Qualcomm Investors Remain Hopeful for Improving Dividend Safety and Growth Prospects in 2020

Qualcomm (QCOM) has had a volatile year as the firm worked to address the significant legal risks faced by its core patent licensing business, which customers and government agencies accused of charging excess rates.

The two major overhangs were a dispute with Apple and an antitrust suit issued against the company by the Federal Trade Commission (FTC). While Qualcomm reached a deal with Apple in April, the FTC won its case against the firm in May.

Qualcomm appealed the ruling, which required the business to renegotiate its licensing deals with smartphone manufacturers and allow rival chip makers to use its intellectual property on more reasonable terms.

Simply put, the ruling threatens to disrupt the lucrative licensing practices that historically generated over 70% of the company's operating profits, creating uncertainty.

If Qualcomm loses its appeal, what will happen to the earning power of this business? How excessive are its current royalty rates? What impact will licensing some of its patents to rival chip makers have? Without being able to sign exclusive supply deals, how much more competition will the firm face?

While forecasting Qualcomm's cash flow in such a scenario is difficult, some income investors worry that losing the appeal could cause Qualcomm's licensing profits to fall significantly enough to potentially threaten its dividend, which consumes about $3 billion per year.

After all, Qualcomm's CDMA Technologies (QCT) segment, which primarily develops and sells chips for smartphones, isn't large enough to fill the gap (not to mention continue funding Qualcomm's substantial R&D investments). This division only generated average annual pretax operating profits of $2.5 billion in recent years and produced profits of $2.1 billion in fiscal 2019.

Qualcomm's licensing business is very important to its ability to invest for the future and pay dividends. This is the main reason why Qualcomm has a Borderline Safe Dividend Safety Score.

In Qualcomm's 10-K filed in November, the company noted how high the stakes are with its appeal (emphasis added):

"Further, if our appeal in the FTC lawsuit is unsuccessful, it could have a material adverse effect on our business. Any such event could result in a materially negative impact on our financial condition, in which case we would have to significantly cut costsand other uses of cash, including in research and development, significantly impairing our ability to maintain product and technology leadership and invest in next generation technologies such as 5G.

Further, depending on the breadth and severity of the circumstances above, we may have to reduce or eliminate our capital return programs, and our ability to timely pay our indebtedness may be impacted. If these events occur, our financial outlook and stock price could decline, possibly significantly."

Oral arguments on the appeal's merits are expected to take place in February or March. Based on the court's history and schedule, management believes it will take 7 months to 1.5 years before a ruling is made.

However, while this is clearly a high severity risk to the company's business model, investors are increasingly optimistic that Qualcomm will be victorious.

In August, the court granted Qualcomm's request for what's known as a partial stay. Essentially, Qualcomm argued its licensing practices were lawful and the judge's ruling in May would harm the company's revenue, ability to invest in R&D, and overall level of competitiveness while it appealed the case.

The court's action allows Qualcomm to continue its business practices during the appeal, and The Wall Street Journalnotes that while this event "isn't a definitive reading of the merits of Qualcomm's appeal," it indicates that "the company has a fair shot at winning."

Standard & Poor's in early December also upgraded Qualcomm's credit rating outlook from negative to stable, citing that it does not believe legal and regulatory risks "represent a serious threat to its long-term business prospects." The firm also applauded management's commitment to "a more conservative financial policy."

Meanwhile, the Justice Department and the Defense and Energy departments took the unusual step of urging the appeals court to consider the interests of national security. They argued that the ruling could hurt Qualcomm so much that it would need to reduce investment in 5G wireless technologies, providing China with an opportunity to gain advantages in a critical of technology.

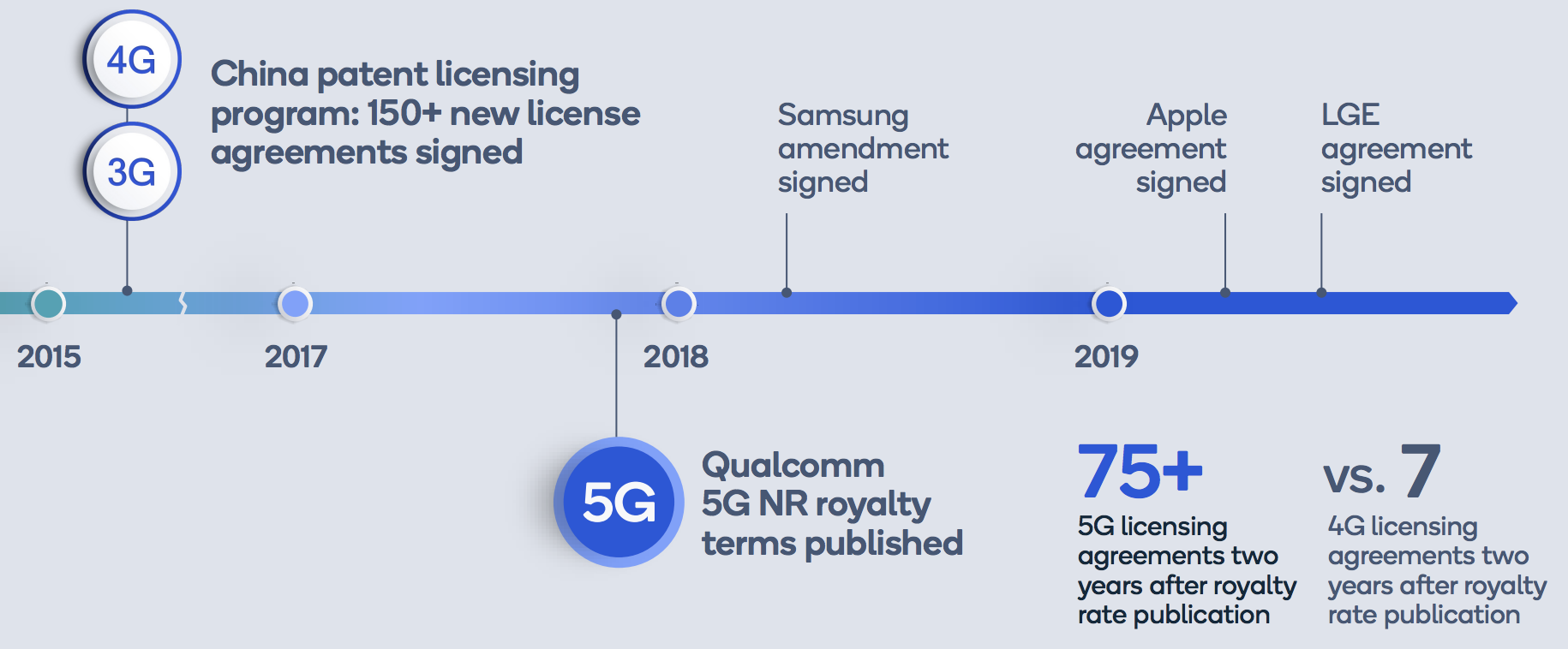

Finally, Qualcomm has continued racking up licensing agreements and describes the environment as "business as usual" despite the ongoing court proceedings. Qualcomm reached a new licensing deal with LGE in August, and management notes that the firm has already executed 75 5G licensing agreements, well ahead of the pace it achieved at a similar point in the rollout of 4G.

Source: Qualcomm Investor Presentation

In other words, it's not hard to see why investors are feeling more comfortable about the chances of Qualcomm's appeal being successful and any potential fallout not significantly disrupting the economics of its licensing business.

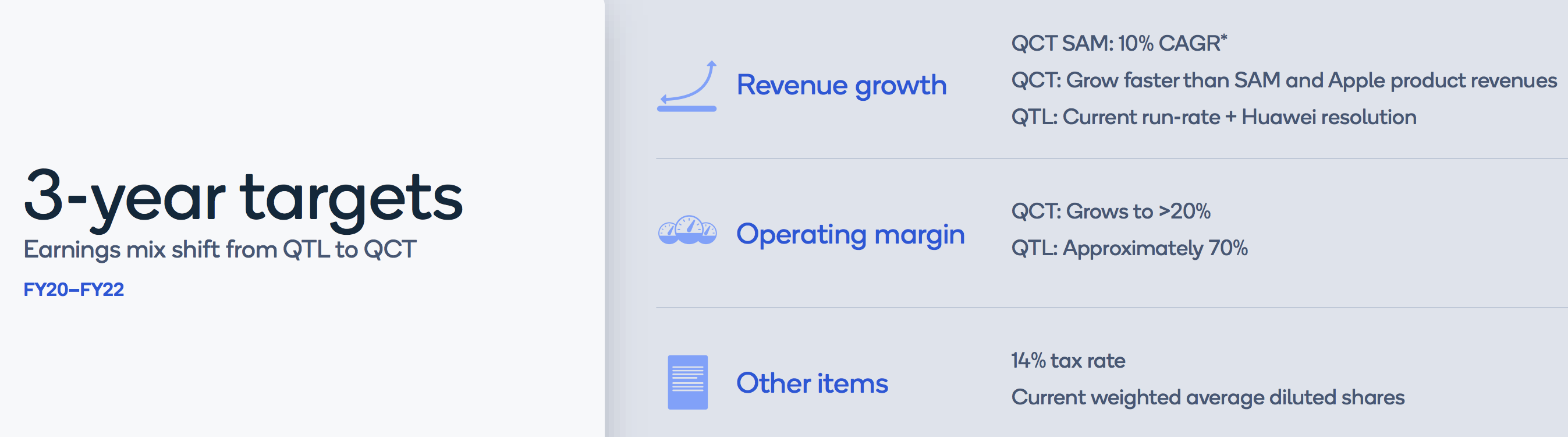

However, it's also fair to say that Qualcomm's licensing operations will no longer be the powerful business driver they once were. Qualcomm in November hosted an analyst day and unveiled 3-year financial targets.

Most notably, the firm expects its licensing business (QTL segment) to essentially tread water from a revenue perspective. Four years ago when Qualcomm held its last analyst day, management believed licensing could be a $10 billion business by 2020, according to The Wall Street Journal. However, the segment produced less than half of that amount in fiscal 2019.

Additionally, licensing is expected to maintain an operating margin near 70% going forward. The segment previously recorded a margin in excess of 85% before facing pushback from customers and government agencies.

Source: Qualcomm Investor Presentation

Qualcomm's growth will instead be driven by its lower-margin chip business (QCT segment), whose addressable market is expected to grow by 10% annually as 5G unlocks more opportunities across mobile, automotive, computing, and Internet of Things markets.

Source: Qualcomm Investor Presentation

Overall, in the years ahead Qualcomm seems likely to remain a cash cow, albeit an even more mature one. The company's most profitable business (licensing) will no longer be a major growth driver, but Qualcomm still maintains a strong position in 5G which seems likely to provide incremental opportunities in both segments as the technology transition begins to ramp next year.

From an income perspective, since June 2018 Qualcomm has held its dividend flat as it dealt with a number of growth and legal challenges. Until final clarity is provided on its appeal, hopefully by the end of next year, it wouldn't be surprising to see management continue holding the dividend steady out of conservatism.

Should a favorable ruling be achieved, which seems to be the more likely outcome investors are betting on, Qualcomm's Dividend Safety Score would likely be upgraded to a Safe rating.

Dividend growth would probably resume as well, as analysts expect Qualcomm's earnings to return to a faster rate of growth next year, management has said dividend growth remains an important long-term priority, and the firm's balance sheet retains a strong investment-grade credit rating.

Investors just have to be comfortable with changing nature of Qualcomm's growth drivers, the industry's general complexity, and the company's lingering legal tail risk.