AT&T's Dividend Safety Score Upgraded to Safe on Deleveraging Progress, New Three-Year Guidance

AT&T (T) reported third-quarter results on Monday and provided a three-year capital allocation framework for its business.

The company continues making progress paying down debt, underlying business fundamentals remain solid, and management plans to allocate capital more conservatively going forward, including a commitment to avoid big acquisitions.

As a result of the firm's improving risk profile, we are upgrading AT&T's Dividend Safety Score to Safe from BorderlineSafe.

AT&T investors have faced their fair share of uncertainty in recent years. The firm's major acquisitions of DirecTV in 2015 and Time Warner in 2018 left AT&T with an elevated leverage profile, a debatable growth strategy, and little margin for error.

Combined with the execution risk AT&T faced integrating new businesses as the media and telecom industries evolved, not to mention the accelerating decline in pay-TV subscribers, some investors understandably had doubts about the company's future.

Fortunately, with some recent nudging from activist investor Elliott Management, AT&T laid out a three-year plan and committed to become a more conservative and focused business, hopefully improving the predictability of its results.

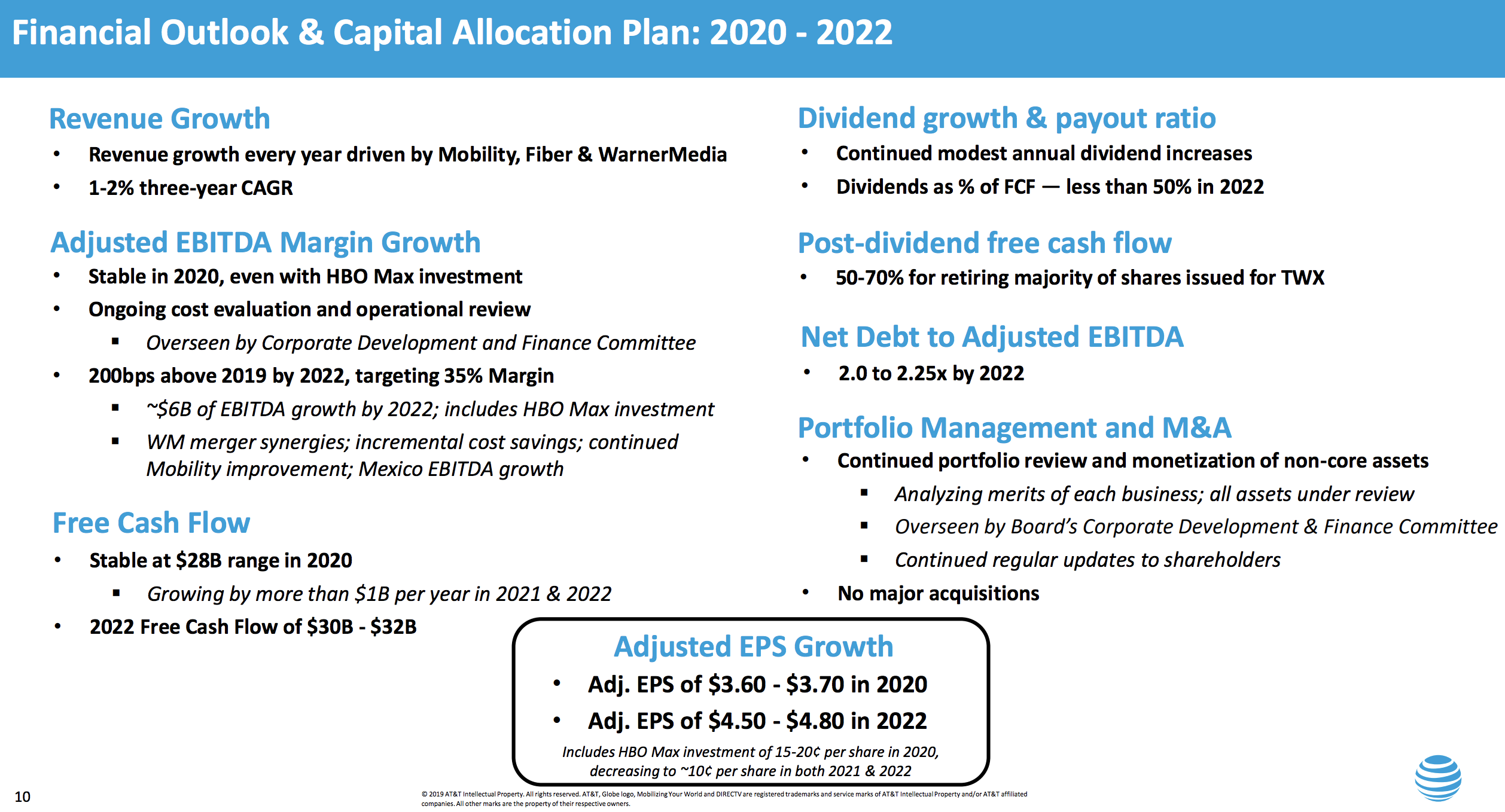

Management expects AT&T's revenue to grow 1-2% annually through 2022, which seems reasonable for a mature enterprise. Margins are also expected to tick higher despite investments in streaming, driven by WarnerMedia cost synergies, growth at AT&T Mexico, and plans to take out costs across the entire company.

But most importantly, AT&T's questionable empire-building days under CEO Randall Stephenson appear to be over. The company plans to repurchase shares with most of the free cash flow it has available after paying dividends and committed to "no material M&A." Whenever Mr. Stephenson retires, AT&T also plans to separate the Chairman and CEO roles for better corporate governance.

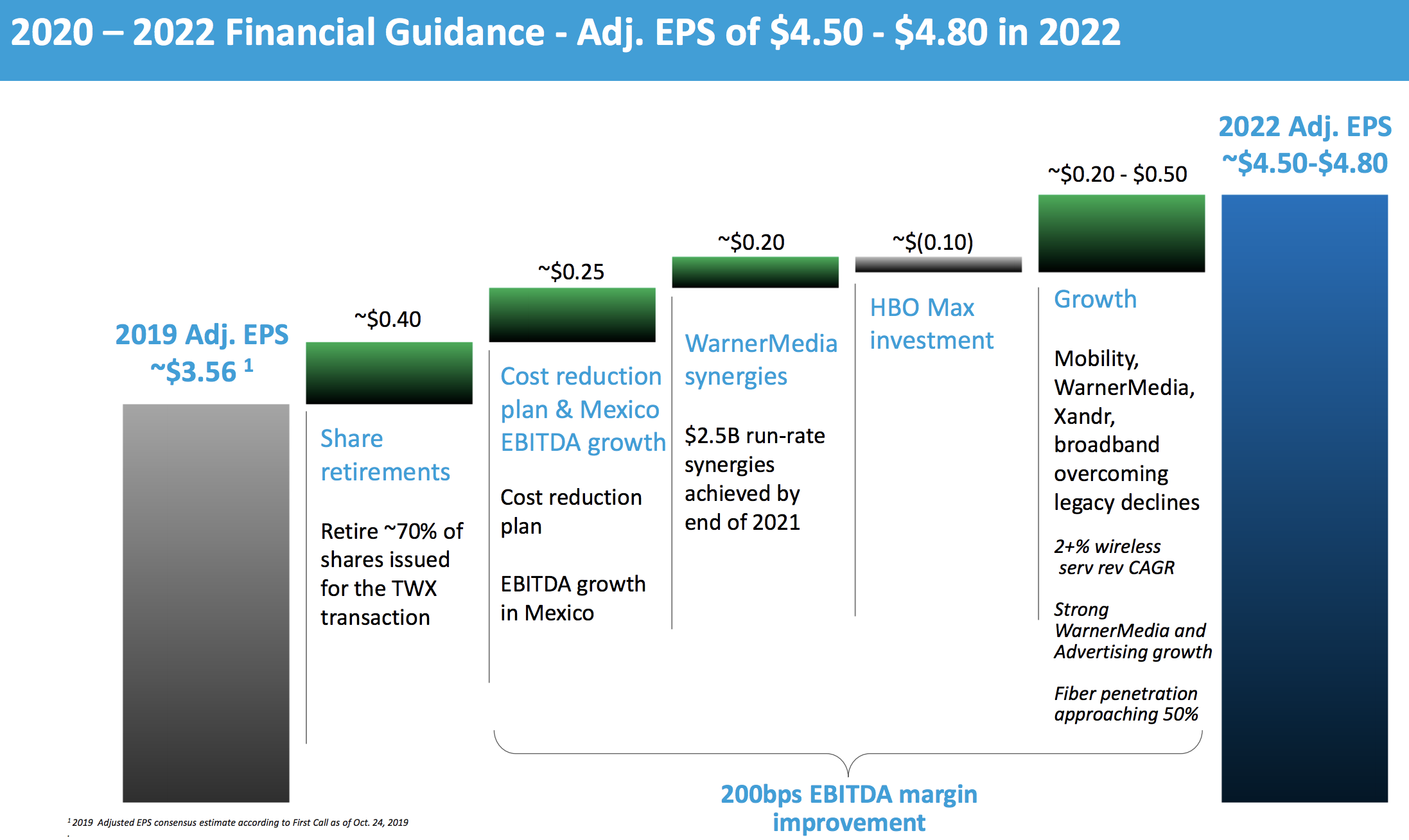

Debt reduction remains a priority over the next three years as well. Thanks to AT&T's excellent free cash flow and opportunities to divest non-core assets, management expects leverage to fall to around 2.5 times by year-end (down from 2.8 in 2018), with a goal of hitting 2.0 to 2.25 times by the end of 2022. At that time, AT&T will have paid back all of the debt taken on to acquire Time Warner.

Source: AT&T Earnings Presentation

If all goes well, management believes AT&T's adjusted EPS could increase by more than 25% between 2019 and 2022. The company's rising earnings are expected to fuel "continued modest annual dividend increases" and result in a conservative free cash flow payout ratio below 50% by 2022 (compared to low 50s% today).

Source: AT&T Earnings Presentation

Basically, AT&T is doing almost everything it can to retain its status as a reliable dividend stock. Management is on track to achieve its leverage target, earnings are growing at a low-single digit pace, free cash flow is tracking ahead of expectations, the Entertainment Group segment is squeezing out cash flow growth despite pay-TV subscriber losses, and the days of large M&A are over for at least several years.

AT&T still faces execution risk as it plods ahead with its cost reduction plans, WarnerMedia synergies, and streaming ambitions. However, the stakes are no longer as high as they were even a year ago thanks to the company's leverage returning to safer levels, management's disciplined capital allocation plans, and AT&T's solid and rising free cash flow.