IFF Plans to Buy DuPont's Nutrition Business in $26 Billion Deal, Maintains Dividend

International Flavors & Fragrances (IFF) announced plans on December 15 to acquire DuPont's Nutrition and Biosciences business for $26.2 billion in a deal that would more than double the company's size. DuPont shareholders will own 55.4% of the new company and existing IFF investors will own 44.6%.

Investors didn't like the news, sending IFF shares 10% lower yesterday. However, from a strategic perspective, the deal actually looks appealing (in theory).

DuPont's nutrition business is a reasonably attractive asset with an impressive 24% EBITDA margin and a presence in many markets with decent long-term growth potential.

The company sells a range of probiotics, enzymes, soy proteins, and ingredients across food & beverage, home & personal care, animal nutrition, and pharma end markets. Within food & beverage markets, the firm's focus is on natural and plant-based ingredients, which are in high demand.

Source: IFF Investor Presentation

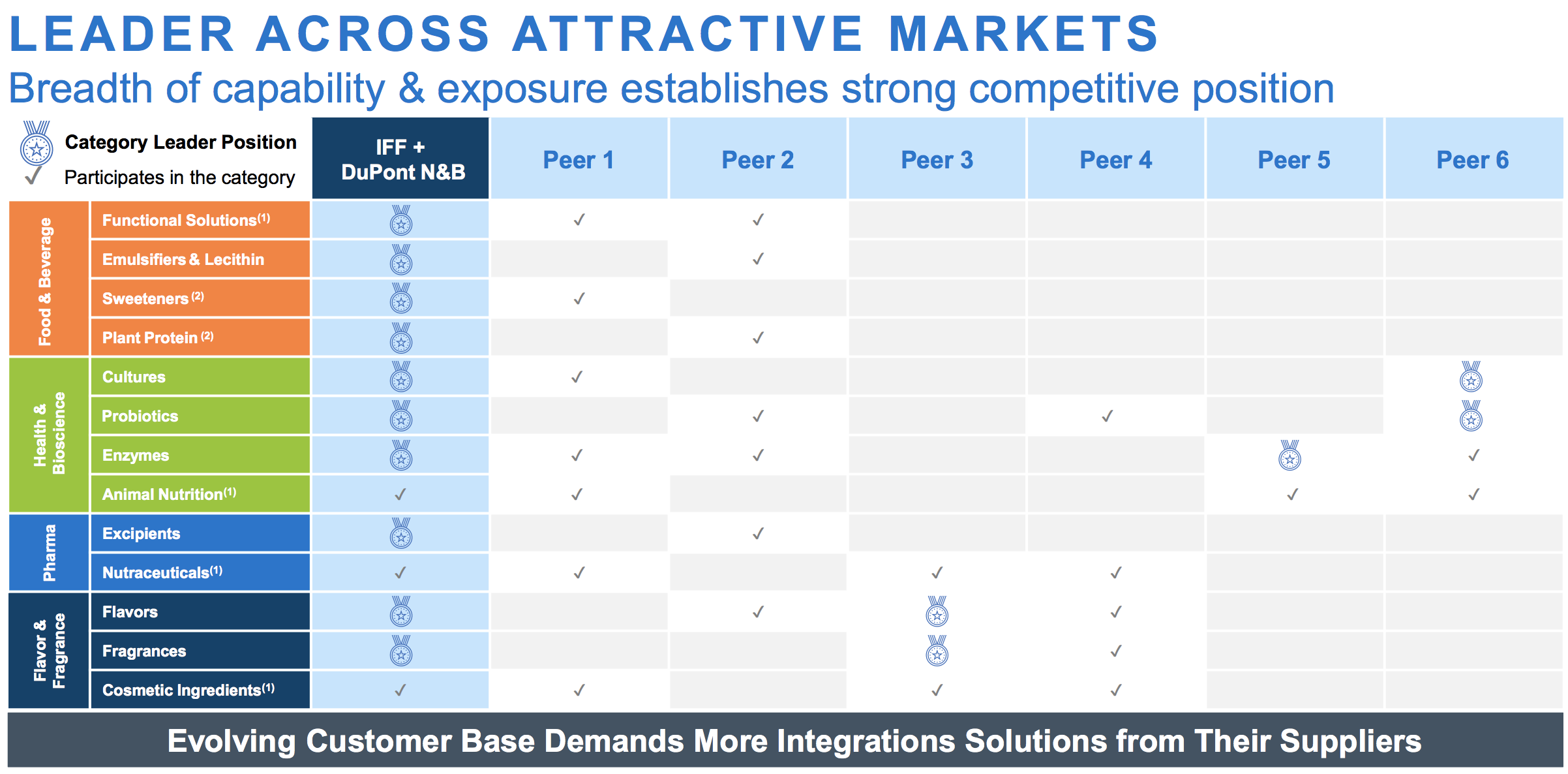

IFF operates in many of these end markets with complementary products. The combined company will have No. 1 or No. 2 positions across many of the largest ingredient categories in food & beverage, health & wellness, and home & personal care markets.

Source: IFF Investor Presentation

As a result, IFF will be able to offer more end-to-end solutions to customers and hopefully be better positioned to meet their needs as consumers increasingly seek healthier, more natural products.

IFF hopes this will translate into numerous cross-selling opportunities and highlighted examples where each company's portfolio overlaps nicely. The company also expects to generate cost synergies from procurement savings and overhead reductions which have potential to lift EBITDA margins from 23% to 26%.

Source: IFF Investor Presentation

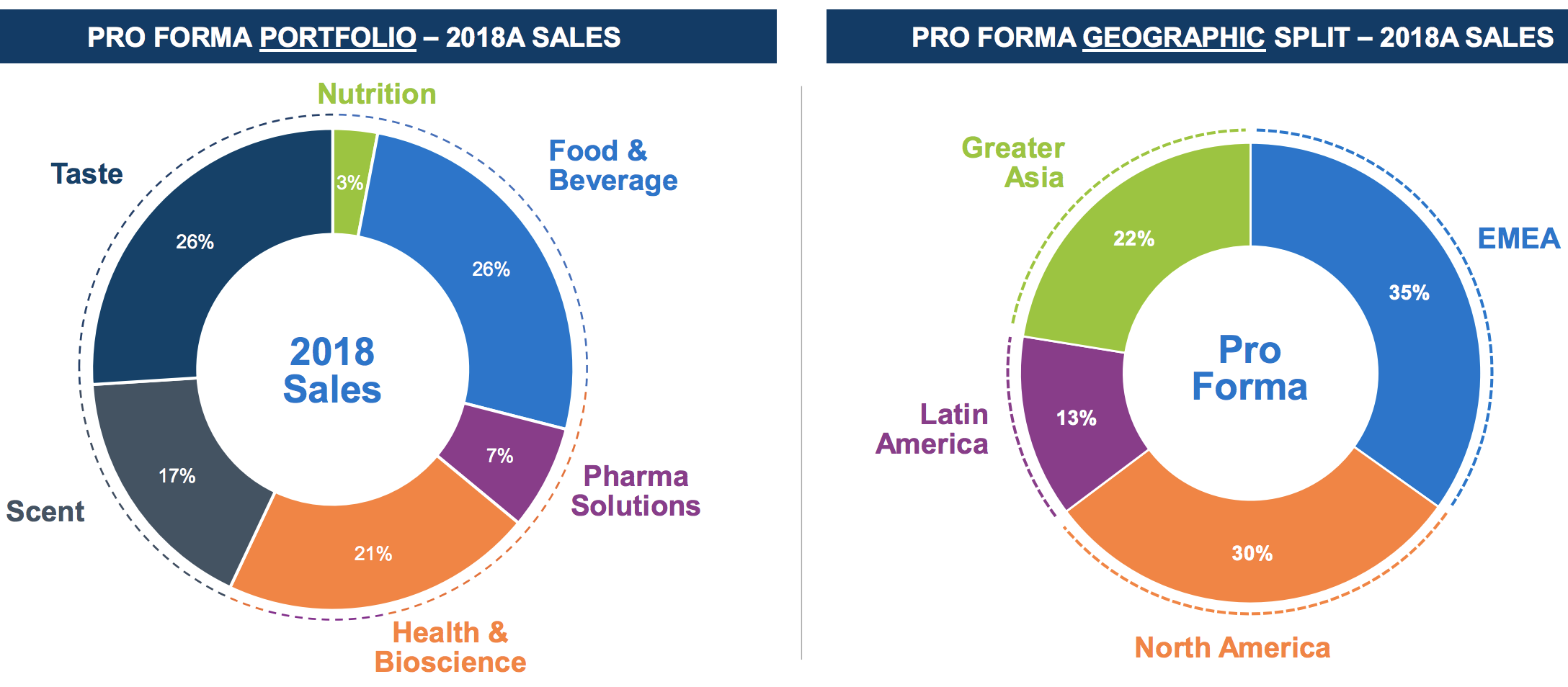

Assuming the tax-free transaction gains shareholder approval and closes in early 2021 as management expects, IFF's business will be well diversified by product application and geography.

If everything goes well, management believes the business has potential to deliver mid single-digit top line growth and high single-digit EBITDA growth.

Source: IFF Investor Presentation

However, investors are justifiably concerned by the increased financial and execution risks IFF faces as a result of this transaction. In recent years, IFF has taken a much more aggressive approach to growth.

Between 2002 and 2013, IFF focused on organic growth and did not make any acquisitions. Since 2014 the firm made several bolt-on acquisitions. Then, in May 2018, IFF announced it was buying rival Frutarom in a $7.1 billion deal that boosted its revenue by about 40%.

IFF paid a lofty ETBIDA multiple in excess of 25 to acquire Frutarom, banking on its impressive growth continuing. Unfortunately, Frutarom's organic sales were flat in the third quarter of 2019 and declined in the second quarter.

In other words, while it's admittedly still early in the process, management has not done much to inspire confidence in its ability to seamlessly integrate and extract meaningful value from large acquisitions.

Now, with Frutarom's integration work still several quarters from completion, IFF is taking an even bigger swing to grow its business. DuPont's nutrition business will more than double the company's size and presents even greater integration risks than Frutarom.

Due to all of these moving parts, it's perhaps unsurprising that this business has only recorded flattish revenue growth in recent years. IFF is paying an EBITDA multiple of 18x, so it's important that management squeezes out better results.

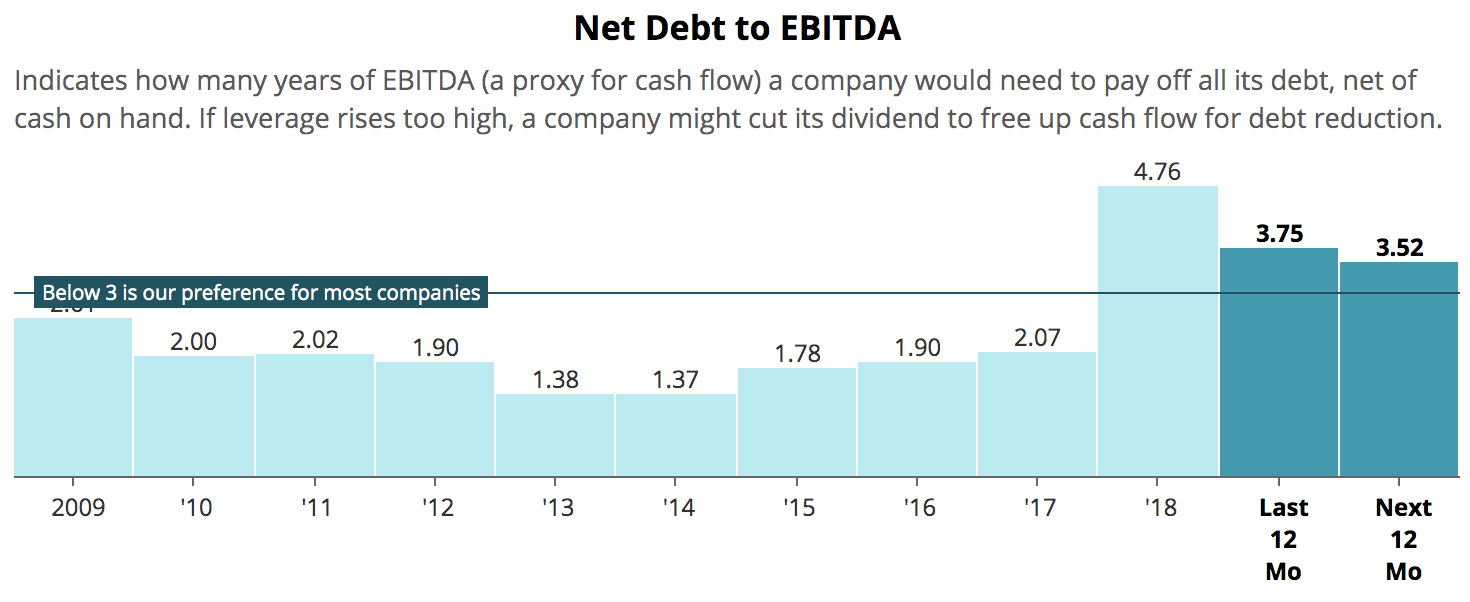

Meanwhile, IFF's net debt to EBITDA ratio is expected to rise to 4.0x after the deal closes, remaining well above its historical norm (the initial spike was due to Frutarom) and further raising the stakes. Management is still committed to maintaining an investment grade rating and expects leverage to fall below 3.0x by the end of two years after the deal closes.

Source: Simply Safe Dividends

IFF also expects to maintain its current dividend, but minimal to no dividend growth should be expected the next few years as cash is directed towards integration work and debt reduction.

The company's dividend seems likely to remain safe given the predictable cash flow this business generates, but there is now less margin for error. If shareholders approve the deal and IFF encounters any hiccups with its integration work and deleveraging, then IFF's Dividend Safety Score could be downgraded.

Overall, IFF's buying spree the last two years has significantly increased the firm's execution risk. Both Frutarom and DuPont's nutrition business have appealing qualities and seem to make sense from a strategic perspective, but I'm generally not a fan of large M&A given the risks that come with it.

Investors who desire faster dividend growth from a stock that yields less than 3% may want to look elsewhere. IFF seems likely remain a "show me" story with investors over the next couple of years until management demonstrates traction integrating these businesses and improving the balance sheet.

We hold shares of IFF in our Long-term Dividend Growth portfolio, and while I don't currently have plans to sell our position, I'm open to evaluating it against other stocks that have stronger dividend growth potential, healthier balance sheets, and less execution risk.