Why Phillips 66's High Yield Continues to Look Safe

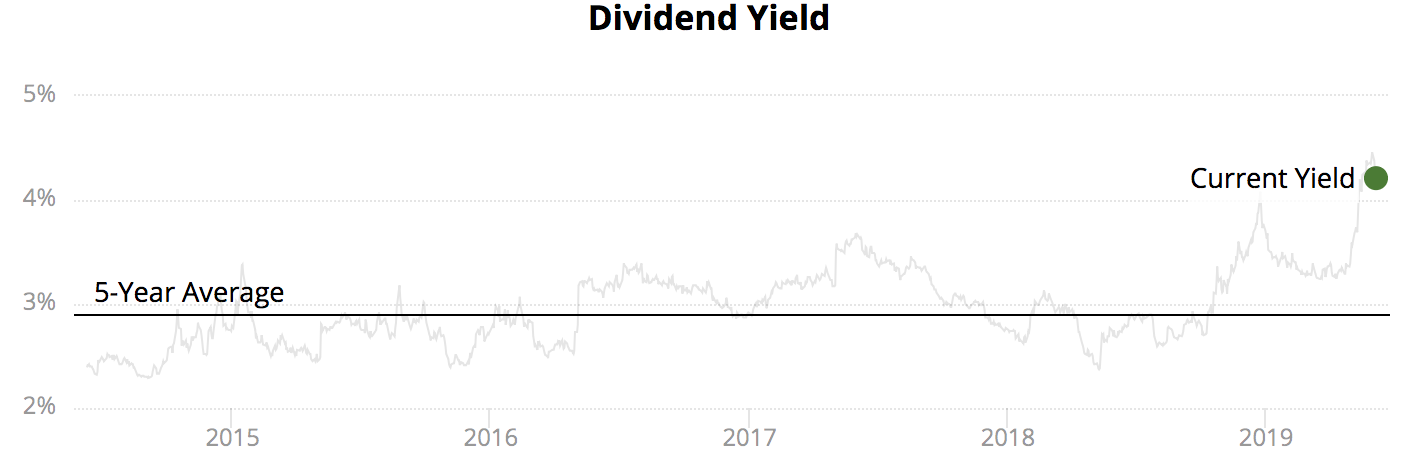

Phillips 66 (PSX) shares are down about 30% since their mid-2018 high. As a result, the stock's dividend yield now exceeds 4%, the highest level since Phillips 66 was spun off from ConocoPhillips (COP) in 2012.

Source: Simply Safe Dividends

Let's take a closer look at why the market has become pessimistic about Phillips 66 and assess why the stock appears to remain a reasonable income option for certain dividend investors to consider.

Why Phillips 66's Stock Has Slumped Phillips 66 is a diversified petrochemical company with operations spanning refining, chemical manufacturing, midstream services, and gas stations. While some of these businesses generate stable cash flow, others are much more cyclical.

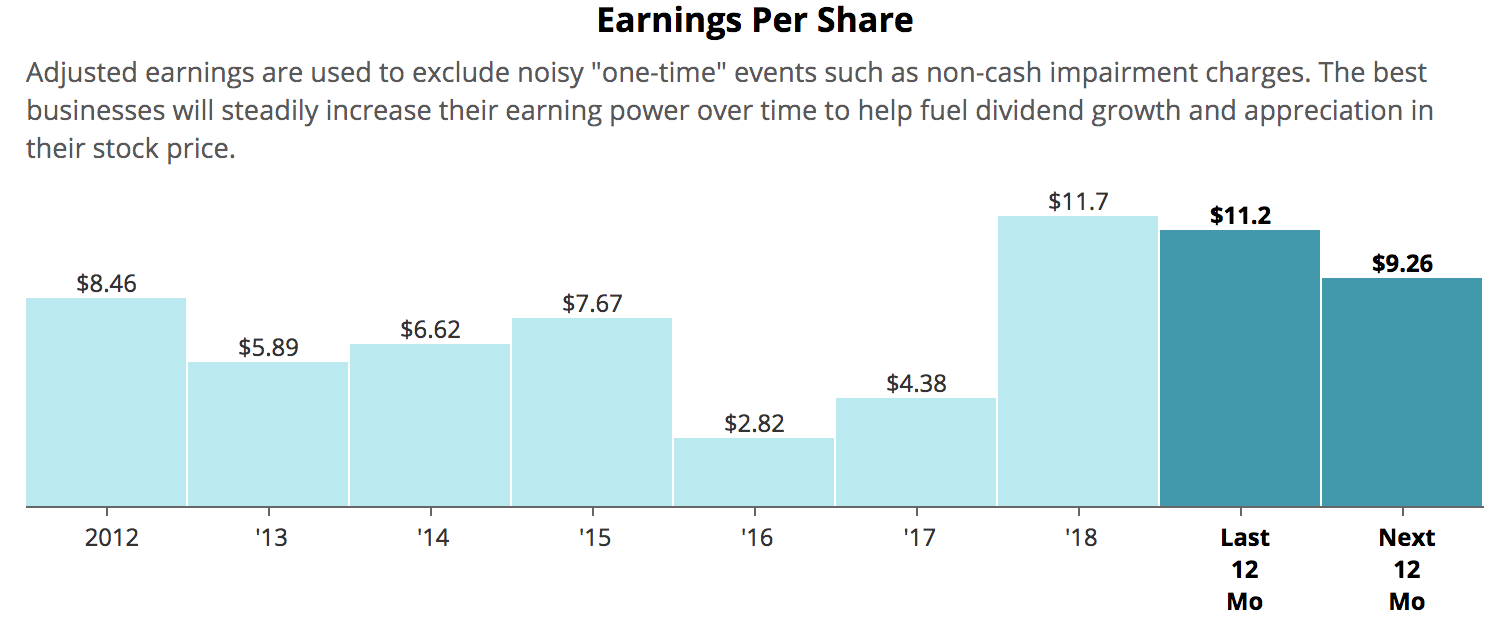

As a result, the firm's adjusted earnings per share nearly tripled in 2018, but now analysts expect profits to decline by approximately 17% over the next 12 months. In other words, investors appear to believe Phillips 66's earnings have already hit a short-term cyclical peak, and results could continue getting worse before they get better.

Source: Simply Safe Dividends

The company's refining business is driving the earnings decline. While Phillips 66 is one of the more diversified independent refiners in America, refining still dominates its pre-tax income:

Refining: 61% of 2018 pre-tax income

Marketing (over 9,000 global gas stations): 21%

Midstream (storage, transportation, and exports): 16%

Chemicals: 14%

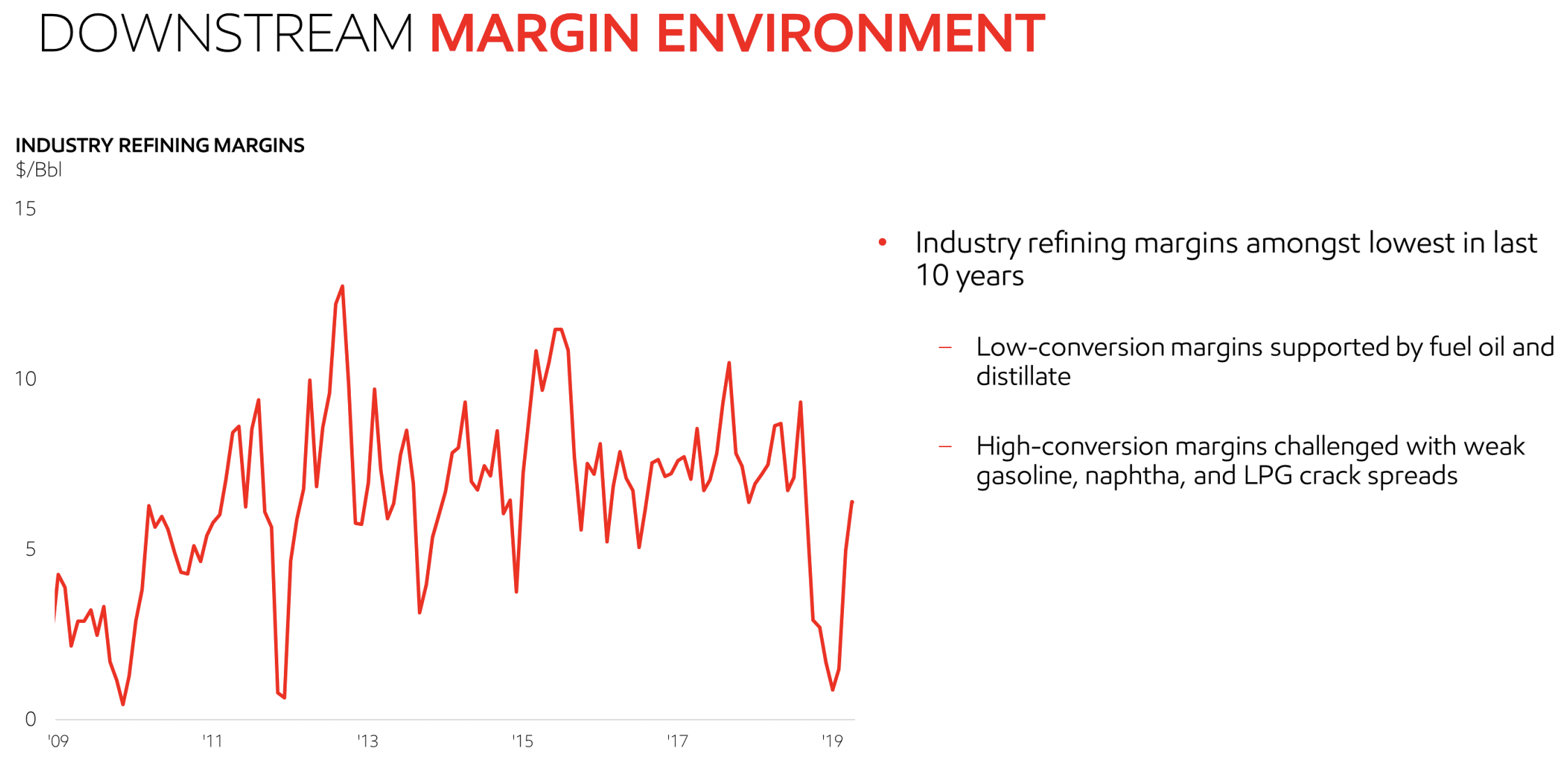

Unfortunately, industry-wide pressure is causing refining margins to fall to some of their lowest levels in 10 years.

Source: Exxon Mobil Investor Presentation

Phillips 66's CEO Greg Garland explained to analysts on the firm's first-quarter 2019 earnings call that last quarter's results were the result of a perfect storm of negative factors:

"Depressed gasoline margins and narrow heavy crude differentials significantly impacted our refining results. Refining operated at 84% capacity utilization, reflecting turnarounds at 5 refineries. We are also impacted by a higher than normal unplanned downtime... We are experiencing cost pressures from higher steel prices and labor rates."

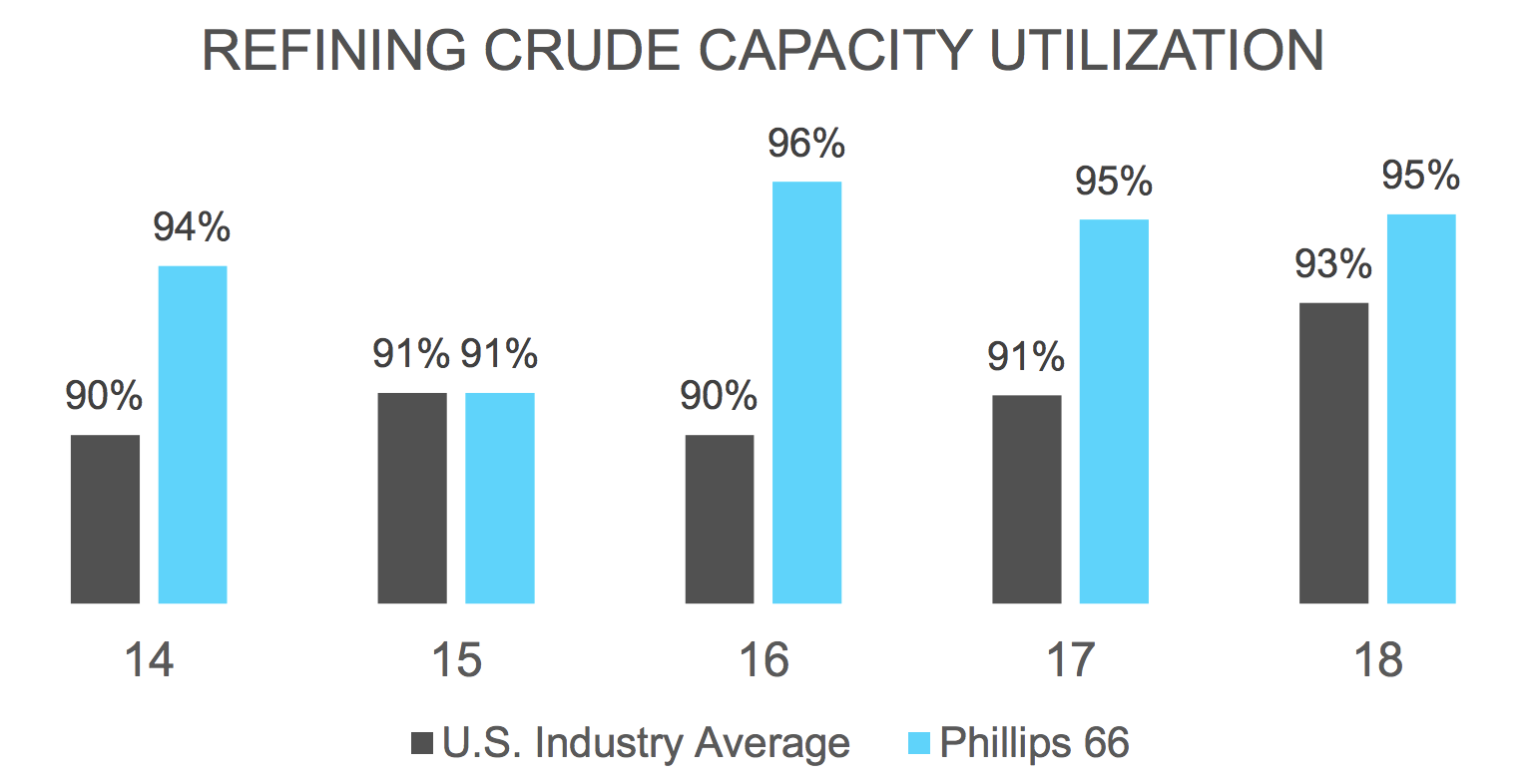

The company's utilization rate across its refineries fell from 99% in the fourth quarter of 2018 to just 84% in the first quarter of 2019, accounting for nearly half of Phillips 66's earnings decline.

Lower utilization caused a sharp drop in profits because high fixed costs at the firm's refineries mean that margins are heavily dependent on production volumes. However, refiners like Phillips 66 typically perform maintenance in winter months in order to be prepared for higher demand during the summer driving season (crude oil is refined into gasoline and other fuels).

Last quarter about 8% of the company's capacity experienced downtime due to routine maintenance, but another 6% of capacity was hit by unplanned downtime. Fortunately, the firm's CFO has confirmed those refineries are back on-line.

Phillips 66's historical refining utilization rate has consistently been at or above industry averages. In other words, this quarter's unexpected downturn (three times more than what the firm normally plans for) isn't an indication of deeper troubles at the company.

Instead, the company's earnings slump appears seasonal and due to one-time events, and not permanent.

Source: Phillips 66 Investor Presentation

Utilization rates are just one part of the profitability equation for refiners. An equally important component is the the crack spread, which measures the difference between the purchase price of crude oil and the selling price of finished products (e.g. gasoline).

This spread is less certain since in recent years refiners have benefitted from the rapid growth of low-cost Canadian and U.S. shale oil which has outpaced takeaway capacity. As a result, domestic refiners enjoyed low costs and higher margins.

However, in commodity markets, high prices often cure high prices. More takeaway capacity is becoming available to move shale oil to new areas of demand, and refiners have also cranked up production levels to take advantage of the wide crack spreads.

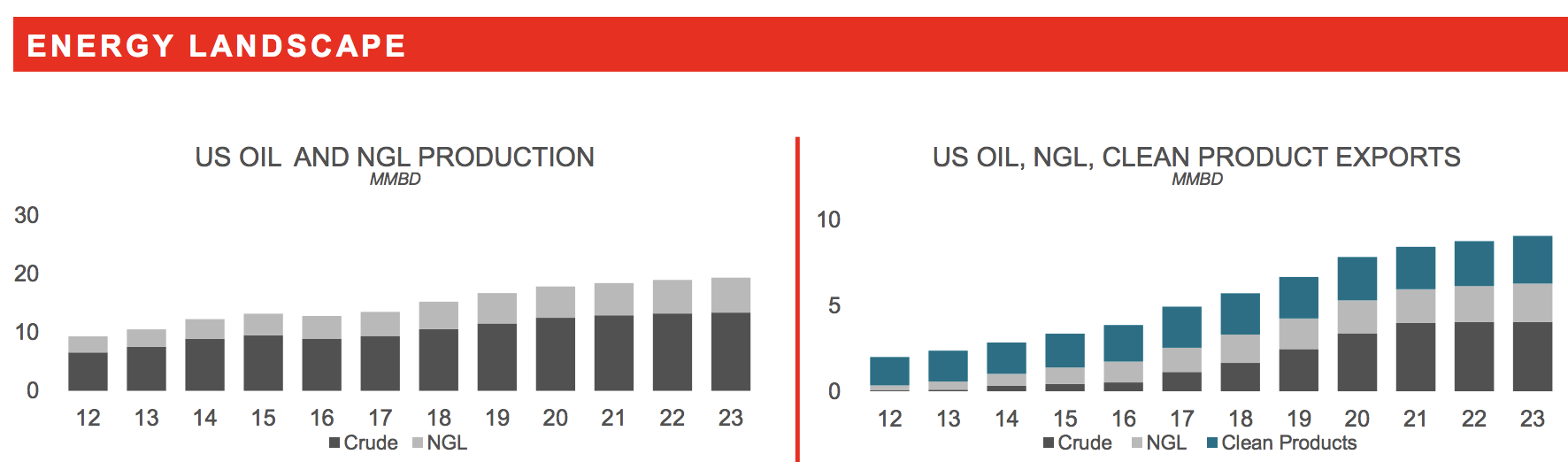

While long-term crack spreads will always be somewhat uncertain (driven by supply and demand for crude oil and refined products), the company is working hard to diversify into higher-margin petrochemicals and stable midstream infrastructure.

These areas have the greatest potential to capitalize on America's boom in oil and gas production, which most analysts and the U.S. Energy Information Administration believe will continue for many years or even decades.

Source: Phillips 66 Investor Presentation

Higher domestic energy production is expected to be needed to meet rising demand from higher-cost overseas markets. Growth in emerging economies, plus Japan and the European Union, is likely to benefit U.S. energy exporters.

Similarly, ethylene, a petrochemical used primarily to make plastics, can be manufactured at cheaper costs on the U.S. Gulf Coast, thanks to fast growth in low-cost ethane production in the Permian Basin.

Phillips 66 plans to vertically integrate its business model to be able to profit from these favorable secular trends.

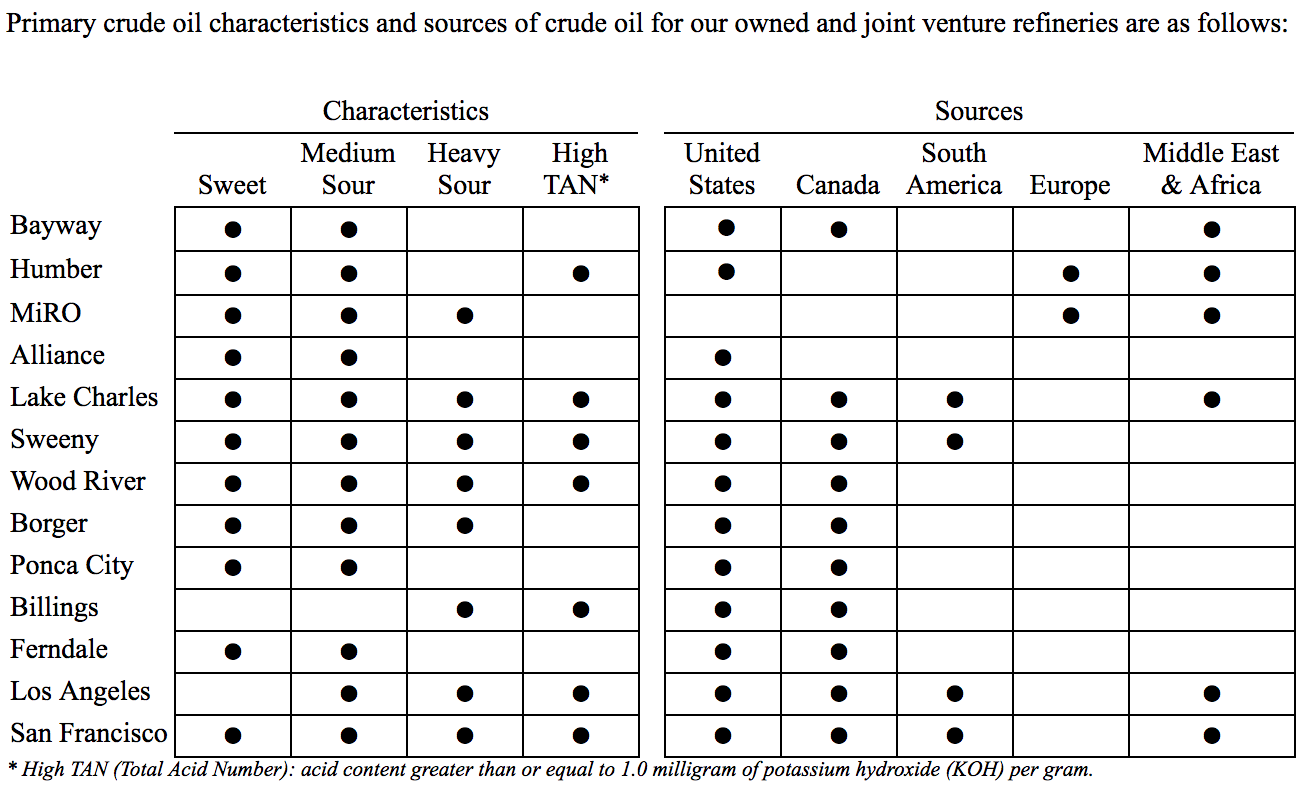

But despite management's long-term ambitions, Phillips 66 shares also came under pressure earlier this month following America's threat to impose tariffs on all goods from Mexico starting June 10.

While a deal was reached before these tariffs were set to go into effect, they would have hurt the short-term profitability of many American refiners. Mexico is the second-largest foreign source of oil to the U.S. and produces heavy oil that gets blended into gasoline and other fuels. Refiners would have to pay higher prices for their oil or find other sources of supply.

America's global trade relationships could remain dynamic, but fortunately Phillips 66 has diverse operations and input sources. As you can see, the company's 13 refineries have a very low reliance on Mexico and are generally able to process numerous types of oil (sweet, sour, etc.). This helps minimize the long-term impact of both unfavorable crude oil differentials and any future tariff issues.

Source: Phillips 66 10-K

Overall, the stock's weak performance over this past year appears to be driven by cyclical weakness in the refining industry, which is coming off a strong 2018. With PSX sporting an unusual high dividend yield, let's take a look at its safety and growth profile.

Phillips 66's Dividend Profile Remains Solid While Phillips 66's business is cyclical and largely at the mercy of commodity prices, the company has grown its dividend every year since it was spun off from ConocoPhillips. And on May 8, the company raised its dividend another 12.5%, indicating it has confidence in its long-term outlook for cash flow growth.

The recent payout hike is part of the company's long-term plan to return about half of operating cash flow to shareholders via buybacks and dividends while retaining enough cash to continue growing the business. Since its 2012 spin-off, the company has grown its dividend at a 25% compounded annual rate.

Despite over half a decade of double-digit dividend growth, Phillips 66's payout ratio, both on an earnings and free cash flow basis, continues to be at safe levels for this industry. Based on analyst estimates, the firm's earnings payout ratio is expected to sit near 40% over the next year.

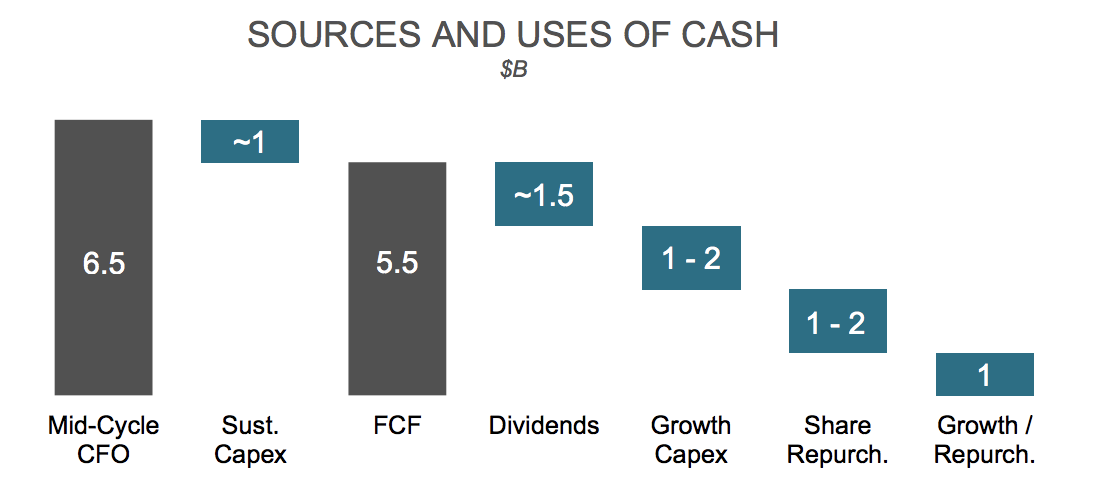

Meanwhile, using mid-cycle cash flow from operations, management expects the business to generate about $5.5 billion in free cash flow. Dividends are projected to consume just $1.5 billion of that figure, representing a free cash flow payout ratio of approximately 27% and leaving several billion dollars of retained cash flow that can be used for growth in chemicals and midstream.

Source: Phillips 66 Investor Presentation

Phillips 66 also does a nice job maintaining a conservative balance sheet to help it navigate through inevitable downturns in this highly capital intensive industry.

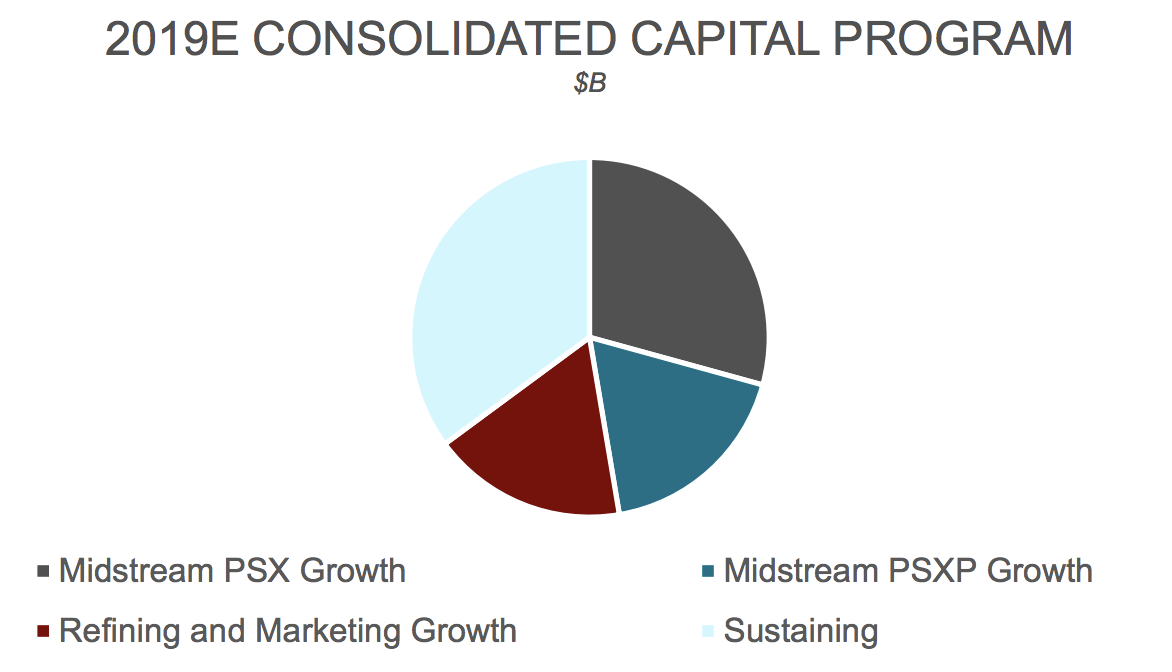

The company's leverage ratio has improved significantly in recent years and earns Phillips 66 a solid investment grade BBB+ credit rating from Standard & Poor's. In May 2019, Phillips 66 also had $6.3 billion in total liquidity to fund its growth plans, and $7.2 billion including its MLPs, a 50% stake in DCP Midstream (DCP) and 56% ownership of Phillips 66 Partners (PSXP).

DCP Midstream already has a self-funded business model, and Phillips 66 Partners continues enjoying access to relatively low-cost capital for its growth projects thanks to its BBB investment grade credit rating from Standard & Poor's. You can also see that Phillips 66's capital spending is not overly dependent on PSXP's budget either.

Source: Phillips 66 Investor Presentation

In essence, neither Phillips 66's payout ratio nor debt levels appear to put the firm's dividend in jeopardy, and the business has good financial flexibility in case a prolonged industry downturn occurs.

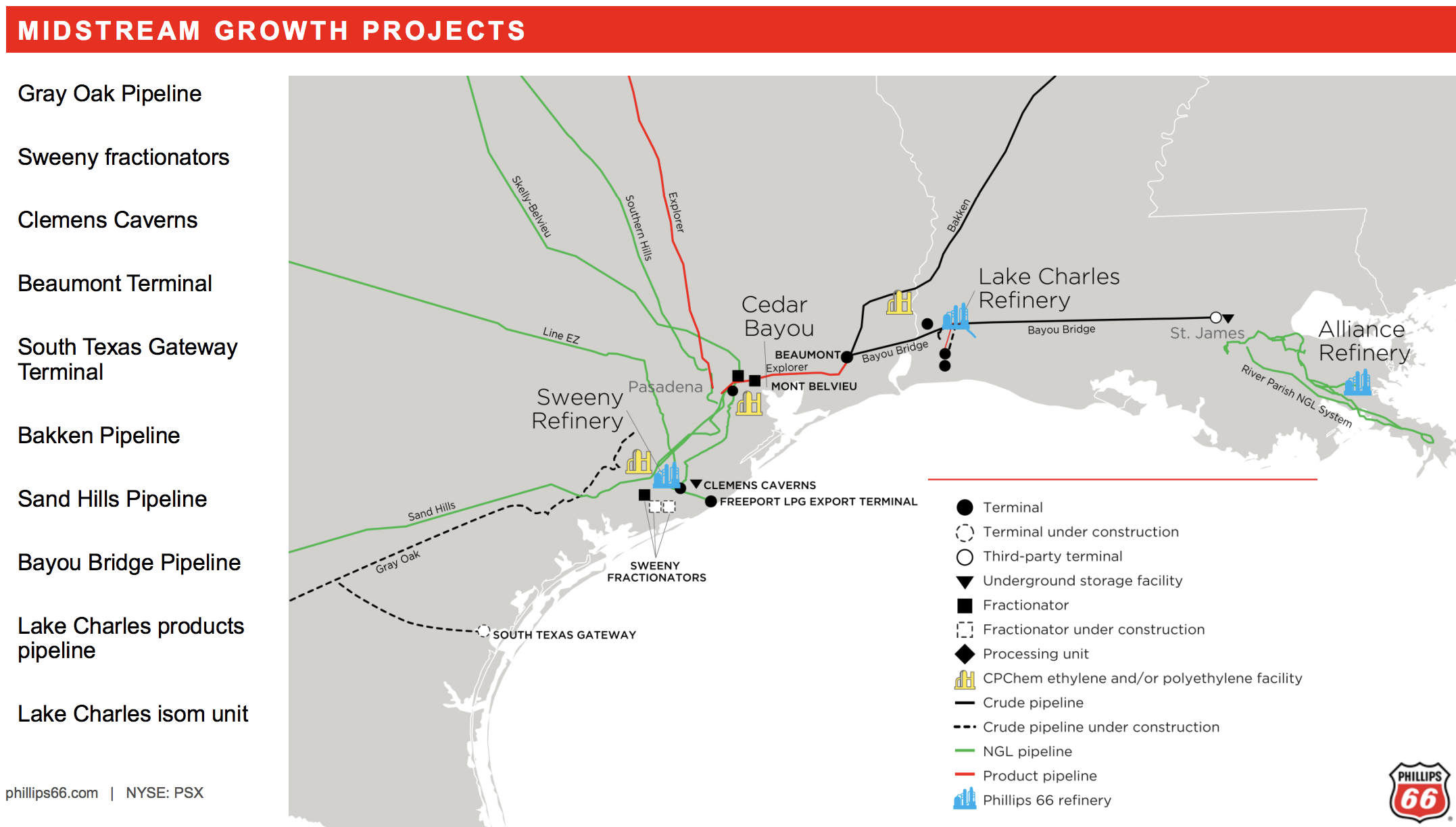

From a long-term growth perspective, not much has changed either. Phillips 66 is one of the more diversified refiners, with its core refining augmented by its CPChemical business and midstream operations.

Source: Phillips 66 Investor Presentation

Phillips 66's chemical business accounted for 14% of its pre-tax income in 2018. CPChem is a 50% joint venture with Chevron (CVX) and benefits from having 80% of its capacity served by low-cost input sources in the middle of America. The company hopes to more than double its exports of refined chemical products in the coming years.

Phillips 66 also has a large midstream business (16% of pre-tax income in 2018) thanks to its stakes in DCP Midstream and Phillips 66 Partners. DCP Midstream is specialized for NGL processing, storage, and transportation, while Phillips 66 Partners is designed to help fund the company's midstream expansion plans.

The company and Phillips 66 Partners plan to invest about $2.9 billion in capital expenditures this year, with over half of that spending targeted at the midstream side of the business. A big focus is on serving export capacity on the Gulf Coast.

Phillips 66, both directly and through its MLPs, has 10 midstream projects in the works, eight of which are expected to be completed by the end of 2020 and deliver about 15% EBITDA margins. That cash flow will be under long-term contracts, creating a more stable stream of income than the firm's core refining business.

Source: Phillips 66 Investor Presentation

Basically, Phillips 66 remains one of the more diversified independent refiners and appears to be in a solid financial position to maintain and continue growing its dividend in the coming years.

The company's recent weakness appears to be driven by temporary factors (unplanned downtime at refineries, volatile crack spreads) that could always get worse but ultimately seem unlikely to threaten the long-term outlook. Concluding Thoughts Any investor owning refiners needs to be comfortable with the seasonal and highly cyclical nature of earnings and cash flow in this industry. As we saw in the first quarter of 2019, unpredictable oil price differentials, when combined with both planned and unplanned downtime at refineries, can result in a significant short-term decrease in profitability.

However, as far as refiners go, Phillips 66's diversified model, which is focused on investing in higher margin petrochemicals and more stable midstream operations, appears to be a sound long-term strategy for delivering increasingly stable cash flow growth in the future.

With Phillips 66's dividend yield sitting at unusually high levels, income investors who are comfortable with the volatility of the firm's short-term results and share price might consider giving the stock a closer look.