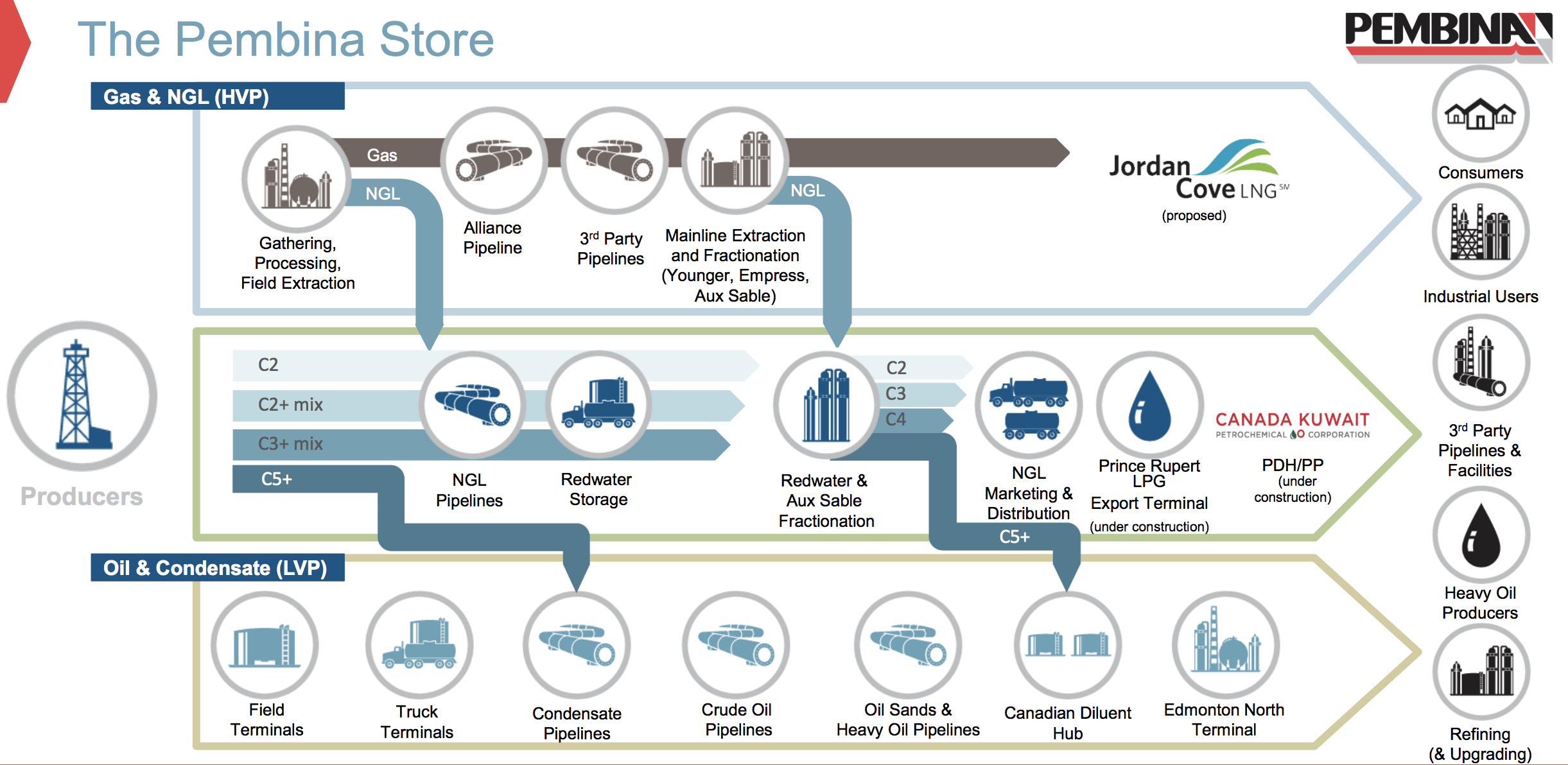

Business Analysis Pembina has long taken a conservative and disciplined approach to growing its business. Through the first 45 years of its existence through 2000, the company focused only on oil and condensate gathering with its conventional pipeline operations.

Then, in 2001, the firm added heavy oil lines and expanded into crude oil marketing in 2005. In 2009 Pembina started processing gas, and in 2012 the company acquired Provident Energy to get into the NGL business. Management finished rounding out Pembina's offerings in 2017 by buying Veresen, which further expanded its gas pipelines and processing infrastructure.

This evolution is important to understand because it has made Pembina a one-stop shop for its customers – the company can provide all the services that a producer needs to get their hydrocarbons to market. Management refers to this as the Pembina Store.

Source: Pembina Investor Presentation

Pembina has the most fractionation capacity serving the Western Canada Sedimentary Basin (WCSB), is the largest third-party gas processor, and is one of Canada's largest storage owners, making it a critical partner for most customers.

With a diversified and integrated portfolio of assets (plus plans to expand its reach into petrochemical facilities and export terminals), Pembina's infrastructure is uniquely positioned to transport almost any product a customer drills, maximize netbacks received by producers, and provide the greatest optionality for customers.

Of course, many income investors are drawn to the midstream industry because of the stable cash flows and generous dividends it often provides. Pembina's CEO Michael Dilger said it best:

"Our job is to build annuities. Highly predictable cash flow streams that will last a long time, that will underpin our dividend."

Most of Pembina's assets are very difficult to replicate, providing a foundation from which to build annuities.

For example, major projects often cost billions of dollars to complete, with a single mile of new pipeline costing over $7 million per mile to build in recent years. Meanwhile, various regulators have to sign off on new construction, which isn't easy in Canada.

These assets also benefit from non-discretionary demand from their customers and have few viable substitutes. Not only is it uneconomical to have too many pipelines, processing plants, and fractionators serving the same basin, but many oil & gas formations are in hard-to-access areas (difficult for rail and truck transportation to cost-effectively compete).

Many of the key shale basins Pembina's assets sit on top of have more than 100 years of reserve life left based on their production rates, and many decades of production are possible in the basins Pembina has long served with its conventional pipelines, according to management.

As long as Pembina maintains its pipelines, which the firm also expects to last upwards of 100 years, the resources it sits on top of have good potential to continue providing predictable demand.

Pembina's cash flow stability and safe dividend profile especially benefit from the nature of its contracts, which typically have long terms (10-plus years) and fee-for-service or take-or-pay provisions.

In fact, about 85% of the company's adjusted EBITDA is fee-based. This helps lower Pembina's sensitivity to commodity price fluctuations. Management also targets at least 75% of its credit exposure from investment grade counterparties, ensuring Pembina has a good chance to continue getting paid regardless of headwinds in the energy market.

Finally, Pembina's conservatism is evident in its target to maintain a strong BBB investment grade credit rating, self-fund its expansion projects, and cover its dividend using only fee-based distributable cash flow (rather than rely in part of the commodity-sensitive parts of its business).

This results in meaningful retained cash flow after paying dividends. Pembina's annual growth spending has potential to grow its asset base at a mid-single rate, and no equity will be needed to make ends meet. In other words, Pembina's organic growth financing is independent of its (sometimes) volatile stock price.

Overall, Pembina looks like a solid bet to continue rewarding its investors with 4-6% annual dividend growth without taking actions that would increase the risk profile of its business. However, there are still several risks to consider.

Key Risks First, note that as a Canadian company, Pembina pays its dividend in Canadian dollars. This creates some currency risk in that a stronger U.S. dollar decreases the effective dividend amount for American shareholders, at least in the short term (each quarterly dividend is converted from Canadian dollars to U.S. dollars when it is paid, based on prevailing exchange rates).

In addition, like all Canadian stocks, U.S. Pembina investors face a 15% foreign dividend tax withholding in taxable accounts. Tax treaties between the U.S. and Canada allow U.S. investors to potentially recoup this withholding, but it can result in more paperwork at tax time.

As for fundamental risks to the business, it's worth noting that the Canadian midstream industry faces several unique risks compared to its U.S. counterpart.

First, Canada's federal and provincial governments, as well as environmental activists and indigenous groups, have struggled to get along. As a result, key pipeline projects initiated by giants like Enbridge and TransCanada to connect Alberta with the Pacific and Atlantic coasts were scrapped in the last decade.

Therefore, despite housing the third-largest proven oil reserves (behind only Venezuela and Saudi Arabia), much of Canada's crude remains stuck in landlocked Alberta, which is home to 97% of the country's reserves.

Pipeline constraints have cost Canada's oil producers more than $10 billion annually in forgone export revenue, made them less likely to invest in production growth, and resulted in a glut of crude.

As a result, oil production is expected to grow only about 1% annually in the long term, according to industry group Canada's Oil & Natural Gas Producers.

While this arguably makes Pembina's established assets all the more valuable, it also limits the large-scale pipeline projects Pembina can pursue to improve its growth profile.

It also means Canada will likely remain dependent on the U.S. market (rather than being able to diversify to other export markets in Asia and Europe). While this isn't problematic today, that could change depending on how long demand will grow for oil and gas.

Some investors worry that the world's growing push to reduce carbon emissions and embrace renewable energy will cause fossil fuel demand to peak within 20 years, sooner than many energy executives expect.

It's hard to say how that could affect U.S.-dependent Canadian producers and the midstream service providers they utilize (risk of overcapacity, sliding contract rates, and falling returns on investment). Investors just need to monitor how the energy sector continues evolving.

Closing Thoughts on Pembina Pipeline Pembina's conservative approach to running its business mitigates most company-specific risks and helps explain how the firm has managed to reward investors with steady dividends for more than two decades – despite the volatility of pipeline politics in Canada and the 2014-16 energy crash.

Looking ahead, Pembina is not pursuing any growth projects that could threaten its dividend if they encounter challenges, and management expects to continue running the business conservatively, with a dividend covered by fee-based cash flow, a self-funding model, and an investment-grade credit rating.

For income investors who are comfortable with the risk profile of Canada's midstream industry, Pembina could be a decent option to consider.