Another Project Delay and Cost Increase Raise Pressure on the Safety of EQM's Distribution

In June, we warned that EQM Midstream Partners' (EQM) Dividend Safety Score could be downgraded if the firm's critical Mountain Valley Pipeline (MVP) project faced further delays.

Unfortunately, on October 22, EQM announced that the MVP's estimated completion date has been pushed back once more from mid-2020 to "late 2020" and its projected cost also increased by $500 million to between $5.3 billion and $5.5 billion.

This latest setback likely keeps EQM's leverage higher for longer, making it more difficult for EQM to maintain its investment-grade credit rating which management has said is a priority. A downgrade to junk status would raise EQM's cost of capital, potentially hurting its ability to profitably fund its future growth projects.

Coupled with analyst estimates now calling for the firm's payout ratio to slightly exceed 100% over the next 12 months, this increased financial pressure has led us to downgrade EQM's Dividend Safety Score from Borderline Safe to Unsafe.

As you may recall, the MVP project is by far the firm's most important growth opportunity, representing over two-thirds of EQM's current backlog and accounting for about 15% of firm-wide EBITDA upon completion.

The 300-mile regulated natural gas pipeline, which EQM owns a 45.5% stake in, was originally expected to be finished in late 2018 at a total cost of $3.5 billion. However, various legal and regulatory challenges had already pushed the project back to a mid-2020 completion estimate at a total cost of $4.8 billion to $5 billion.

Standard & Poor's, which has had a negative outlook on EQM's BBB- credit rating (its lowest investment-grade rung) since March 2019, noted in May that a downgrade was possible in the event of further delays or cost increases that management was unable to mitigate:

"We could lower our ratings on EQM if meaningfully further delays or rising construction costs for MVP occur without management taking mitigating actions to lower leverage below 4.5x by 2021.

We could stabilize the rating if MVP's regulatory issues are resolved leading to a firm in-service date. Alternatively, if MVP is further delayed and EQM takes steps which provide a clear line-of-site to leverage below 4.5x we may change the outlook to stable." – Standard & Poor's

As of October 24, S&P had not yet commented on this week's news. However, the firm's rating had previously assumed the MVP would be in-service by June 2020.

This latest delay not only pushes back the timing of when EQM can start generating cash flow from this pipeline, but it also increases the amount of debt EQM needs to reach the finish line.

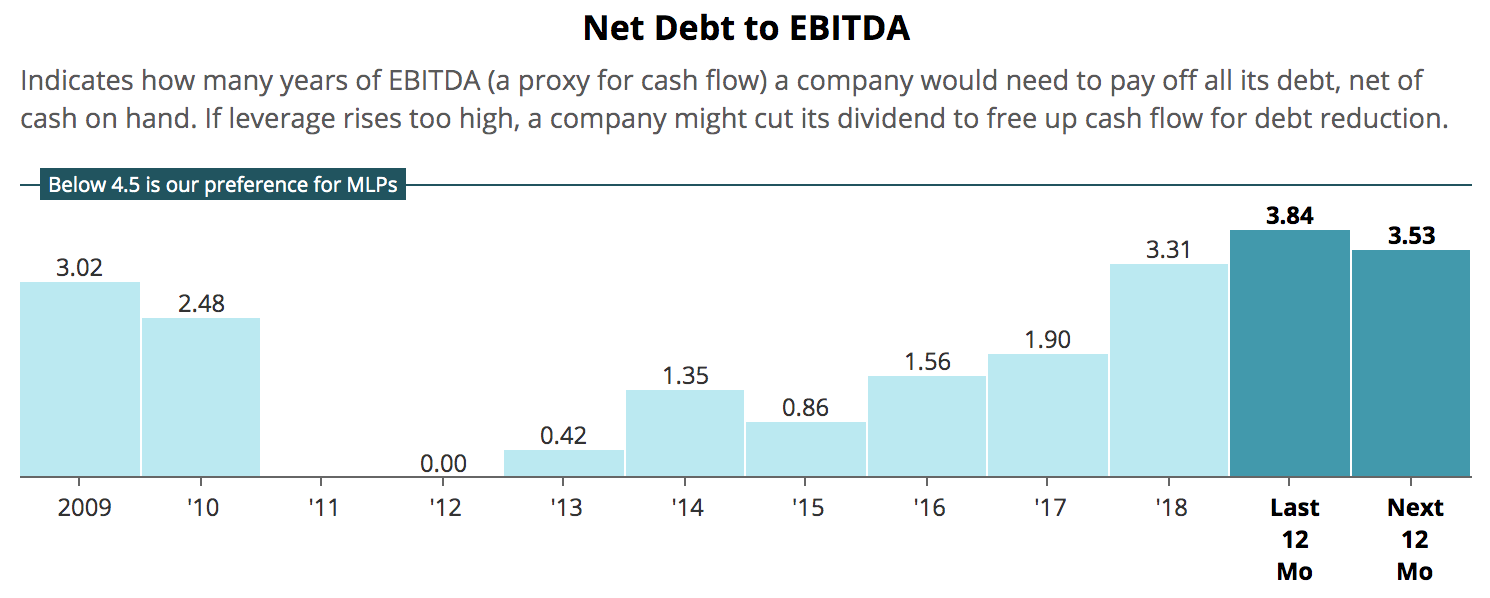

EQM's leverage ratio (note that our calculation is somewhat different than S&P's but the trend is the same) has already doubled since 2017 as the MVP's funding needs have grown.

Source: Simply Safe Dividends

On a positive note, EQM expects the MVP project to be 90% completed by year-end. The pipeline is also already fully subscribed under 20-year firm contracts, so it just needs to get to the finish line.

However, the issues standing in the way of completion are hard to evaluate, as evidenced by the series of delays the project has already faced. Legal attacks by environmental groups have resulted in several lost permits for the pipeline to pass through certain areas, causing the timing of certain work to shift or even halt.

Some investors are worried that the MVP will take even longer than management has communicated, further pressuring EQM's ability to maintain an investment-grade balance sheet without cutting its distribution to help manage leverage.

In its press release this week, management said that EQM expects to maintain its quarterly distribution "at least through the in-service date" of the MVP. Upon completion of the project, "the distribution growth rate will be reassessed."

In other words, management doesn't seem to think that the MVP's latest delay will threaten the safety of its distribution yet. EQM remains in close contact with S&P, so perhaps they have agreed on the short-term nature of this setback or identified a plan that can alleviate leverage concerns without risking the distribution.

EQM previously discussed several ways it could defend its credit rating, including cost reductions, less spending, and managing its distribution growth rates.

EQM now intends to keep its distribution frozen through at least the in-service date of the MVP to conserve cash, but the latest projected cost increase still adds nearly $230 million to the firm's obligations to finish MVP.

For context, that's nearly half of the $510 million in operating cash flow that EQM generated in the first six months of 2019. It's hard to imagine the firm finding enough expense reductions and spending cuts to fully offset the cost increase.

Reducing the distribution, which consumes about $900 million annually, would be an easy lever to pull to help reduce EQM's debt burden, which exceeds $4 billion.

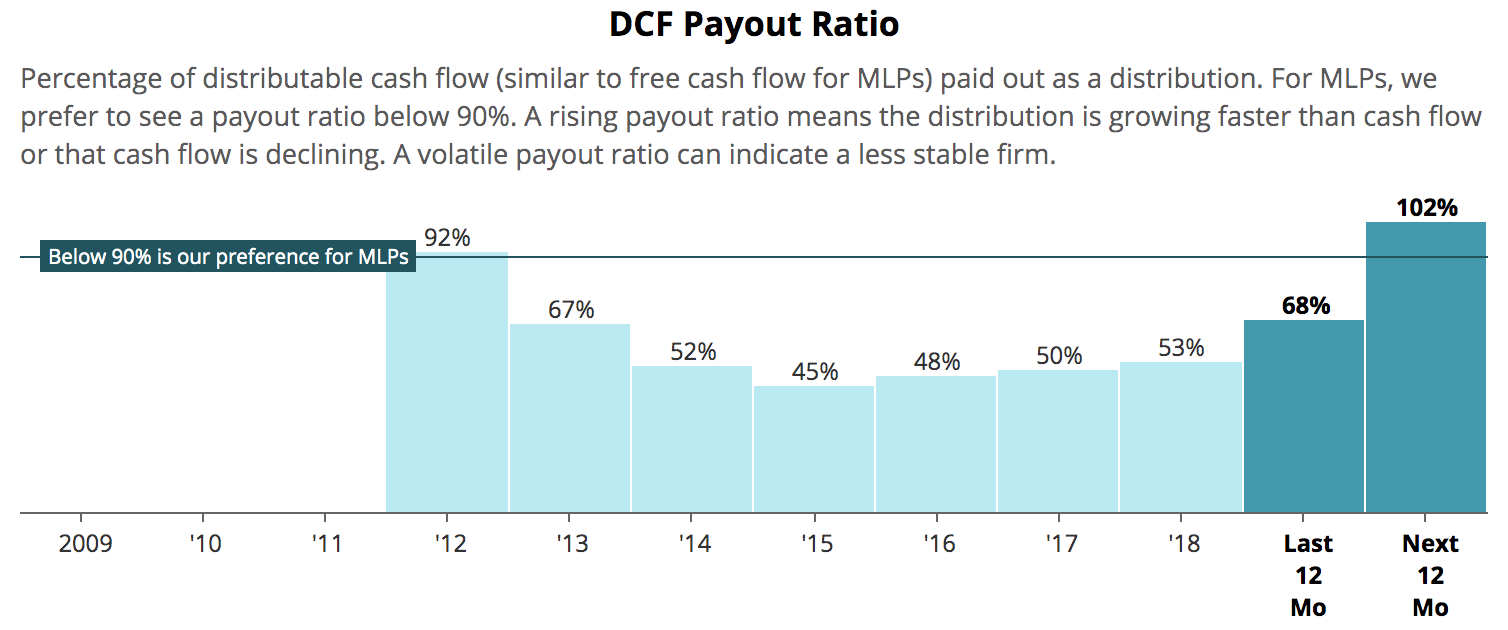

After all, the partnership's distributable cash flow payout ratio is now expected to top 100% in the year ahead. In other words, EQM's existing operations are not providing the company with any excess retained cash flow it can use to help fund the MVP or protect its balance sheet.

Source: Simply Safe Dividends

It's not hard to see why EQM units offer a double-digit yield. This is a speculative income stock with a wide range of potential outcomes.

The latest MVP setback puts further pressure on EQM's ability to maintain its distribution without threatening its credit rating and ability to profitably fund its long-term growth.

It's hard to say how likely it is that the MVP actually goes into service by the end of 2020 due to the murky nature of the legal and regulatory challenges plaguing the project, but any further headwinds could result in a distribution cut for EQM.

Reducing the distribution would provide a more sustainable payout ratio and make it much easier for the firm to deleverage its balance sheet in the years ahead. While management appears hopeful about maintaining the current distribution, there is now zero margin for error, which our Unsafe rating reflects.