Lazard's Dividend Appears Safe For Now Despite Cyclical Concerns

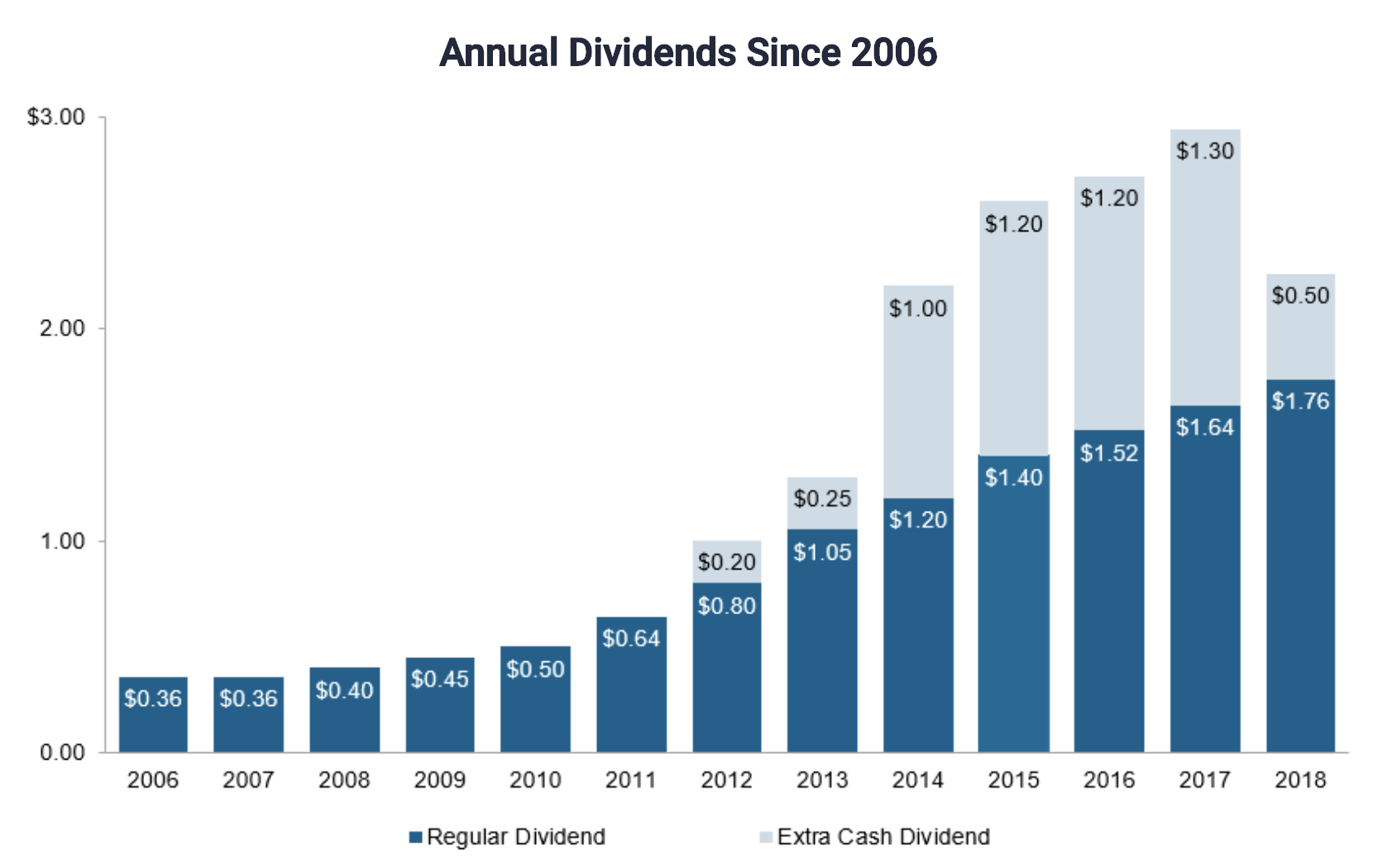

With origins dating to 1848, Lazard (LAZ) was a pioneer in offering financial services around the world. In recent years the company's popularity with income investors has increased. Not only has Lazard paid uninterrupted dividends since it went public in 2005, but the firm has also doled out special dividends each year since 2012.

Source: Lazard

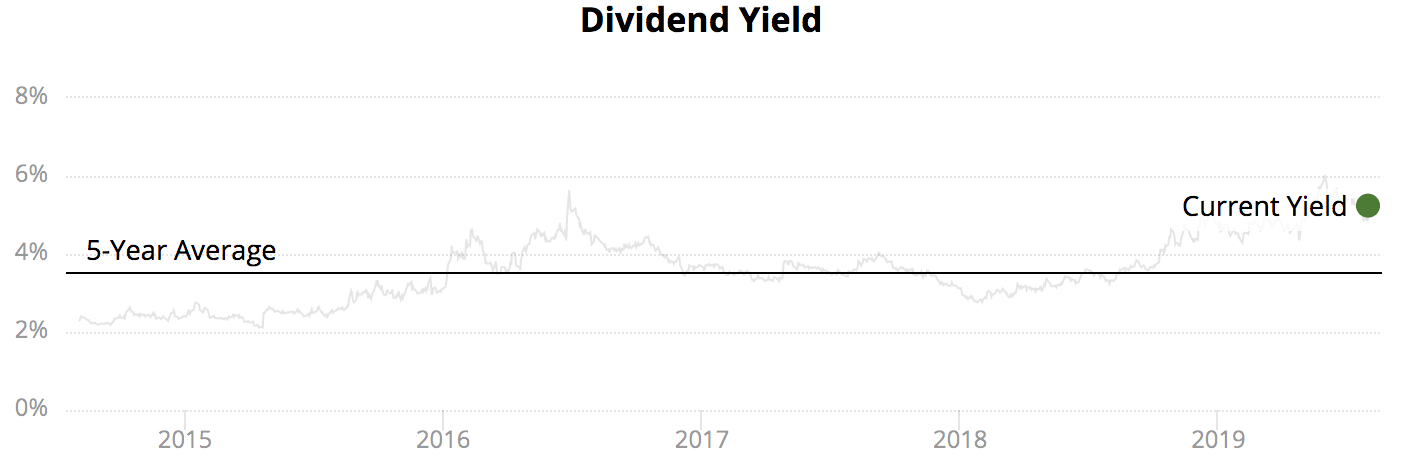

Based on the firm's regular dividend alone, shares of Lazard sport a yield above 5%. The stock's yield is unusually high compared to its long-term average. Coupled with Lazard's Borderline Safe Dividend Safety Score, now is a good time to review the firm's dividend profile and key risks going forward.

Source: Simply Safe Dividends

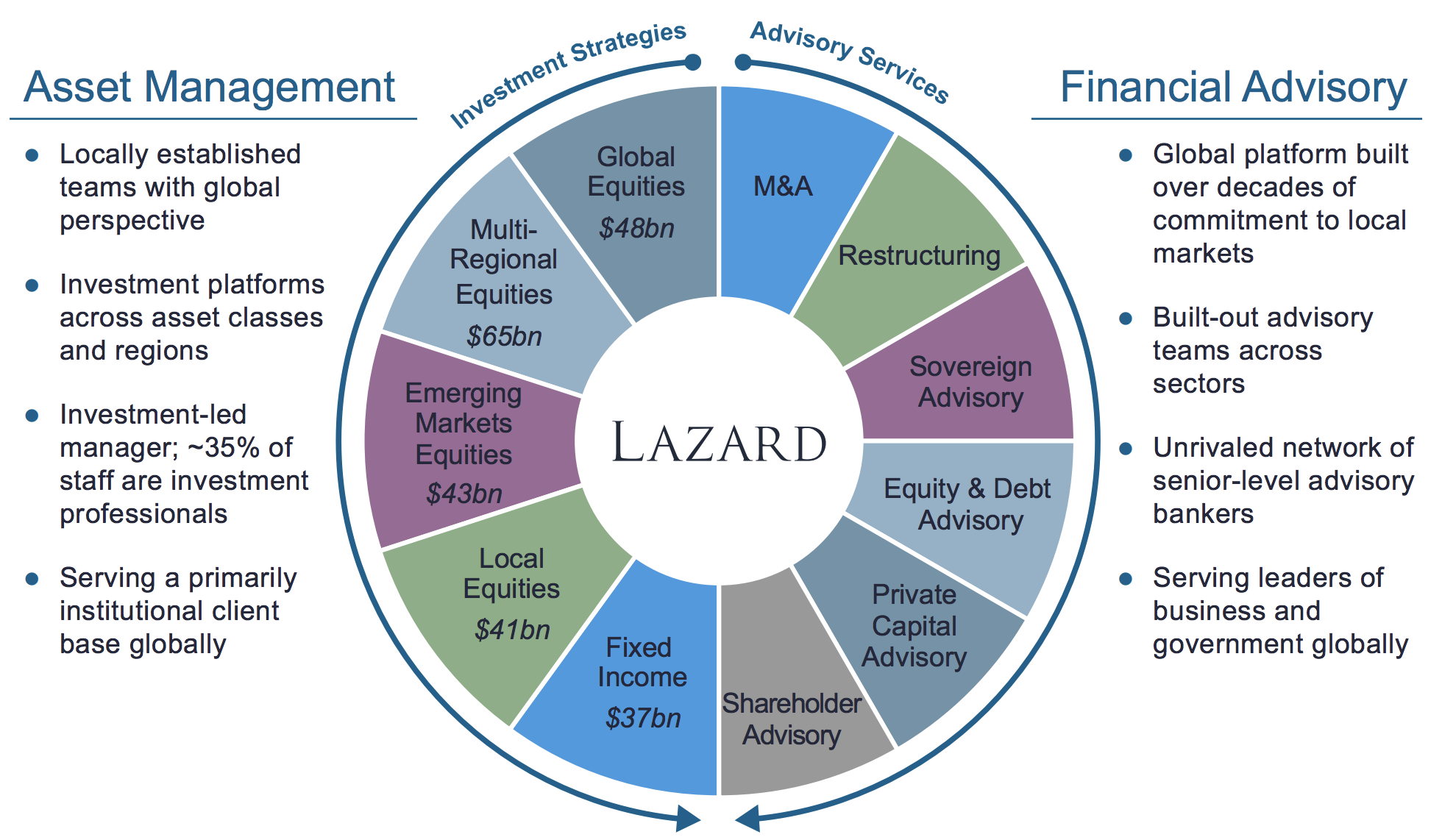

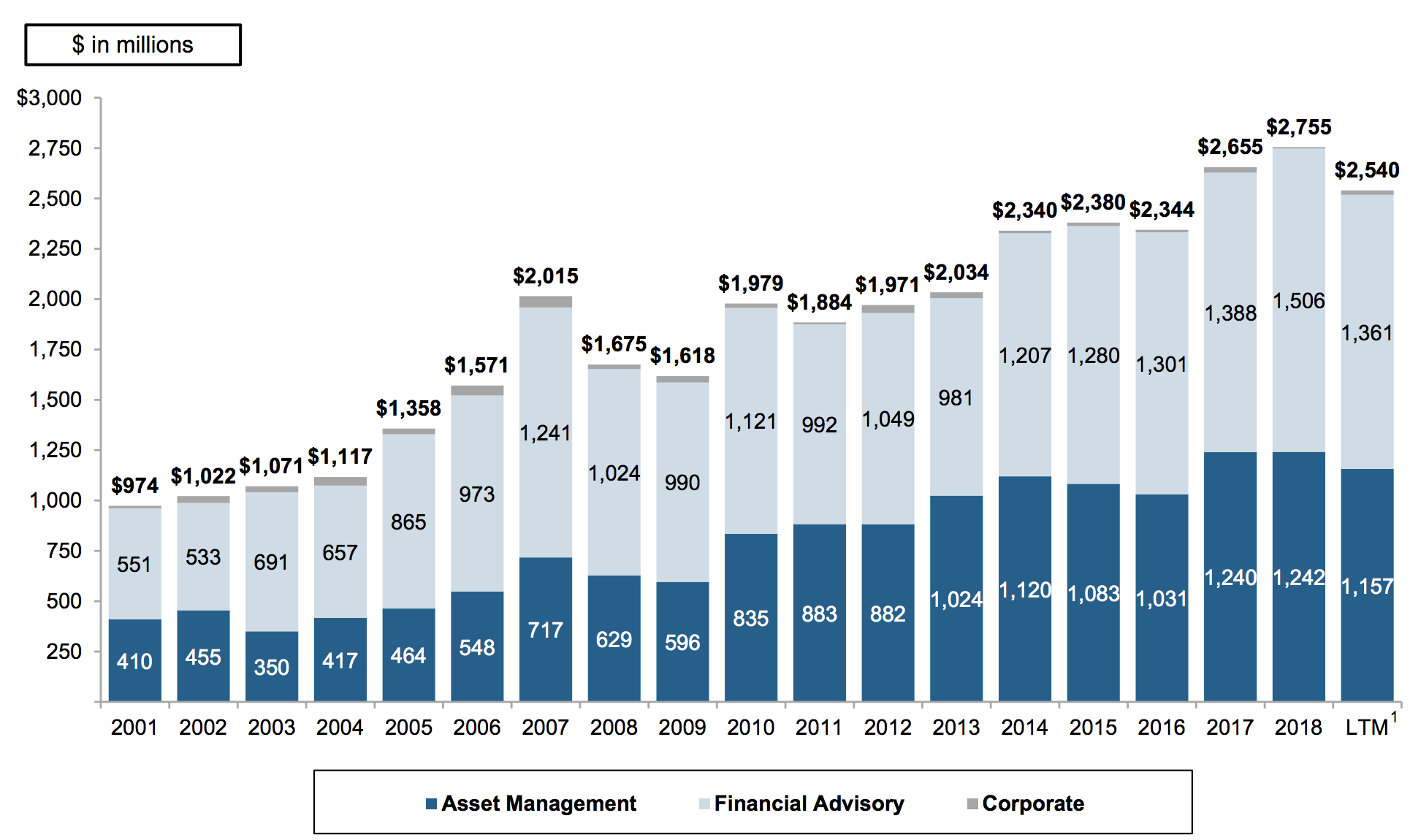

Lazard's business is divided between financial advisory services (54% of revenue) and asset management (46%). In its advisory business, the firm advises companies on M&A, restructuring, and other strategic matters. Lazard's asset management business serves primarily institutional investors and focuses mostly on equities. The business is very global, serving clients in more than 70 countries and deriving 43% of its revenue outside of the Americas.

Source: Lazard Investor Presentation

While Lazard's rising yield might seem to suggest otherwise, these aren't bad businesses by any means. Lazard's free cash flow margin towers above 30%, and revenue has increased more than 40% since 2011.

Both divisions are largely driven by trust and performance. On the asset management side, Lazard earns money through investment advisory fees based on the market value of assets under management, which most recently totaled $237 billion. (Lazard's average fees are 48 basis points.)

The asset management business is highly scalable. The firm can take in more assets without needing to increase its research headcount much, and the market's tendency to rise over time provides a natural tailwind. Institutional clients such as pension funds tend to be stickier than individual investors as well, and Lazard's scale, trusted brand, and diverse strategies make it a safe choice for big investors.

On the advisory side, Lazard has served clients for over 170 years. Unlike the asset management business which enjoys recurring management fees, this business has no long-term contracted sources of revenue. Each engagement is separately negotiated and awarded. Once a transaction is completed, Lazard must find the next one to continue generating revenue.

As one of the largest advisory firms in the world with numerous longstanding client relationships, Lazard's extensive network of people, industry connections, and areas of expertise (e.g. restructuring) keep its advisory business humming. Simply put, many executives know and trust Lazard's investment bankers.

Despite their strengths and enduring brands, Lazard's advisory and asset management businesses also have some drawbacks, which have the market worried.

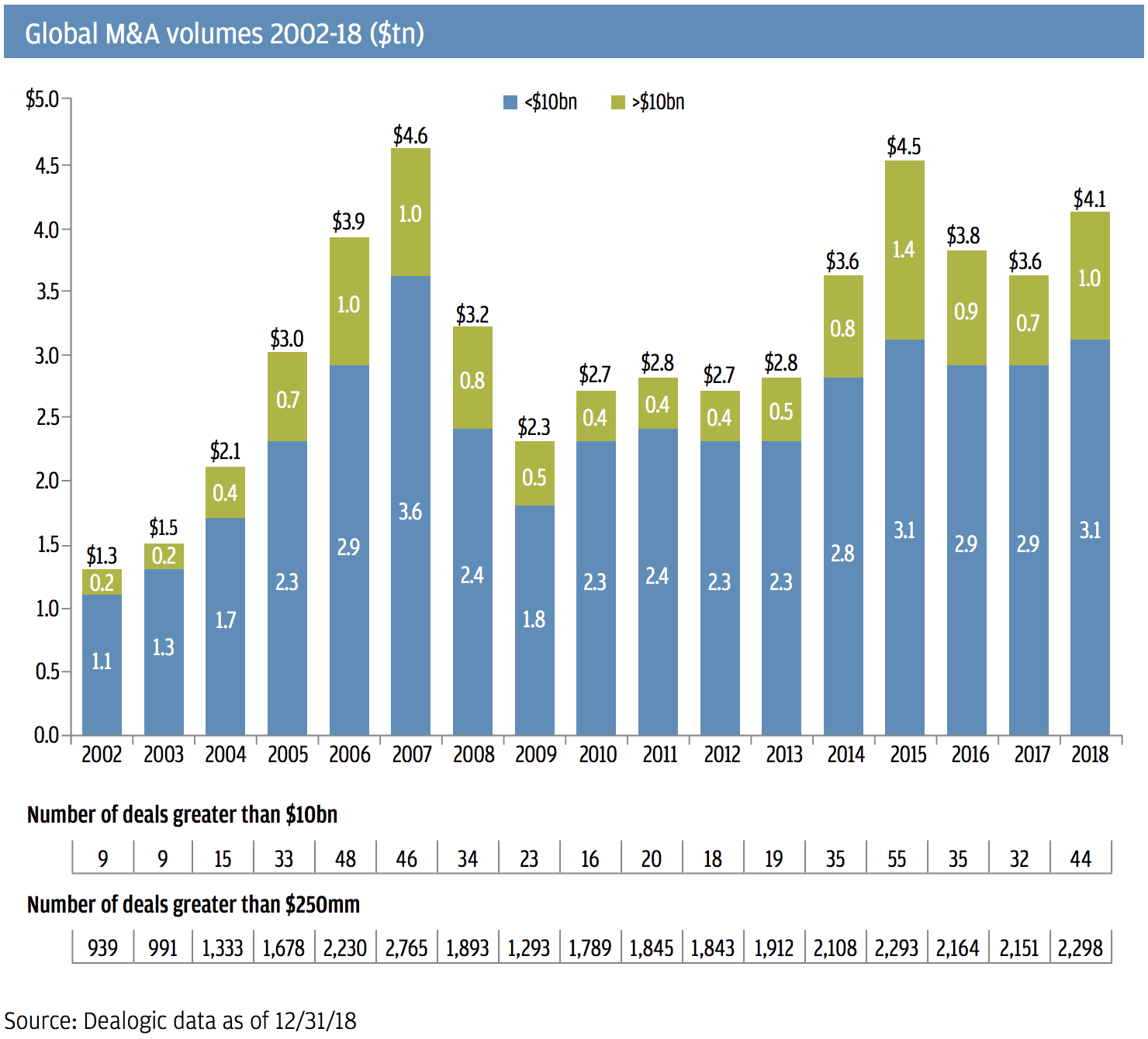

Most notably, Lazard's short-term results are tied to the health of global financial markets. For example, M&A activity is driven by global economic growth, rising corporate profits, CEO confidence, and cheap access to capital. During the financial crisis, when those factors moved the wrong way, global M&A volume was cut in half from 2007 through 2009.

Source: JPMorgan Chase

Lazard's advisory revenue depends on the volume and value of the transactions it completes. The firm has a large restructuring business which performs better during periods of economic weakness, but it's not enough to offset lower M&A activity. The firm's financial advisory revenue fell from $1.2 billion in 2007 to $990 million in 2009, a decline of 20%.

Asset managers also get pounded during financial market downturns. Falling asset prices reduce their assets under management and thus their fees. Some investors also withdraw funds from asset managers due to uncertainty or volatility in the market, further reducing investment advisory fees. During the financial crisis, Lazard's asset management business declined from $717 million in 2007 revenue to $596 million in 2009, a 16% fall.

Source: Lazard Investor Presentation

The asset management industry also faces headwinds from the rise of low-cost index investing, which continues taking share from active managers. Lazard is purely an active manager. Although its average fee of 48 basis points is on the lower side for an actively managed fund, it's still much higher than the 0.11%average fee for passive U.S. equity funds, according to data from Morningstar.

Lazard doesn't disclose performance data for its investment funds, so it's hard to keep tabs on whether or not they are earning their fees. However, the firm reported net outflows totaling about 2% of its beginning assets under management in both 2018 and the first half of 2019. Clients have withdrawn more funds than they've been adding, suggesting some performance dissatisfaction.

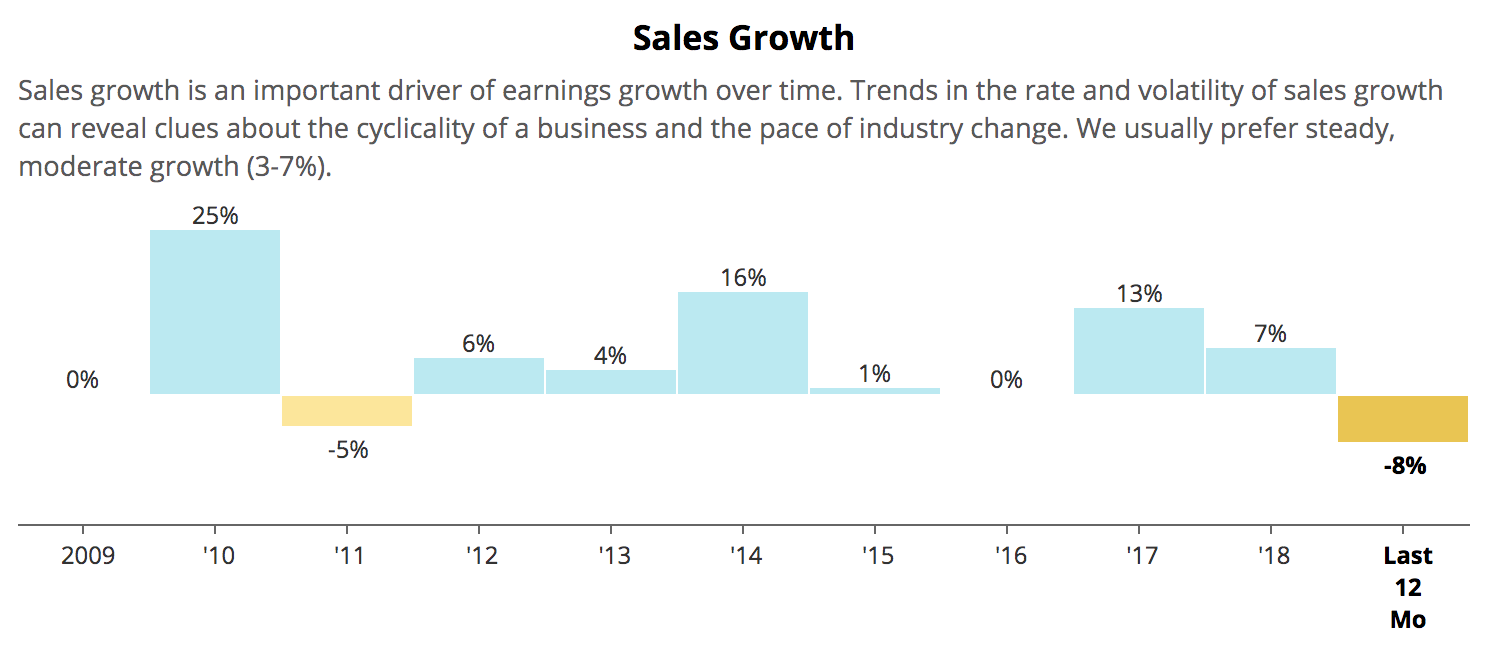

Long-term growth concerns aside, Lazard's weak stock performance and high yield most likely signal that investors expect a cyclical downturn sooner rather than later. Lazard's sales growth is notoriously lumpy due to its ties to financial market conditions, but the firm's 8% decline over the last year still sticks out.

Source: Simply Safe Dividends

Lazard's revenue and earnings fell 15% and 34%, respectively, in the second quarter of 2019. Financial advisory sales slumped 21% due to softness in European M&A and global restructurings. Asset management revenue declined 12% and is expected to remain under pressure in the near term due to continued net outflows triggered by institutional investors rebalancing and derisking their portfolios.

What does this mean for Lazard's dividend? For now, the firm's payout appears to remain safe. However, dividend growth will likely slow to a low single-digit pace, and management probably favors share repurchases over special dividends based on the stock's current valuation.

Based on analysts' estimates, Lazard's earnings payout ratio is expected to hover near 50% over the next year, a reasonable level. The company's balance sheet is solid as well, earning a strong investment grade credit rating from Standard & Poor's. At the end of June Lazard also held $919 million in cash, more than four times the amount of its annual dividend commitment (about $210 million).

Simply put, Lazard's dividend looks well protected today. However, the firm's Borderline Safe rating reflects the long-term view our Dividend Safety Scores take when gauging risk. With Lazard, the big question is what happens during the next recession.

Since the financial crisis, Lazard's earnings have nearly doubled. However, its dividend per share has nearly quadrupled, pushing its payout ratio up to 50% today in an environment where financial market conditions are favorable. If Lazard's profits get cut in half during the next downturn (operating cash flow fell 52% in 2009), then the firm's payout ratio will approach 100%.

Management has wisely maintained a solid balance sheet to help Lazard weather difficult times, but there appears to be less margin for error. In a prolonged downturn with limited visibility, it's hard to say how long the company would choose to operate with a very high payout ratio. Lazard's cyclical business model makes it a more difficult dividend stock to hold, especially for risk averse income investors.

Besides its cyclicality, Lazard's business also has some client concentration risk. The firm's ten largest advisory clients accounted for 19% of its Financial Advisory segment revenue in 2018. Similarly, its top ten asset management clients accounted for 26% of its total assets under management.

While no single client accounts for more than 10% of Lazard's total revenue, during the next downturn it's possible that several large customers will cease their strategic activities that required Lazard's guidance or pull the plug on the firm's investment services to derisk their portfolios. In other words, parts of Lazard's business can melt quickly during downturns.

These aren't necessarily reasons to avoid the stock if you're comfortable with the firm's risk profile. Lazard has been in business a long time, and the services it provides are timeless in nature (even as asset management evolves). However, if your goal is to own companies that perform well during recessions, have low volatility, and appear to have very safe dividends over a full economic cycle, then Lazard is probably not for you.

Investors involved with the stock should also be aware that Lazard, which is a Bermuda corporation, has a partnership structure for U.S. tax purposes. The firm issues a K-1 form for dividends, though it generates no Unrelated Business Taxable Income (UBTI) and is therefore appropriate to hold in tax-exempt accounts.